Fellow Investor,

Thank you for requesting your copy of my latest special report, 7 Great Dividend Growth Stocks for a Secure Retirement.

In addition to your free report, I’ve also arranged for you to receive a complimentary subscription to the Contrarian Outlook email newsletter. Inside it, you’ll receive my unique “second-level” analysis on dividend payers and growers so that you can maximize your portfolio’s current yield AND upside, even in this uncertain market. Look for your first issue soon.

In the meantime, enjoy your free special report below.

Yours in payout profits,

Brett Owens

Chief Investment Strategist

Hidden Yields

Brett Owens, Chief Investment Strategist

Today I’m going to show you seven under-the-radar companies growing their dividends by 10% or more annually. All of these stocks are poised to deliver secure double-digit gains in the years ahead, with upside potential of 100% or more.

But before we buy these issues, we need to make sure your portfolio is free of ticking time bombs. So let’s call out five dividend darlings that are actually “yield traps.” Their dividend histories make them look tempting – but buying now could be a recipe for steep losses. Why?

Because You Can’t Take Any Dividends for Granted Today

Business disruption is accelerating as entire industries are being eaten alive.

Uber (UBER) and Lyft (LYFT)? Killed cabs.

Amazon (AMZN)? It’s crushing retail, and starving their REIT landlords right before our very eyes.

And soon, these disruptors might team up to offer more same-day deliveries – and make more rivals obsolete!

These types of disturbances have added a new layer to contrarian investing. In years past, it was as simple as buying stocks when they were out-of-favor and holding them until they became back in vogue. The “Dogs of the Dow” strategy, for example, usually beat the market by banking the highest blue chip dividend yields – a sign that the tide was ready to turn back in the dogs favor.

But in 2020, it’s not good enough to buy what’s hated. In fact, it’s often dangerous. We income investors must decide whether the light at the end of the tunnel is real, or the lights of an oncoming train filled with Amazon boxes!

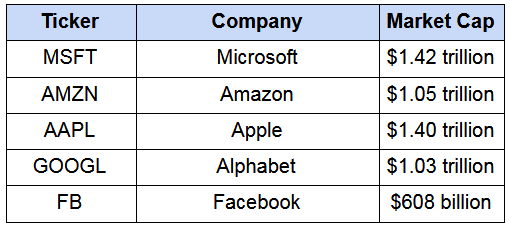

Here are the five locomotives steamrolling business models across the country (and globe). They are currently the five largest firms by market cap:

Notice a pattern? All five are tech titans. More specifically, they are the five best companies at writing software – which they use to scale their own businesses, at the expense of countless others.

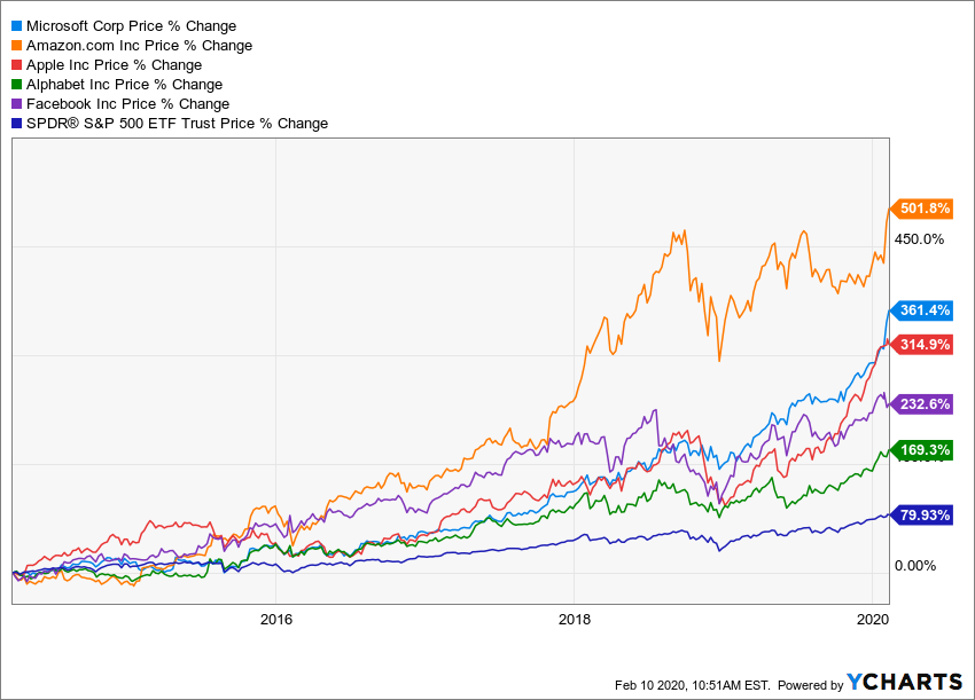

In recent years, they’ve routed the broader market. Their advantage faltered a bit during the 2018’s end-of-year downturn, but it has since accelerated again.

Bubble? Probably not. While the stock market at large may be a bit richly priced right now, these five firms are legitimately beating up brick-and-mortar competitors in real life.

Of course, these five stocks aren’t usually our beat. Only two (Apple and Microsoft) pay any dividend. Even then, their yields are modest (1.0% and 1.1%, respectively), though cases can be made for them as dividend growth plays.

But we’re not going “off script” to pick up one of these names. Instead we’re going to quickly review the dividend landscape at-large to separate the values from the value traps. There are safe and more compelling dividend growth plays today, and I’ll share my favorite in a moment. First, let’s stay away from payout trouble.

Stay Away: Retailer and Retail REIT Dividends

With delivery services just beginning to take off, I’m not sure even “safe” spots like supermarkets are safe. As I mentioned earlier, there are countless Uber and Lyft drivers cruising this country looking for someone, or something, to drive from here to there.

Pharmacies were thought to be Amazon-proof, but CVS (CVS) and Walgreens Boots Alliance (WBA) investors were sent scrambling after reports that Amazon is looking into the pharmacy business. That alone was a potential problem—especially with CVS’ payout ratio already climbing. But the company’s attempted merger with Aetna has essentially put payout growth on ice.

GameStop (GME) provides a cautionary tale. We have warned about this retailer’s dividend for some time – despite the fact that it boasted a payout coverage ratio well outside the “worry zone.” See, payout ratio isn’t everything. If a company’s core business is circling the drain, the company might decide to pull the plug well before the point where it can’t afford its distributions, and instead preserve as much cash as it can to make a final turnaround attempt.

Sure enough, GameStop suspended its dividend in June. Here’s CFRA Research with the predictive obituary: “While GME said the dividend elimination would provide flexibility to drive value creation for shareholders and transform GME for the future, Apr-Q results and intensifying competition from Apple Arcade and Alphabet’s Stadia suggest it may be game over.”

Don’t forget this lesson, because several more retailers are writing out similar scripts right now.

Stay Away: Consumer Staple Dividends

Consumer staples as a whole performed relatively well in 2019, mostly because no one is sure what’s around the next corner, whether it’s a Trump tariff target, the Federal Reserve or Middle East flare ups. But they’re not the same “sure thing” that they used to be.

The internet has squashed these barriers to entry. Prime retail shelf space becomes less and less important as consumers move their shopping online – where they can buy any brand they’d like. And online reviews have created a new “brand recognition” – five stars is five stars, after all.

Consider Kellogg (K), which was one of the most no-brainer companies in the world to own. Everyone had Kellogg’s planted on their breakfast table, whether it was Special K, Frosted Flakes or Rice Krispies cereals, or Eggo waffles or even Pop-Tart pastries.

Not anymore.

Cereal sales have been slumping for years. Some of it is dietary—Americans especially have been leaning away from higher-carb diets, which puts most of Kellogg’s offerings at a disadvantage. But you also have the “problem” of better employment and wages, which allow people to splurge more on fast-food options during their commutes.

The result? Kellogg’s sales (orange line in the chart below) have mostly stagnated for years – and shareholders have gotten the short end of the stick.

Stay Away: Restaurant Dividends

The food business today is, more or less, a zero-sum game. Food delivery companies have raised boatloads of money from the public and private markets to advertise and scale their businesses. Their gains have come at the expense of traditional restaurants.

While a few of these eateries have actually pushed back and become solid contenders in their own right, some have merely turned into dining dividend traps.

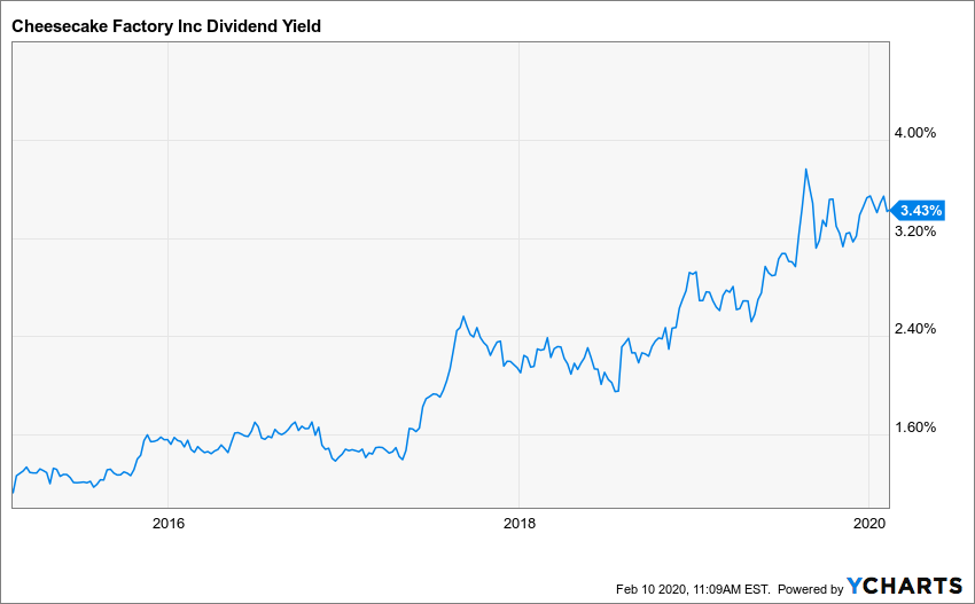

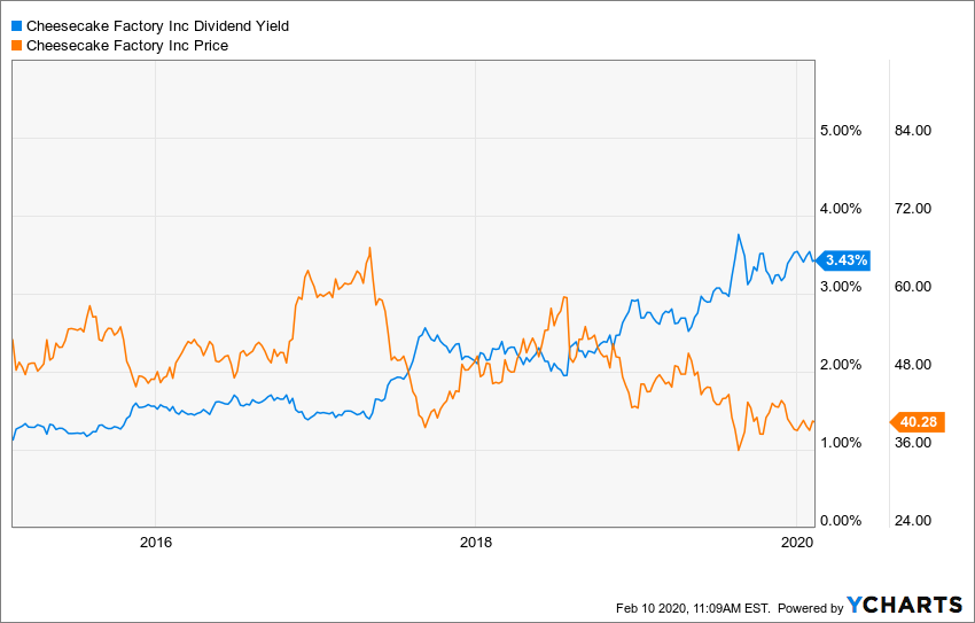

For instance, you might be tempted by Cheesecake Factory (CAKE), the upper-tier chain of Big Bang Theory fame whose yield has been steadily growing for several years now …

… until you realize why that yield has been climbing.

Actual dividend growth has been some of the story. But the company has been dogged by rising labor costs and a longtime chief who has been slow to meet the restaurant’s challenges in recent years.

My advice? Leave the food section to short-term traders. Let’s instead turn our focus to reliable dividend payers with business models that are booming. I like seven firms in particular – all seven should see their profits continue to roll higher, no matter what happens politically or economically.

Sure, most stock prices are on the high side right now. But, believe it or not, there are a few quality dividend growers that are still pretty cheap. These payouts will continue to climb in the years ahead, powering these shares prices – which each have 100% upside.

Buy #1: A Boomer-Powered Payout

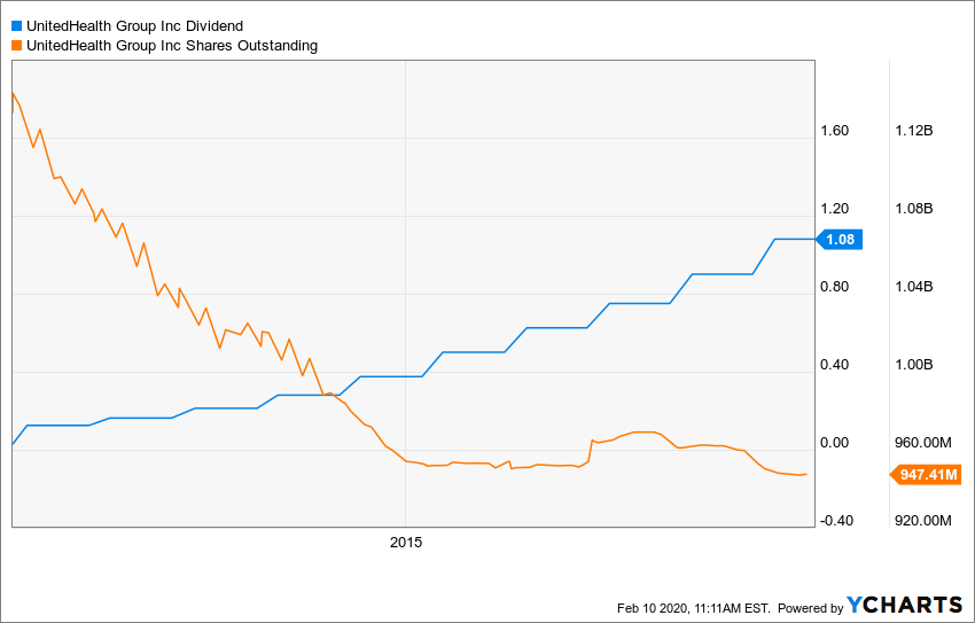

UnitedHealth Group (UNH), the largest health insurance carrier in the U.S., cares for its shareholders personally. The firm has bought back 18% of its shares outstanding over the past decade and boosted its dividend by an incredible 3,500%!

UNH pays a modest 1.5% today, and investors know this stock is never “cheap” by traditional measures, but it always rewards its shareholders. For example, those who bought just five years ago are now pocketing a healthy 5% yield on their initial investments because the payout has roughly tripled in that time.

But if you think you’re late to the UNH party, don’t worry. There’s plenty more to come.

The company is one of the most consistent profit-growers out there, with UNH growing EPS at a nearly 27% annualized rate over the past five years. And analysts brave enough to look five years down the road see average annual profit growth of 12% into 2025.

A huge growth driver will be the company’s technology driven Optum unit, which the firm had the foresight to start in 2011. Optum provides pharmacy benefits, runs clinics and supplies data analytics and other cutting-edge tech to streamline healthcare. Business is booming: in 2019, Optum’s revenue grew to over $100 billion for the first time.

Those numbers will keep climbing as baby boomers retire, sending healthcare demand through the roof. And with a conservative sub-30% payout ratio, UNH has plenty of room to keep its dividend growth fans happy with double-digit increases for years to come.

Buy #2: The Rare Retailer That Bezos Fears

I need to give some credit to Walmart’s (WMT) latest efforts. I didn’t think they’d be able to pull it off!

Regular readers know that I’ve been down on the original big-box retailer for the past couple of years. Walmart’s core business was slowing because of online competition. The giant needed to get its e-commerce (online sales) rolling ASAP.

I doubted, but “Wally World” has (thus far) proven me wrong. Sales through Walmart’s website and mobile app are booming. Its e-commerce revenue is growing at a brisk 41% clip year-over-year.

In my college days, we actually studied Walmart’s supply chain. It was one of the finest examples of operations research applied to market domination.

Wally is one of the few retailers positioned to compete with Jeff Bezos and Amazon on same-day delivery, thanks to its logistics expertise and deep bench of brick and mortar locations. Really the firm is one partnership with Uber away from getting you anything you want within the hour.

Can Walmart make quick deliveries cost effectively? We’ll leave the math to company execs. But Wall Street is clearly pleased with the firm’s progress over the past year. So are income investors, who were rewarded with Walmart’s 46th consecutive annual dividend hike earlier this year.

Buy #3: Bet on the NYSE

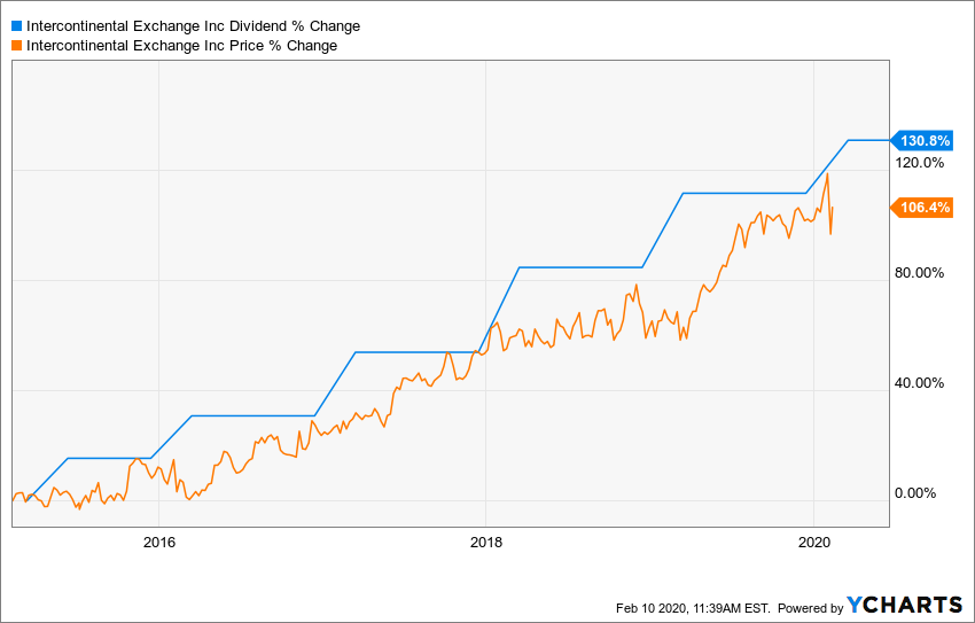

It’s a bull market in U.S. stocks, which is benefiting shareholders of a little-known dividend grower. Intercontinental Exchange (ICE) has increased its dividend by 130.8% over the past five years and, on cue, its share price has more than doubled, too.

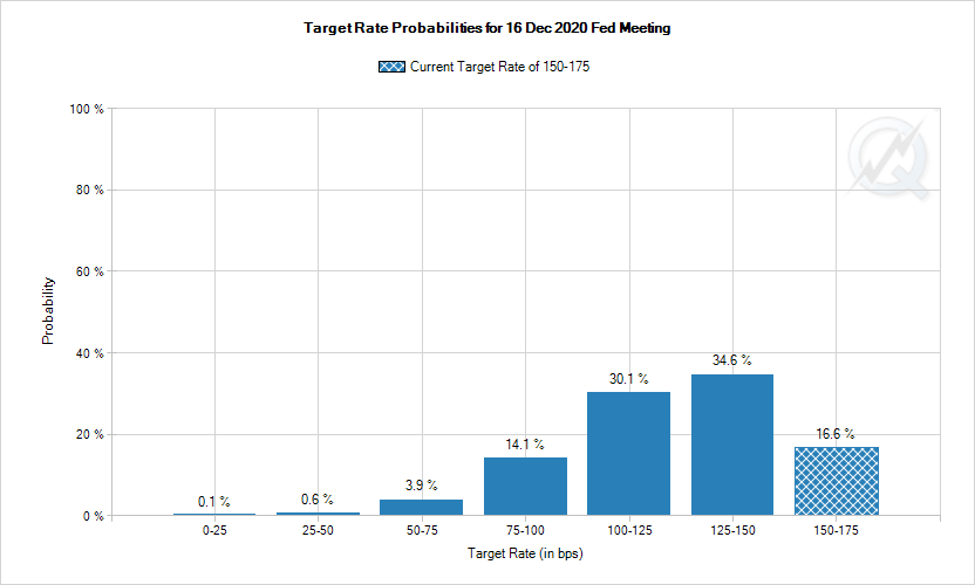

Federal Reserve Chair Jay Powell looks oh-so-likely to cut rates further in 2020. In fact, future traders believe Jay will cut the Fed funds rate by another 50 basis points between now and year’s end!

The last time the Fed cut rates while the stock market was soaring, it was July 1995. That dovish move drove stocks higher by another 20% over the ensuing 12 months.

With the months ahead looking good, it’s certainly blue skies ahead for ICE shares.

Same goes for dividend growth. Intercontinental Exchange has a meager payout ratio of less than a third of its profits, meaning raises like February’s 9.1% bump are plenty doable in the years ahead.

Buy #4: Tapping a Tech Revival

Microsoft (MSFT) got its mojo back. All it had to do was ship its middling CEO to the Los Angeles Clippers!

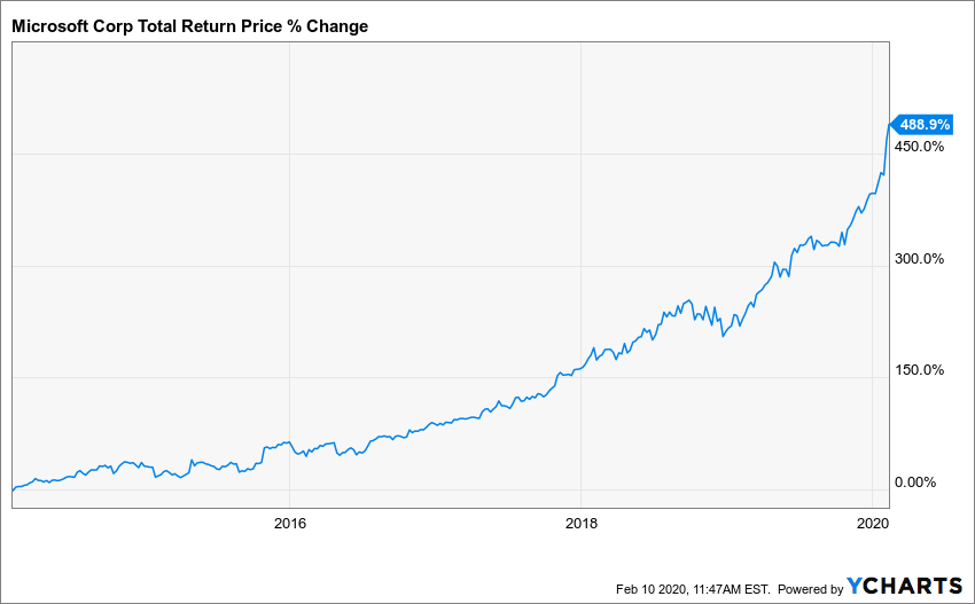

The world is full of mediocre business leaders, but few of them get to purchase a professional basketball team as a reward. Think I’m being harsh on Steve Ballmer? Let me present Exhibit A: Over his 15 years as Microsoft’s boss, his stock returned a cumulative negative 15% to investors:

Now for Exhibit B. Exit Steve and enter Satya Nadella, who quickly pivoted Microsoft toward cloud and business computing (which is growing by leaps and bounds) and away from personal computing (which is shrinking). The result? A quadrupling in Microsoft’s stock price:

The firm’s Azure platform is particularly exciting. It’s the most legitimate competitor to Amazon’s wildly successful Amazon Web Services platform, which lets companies “outsource” their computing needs. Instead of buying and maintaining expensive servers, they rent storage space and processing power from Amazon and Microsoft.

Current Azure customers include GE Healthcare, Rolls-Royce and Samsung. Demand is booming – the unit is growing by 59% year-over-year.

Overall, Microsoft itself is split into three business segments:

- Intelligent Cloud (which includes Azure)

- Productivity and Business Processes

- Personal Computing

The first two are the growth drivers, and they now represent more than half of Microsoft’s total revenues – which marks an important turning point, because personal computing losses will affect the bottom line less and less. Analyst expectations reflect this, projecting earnings per share (EPS) gains of almost 12% annually in the years ahead.

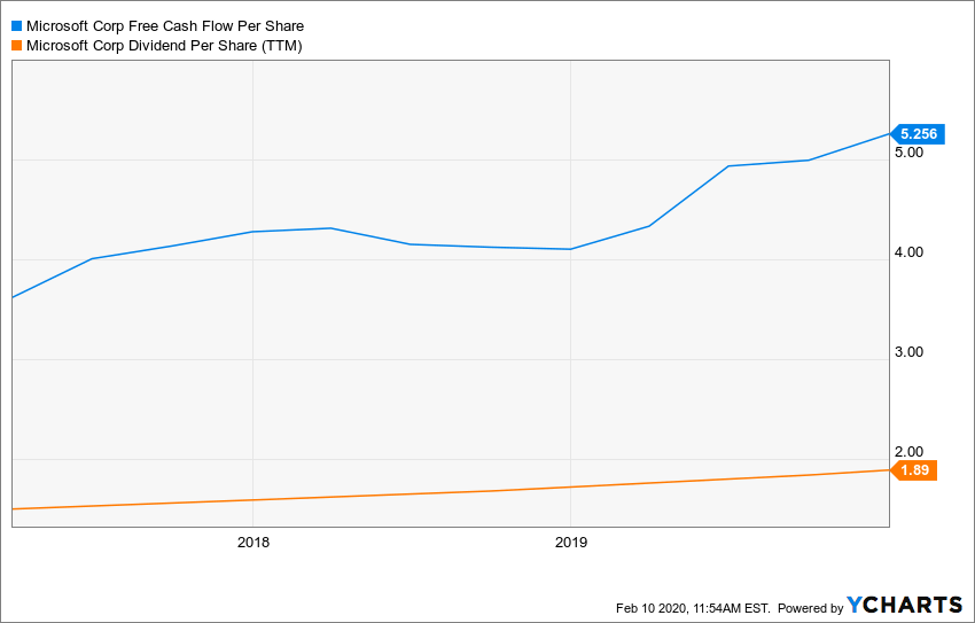

And Earnings Gains Drive Dividend Hikes

Nadella has raised Microsoft’s dividend by 64% since taking the helm. And he still has plenty of dry powder for more payout hikes, with the company paying out just more than a third of its free cash flow (FCF) as dividends today:

The future looks bright for the company and its stock.

Buy #5: This Ain’t a Game

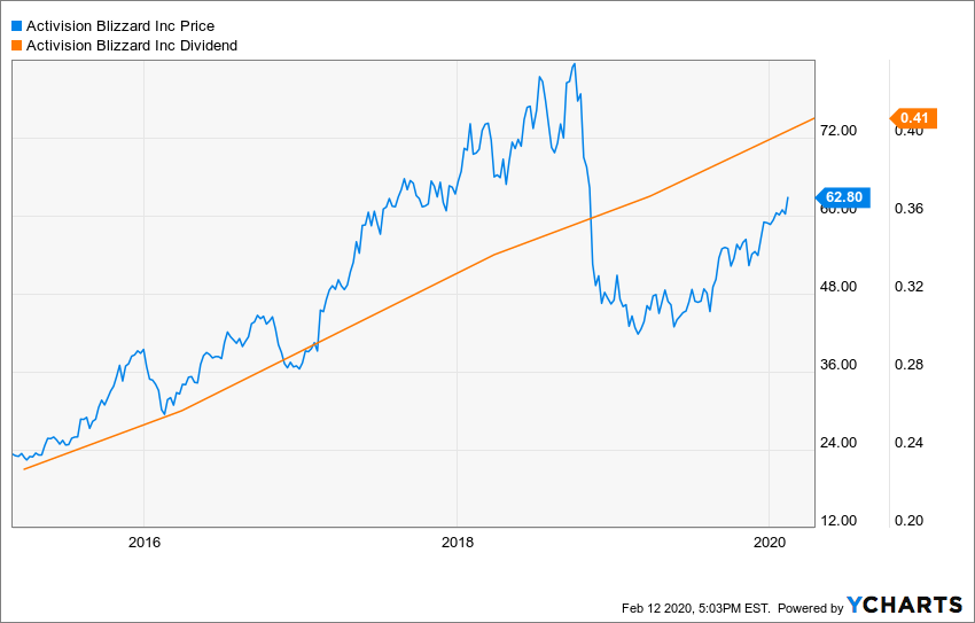

A dramatic 2018 for Activision Blizzard (ATVI)—in which the stock was crushed—led to an especially quiet 2019 uptrend. With the bad news (and more) already priced into shares, they had nowhere to go but up.

Plus, the firm’s payout goes up every year. The video game publisher has paid an annual dividend every spring since 2010. Its dividend sits nearly 80% higher today.

We can see now that 2018’s pullback was nothing more than an expected correction.

Dividends act as “magnets” for their stock prices, for better and for worse. This is why smart dividend growth investors prefer to buy shares when they are due to “catch up” to their rising payouts:

The fast-growing eSports industry and the company’s promising sequel to World of Warcraft are being credited for the recent comeback. But actually, the stock was “due” to start catching back up with its dividend.

Buy #6: A Rare High-Growth Utility

If you’re buying utility stocks for dividends, focus on the firms that are boosting their payouts the fastest. Growth matters today especially because the Utilities Select Sector SPDR ETF (XLU) pays just 3.4% currently. This puts utility dividends at a 10-year low.

The problem with buying utility stocks with low yields is that, in most cases, payout boosts aren’t going to provide much help.

Even stalwarts like Duke Energy (DUK) and Southern Company (SO) are clocking anemic 4% to 5% annual dividend growth respectively. Yawn.

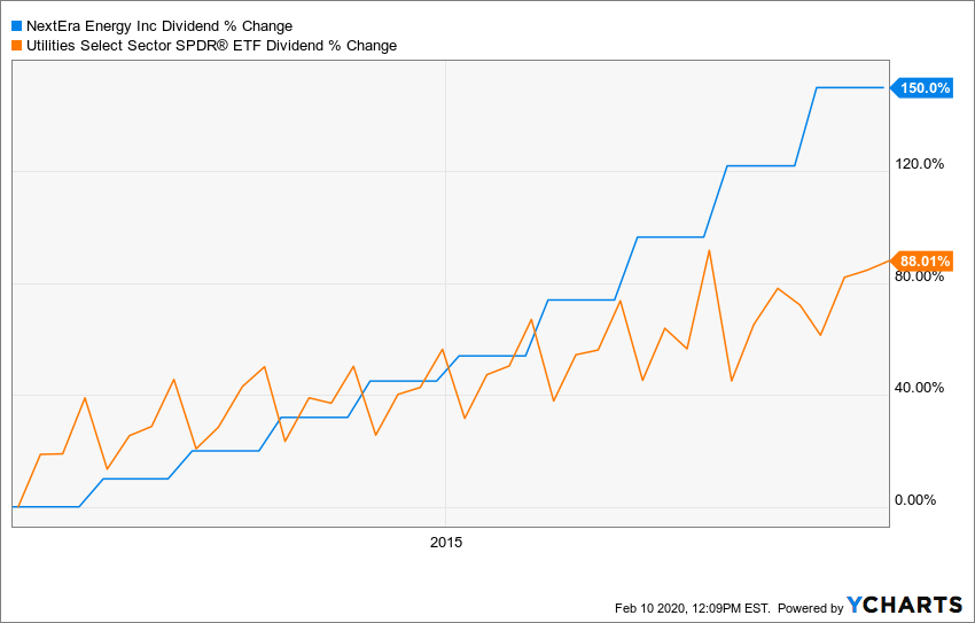

Instead, let’s consider NextEra Energy (NEE), the largest developer of renewables in North America. Most of its customers are based in Florida and serviced by subsidiary Florida Power & Light Company, which boasted 20%-plus EPS growth in the first quarter of 2019.

The firm has been a fast grower for decades. It has increased its dividend for 25 straight years. And these have been meaningful raises – NextEra has dusted its peers with 150% dividend growth over the last decade (versus just 88% for XLU):

NextEra gives dividend investors the best of both worlds: the safe current yield of a utility, with the promise of strong future payout hikes and stock price growth.

Buy #7: A Resilient Dividend, Moving Higher Again

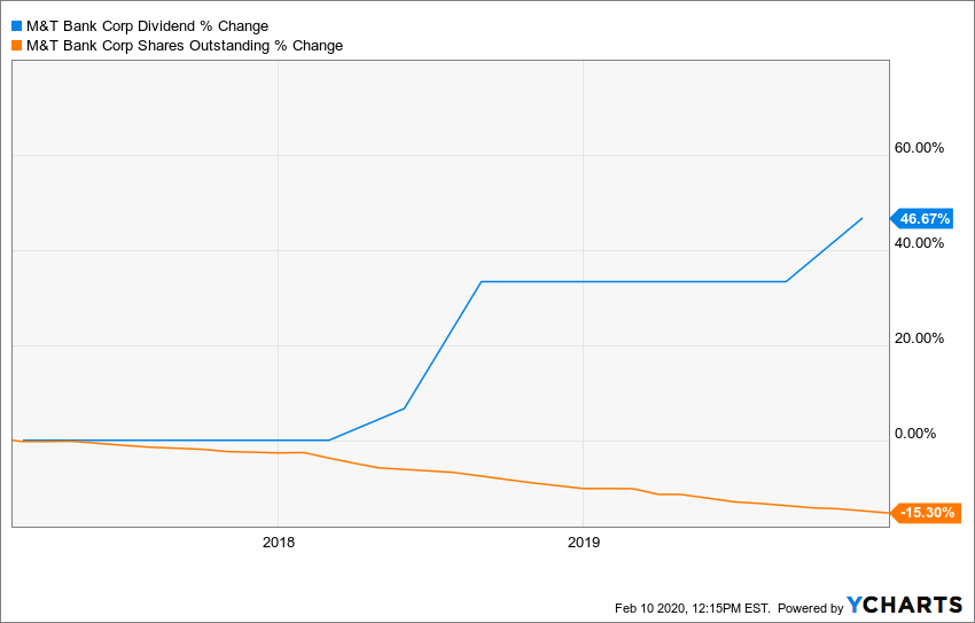

M&T Bank (MTB) has posted a quarterly profit 167 times in a row (since 1976). It was one of two commercial banks (out of 20) that maintained its dividend throughout the financial crisis.

The bank held onto more than 50% of its profits from 2008 through 2015 as it hunkered down through the financial crisis and the stricter regulatory environment that followed. Its conservative strategy resulted in a stockpile of capital, and this bank with “too much cash” continues to dish more of its profits back to shareholders.

In just the last three years, M&T bank has boosted its dividend (by 46.7%) while repurchasing 15.3% of its shares outstanding:

The stock trades for a reasonable 14.4 times free cash flow (FCF) today while paying a 2.6% dividend. It’s a safe bet in an uncertain world.

Altogether, the stocks I’ve told you about today are a good first step on the path to growing your nest egg and income.

But to show you just how much this strategy can juice your returns, I’m going to do something I don’t normally do.

I’m going to share with you my 7 absolute favorite recommendations — normally reserved exclusively for premium members of my Hidden Yields research service — free, right here, today.

These seven companies are the “cream of the crop” when it comes to rising dividends and strong buyback programs … the kind of stocks that could easily spin off annual total returns of 15%, 19%, even 25% or more … doubling your money in very short order.

They’re certain to do well no matter which way the broader market swings … regardless of what happens in Washington … and irrespective of interest rate trends.

My publisher isn’t happy about this, but I love these high-velocity plays so much that I want to share them with as many investors as possible.

And, naturally, I’m hoping you’ll give me the opportunity to show you more big profit opportunities in the months ahead.

So, if you’re ready to start growing your portfolio by 15%+ per year, I’d like to give you three additional reports …

Free Bonus Report #1 (a $99 value)

The first is called “The 7 Best Dividend Growth Stocks With 100%+ Upside.”

Inside, you’ll find the ticker symbol, my specific buy-up-to price and in-depth back story on each, including:

Inside, you’ll find the ticker symbol, my specific buy-up-to price and in-depth back story on each, including:

- An under-the-radar income play that’s delivered 1,000% revenue growth since 2008 and shows no sign of slowing down,

- Another company that’s raised its dividend by 140.5% over the past 5 years,

- And yet another that rose 250% the last time its shares were trading this cheap!

Free Bonus Report #2:

Behind the 8-Ball: Eight Popular Dividends Set for a Cut

To gauge dividend health, you can’t simply look in the rearview mirror. Many “surprise” payout cuts are issued from companies with long streaks of paying — or even raising — their dividends.

Instead, it’s important to consider leading indicators of dividend health like cash flow, earnings growth, and payout ratios.

Of course, it’s time consuming to give each public company a dividend health checkup – so I’ve done the work for you in this special report.

Using a combination of seven fundamental factors, I have identified eight popular companies that are likely to cut their dividends over the next twelve months.

Investors caught holding these stocks through dividend disappointments will likely suffer losses of at least 20%, and perhaps as high as 50%.

Therefore, if you own any of these eight paper tigers, you’ll want to sell them immediately.

This one-of-a-kind report is another $99 value – and it could easily save you thousands in future losses – but you can get it FREE today along with …

Free Bonus Report #3:

Shareholder Yield: How to Identify Double-Digit Returns from Buybacks

As we saw above with UNH and MTB, when done right, share buybacks can light a fire under stock returns.

They also act like a magnifying glass on dividend payments because they cut the number of shares outstanding, leaving fewer for the company to pay out on.

But many companies are going too far, paying out more in buybacks than they’re bringing in through free cash flows.

Worse, many buy back their stock willy-nilly, without making sure it’s a good value first. There’s no better way to destroy shareholder value than by repurchasing overpriced stock.

This report gives you everything you need to know to make sure the companies you invest in are buying back shares the right way – not simply burning up cash that would be better used as dividends or to develop revolutionary new products.

These three reports will give you seven rock-solid income investments that can keep growing your portfolio … hand you larger and larger income … while also protecting you from suffering dividend cuts or ill-advised buyback programs.

But there are two things those reports can’t give you – ongoing updates and all my FUTURE income recommendations.

That’s why, in addition to giving you these three reports – worth $297 on their own – I also want to give you a risk-free, 60-day trial to my premium newsletter called Hidden Yields.

My Hidden Yields picks are perfect for savvy investors looking to rack up fast gains in the near term plus bigger and bigger yields thanks to soaring dividend payouts.

Right away, you’ll get instant access to many more under-the-radar picks in the publication’s portfolio – the vast majority of which are hiking their payouts at double-digit rates – plus all the new buys I uncover in the coming months.

I do all the digging for you, recommending only the safest dividend growers and keeping you well clear of companies funding their payouts with borrowed money — or worse, betting the farm on shaky business models that will crumble at the first hint of a downturn.

What’s more, I send out new recommendations whenever they’re worth buying plus I give you regular updates on earlier recommendations … all in plain, everyday English.

All told, you’ll get:

- Monthly Research Bulletins: On the third Friday of each month, you’ll receive my latest investment analysis right in your inbox. I’ll include detailed analysis on new recommendations, updates on existing positions, and an overview of trends and events that may affect your portfolio.

- Our Full Members-Only Portfolio: All of our recommendations are laid out in an easy-to-read portfolio that includes exact buy/sell recommendations and buy-under prices.

- Weekly Market Updates: Sent straight from my desk to your inbox, you’ll get my weekly investing ideas on stocks I’ve been watching and analysis of major market events taking place.

- Additional Flash Alerts: You’ll never have to worry about breaking news on our portfolio stocks. I’ll have an eye on all of them constantly and will email you right away if there’s ever any need to take action.

- Unlimited Access to Our Members-Only Website: Day or night, you can log into our password-protected website, where you’ll find easy access to all of our resources, including an archive of past issues, special reports, Flash Alerts, and the full portfolio.

- Plus, a whole lot more!

Obviously, this is a serious investment service for serious income investors and all you have to do is click here to activate your risk-free trial now.

And unlike some other publications that give you risky ideas and let the chips fall where they may, I want to protect you in one more critical way …

And Keep Your Portfolio Growing 15% a Year,

You’ll Never Have to Pay One Red Cent!

The regular annual subscription rate to Hidden Yields is $299 and I think that’s more than fair. After all, just a small investment in any one of my recommendations could easily cover the membership fee many times over.

But as part of this special offer, I want to reduce your risk down to ZERO.

So here’s the deal …

If you join right now, you can get a charter membership for just $99 … a full 67% off the regular retail rate.

Then, download your three free reports (worth $297 alone) and enjoy all the other members-only benefits for the next 60 days.

If, at any point during that period, you don’t think my ideas can help you double your income and keep your portfolio growing at least 15% a year – or you’re unhappy for any other reason at all – just give us a call and we’ll gladly refund your entire membership fee with no questions asked.

Plus, you can keep everything you’ve received up until that point just for giving my research a shot!

That’s how confident I am that you’ll profit from the ideas and recommendations in your free reports and first few issues of Hidden Yields!

Just to recap, you’ll get:

A free copy of “The 7 Best Dividend Growth Stocks With 100%+ Upside” –which will introduce you to my seven favorite rock-solid companies with fast-growing dividend streams (a $99 value!)

A second free report called “Behind the 8-Ball: Eight Popular Dividends Set for a Cut” – which exposes eight widely-popular dividend stocks for the massive risks that they really are (a $99 value)

A third free guidebook called “Shareholder Yield: How to Identify Double-Digit Returns from Buybacks” – which will help you make sure none of the stocks you own are ticking buyback bombs (a $99 value)

Plus, a full year of Hidden Yields and all the charter membership benefits that subscription includes (normally $299 a year) …

And you’ll be fully covered by a full, unconditional, 60-day money back guarantee!

Obviously, the final decision is all yours.

But I don’t see how you can lose here since I’m the one taking all the risk.

Again, all you have to is click here to activate your risk-free trial now.

I’m really looking forward to welcoming you aboard!

Yours in profits,

Brett Owens

Chief Investment Strategist

Hidden Yields

P.S. This special offer is only good for a limited time – so if you want to get everything I just told you about with absolutely no risk or obligation whatsoever, you need to act now.

Nothing in Contrarian Outlook is intended to be investment advice, nor does it represent the opinion of, counsel from, or recommendations by BNK Invest Inc. or any of its affiliates, subsidiaries or partners. None of the information contained herein constitutes a recommendation that any particular security, portfolio, transaction, or investment strategy is suitable for any specific person. All viewers agree that under no circumstances will BNK Invest, Inc,. its subsidiaries, partners, officers, employees, affiliates, or agents be held liable for any loss or damage caused by your reliance on information obtained. By visiting, using or viewing this site, you agree to the following Full Disclaimer & Terms of Use and Privacy Policy.