Fellow Investor,

Thank you for requesting your copy of my latest special report, The “Forever Income” Retirement Plan: 7%+ Dividends and 66%+ Upside.

In addition to your free report, I’ve also arranged for you to receive a complimentary subscription to the Contrarian Outlook email newsletter. Inside, you’ll receive my unique “second-level” analysis on dividend payers and growers so that you can maximize your portfolio’s current yield AND upside, even in this uncertain market.

Look for your first issue soon.

In the meantime, enjoy your free special report below.

Yours in payout profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

Brett Owens, Chief Investment Strategist

You’ve made a great choice in downloading my exclusive Special Report, “Your 3-Buy ‘Forever Income’ Retirement Plan: 7%+ Dividends and 66%+ Upside.”

My team and I have designed this handy guide to do 3 things for you:

- Safely steer around the biggest risk retirees face today. (It’s hiding in plain sight, which is why most folks miss it entirely!)

- Show you 3 terrific investments to put yourself on the path to the Golden Years you want. These 3 unsung income plays boast yields up to 7%+, helping you clock out on a much smaller nest egg than Wall Street or the CNBC talking heads say you need.

- Reveal 3 investments (and 6 specific stocks) that look safe but are anything but! Lean too hard on any of them and you could easily come up short once you clock out of the workforce.

So let’s get started by addressing the nasty risk I mentioned in point number 1 right off the top, and it is this: most folks face a much larger chance of outliving their nest egg than they think.

That’s because, according to a just-released breakthrough study, they’re very wrong about the length of their retirement.

A Hidden Danger

Here’s what the numbers say: in 1992, the University of Michigan asked 26,000 Americans 50 years of age and older how long they thought they’d live. The results, 25 years later, are in, and they’re staggering.

When first asked, 7 percent of participants said they had zero chance of making it to 75. But despite their pessimism, 49.2% did just that. Of the folks who gave themselves a 50/50 shot, 75% went on to do so.

So now might be a good time to rethink your expectation of how long you’ll live—because you’ll likely be around a lot longer!

Don’t Buy Wall Street’s Retirement “Solution”

Here’s where Wall Street comes in, with a “solution” only it could cook up.

It’s called the 4% withdrawal rule, and it recommends supplementing the dividend income you get from your portfolio by withdrawing 4% from your capital every year in retirement.

Trouble is, every few years you get a situation like this:

As you can see, you’d be forced to sell shares of Microsoft (MSFT) and withdraw your money at exactly the wrong time (orange line). Microsoft’s dividend is fine (blue line), but you still need to sell shares for extra income.

Remember dollar-cost averaging, which you may have used to build your nest egg? This is the same phenomenon but in reverse! In this scenario, you’re selling more shares when prices are low and fewer when prices are high.

It’s a straight path to prematurely running down your savings. And it pains me that so many folks take it as gospel.

But don’t despair, because there’s an easy solution: build a retirement portfolio with an outsized dividend yield. I’m talking a 7% average payout or better!

That’s about 4 TIMES what you get from the average S&P 500 stock—and enough to let you generate a $40,000 income stream on a nest egg that’s about one-third of what most folks would need to get an income stream like that.

I’ll show you the 3 investments that hold the key just a little further on.

But bear with me, because before we build our high-yield retirement portfolio, we need to purge “sacred cows” that look safe but actually drain your returns—starting with these 3:

Fixed Income

As I write, 10-Year Treasuries yield barely 1%. You could get close to that with a CD … if you lock away your cash for 5 years.

That’s a lot to ask for such a pathetic yield! And it’s the definition of “dead money,” because you’ll get no capital gains, just your cash back after the 5 years is up.

This may sound safe, but don’t forget that inflation. It’s running around 2% now and will eat almost all of that 2%, leaving you right back where you started!

And even if you did try to retire on it, you’d need to invest more than $2 million to drive a $40,000 yearly income stream, which I’d consider to be a livable retirement income for many folks across the country—and generating a nest egg that big just isn’t realistic for most of them.

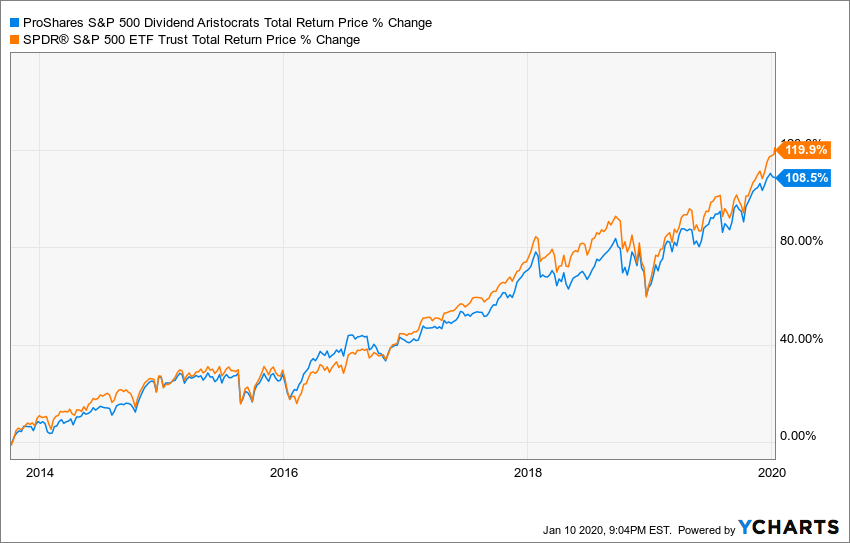

Dividend Aristocrats

You’ve probably heard of these 57 companies, which have raised their dividends annually for 25 years. Some of America’s best-known firms make the cut, like Walmart (WMT), 3M (MMM) and McDonald’s (MCD).

And there are some decent picks among the so-called aristocracy. But the average Dividend Aristocrat, as measured by the ProShares S&P 500 Dividend Aristocrats ETF (NOBL), yields only slightly better than the 10-Year: just 1.4%! So you’d need north of $2.8 million just to get our theoretical $40,000 income stream.

Worse, your average Aristocrat has underperformed the S&P 500 since NOBL was launched in 2013—even when you include dividends!

That’s disappointing because dividend growth is the No. 1 driver of share prices, so these companies should have a built-in edge.

The problem? Too many Aristocrats—AT&T (T) and Colgate-Palmolive (CL) among them—deliver tiny yearly increases just to stay in the club, and it’s not enough to tempt the income-starved to pile in and drive up their share prices.

Consumer Staples Stocks

The third “sacred cow”? Consumer staples stocks with household names like General Mills (GIS), Coca-Cola (KO) and Kimberly Clark (KMB).

The conventional wisdom says it’s smart to put your nest egg in these stocks because people buy their products no matter what the economy does.

But it’s not that simple. Because many big consumer staples names are falling behind the lightning-fast changes we’re seeing in society today.

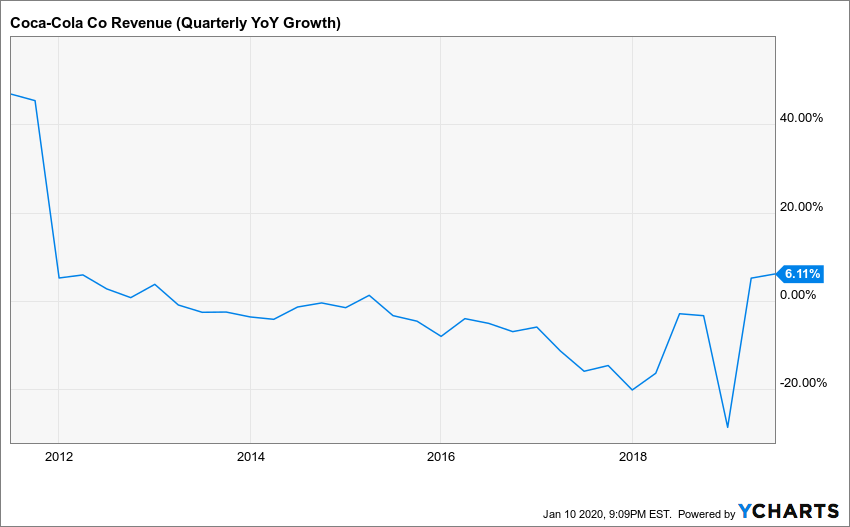

Take food stocks, which are being steamrolled by the trend toward fresh and natural foods and away from packaged fare.

And make no mistake, homegrown competitors are eating the big guys’ lunch. You can see it in the sales figures over at Coke:

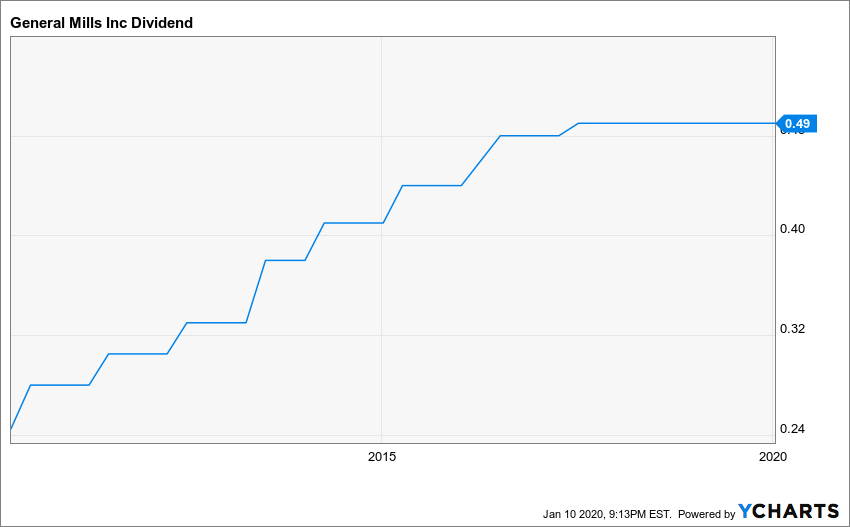

Meantime, folks look at General Mills (GIS), see it yielding a “generous” 3.7%, and think it’s a good buy. The problem is that anyone who bought this “safe” stock three years ago has suffered a 13.7% price decline:

Unfortunately these investors bought the wrong chart for investment income. They wanted the stock’s payout, but were steamrolled by the stock’s price decline while they waited.

Wouldn’t it be nice if you could collect the dividend without the price risk? For example, General Mills’ dividend never goes down. Isn’t this a better bet for retirement income?

Too bad the dividend-only chart isn’t for sale! There was a time you could count on their dividend so much that they became a “must have” stock.

General Mills isn’t really a “must have” stock anymore, though. Sagging demand for Cheerios and Green Giant Peas have weighed on its profit (and hence, dividend) growth in recent years.

We need to do better—and crushing these 3 so-called “safe” asset classes (and 6 overhyped stocks) is a lot easier than most folks think. You just need to venture a little outside the “sacred cows” of the S&P 500.

The best news is you don’t even have to crack open a quarterly report or click over to your favorite stock screener, because I’ve done all the work for you!

So let’s move on to our 3 winning retirement buys, starting with…

BIG Dividends From Closed-End Funds

Here’s something most folks don’t know: you can double, triple or even quadruple your dividend payouts simply by switching from the average S&P 500 stock to a closed-end fund (CEF).

And you can often do it without even switching investments!

Here’s just one example: if you own JPMorgan Chase (JPM) or American Express (AXP), you can trade them in and grab a 6.1% dividend from the Gabelli Dividend & Income Trust (GDV), which has both stocks in its top 10 holdings.

Better still, GDV trades at an 8.6% discount to net asset value (NAV, or what its underlying portfolio is actually worth).

Don’t get too hung up on the jargon here; what that means is that this is free money! You’re basically getting access to GDV’s top-flight portfolio and management team (more on them in a moment), for a little over 92 cents on the dollar.

Aside from some nice upside, that discount also has a knock-on effect most folks forget about: it makes the dividend safer, because fund manager Mario Gabelli only has to make 5.8% of NAV—not the 6.1% yield on GDV’s market price—to keep its payouts coming.

That’s a cinch for a seasoned vet like Gabelli, a value-investing legend who’s racked up a ton of awards for his disciplined style.

One of the latest: the New York Society of Security Analysts’ Lifetime Achievement Award.

If that sounds like an obscure group to you, that’s because it is. But here’s the upshot: this is not an easy bunch to win over! The NYSSA’s very obscurity and off-the-radar approach mean it gives awards much more conservatively than most investment firms and media outlets.

Finally, there’s Gabelli’s five-person portfolio-management squad, which is stocked with Columbia Business School MBAs and has over 80 years of combined experience in fund management, plus connections with some of the biggest investment banks on Wall Street.

Now let’s move on to…

Bargain-Basement REITs

Real estate investment trusts—owners of properties ranging from apartments to self-storage units—don’t pay income taxes so long as they hand over most of their earnings to shareholders.

That means bigger dividend checks for us!

Take bargain-priced hotel operator Apple Hospitality REIT (APLE), owner of 233 modern hotels under the Marriott and Hilton banners—and payer of a gaudy 7.6% dividend yield!

Not only that, this unloved dividend champ pays dividends monthly.

And when I say “modern,” I mean it: the average age of Apple Hospitality’s portfolio is just four years. But if you hear “hotels” and think “Airbnb,” let me drive that elephant from the room now, because Apple Hospitality makes a policy of going where the home-sharing giant isn’t.

Suburban markets chip in around 56% of the REIT’s adjusted hotel EBITDA (earnings before interest, taxes, depreciation and amortization). Airports, resorts, smaller cities and interstates supplied around 19%. That means Apple Hospitality has prime position in areas that are prime growth hotspots as the US economy surges, while sidestepping the mostly downtown home-sharing competition.

Nonetheless, that overblown fear and another overblown fear—the worry that interest rates will hurt REITs—have APLE trading at just 11 times modified funds from operations (FFO, the REIT equivalent of earnings per share).

That’s absurd for a REIT that’s adding state-of-the art hotels in terrific locations while easily covering its dividend: APLE paid out just 78% of trailing-twelve-month FFO as dividends, very low for a REIT—especially a well-run one like this. Grab it now, before you lose your chance to buy cheap!

“Preferred” 7.1% Payouts From Your Favorite Stocks

Preferred stocks are stock-bond hybrids that can trade on exchanges, like common stocks, but trade around a par value and dole out a fixed regular payment, like a bond.

Their biggest appeal? Massive payouts! Many preferreds boast payouts of 7% and up.

Trouble is, the preferred-stock world can be complex, so my favorite way to tap into them is through, you guessed it, closed-end funds. This puts a pro to work spotting the best opportunities for us. And when it comes to preferreds, the human edge makes all the difference.

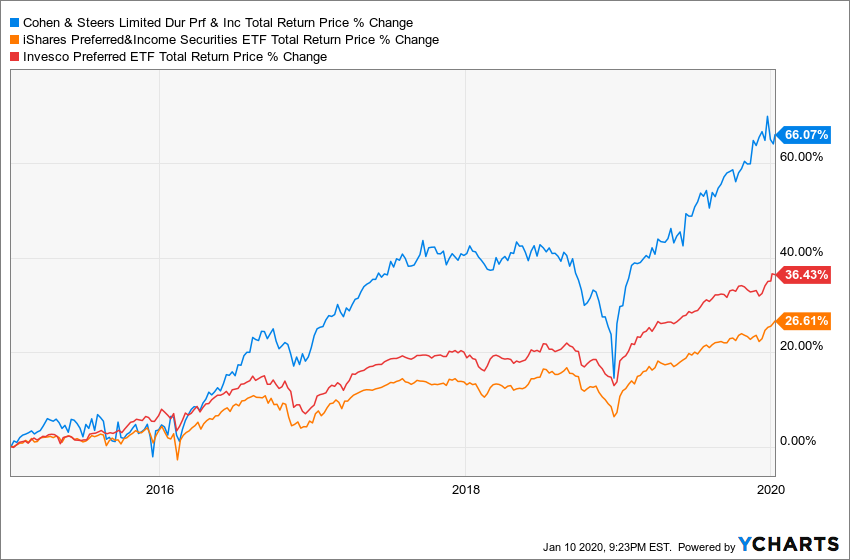

Take the Cohen & Steers Preferred Securities and Income Fund (LDP), which boasts a fat 7.1% dividend yield and a management team on par with that of GDV.

Cohen & Steers executive vice-president William Scapell and senior vice-president Elaine Zaharis-Nikas manage LDP, and this duo has 49 years of experience between them.

Their track record speaks for itself: they’ve crushed two of the most popular “dumb” preferred funds since they launched LDP, racking up a 66% total return in the last 5 years.

Even if the competition had been closer, I’d still go with LDP due to its 7.1% yield, which trounces the 5.3% PowerShares Preferred Portfolio (PGX) and the 5.9% iShares S&P U.S. Preferred and Income Securities ETF (PFF), shown in the red and orange lines above, pay.

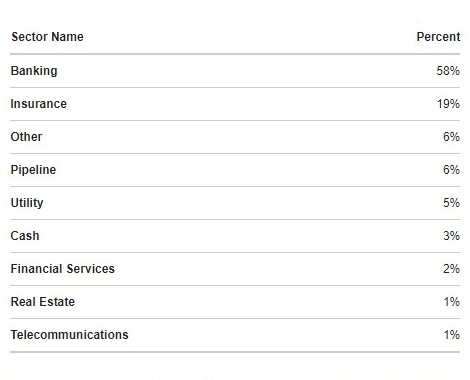

Financial stocks are the main issuers of preferreds, and that’s reflected in LDP’s portfolio:

Even better, you won’t have to worry about your money heading off to wobbly corners of the earth here: stable countries like the US (31% of assets), Japan, France, Switzerland, Canada and Australia dominate LDP’s portfolio.

Which brings me to LDP’s valuation. The fund trades at a 1.1% discount to NAV. That gives you little built in upside, plus some nice downside protection while you collect the fund’s gaudy 7.1% payout.

The bottom line? Throw APLE, GDV and LDP in together and you’ve got an “instant portfolio” with a 7% yield—enough to hand you over $40,000 of yearly income on a $600,000 upfront investment.

But we’re not stopping there! Because your best strategy is to go just one step further and …

APLE, LDP and GDV are terrific buys now, but let’s be honest, $600,000 is still a lot of money for many folks to save.

So what if I told you that you could kick-start that same $40,000 income stream on even less cash—$100,000 less, to be exact.

That’s right: $40,000 of income every year on just a $500,000 nest egg.

Oh, and you’re getting a lot more diversification here, because we’ll spread your cash out over 6 rock-solid investments instead of just 3 (and yes, they’re CEFs, REITs and preferred-stock funds).

They’re all in my 8% “No-Withdrawal” retirement portfolio, which I’ve custom-built to protect your nest egg in a downturn and deliver an 8% average dividend all the time, easily enough to hand us $40,000 a year on just $500,000 in savings!

Best of all, you won’t have to worry about outliving your cash, because unlike Wall Street’s deadly 4% plan, you won’t have to draw a single penny of your capital in retirement!

And to show you just how much the “No Withdrawal” strategy can juice your income, I’m going to do something I don’t normally do.

I’m going to share my absolute favorite picks—normally reserved for premium subscribers to my Contrarian Income Report research service—free, right here, today.

My publisher isn’t happy about this, but I like these high-yielders so much that I want to show them to as many investors as possible. And naturally, I’m hoping you’ll give me the opportunity to show you more double-digit dividend growers just like it.

So, if you’re ready to kick start your “No Withdrawal” retirement, I’d like to give you three additional reports on each of the strategies mentioned above, including my absolute favorite recommendations, reserved exclusively for premium subscribers…

Special Report #1 (a $99 value)

The first is called the Monthly Dividend Superstars: 8% Yields With 10% Upside.

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on each of my three favorite CEFs, including:

- An 8.1% payer that’s set to rake in huge profits from an artificially depressed sector,

- The brainchild of one of the top fund managers on the planet that pays 9.1%,

- And a rock-steady 6.5% dividend trading at a massive discount to NAV.

Special Report #2 (a $99 value)

The second guide is called Preferred Shares: Looking Past Common Dividends for 6.5% Income.

Inside you’ll find my favorite fund for investing in preferred shares, along with its management profile and investing strategy.

The fund pays 6.5% today. High yield is great, but its best quality may be its lack of correlation with the broader stock market. The shares this fund owns are preferred in every sense of the word – meaning it gets paid its fat dividends no matter what the broader market does.

Special Report #3 (a $99 value)

Your third guide, Recession Proof REITs: 2 Plays With 8% Yields and 25% Upside, reveals the two REITs I recommend only to premium subscribers. They include:

Your third guide, Recession Proof REITs: 2 Plays With 8% Yields and 25% Upside, reveals the two REITs I recommend only to premium subscribers. They include:

- The 8.2% payer uniquely positioned to thrive in the current interest rate environment, and

- A 7.9% “unicorn” that’s increased its payout by 36% since 2015!

In each report you’ll get the rationale behind where, why and how to profit. In short, everything you need to know about these stocks before you invest a single penny.

How to Get All 3 Reports Absolutely Free

To access all three reports at no cost whatsoever, I simply ask that you take a risk-free trial of my research service, Contrarian Income Report.

I created Contrarian Income Report to help self-directed investors uncover overlooked and under-appreciated income plays before Wall Street and the mainstream herd bid them up.

Right now, there are 20 high-yield stocks and funds in our CIR portfolio, and you get instant access to each one the moment your no-risk trial starts.

PLUS you’ll get my next 2 NEW monthly issues.

Every new investment you get in Contrarian Income Report comes with a simple guarantee: it will pay SAFE 6% dividends—or better.

And 6 holdings in our portfolio go way further than that, delivering 8%+ income right now.

So just by “swapping out” your blue chips for these high-powered dividend stars, you could double, triple—or even quadruple—your income. And you could do it TODAY!

But don’t take my word for it. Here’s what some of my subscribers have to say about these recommendations:

Mark M. from Michigan wrote:

“Contrarian Income Report has made a big difference in my retirement income and I am very glad I found this report. My dividend income is up almost 25% since I converted everything to the Contrarian portfolio.”

B.E. from Alaska said:

“Instead of paying [my advisor] $16,000 a year to invest my money, I am receiving $86,000 per year in dividends in my IRA, and $24,000 tax free dividends in our taxable account. I very much appreciate all the work that you guys do.”

Craig R. from Pennsylvania told us:

“Just wanted to write and let you know I’m very pleased with my subscription to your services… Keep up the good work! I sleep better at night not worrying about the daily gyrations of the market. I’m very glad I found your service.”

J.C. in California wrote:

“I love your insights and as a financial advisor the way I invest my clients’ money many of your newsletters provide me with new ideas to explore and work hand in hand with my value approach. You make my job easier and I appreciate that.”

Scott G. from Indiana said:

“We have been extremely pleased with Brett’s Contrarian recommendations and have friends getting ready to join! We are lifers!”

Richard W. from Massachusetts wrote in to say:

“I have subscribed to several of the biggest advisory services (a couple are even ‘lifetime’ subscriptions) but those from Contrarian Outlook are my favorites and the only ones I actually act on these days.”

Tom I. from Florida told us:

“I’m very happy with your service. It solved my retirement income dilemma which is an incredible relief. Thank You!”

Now, the regular member price to join Contrarian Income Report is $99 per year, but I’m sure you’ll agree it’s well worth the cost. Heck, the three reports you’ll get absolutely free are worth three times that much.

And even a small position in any one of the picks inside will easily cover that in just the first few months.

Imagine 7%, 8%, even 9% dividends rolling in from these picks, and then watching them appreciate as mainstream investors realize what they’ve been missing and inevitably pile back in.

But it’s important that I earn your trust and you have the chance to see exactly how profitable this service can be.

So I’ve arranged for a small number of investors to take 60% off the regular price and try out Contrarian Income Report for just $39.

And I’m so confident you’ll enjoy (and profit from) this service that I’m going to give you 60 days to try Contrarian Income Report absolutely risk-free.

If, after nearly 2 months, you don’t feel the advice has more than covered your cost, or if it’s just not right for you, simply let me know and I’ll issue a full refund.

That’s 100% of your money back, no questions asked.

Plus you’re welcome to keep all of the special reports with my thanks for trying it out.

If you’re ready for 8%+ income and double-digit capital gains, simply click here to get started right now.

Yours in payout profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

P.S. Since my recommendations are contrary to prevailing popular beliefs, they have a habit of rallying quickly as soon as the mainstream herd catches on to what they’ve been missing. I encourage you to get started right now so that you can get in at a good price!

P.P.S. Remember, your risk-free membership comes with the names and full details on my top 3 closed-end funds paying up to 9.1%, dividends up to 8.2% from my top REIT plays, and the Preferred fund that will hand you 6.5%. Even a small position in any one of these picks will easily cover a full year’s membership… most likely before your 60 day trial even ends!

Nothing in Contrarian Outlook is intended to be investment advice, nor does it represent the opinion of, counsel from, or recommendations by BNK Invest Inc. or any of its affiliates, subsidiaries or partners. None of the information contained herein constitutes a recommendation that any particular security, portfolio, transaction, or investment strategy is suitable for any specific person. All viewers agree that under no circumstances will BNK Invest, Inc,. its subsidiaries, partners, officers, employees, affiliates, or agents be held liable for any loss or damage caused by your reliance on information obtained. By visiting, using or viewing this site, you agree to the following Full Disclaimer & Terms of Use and Privacy Policy.