Fellow Investor,

Thank you for requesting your copy of my latest special report, How to Live Off $500,000 Forever.

In addition to your free report, I’ve also arranged for you to receive a complimentary subscription to the Contrarian Outlook email newsletter. Inside, you’ll receive my unique “second-level” analysis on dividend payers and growers so that you can maximize your portfolio’s current yield AND upside, even in this uncertain market.

Look for your first issue soon.

In the meantime, enjoy your free special report below.

Yours in payout profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

Brett Owens, Chief Investment Strategist

A half-million dollars is a lot of money. Unfortunately, it won’t generate much income today if you limit yourself to popular investments.

The 10-year Treasury pays barely 1%. Put your $500K in them and you’re sitting below the single-person poverty level, netting less than $5,000 annually. Yikes.

Dividend-paying stocks are masquerading around as bond proxies for this reason. But they still don’t yield enough. Vanguard’s popular Dividend Appreciation ETF (VIG) pays less than 1.9%. The iShares Select Dividend ETF (DVY) pays 3.3% – better, but that still only gets you $16,500 per year, which is below the poverty level for a two-person household.

When investment income falls short, retirees sell their investments to supplement the income. Of course, the problem here is that when capital is sold, the payout stream takes an immediate hit – so more capital must be sold next time, and so on.

The Only Reliable Retirement Solution: No Withdrawals

Rather than rely on, say, a 4% annual drawdown for income, the only dependable way to retire and stay retired is to boost your payouts so that you never have to touch your capital.

This is easier said than done, and obviously the more capital you have the better off you are. But with rates and yields so low, even rich guys have a tough time living off interest today.

You can actually live better than they can off a (much) more modest nest egg if you know where to look for lesser-known, meaningful and secure yield. I’m talking about annual income of 6%, 7% or even 8% – so that you’re banking up to $40,000 each year for every $500,000 you invest.

And you’ll never have to touch your nest egg capital – which means you’ll never have to worry about stock prices.

The only thing you need to concern yourself with is the security of your dividends. As long as your payouts are safe, who cares if your stock prices swing up or down on a given day?

Most investors know this is the right approach to retirement. Problem is, they don’t know how to find 7% and 8% yields to fund their lives.

And when they do find high yields, they’re not sure if these payouts are safe. Will the company or fund have enough cash flow to pay the dividends into the future? And how sensitive are these payouts to interest rate changes?

Let’s walk through my three favorite corners of the investment universe for income today.

“No Withdrawal” Play #1: Closed-End Funds

Some closed-end funds (CEFs) paying up 7%, 8% or even 9% can be good income candidates – if you choose wisely.

You’re probably familiar with their mutual “cousins.” Closed-ends are a bit different. While mutual funds tend to buy individual stocks and mirror the market, CEF managers tend to have wider mandates and longer leashes. A top CEF manager takes advantage of this flexibility to generate alpha.

He might buy safe sovereign debt in Australia when investors are scared of Asia altogether, and lock in secure 6% yields. Or he might buy preferred shares issued by a financial firm paying 6.1% annually – a deal not available to an individual investor like you or me (more on this in a minute).

A savvy closed-end manager can even borrow cheaply and juice returns. CEFs borrow at rates tied to Libor (the London interbank offered rate) – good living today with the international benchmark at just 2.5%. The “spread” turns already good yields into great ones.

One aspect of the CEF structure lends itself perfectly to contrary-minded investing – fixed pools of shares.

Mutual funds issue more shares whenever they want. But closed-ends have a fixed share count, with their funds trading like stocks. As a result, from time-to-time a fund will fall out-of-favor and find its shares trading at a discount to its net asset value (NAV).

This is basically “free money” because these underlying assets are constantly marked to market. If a fund trades at a 10% discount, management could theoretically liquidate the fund and cash out everyone at $1.10 on the dollar immediately. Or it can buy back its own shares to close the discount window (and boost the share price).

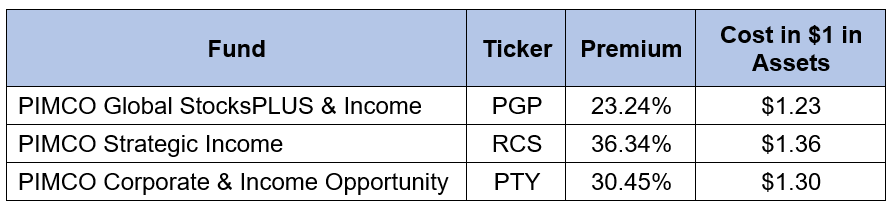

Premiums, on the other hand, are rare in the closed-end space, and usually reserved for “rock star” managers and hot ideas. PIMCO’s funds would often trade at a premium when “Bond King” Bill Gross was running the show. In fact, three still do trade at double-digit premiums, with the most excessive at nearly 34% today!

Yes, you read right – there are people who pay $1.36 for $1.00. Personally I prefer not to be down big out of the gate.

I demand a discount when I buy closed-ends, and so should you.

Then, Look for Alpha

Visit the homepage of any CEF you’re considering. Read through the most recent reports and the letters from management and figure out if their strategy is adding value or just paying their own salaries.

There’s an easy way to verify – check the track records. Funds have histories, as do their managers. Look at both.

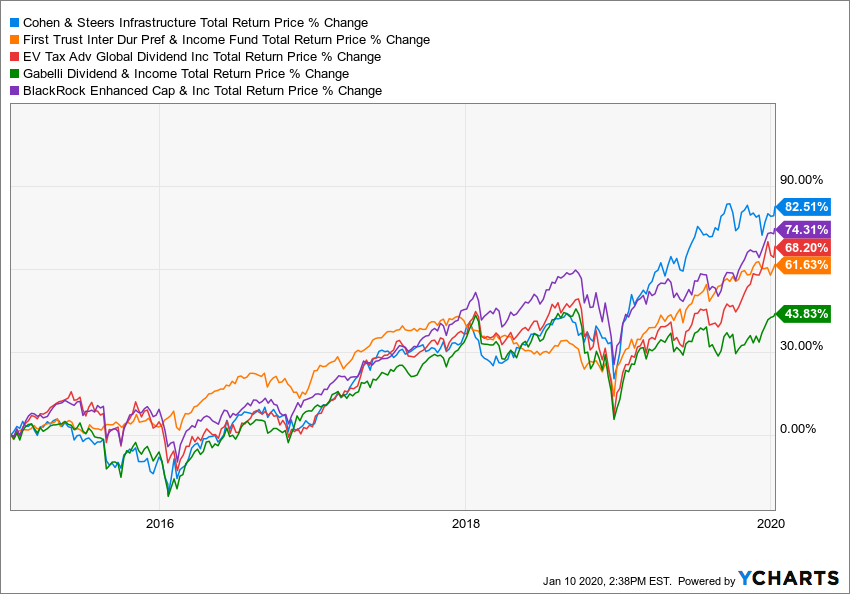

To check a fund’s track record, use the “total return” calculation, which includes dividends – this is important because most of the gains from CEFs come in the form of payouts.

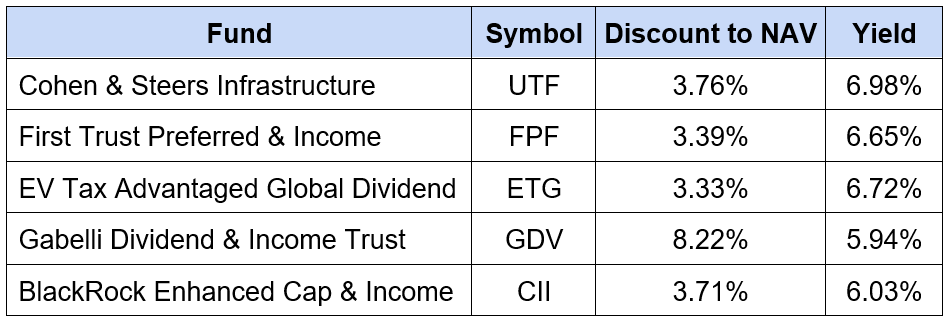

Five Alpha-Worthy 5% CEF Yields (at Big Discounts, Too)

Here are five CEFs that meet our initial criteria. They all:

- Pay 5% yields or better.

- Trade at a discount to NAV.

- Have returned 40% cumulatively or better over the last five years.

“No Withdrawal” Play #2: Preferred Shares

You can double your yields, and actually reduce your risk, by trading in your common shares for preferreds. Most investors only consider “common” shares of stock when they look for income. These are the shares in a company you receive when you place an order with your broker.

Problem is, most dividend darlings don’t pay much on their common shares today. You’ll be hard pressed to find a dividend aristocrat with a yield above 3% or a P/E ratio below 20–evaporating business models or not!

A company will issue preferred shares to raise capital. In return it will pay regular dividends on these shares – and as their name suggests, preferreds do receive their payouts before common shares. They typically get paid more, and even have a priority claim on the company’s earnings and assets in case something bad happens, like bankruptcy.

So far so good. The tradeoff? Less upside. But in today’s expensive stock market, it may not be a bad trade to make.

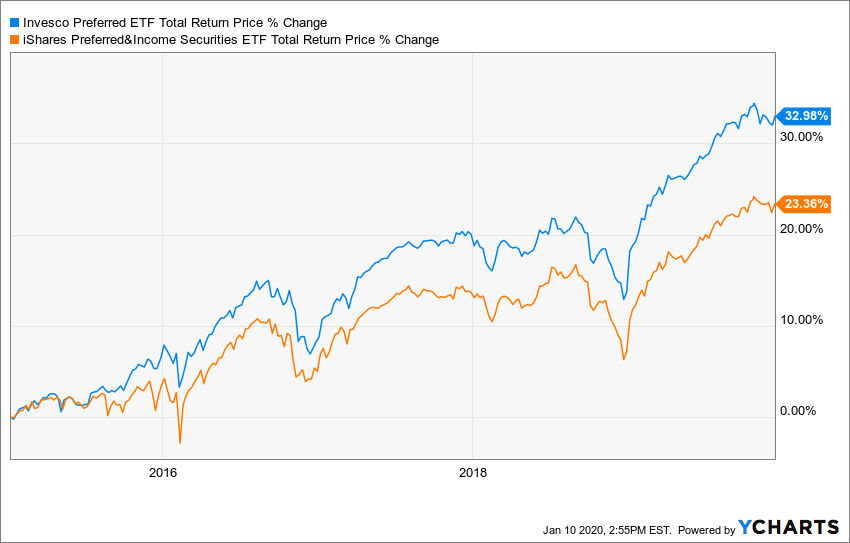

However, the complexity of buying preferred funds tempts many investors to streamline their online buys and simply purchase ETFs like the PowerShares Preferred Portfolio (PGX) and the iShares S&P U.S. Preferred and Income Securities ETF (PFF). After all, these funds pay 5% or more and, in theory, they diversify your credit risk.

Be careful because I believe they actually expose you to unnecessary credit risk. The only way you lose with this vehicle is by giving your money to a driver who crashes your car. But the S&P 500 and NASDAQ are large enough that there’s usually a company financially crashing into a brick wall at any moment in time.

And if we look back to the brick walls over the past 5 years, these funds barely even broken their current yields:

I suspect PGX and PFF probably won’t actually return 5% annually over the next decade, either. Which why I recommend moving past a broad-based ETF in favor of a fund with an active manager working for you. There’s extra yield to be had in preferred shares – but you should make sure you have an expert buying your stock to keep you safe and on the road.

Instead, consider the Flaherty & Crumrine Dynamic Preferred & Income Fund (DFP), which buys high-quality preferred securities. The managers and analysts do their own internal credit research on each issue they consider, focusing on “avoiding strikeouts rather than hitting home runs.”

They’ve got their own database with the specific terms and interest rates on each preferred security on the planet. They shoot for “attractive levels of income” while balancing credit, liquidity, and interest rate risks. The level of sophistication required to invest in this market highlights why you want an experienced team doing the legwork for you.

The DFP portfolio management team has decades of experience with preferreds. They’ve more than quadrupled what the Barclays U.S. Aggregate Bond Index (a proxy for the fixed-income market) has returned since the fund’s inception in May 2013.

“No Withdrawal” Play #3: Recession-Proof REITs

Real estate investment trusts, or REITs, can be powerful investment vehicles for safety and high yield. Legally required to return 90% of income to shareholders, these firms find high-quality real estate opportunities while providing investors the opportunity to be a landlord with the liquidity – and convenience – of a stock.

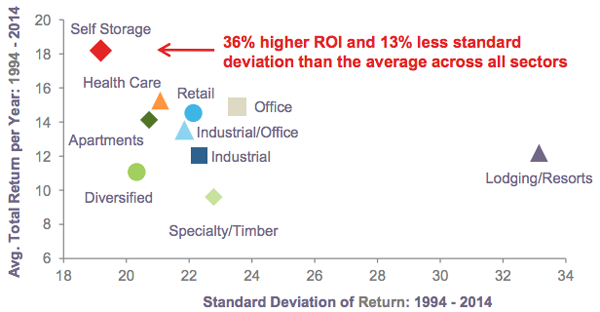

Some REITs are relatively recession-proof. Self-storage REITs, for example, were industry darlings for two decades. These stocks delivered 18% annual gains with the least amount of volatility (or price gyrations) in the REIT world from 1994 to 2014:

While REITs that specialize in strip malls or hotels suffer if a recession hits, others such as healthcare REITs will see steady demand no matter what happens with the broader economy. Sector staple Ventas (VTR) pays 5.5% today, and some quality issues actually pay 8% or better.

Meanwhile self-storage REITs like Public Storage (PSA) can actually see an uptick in demand when economic trouble strikes. For example, in 2008 when millions of Americans were losing their homes, demand for self-storage went up as people abandoned their underwater houses and looked for a place to keep their valuable possessions.

PSA only pays about 3.7% today, but Stag Industrial (STAG) yields 4.5%. It owns, operates and rents 390 standalone industrial buildings, most of which are warehouses or distribution centers in hot demand thanks to the e-commerce megatrend.

An Average 8% Yield, With Upside

Altogether, these three “No Withdrawal” vehicles—and the nine picks I’ve named here—are a good first step on the path to a secure, worry-free retirement.

And it won’t be long before other income investors ditch their paltry 3% and 4% payers and find their way over to these “slam dunk” income plays, sending prices through the roof. The time to start re-imagining your portfolio is now, while they still trade at deep discounts to NAV and FFO.

But to show you just how much the “No Withdrawal” strategy can juice your income, I’m going to do something I don’t normally do.

I’m going to share my absolute favorite picks—normally reserved for premium subscribers to my Contrarian Income Report research service—free, right here, today.

My publisher isn’t happy about this, but I like these high-yielders so much that I want to show them to as many investors as possible. And naturally, I’m hoping you’ll give me the opportunity to show you more double-digit dividend growers just like it.

So, if you’re ready to kick start your “No Withdrawal” retirement, I’d like to give you three additional reports on each of the strategies mentioned above, including my absolute favorite recommendations, reserved exclusively for premium subscribers…

Special Report #1 (a $99 value)

The first is called the Monthly Dividend Superstars: 8% Yields With 10% Upside.

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on each of my three favorite CEFs, including:

- An 8.1% payer that’s set to rake in huge profits from an artificially depressed sectort,

- The brainchild of one of the top fund managers on the planet that pays 9.1%, and

- A rock-steady 6.5% dividend trading at a massive discount to NAV.

Special Report #2 (a $99 value)

The second guide is called Preferred Shares: Looking Past Common Dividends for 6.5% Income.

Inside you’ll find my favorite fund for investing in preferred shares, along with its management profile and investing strategy.

The fund pays 6.5% today.

High yield is great, but its best quality may be its lack of correlation with the broader stock market. The shares this fund owns are preferred in every sense of the word – meaning it gets paid its fat dividends no matter what the broader market does.

Special Report #3 (a $99 value)

Your third guide, Recession Proof REITs: 2 Plays With 8% Yields and 25% Upside, reveals my two favorite REITs. They include:

Your third guide, Recession Proof REITs: 2 Plays With 8% Yields and 25% Upside, reveals my two favorite REITs. They include:

- An 8.2% payer uniquely positioned to thrive in the current rate environment, and

- A 7.9% “unicorn” that’s increased its payout by 36% since 2015!

In each report you’ll get the rationale behind where, why and how to profit. In short, everything you need to know about these stocks before you invest a single penny.

How to Get All 3 Reports Absolutely Free

To access all three reports at no cost whatsoever, I simply ask that you take a risk-free trial of my research service, Contrarian Income Report.

I created Contrarian Income Report to help self-directed investors uncover overlooked and under-appreciated income plays before Wall Street and the mainstream herd bid them up.

Right now, there are 20 high-yield stocks and funds in our CIR portfolio, and you get instant access to each one the moment your no-risk trial starts.

PLUS you’ll get my next 2 NEW monthly issues.

Every new investment you get in Contrarian Income Report comes with a simple guarantee: it will pay SAFE 6% dividends—or better.

And 6 holdings in our portfolio go way further than that, delivering up to 8%+ income right now.

So just by “swapping out” your blue chips for these high-powered dividend stars, you could double, triple—or even quadruple—your income. And you could do it TODAY!

But don’t take my word for it. Here’s what some of my subscribers have to say about these recommendations:

Mark M. from Michigan wrote:

“Contrarian Income Report has made a big difference in my retirement income and I am very glad I found this report. My dividend income is up almost 25% since I converted everything to the Contrarian portfolio.”

B.E. from Alaska said:

“Instead of paying [my advisor] $16,000 a year to invest my money, I am receiving $86,000 per year in dividends in my IRA, and $24,000 tax free dividends in our taxable account. I very much appreciate all the work that you guys do.”

Craig R. from Pennsylvania told us:

“Just wanted to write and let you know I’m very pleased with my subscription to your services… Keep up the good work! I sleep better at night not worrying about the daily gyrations of the market. I’m very glad I found your service.”

J.C. in California wrote:

“I love your insights and as a financial advisor the way I invest my clients’ money many of your newsletters provide me with new ideas to explore and work hand in hand with my value approach. You make my job easier and I appreciate that.”

Scott G. from Indiana said:

“We have been extremely pleased with Brett’s Contrarian recommendations and have friends getting ready to join! We are lifers!”

Richard W. from Massachusetts wrote in to say:

“I have subscribed to several of the biggest advisory services (a couple are even ‘lifetime’ subscriptions) but those from Contrarian Outlook are my favorites and the only ones I actually act on these days.”

Tom I. from Florida told us:

“I’m very happy with your service. It solved my retirement income dilemma which is an incredible relief. Thank You!”

Now, the regular member price to join Contrarian Income Report is $99 per year, but I’m sure you’ll agree it’s well worth the cost. Heck, the three reports you’ll get absolutely free are worth three times that much.

And even a small position in any one of the picks inside will easily cover that in just the first few months.

Imagine 7%, 8%, even 9% dividends rolling in from these picks, and then watching them appreciate as mainstream investors realize what they’ve been missing and inevitably pile back in.

But it’s important that I earn your trust and you have the chance to see exactly how profitable this service can be.

So I’ve arranged for a small number of investors to take 60% off the regular price and try out Contrarian Income Report for just $39.

And I’m so confident you’ll enjoy (and profit from) this service that I’m going to give you 60 days to try Contrarian Income Report absolutely risk-free.

If, after nearly 2 months, you don’t feel the advice has more than covered your cost, or if it’s just not right for you, simply let me know and I’ll issue a full refund.

That’s 100% of your money back, no questions asked.

Plus you’re welcome to keep all of the special reports with my thanks for trying it out.

If you’re ready for 8%+ income and double-digit capital gains, simply click here to get started right now.

Yours in payout profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

P.S. Since my recommendations are contrary to prevailing popular beliefs, they have a habit of rallying quickly as soon as the mainstream herd catches on to what they’ve been missing. I encourage you to get started right now so that you can get in at a good price!

P.P.S. Remember, your risk-free membership comes with the names and full details on my top 3 closed-end funds paying up to 9.1%, dividends up to 8.2% from my top REIT plays, and the Preferred fund that will hand you 6.5%. Even a small position in any one of these picks will easily cover a full year’s membership… most likely before your 60 day trial even ends!

Nothing in Contrarian Outlook is intended to be investment advice, nor does it represent the opinion of, counsel from, or recommendations by BNK Invest Inc. or any of its affiliates, subsidiaries or partners. None of the information contained herein constitutes a recommendation that any particular security, portfolio, transaction, or investment strategy is suitable for any specific person. All viewers agree that under no circumstances will BNK Invest, Inc,. its subsidiaries, partners, officers, employees, affiliates, or agents be held liable for any loss or damage caused by your reliance on information obtained. By visiting, using or viewing this site, you agree to the following Full Disclaimer & Terms of Use and Privacy Policy.