Dear Reader,

Thank you for requesting your copy of my latest special report, Indestructible Income: 5 Bargain Funds With Steady 10% Dividends.

In addition to your free report, I’ve also arranged for you to receive a complimentary subscription to the Contrarian Outlook email newsletter.

Every weekday, you’ll receive our unique “second-level” analysis on dividend payers and growers to help you maximize your portfolio’s current yield and upside, even in this uncertain market. Look for your first issue soon.

In the meantime, enjoy your free special report below.

Yours in payout profits,

Michael Foster

Investment Strategist

CEF Insider

Michael Foster, Investment Strategist

In this exclusive special report, I’m going to show you something most investors think is impossible: five funds that hand you an average dividend more than nine times bigger than the weak 1.1% payout you get from the typical S&P 500 stock.

All five also trade at attractive valuations now. So if we grab these five low-key investments today, we’ll quietly collect their incredible cash dividends while we watch their prices spike, too!

These five funds all have something else in common: they’re all actively managed funds called closed-end funds (CEFs). I’ll have more to say about CEFs—and reveal the names of my “fabulous five”—in a moment.

First, if you saw the phrase “actively managed” and immediately thought “high fees, low returns,” you need to hear what I have to say next:

You’ve probably heard a lot of folks in the media tout low-fee index funds as the best way to invest in stocks.

It makes sense—these funds, which are managed by no one and simply track a “dumb” index, charge you lower management fees than managed funds, so your profits should be higher, right?

Wrong.

This is bad advice, for three reasons.

- With municipal- and corporate-bond funds, passive funds massively underperform those with a real human manager, and that gap is huge.

- Some of the best actively managed stock funds have outperformed the S&P 500 for a decade or longer—and they’re still winning.

- What about cash flow? Maybe a 1.1% dividend is all right for you, but what if it isn’t? Do you want to be stuck selling part of your portfolio to meet your income goals, even in a bear market?

These are just a few reasons why we need to choose the best-performing funds on the planet. But instead of obsessing over saving a fraction of a percent in annual fees, let’s look past the herd’s fee phobia and simply zero in on funds that have a history of outperforming the market.

And that’s where closed-end funds come in.

Everybody knows about mutual funds—closed-end funds’ “open-end” cousins. So what’s the difference between “open-end” and “closed-end” funds?

Simple: a CEF is “closed” in one specific way—it typically can’t issue new shares to new investors. That’s different from an open-end fund, which can issue new shares at will.

That matters because it means shares of CEFs are much more dialed into market demand. It also means there can be a big disconnect between the fund’s net asset value (NAV, or the value of the actual holdings in its portfolio) and its market price.

Stick with me for just a moment more because this is where our opportunity lies—including our shot at big, safe CEF dividends—especially through the five powerhouse funds I’ll reveal at the end of this report.

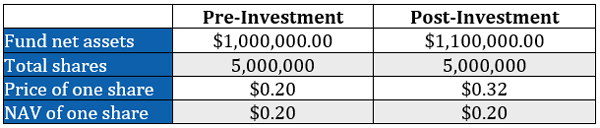

Let’s say a closed-end fund has $1 million in assets and five million shares. That means the fund starts out the same way as a similar-sized open-end fund would, with each share worth $0.20.

Now let’s say an investor wants to invest $100,000 in the CEF. The investor can only get in if another shareholder sells to the new investor.

Already you can see a big difference between open-end and closed-end funds. With CEFs, management has a lot less power; instead, shareholders have a lot more power over whether to allow new capital into the fund or not.

It gets better.

Let’s say no one wants to sell to the new investor. In that case, the new investor needs to create an incentive to get those shareholders to sell. They won’t sell $0.20 of assets for $0.20? Okay—what if the investor offers $0.21 for every $0.20 of assets?

If that isn’t enough, the investor may want to go higher … and higher. Let’s imagine, for this example, that the investor is able to buy $100,000 in assets from three CEF shareholders at three different prices:

- Shareholder #1 sells $20,000 worth $0.25 per share.

- Shareholder #2 sells $50,000 worth $0.27 per share.

- Shareholder #3 sells $30,000 worth $0.32 per share.

After these transactions are completed, the new market price for the CEF is $0.32 per share—even though the NAV is still $0.20!

In other words, the CEF is trading at a 60% premium to its NAV. At the same time, the total number of shares in the fund has remained constant.

Keep in mind that a $500,000 nest egg gets you $4,167 per month, on average, in income with CEFs yielding 10%, which is the average payout on the five funds discussed below. That’s enough for many investors to either clock out of the workforce entirely or drastically scale back their working hours.

Most CEFs trade at discounts to NAV, which actually helps them sustain dividend payouts of 8% or more.

I know the connection between discounts and dividends might be tough to spot, so let me clear that up now.

Let’s say a CEF is trading at a 10% discount, as many regularly do, and yields 8% on its market price. But the fund’s managers are really only concerned with yield on NAV. And in that case, the fund would only need to yield 7.2% on its NAV—an easier target—to sustain its dividend payout.

This is what makes CEFs particularly attractive to income investors: you’re getting a higher and safer dividend than you can get with an ETF or a mutual fund.

And you choose how to use that income: You can reinvest your payouts, building your upside potential (and your income stream) as you do. Or you can use your CEFs’ outsized dividend streams to pay your bills, and possibly even retire early. It’s your call!

Keep in mind that a $500,000 nest egg gets you $4,167 per month in income with CEFs yielding 10%, which is the average payout on the five funds discussed below. That’s enough for many investors to either clock out of the workforce entirely or drastically scale back their working hours.

There’s another reason why CEFs are a better choice than mutual funds, and it comes down to two words: “crisis survival.”

Let me take you back to the market crash we experienced in March 2020 and put you in the shoes of a mutual fund manager at the height of the pullback. You see the market crashing, but you feel that it’s going to recover.

You see tons of investment opportunities you’d love to put money into … but you can’t.

Why? Because panicked investors are selling shares of your mutual fund left and right, and you’re being hit with a huge wave of redemptions that takes money out of the pool you can use to invest in that fire-sale market.

This happens every time the market heads south, and it’s a big reason why mutual funds underperform the S&P 500.

This never happens with CEFs.

It’s another hidden benefit of the fund’s “closed” structure: if investors want to exchange their shares for cash, they’ll have to sell them on the stock market. But that has zero effect on how many assets the fund is managing.

That means the fund does not have to sell assets during a panic—and the pros who manage CEFs go to work for investors like us, using their expertise to grab the bargains their research is telling them will snap back with a vengeance.

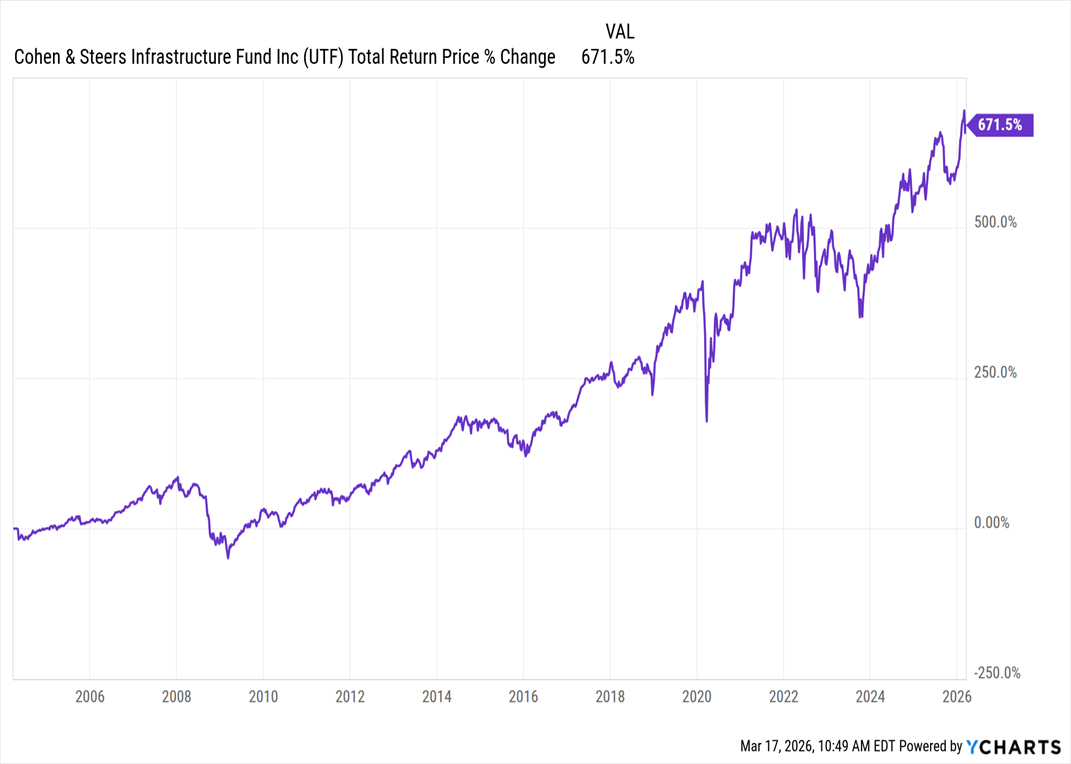

Just how powerful is that freedom? Let me show you an example using a fund whose savvy management team has done a terrific job of providing a strong return to investors who count on it for steady income.

The Cohen & Steers Infrastructure Fund (UTF) is a CEF that yields 7.2% and specializes in shares of utilities. You may know of utilities as a “widows and orphans” sector—a sleepy group of companies that yield a lot but return a little over the long term. Yet UTF has delivered well over a 600% return since inception, as of this writing.

But the real deal-clincher here is that essentially all of UTF’s return was in cash, thanks to its high yield. That’s something investors who buy utilities directly, or pretty well any ETF, simply can’t match.

That high yield means UTF investors are less likely to have to sell their shares to raise cash. That, in turn, means they don’t have to deal with the headaches, taxes and paperwork of juggling capital gains and income. They simply wait for their dividends to drop into their accounts.

And while UTF is one compelling play, given its historical returns, there are even higher yielding CEFs that are steeply discounted today that can drive your passive income even higher.

These five CEFs have impressive past returns and strong upside potential. The best part is the yield: buy all five now and you’re looking at an incredible 10% average payout!

That means, as I mentioned a second ago, that you can invest $500,000 and get $4,167 per month in income. With an S&P 500 index fund, you’re stuck with just $458 per month, as of this writing.

The other nice thing is that these 5 funds are diversified, including preferred stocks, real estate investment trusts (REITs), corporate bonds and utility stocks.

So let’s get to them, starting with …

The first fund I want to show you has three things all income investors crave: diversification, big dividends and prudent management. And it all comes from a respected source: Prudential, which manages the PGIM Global High Yield Fund (GHY).

Let’s start with diversification. As a global fund, GHY focuses its assets around the world while basing its portfolio in countries with the steadiest economies: The US, Canada and France account for just under half its assets. It complements those with high-growth regions like Mexico and Brazil, where its managers find particular value. And thanks to the higher yields in those parts of the world, GHY pays out a 10.6% dividend today.

That makes GHY a great play for income and diversification.

With wide fluctuations in currency markets, GHY has had a lot of opportunities to go in and out of bonds denominated in different currencies around the world. Plus, with Prudential’s global reach and client contacts, the fund’s managers can foresee those trends and invest accordingly.

With an 8% discount to NAV that has been steadily narrowing, this is a fund that’s likely not going to stay undervalued for long, and now is the time to grab it.

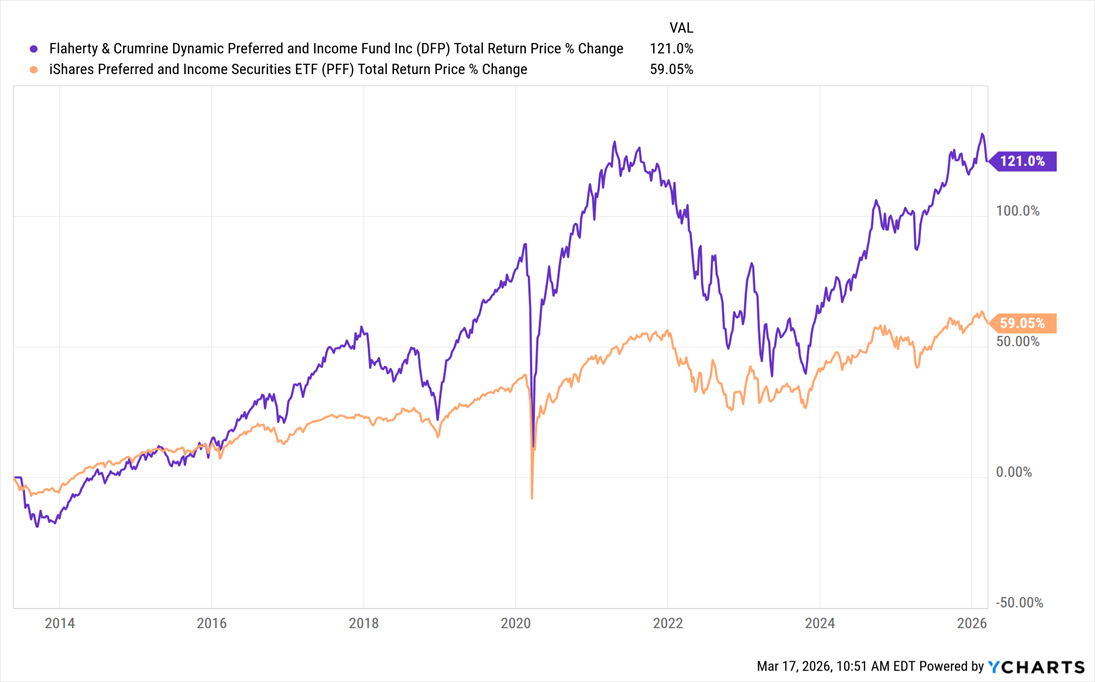

The Flaherty & Crumrine Dynamic Preferred and Income Fund (DFP) is managed by one of the savviest companies in the CEF game: Flaherty & Crumrine. Not only are they top-notch financial minds, but they also pay a healthy 7.3% dividend to DFP shareholders. And they’ve handily beaten their index, in this case represented by the iShares Preferred and Income Securities ETF (PFF), since its IPO.

DFP’s return—much more than that of the “dumb” preferred-stock index fund—gives it a lot of appeal. Plus its 7.3% dividend is a strong stream of income that isn’t too big as to be unreliable nor too small to be insignificant.

Moreover, the last few years’ rise in interest rates mean that payout is stable, since higher rates allowed management to “lock in” the higher yields available on preferreds today. This is one of those “set it and forget it” CEFs you could buy and hold for years.

A lot of retirees see real estate as a go-to for income. It just feels more “real” than stocks. Even if you don’t live in the house and instead rent it out for income, owning property means you can go and see your asset.

But America’s love affair with real estate has often been misguided. Landlords, of course, need to manage deadbeat tenants, vandalism, leaky faucets, sagging roofs, you name it. Renting out real estate is hardly the way to get “passive” income—landlords work hard for their money.

Fortunately, you can outsource all of that management and benefit from economies of scale by buying stocks in companies that rent out property. And when it comes to real estate investing, we want to be sure we’re going with a team that has a proven track record.

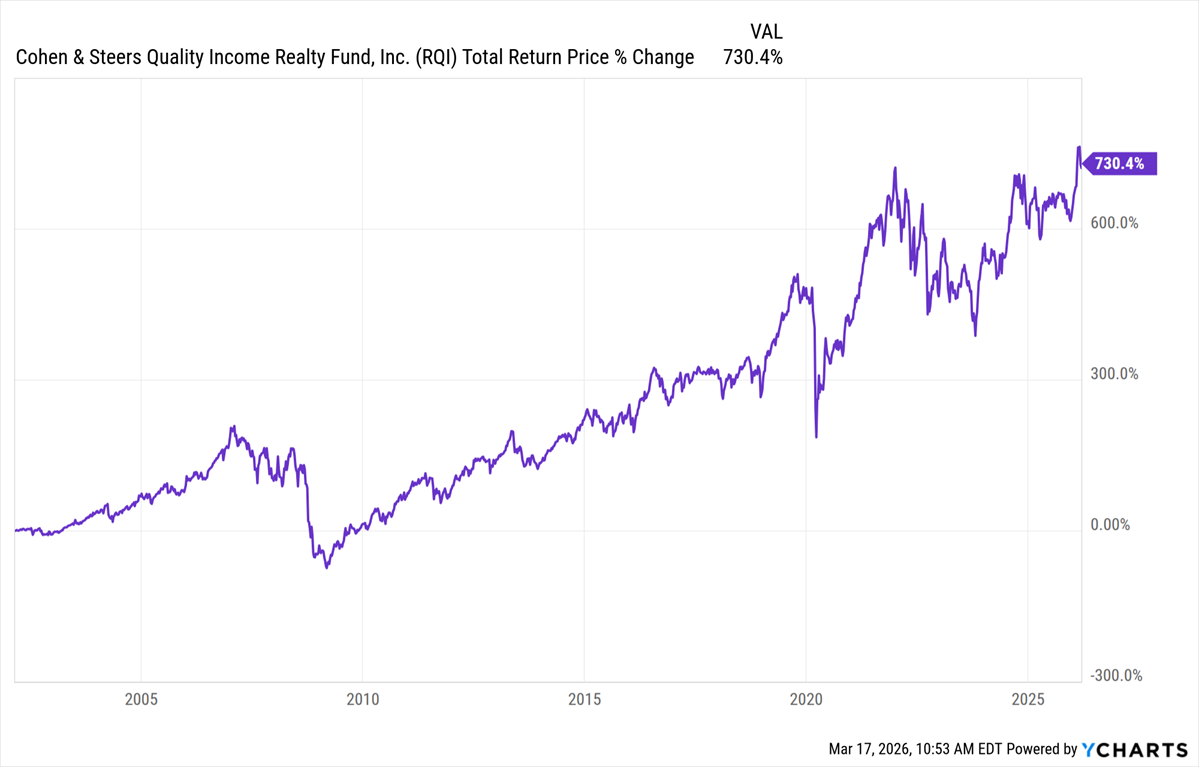

Enter the Cohen & Steers Quality Income Realty Fund (RQI), which has long been a solid option for investors looking for real estate exposure. Instead of buying property directly, or originating mortgages itself, RQI buys shares of REITs, companies that own real estate—everything from doctors’ offices to cell towers—and hands most of the rental income back to investors as dividends.

Individual REITs trade on the stock market, just like other publicly traded companies, and RQI is the best “one stop” shop to buy a collection of the best REITs out there, with the most desirable properties.

RQI also pays you a much higher dividend than you’d get by buying REITs yourself: a nice 8.7% income stream that now trades at a 2.2% discount. That’s net income on your investment. How many landlords do you know who are getting that level of profit after all expenses (repairs, taxes, mortgage, insurance, property managers, lost rent from vacancies, etc.)?

Thirdly, you are diversified over literally thousands of tenants. No need to worry about a vacancy—there are plenty of occupied units to make up for that!

Finally, RQI has performed well over the long term.

Looking ahead, REITs, particularly those in sectors like warehouses and data centers, which the AI sector cannot get enough of, will likely be able to continue to boost their rents and roll out profitable expansion plans. They’ll get a further boost as interest rates move lower in the longer term, cutting their borrowing costs.

If you want to invest in real estate without the hassle, RQI should be high on your list.

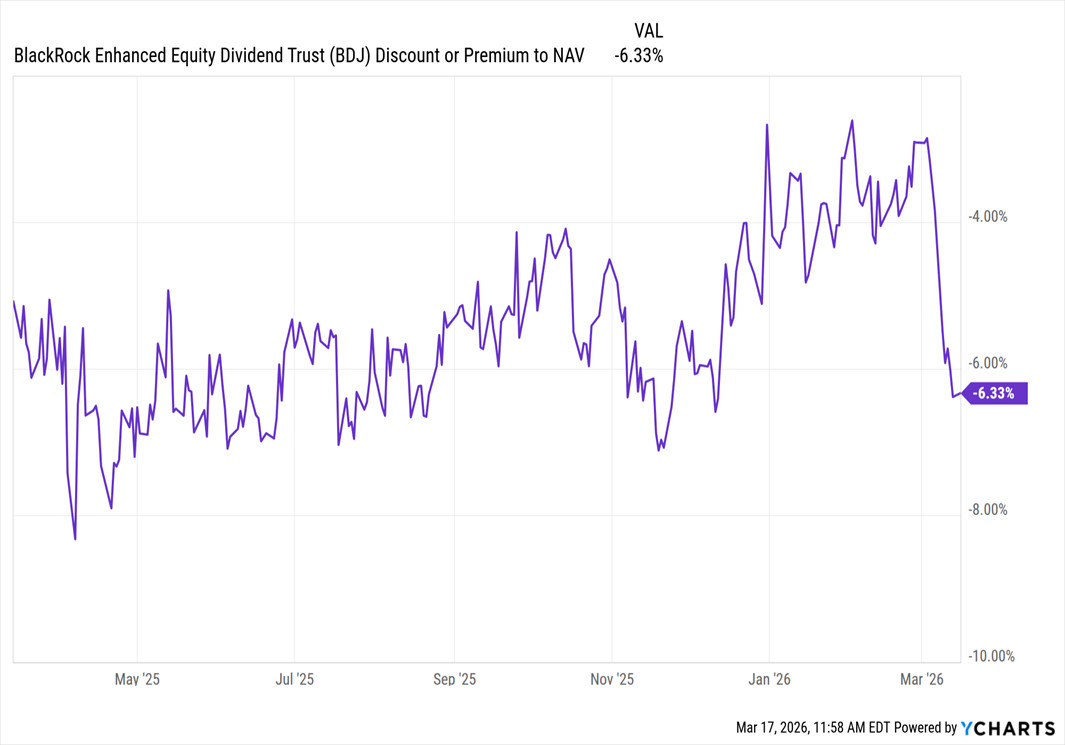

The BlackRock Value Dividend Trust (BDJ) is now trading at a 6.3% discount, as the fund’s markdown has suddenly widened after closing for a long time.

This kind of drop in CEF discounts often happens, regardless of a fund’s performance, as money flows into and out of these funds, often at the behest of wealth managers. That’s something we can take advantage of to grab a strong fund cheap.

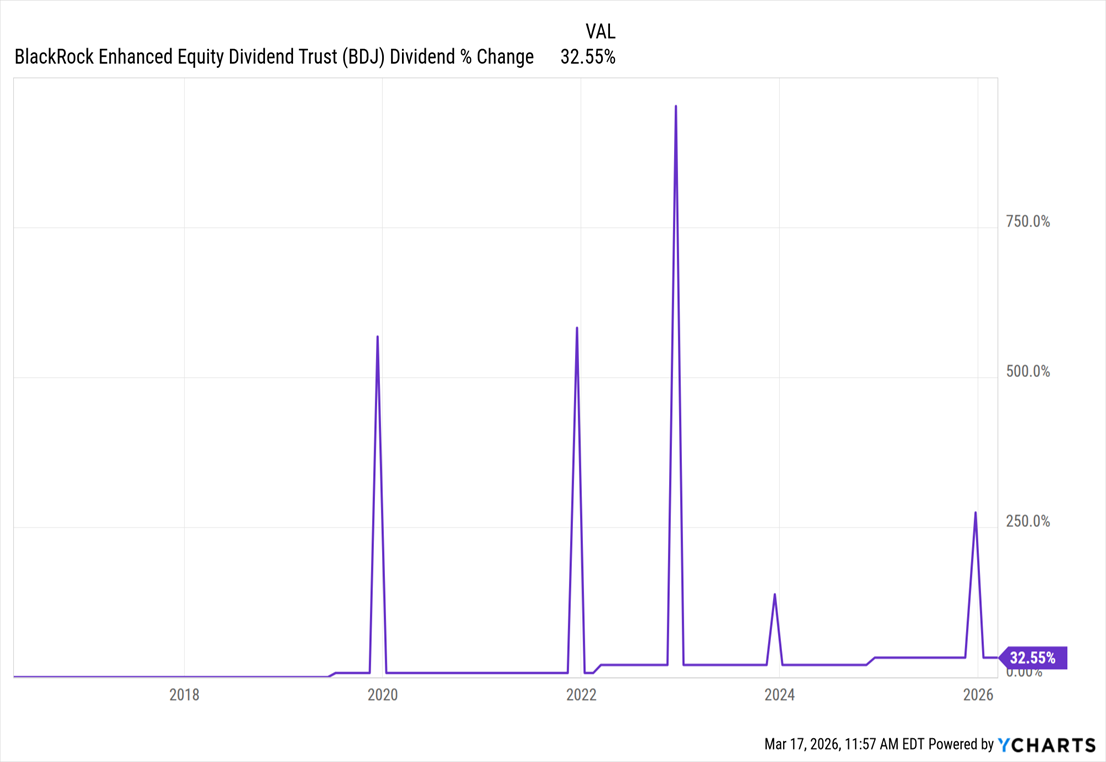

The main holdings of the fund, which yields 8.5% today, are big-cap US stocks, with Microsoft (MSFT), Amazon.com (AMZN) and Wells Fargo (WFC) as top picks. Another reason why the fund is trading at such a deep discount is the dividend.

Note the special dividends over the last few years, as well as the small increases in the regular payout. In all, though, BDJ has posted relatively meager payout growth over the last decade compared to some more-aggressive CEFs yielding 9% or more.

But notice the long-term trend of continually increasing payouts. Moreover, periods of higher market volatility make BDJ more profitable because the fund sells call options on its portfolio, and this strategy does well in choppy markets. As a result, BDJ has more income to pass over to shareholders.

That steadily (even if slowly) rising payout and BDJ’s habit of paying regular special dividends is slowly attracting more income investors. This, in turn, stands to whittle away the discount over the long term, making the current 6.3% discount a nice entry point.

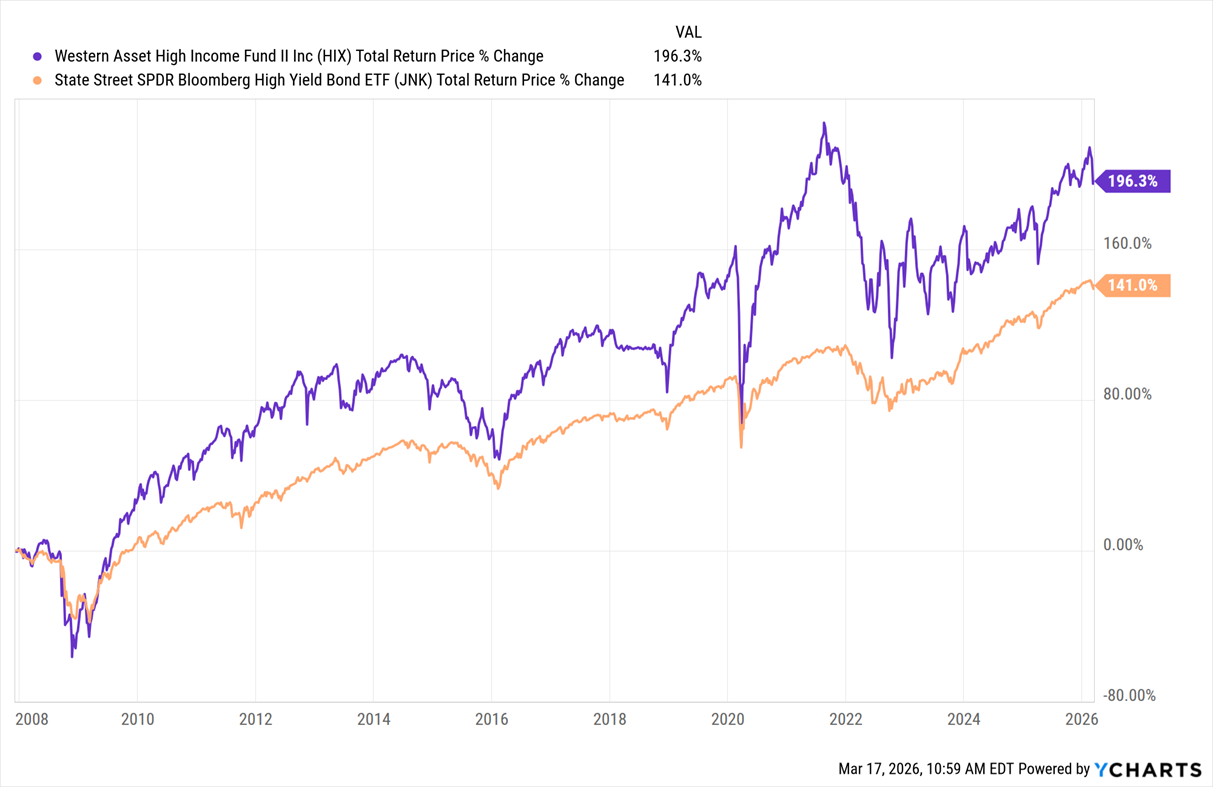

My final pick for you is a really misunderstood one: the 6.5%-discounted Western Asset High Income Fund II (HIX).

A lot of people are uncertain when it comes to bonds right now, as geopolitical flare-ups risk boosting costs in the US. But in the long run, inflation will come to heel, in part because AI is weighing on wage growth.

That makes now a good time to buy HIX, whose experienced management team has navigated (and profited during) many global crises in the past.

That’s in part because the team at the top has been carefully balancing their bond purchases to give themselves maximum flexibility, no matter what happens to interest rates. This, in turn, has helped HIX has been outperform (in purple below) outperform the corporate-bond index for years:

This is a fund you can buy now to lock in a hefty double-digit payout and nicely position yourself to sell at a profit later, after you’ve pocketed a stream of healthy dividends.

These 5 funds are a good first step toward secure, stable income and solid gains in the months ahead.

But to show you just how much the very best closed-ends can juice your returns, I’m going to take it one step further.

I want to share with you 4 of my absolute favorite CEF recommendations that are typically reserved exclusively for my premium readers.

These four funds are the “cream of the crop” when it comes to outsized discounts to NAV and safe high yields … the kind of funds that are perfectly set to bounce as their “coiled spring” discounts narrow to their usual levels.

My research indicates they’re perfectly positioned to do well no matter which way the broader market swings … regardless of what happens in Washington or beyond America’s borders … and irrespective of interest-rate trends.

Naturally, I’m hoping you’ll give me the opportunity to show you more big profit opportunities in the months ahead.

So, if you’re ready for a rare chance to profit from my exclusive premium recommendations, I’d like to send you three additional reports …

Free Bonus Report #1 (a $99 value)

The first is called “4 Great CEFs to Buy Now: 9.9% Yields and 20% Upside Ahead.”

Just like the title says, this off-the-radar “4-pack” boasts outsized upside AND huge dividends!

I’m especially excited about one high yielder, which throws off a rich 8.3% payout and trades at a 4% discount today.

That’s our cue, especially when you consider that the team at the top holds the top US blue chips and recently made a change to the dividend policy that makes the payout more reliable than ever.

It’s only a matter of time before the masses bid the silly discounts on this fund and my 3 other top picks into premium territory … propelling them to strong price gains as they do. PLUS we’ll be collecting these 4 funds’ outsized CASH dividends while we wait.

Free Bonus Report #2:

Your source for all things CEF, “The Ultimate Guide to CEFs” gives you everything you need to know to reap maximum profit from your own CEF picks, including:

- How CEFs can pay outsized dividend yields—and a simple way to make sure your fund’s payout is sustainable.

- The relationship between CEF performance and management fees (it’s not what you think!)

- The simple trick CEF managers regularly use to keep their funds’ discounts from getting too wide (this unique “insurance” simply doesn’t exist in stocks, bonds or ETFs).

- The surprising reason why the liquidation of a CEF is actually good news for investors.

This one-of-a-kind report is another $99 value—and it could easily save you thousands in future losses—but you can get it FREE today along with …

Free Bonus Report #3:

Your third guide is called “5 Toxic CEFs That Could Ruin Your Retirement.”

These 5 funds look attractive but contain hidden traps waiting to snap on the unwary, including:

- Outrageously high fees hidden deep in the fine print (in one case, management is snagging about a quarter of the fund’s investment income for itself!).

- Ridiculous valuations: One of these funds simply holds other CEFs , a dead-simple business model, yet it trades at a premium and charges a 2.8% management fee, too!

- Dangerous dividends, like the 20% yields two of these funds pay. But because these CEFs trade at absurd premiums, they’re at risk of a sharp drop that would be magnified by a (very probable) dividend cut.

These reports give you four rock-solid funds that pay handsomely while growing your portfolio … a complete roadmap to investing in closed-end funds … while also protecting you from some of the worst disasters in the CEF universe.

But there are two things those reports can’t give you—ongoing updates and all my FUTURE income recommendations.

That’s why, in addition to giving you these three reports—worth $297 on their own—I also want to give you a risk-free 60-day trial to my premium newsletter called CEF Insider.

My CEF Insider picks are perfect for savvy investors looking for strong cash dividends backed by smartly run funds that are overlooked by the mainstream crowd.

Right away, you’ll get access to many more discounted picks in the publication’s portfolio, plus all the new buys I uncover in the coming months.

I do all the digging for you, recommending only the safest CEFs and keeping you well clear of questionable funds that will crumble at the first hint of a downturn.

What’s more, I send out new recommendations whenever they’re worth buying, plus I give you regular updates on earlier recommendations … all in plain, everyday English.

Sounds great, right?

After all, who wouldn’t want potential double-digit gains from their dividend investments? Given that most people look to these holdings for income alone, this is basically free money!

Even so, CEF Insider isn’t for everyone.

It’s a unique service I’ve custom built for folks who want to go further than the average investor to get in on the very best CEFs for high, safe income and massive upside.

Because I’ve bulked it up with a set of wealth-building tools you simply won’t find anywhere else, starting with …

Our streamlined CEF Screener (recently fully revamped and upgraded by our in-house IT staff) lets you sort through the roughly 400 funds in the CEF universe worth your consideration at the click of a mouse.

Sort by ticker symbol, asset class or discount/premium to NAV and you’ll instantly see how each CEF stacks up to its peers.

This one-of-a-kind fund-picking tool is backed by a rigorous 6-point assessment that judges each CEF by its current and historical NAV, 10-year return, fees, yield on NAV (the best measure of dividend safety) and much more.

That’s not all. You also get our one-of-a-kind “CEF Insider Heat Map,” which instantly separates attractive funds (green) from dangerous pretenders (red).

It’s like having me personally guide you to the CEFs worth further consideration for your portfolio.

I’d normally charge $99 a month for access to the Screener alone—but you get it absolutely FREE when you try CEF Insider.

PLUS you also get…

Our easy-to-use CEF Index Tracker lets you instantly compare the performance of practically any CEF to any other CEF and stack up as many funds as you like to our proprietary CEF indexes.

The bottom line: At a glance, you can see which CEFs have outperformed (and may be overpriced) and which have underperformed (and may be screaming bargains)!

You won’t find another CEF tracker anywhere on the web—paid or free—that lets you do this, which is why I just added this revolutionary tool to your CEF Insider trial membership.

A $99-a-month value, you also get the Index Tracker FREE as part of your CEF Insider subscription.

Are Just the Start

In addition to the CEF Screener and your 3 reports with my very best picks for 9%+ income and double-digit upside, your risk-free trial contains a whole lot more, including:

- Your CEF Watch List: My “shortlist” builds on our CEF Screener by giving you the Top 20+ CEFs I’ve got my eye on—the ones I’ve handpicked and personally safety checked. Each one offers outsized yields and bigger-than-average discounts, so they’ve got plenty of built-in upside, too. But they don’t yet qualify for our…

- Members-Only Portfolio: These are the “best of the best”—my top CEF picks for high, safe income and big gains right now. All of them are laid out in an easy-to-read portfolio that includes my up-to-the minute recommendations, buy-under prices, current yields, discounts to NAV and much more.

- Monthly Issues: On the fourth Friday of each month, you’ll get my latest analysis of the ever-changing CEF space right in your inbox. I’ll include detailed analysis on new fund recommendations, updates on existing positions and an overview of trends and events that may affect your holdings.

- Weekly Analysis: I’ll email you every week with my latest investing ideas in CEFs I’ve been watching, plus analysis of major market events.

- Flash Alerts: You’ll never have to worry about missing out on breaking news on the CEFs in our portfolio. I’ll have an eye on all of them 24/7 and will email you right away if there’s ever any change in our position.

- Unlimited Access to the Members-Only Website: Day or night, you can log into our password-protected website, where you’ll find easy access to all of our resources, including the CEF Screener, Index Tracker, CEF Watch List and the full portfolio. You also get a complete archive of our monthly issues, special reports and Flash Alerts, so you can see how our recommendations have changed over time.

If you’ve read this far, I’m guessing you think these high-yield funds may be a good fit for your portfolio.

But I also understand that you may still be hesitant to try a new service, and I want you to be certain this is worth your time, so there’s one more thing I’d like to add…

I’m so confident you’ll profit from my research that I’m going to give you 60 days to try CEF Insider absolutely RISK-FREE.

Simply click here to start your Charter Membership today.

Download your special reports, read the latest issue, kick the tires on our CEF Screener and Index Tracker and start following one or two picks from the portfolio.

Then enjoy the next couple issues of CEF Insider, my weekly column and all the other benefits of your full Charter Membership.

If after nearly two months you don’t feel the advice has more than covered your cost, or if it’s just not right for you, simply let me know and I’ll issue a full refund of your membership fee. That’s 100% of your money back, no questions asked.

Plus you’re welcome to keep the FREE special reports as my thanks for trying the service out.

But I have to tell you something here. I’ve built CEF Insider for people who truly understand the explosive gains and double-digit yields these ignored funds offer.

So if you’re okay with trying a new way of investing …

… and you’re brave enough to move a little beyond the mainstream to goose your portfolio’s yield and add a double-digit capital gains pop in the coming year…

If that sounds like you…

Then taking me up on a risk-free road test of CEF Insider is a no-brainer!

Which brings me to my next point.

As I mentioned, CEF Insider is a totally unique service, so it’s vital that we keep our group small.

How small?

I’m only letting in 2,000 members to CEF Insider in total.

You read that right: just 2,000 people, and nearly 1,700 have already snagged spots!

So once we hit that 2,000-person limit, my publisher may force me to close the doors. If you try to sign up after that, your name will go on a waiting list, and you’ll only be able to get in when another member drops out.

I expect those remaining spots to go fast. Especially when folks see the eye-popping gains and outsized income we’re talking about here.

I don’t want you to miss out, which is why I’m urging you to start your no-obligation road test right now … while this is in front of you.

To recap, you get a full Charter Membership, with full access to our powerful CEF Screener (a $198 value), Index Tracker (a $198 value), the CEF Watch List, the complete CEF Insider portfolio and ALL of our premium research.

Plus you’ll also receive 3 FREE research reports (a $297 value), weekly email updates and alerts, and a full 60 days to decide if you like the service.

And it’s all completely RISK-FREE.

I don’t see how you can lose here, because I’m the one taking all the risk. All you have to do is click the button below to get started right now.

In the coming months, many investors will still be on the sidelines, wary of more political shenanigans in DC or an unexpected jump in inflation or a flare-up in the trade wars.

Meantime, our CEF Insider members will be quietly pocketing their huge CASH payouts and watching as their funds’ unusual discounts swing shut, putting a lift under their share prices. Don’t be left on the sidelines. Start your no-risk trial to CEF Insider now.

Yours in payout profits,

Michael Foster

Investment Strategist

CEF Insider

P.S. As soon as you join CEF Insider, you’ll have immediate access to our CEF Screener, Index Tracker, Watch List, the complete portfolio, your 3 special reports and your first issue. The 3 reports and two months’ access to the Screener and Tracker alone are worth $693, but they’re yours free as a new CEF Insider member.

P.P.S. The clock is ticking! Other investors are reading this invitation right now, too, and I expect our remaining seats to fill up fast.

You can’t afford to hold off on this one. Simply click on the button below. You have no risk and no obligation whatsoever.

Nothing in Contrarian Outlook is intended to be investment advice, nor does it represent the opinion of, counsel from, or recommendations by BNK Invest Inc. or any of its affiliates, subsidiaries or partners. None of the information contained herein constitutes a recommendation that any particular security, portfolio, transaction, or investment strategy is suitable for any specific person. All viewers agree that under no circumstances will BNK Invest, Inc,. its subsidiaries, partners, officers, employees, affiliates, or agents be held liable for any loss or damage caused by your reliance on information obtained. By visiting, using or viewing this site, you agree to the following Full Disclaimer & Terms of Use and Privacy Policy.