This “Iron-Clad”

11% Dividend Is the

Cure for Market Chaos

The deadline for grabbing its next

monthly distribution is days away.

You do NOT want to miss it.

Dear Reader,

The 12% dividend I’m pounding the table on now is the cure for the stress many investors suffer from these days.

A bold claim, I know.

But here’s the thing: The fund throwing off this huge cash payout is run by one of the best managers in the business.

He’s been recognized by his own peers as one of the “kings” of fixed income.

And how’s this for swagger: He’s not only kept that huge payout steady through bull and bear markets, he’s grown it.

He’s no stranger to special dividends, either: They’re nice “bonuses” his lucky shareholders can always look forward to.

The kicker? Since special dividends don’t show up on regular stock screeners, our real yield could be much more than 12%.

The bottom line here is that this rock-solid fund gives us a valuable “dividend shield.”

When you add it to your portfolio, it could help bolster your income stream, and investment capital, no matter what storms (from the Fed, DC or elsewhere) hit.

The Ultimate “Set-It-and-Forget-It” Play (Except When Your Monthly Payout Arrives!)

This 12% dividend is the kind of long-term play our parents would have recognized—with one thing they definitely wouldn’t.

You probably remember that, back in their time, most investors simply bought a collection of large cap stocks—maybe a few of the so-called “Nifty 50,” which soared back in the 1960s and 1970s and included household names still around today.

McDonald’s, Pfizer, Johnson & Johnson, 3M. These are just a few examples of stocks from our parents’ (and in many cases grandparents’) time that have stood the test of time.

Once bought, folks mostly forgot about these holdings, until their latest investment statement showed up in the mail.

But as solid as the stocks they bought back then were, they had one flaw. It’s the same one they have now. Lousy dividends!

That’s where this unique 12%-paying fund comes in.

I think you’ll agree that a predictable payout like this goes a long way toward simplifying our lives, not least because its payout rolls in monthly, right alongside our monthly bills.

And that’s before we talk about the real dollars and cents behind a double-digit payout like this.

At a 12% yield, it amounts to $1,000 every month on a $100k investment …

$24,000 in yearly dividends on $200k …

And if you invest half a million, you’re looking at $60,000 per year.

That’s a decent middle-class income in many parts of the US!

Got more? Great!

A $1-million buy-in would land you $120,000+ in dividends every single year!

With that kind of income, you really can tune out Mr. Market—and sit back and wait for your next monthly “paycheck” to roll in!

That’s exactly the kind of income (and peace of mind) we all need these days.

And that’s before we even talk about the upside here. Let’s get into that now.

This 12% Yielder Looks Poised for Stock-Like Gains

I’m also imploring readers to grab this fund now because it’s set up for big capital gains as the Fed shifts toward interest-rate cuts.

Why am I so confident that will happen?

First, because the Trump administration specifically appointed new Fed chair Kevin Warsh to bring down rates.

As a result, I expect him to start calling for rate cuts as soon as the data lets him justify doing so.

But the second, and much more important, reason is AI which provides a sweeping level of automation to white-collar work that is highly deflationary.

In the 1990s, the Internet acted as a similar “deflator” on prices. The move from snail mail to email and from fax machines to web browsers made businesses wildly more efficient, which kept a lid on consumer prices—and a floor under bond prices. They rallied throughout the entire decade.

That’s a key parallel for this 12%-paying fund’s holdings: high-yield credit, a.k.a., corporate bonds.

Because when interest rates move lower, new bonds will be issued at lower rates, driving up the value of our 12%-payer’s already issued bonds.

As that happens, our high-yielding pick will jump from relative obscurity to the top of many “first-level” investors’ buy lists.

The bottom line:

We’ve got a 12% dividend here, and a shot at price upside, too!

Even better, there’s something else you should know …

In addition to its monster 12% yield, this fund has a history of actually growing its payout: Since its inception around four years ago, it has already increased its regular dividend by 8% and has paid two special dividends, too!

A Dividend Hike Plus 2 Big “Specials”

Sure, these special dividends and raises are great news for current investors in the fund. But there’s something else few people realize about them …

They don’t typically show up in the yield calculations on the free stock screeners, like Yahoo! Finance and Google Finance.

This means that the fund’s 12% stated yield could turn out to be an undercount.

Now I’m not going to claim this is the norm for the fund. Fact is, no one can say for sure what management will do when it comes to future dividend hikes and special payouts.

But this track record shows that management isn’t afraid to drop a nice bundle of extra cash on shareholders when the time is right. So we can assume our buy now locks in a 12% “starter yield,” with plenty of potential to move higher.

Why This 12% Payer Is a “Must-Buy” Right Now

Before I tell you more about this breakthrough fund, let me first take a moment to introduce myself.

I’m Brett Owens, chief strategist of the Contrarian Income Report high-yield investing service.

My colleague Tom Jacobs and I literally wrote the book on how to build an income portfolio that throws off cash payouts big enough to live on.

In How to Retire on Dividends: Earn a Safe 8%, Leave Your Principal Intact, we lay out a simple, yet radical, plan: Fund your entire retirement from dividends of 8% and up… without drawing down your nest egg.

To make sure our investments give us enough dividend cash to live on without having to invest seven figures, we really need yields in the 8% to 10% range, and even higher.

And that’s exactly what today’s overlooked 12% payer allows you to do.

And the key to our opportunity here is the fact that this isn’t just your typical mutual fund or ETF — it’s a special kind of fund called a closed-end fund (CEF).

CEFs are like “regular” stocks and ETFs in that they trade openly on the public markets.

You can buy and sell them easily from almost any standard brokerage account. And CEFs hold the same assets that ETFs hold.

You can buy CEFs that hold blue chip stocks, corporate bonds, real estate investment trusts (REITs), you name it.

The difference? Dividends! Right now, for example, the average CEF yields around 8%.

So simply by “swapping out” your ETFs and individual stocks for CEFs, you could go from, say, the 1% average dividend the typical S&P 500 stock pays to north of 8% — a nearly sevenfold increase!

And that’s just the yield on the average CEF. Many, like this 12% payer, deliver MUCH more — massive dividends yielding 10%+ are readily available in the CEF market.

That’s EXACTLY what makes CEFs such incredible wealth generators.

And they are proven. We’ve ridden these income generators to big gains again and again in my Contrarian Income Report high-yield investing service.

Here are just a few of the returns, including dividends, we’ve posted in CEFs:

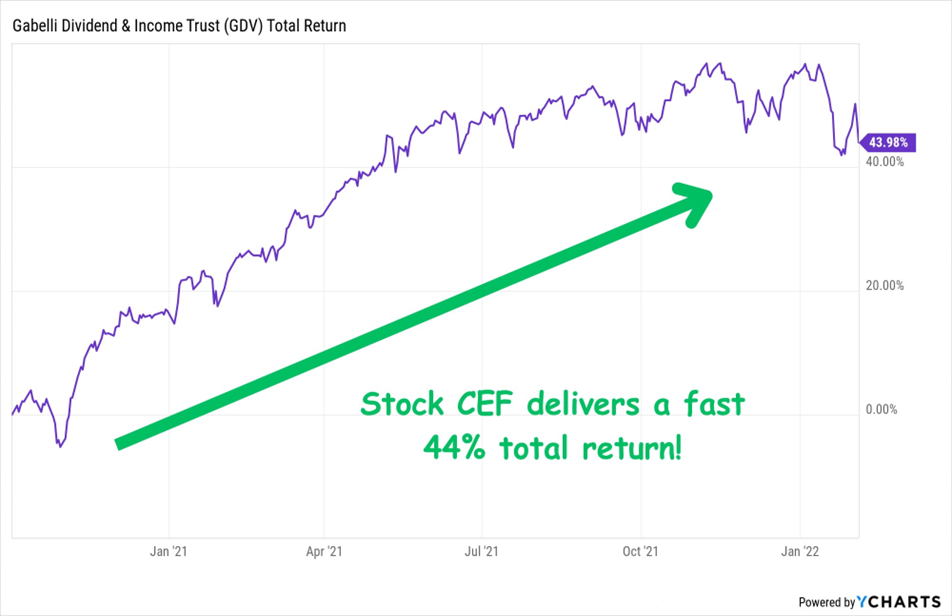

A Blue Chip Stock CEF That Returned a Sparkling 44% in 15 Months

14.6%-Paying Bond CEF Has Returned 42% in a Just Over 3 Years

A “Boring” Infrastructure CEF That Delivered a 95% Return

And talk about dividends!

That blue chip fund, the Gabelli Dividend & Income Trust (GDV), paid a healthy 7.3% when we bought.

The PIMCO Dynamic Income Fund (PDI)? An incredible 14.6% at the time.

And the utility-focused Cohen & Steers Infrastructure Fund (UTF) was throwing off an 8.8% cash stream, nearly triple what the typical utility yielded.

Do all of our calls work out like this? Of course not. I wouldn’t insult your intelligence and suggest they do. Investing involves some risk, even with top-quality funds like these, and you can lose money.

But I think you can see where I’m going here: Buying attractively valued CEFs with big dividends and savvy managers is a proven way to build wealth over time.

And the bond-buying pro running the fund we’re targeting today is, hands-down, the savviest of the bunch.

Morningstar previously named him a Fixed Income Manager of the Year, and he has been inducted into the Fixed Income Analysts Society Hall of Fame.

When he took the top job at his management company, he displaced the firm’s founder — a legend who revolutionized bond trading in the ’70s and ’80s. His long-term track record is a matter of public record.

Check out the drubbing he’s laid on the corporate-bond benchmark (orange line) through another of his firm’s CEFs since he took over as his Group CIO (knocking off that bond legend I just mentioned) a little over a decade ago (in purple):

Our Income Pro Clobbers Corporate Bonds

That’s no fluke. Since March 30, 2007, one of his company’s most established mutual funds has soared 256%.

And since the benchmark ETF for corporate bonds, the State Street SPDR Bloomberg High Yield Bond ETF (JNK), launched later that year, this fund has crushed it:

Another Big Win for Our Bond Pro

Our manager also has a team of 4 other bond experts backing him up that, between them, boast 90+ years of experience.

So we can be sure we’re getting the cream of the crop working for us here — and that’s particularly critical in the small world of fixed income, which isn’t as “democratic” as stocks.

Well-connected managers get the first call when new issues roll out, and our top-flight manager and his team are at the top of the “to-call” list.

This, by the way, is why we always go with CEFs over ETFs for our bond picks. ETFs are simply tied to a “robotic” bond index — so there’s just no way they can compete.

A One-Time Chance to Buy Into

the “Amazon of CEFs”

One more thing we should be clear on is that the company that runs this 12% payer really is the top name in the CEF space — I consider them the “Amazon of CEFs,” in fact.

As such, its funds almost always trade at premiums to NAV, or the net asset value of the issues they hold.

Heck, as I write to you today, one of this company’s CEFs trades at a 17% premium!

Investors have fallen so in love with that fund that they’re willing to pay $1.17 for every dollar of its assets!

When you look at the performance charts above, you can see why.

This team is proven.

But because our 12%-yielder is only a few years old, CEF investors, conservative sorts they are, haven’t warmed to it yet. It trades at a premium, too, but a much smaller one that’s really a discount in disguise for this firm’s funds.

The bottom line is that when our pick hits premiums at which its sponsor’s funds normally trade, it’ll drive the share price up double-digits.

And that’s BEFORE the “baked in” additional upside we’ll see as rate cuts kick in.

Plus, this one has a broad mandate, so we get our elite manager completely unchained and working for us.

He’s not limited to ANY specific kind of bond.

Instead, he’s free to use his proven talents, his firm’s vast research resources and, yes, his deep contact book to get first crack at the best new issues, whether they’re high-yield corporates, ultra-safe municipals or — a specialty — mortgage-backed securities (MBS).

Yes, these were the investments that touched off the 2008 crisis, but they’ve been regulated (and regulated and re-regulated!) since.

That makes them yet another savvy contrarian play in this fund’s portfolio now. Especially as many mainstream investors who haven’t taken the time to research them still panic when they hear the name.

That’s our cue to punch our ticket — before our “contrarian-in-chief” makes his next big buy, and before this fund’s next payout-cutoff date arrives.

I Want to Give You Full Details on This

Bargain-Priced 12% Payer Now

I’ve put all the details on this life-changing 12% payer into a NEW Special Report I call “The One 12% Dividend to Own Now.”

Inside I’ll give you my full research on this incredible income play, including its name, ticker, updated yield, valuation and — the best part — my complete take on its class-leading manager, who delivered that benchmark-crushing performance I mentioned a second ago.

This well-connected bond-trading pro is, quite frankly, the No. 1 bond investor of his generation.

He came out of nowhere, ably stepping in and cranking out doubles, triples and the occasional home run after the founder of his company left in a huff.

Now, with 4 other top managers and the deep resources of his firm — as I said, it’s practically the “Amazon of CEFs” — behind him, he’s ready to go to work for us.

You’ll get everything you need to know about this top bond trader, his team and our fund in “The One 12% Dividend to Own Now.”

Inside you’ll discover:

- The name, ticker and all the vital stats on this breakthrough 12%-paying income generator.

- The backstory on the seasoned vet who runs the fund and a deeper look at the team in charge.

- How it beats bond ETFs in every way: dividends, performance history, future gains, you name it.

- The full scoop on its NAV, a critical forecaster of future gains that most people have overlooked.

- And most important … the timing of its next “cutoff” date and its next monthly payout.

Now I want to invite you to start profiting from this revolutionary pick — today, while we can still lock in that massive 12% yield, and before it drops its next big payout.

I’m Going to GIVE You This Special Report Naming My Top 12%-Paying CEF — FREE

To access this exclusive Special Report at no cost whatsoever, I simply ask that you take a risk-free 60-day trial of my research service, Contrarian Income Report.

I created Contrarian Income Report to help investors uncover overlooked and underappreciated income plays before Wall Street and the mainstream herd bid them up.

Income plays like our 12%-paying bond play, which fit our playbook perfectly.

People often ask me, “I get the income part, but where does ‘contrarian’ fit in?”

My answer is simple: You’ll never beat the market by following the herd.

If you buy the same investments as everyone else, you’re going to have the same results as other people — which are always mediocre.

This is why my advisory is defiantly contrarian.

It all boils down to one simple principle: If you want to make money, really big money, do what nobody else is doing.

Contrarian investing is probably the simplest, sanest, most powerful and reliable money-making technique ever devised to buy low and sell high.

It works in any market, from stocks and bonds to gold and real estate — because human nature is the same everywhere.

You don’t need special training. All you need is an independent mind, a bit of patience and an ounce of courage.

If you want to buy low and sell high, you must be prepared to buy when everybody, including yourself, is feeling discouraged — when the news is bad. That’s likely to be the bottom. And be prepared to sell when everybody is excited and the news is good, because that’s likely to be the top.

Right now we’re holding a diverse portfolio of 20+ high-yielding stocks and funds with an average yield of 8%, and you’ll get instant access to every single one the moment your no-risk trial starts.

And every new investment you get in Contrarian Income Report comes with a simple goal: it will pay a reliable 5% dividend — or better.

In fact, some holdings in our portfolio go way further than that, including the 12%-paying bond fund you’ll discover in the pages of your FREE report — coming your way in just a second.

So just by “swapping out” your anemic blue chips for these cash cows, you could double, triple — or even quadruple — your income. And you could do it TODAY!

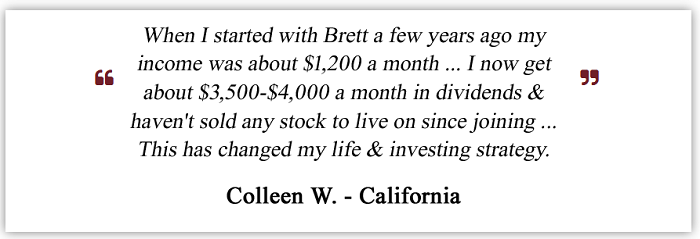

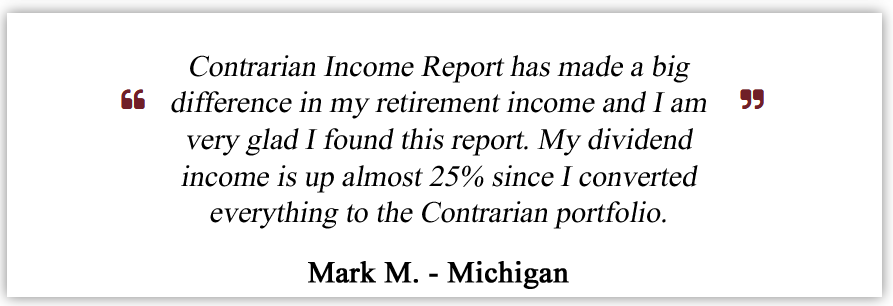

That sort of money can upgrade your lifestyle in a hurry. Take it from my subscribers:

Of course, not everyone follows my recommendations at the exact same time or in the same way. Each member’s personal financial situation is different, so your experience may also be different… but I’m thrilled to say we’ve received dozens more anecdotes similar to these.

Now let’s talk about what you can expect with Contrarian Income Report.

High, Safe Yields Are Only the Beginning

In addition to full details on my 12%-paying income fund, you’ll get ALL of the high-yield picks in our Contrarian Income Report portfolio, which is packed with payers yielding 8%, 9%, 12% and one fund yielding an incredible 16% as I write this.

Plus your risk-free trial look at Contrarian Income Report includes a whole lot more, such as …

- Full portfolio access. You’ll have immediate access to every pick I make, including my exact buy and sell recommendations and “buy-under” prices.

- New income investing ideas and analysis of major market events delivered straight to your inbox every single week.

- Flash Alerts, with breaking news on our portfolio stocks. I’ll have an eye on all of them 24/7.

- Monthly research bulletins — On the first Friday of each month, you’ll receive my latest research, including new portfolio additions, updates on existing positions and an overview of trends and events that may affect our holdings.

- Members-only website — You’ll get access to a password-protected website where you can access all of our resources: current and past issues, special bonus reports, and our full portfolio. Whenever you want to check on our recommendations, everything is there for you, day or night.

- Exclusive Webcasts — Several times each year, you can join me for a live, members-only webcast. We’ll run through what’s going on with our holdings and I’ll personally answer your questions.

- VIP Customer Service — If you ever have questions about your subscription, you can email our team anytime, or call our New York office during regular business hours and receive a prompt reply.

Now, the regular member price to join Contrarian Income Report is $99 per year.

That’s a modest sum considering everything that’s included. But I want you to see firsthand exactly how profitable this service can be. And I don’t want the subscription fee to get in the way.

So I’ve arranged for new members to receive an introductory discount of 60% off the regular price and to try out Contrarian Income Report for just $39. (Note: this offer is valid for new subscribers only.)

And to start you off with everything you need to hit the ground running, I’m going to include three more incisive Special Reports, giving you a complete library of high-yield opportunities and strategies to pick from …

Extra Bonus #1: “5 ‘All-Weather’ Dividends

Paying Up to 10.1%”

This unprecedented period in history has created a classic stock picker’s market — where you can find businesses that are being completely mispriced and completely misunderstood.

I explain exactly why and how in an exclusive Special Report called “5 ‘All-Weather’ Dividends Paying Up to 10.1%.” It also includes all the details on some of my absolute favorite buys right now, including:

- A unique bond fund run by a savvy manager who’s smartly used the big dips in the bond market over the last five years to snap up bonds with high credit quality and big yields.

That, plus a modest amount of leverage, is helping him deliver 10.1% payouts to this fund’s lucky shareholders.

- A fund that thrives on volatility, holds the blue-chip stalwarts we all know well and yields 8.4%.

- And a rock-steady lender that not only loans to companies but takes direct stakes in them, too. That gives it not one but two growth engines, which it uses to fund the rich 8.4% dividend it sends our way.

All of these investments can be bought inside your regular US brokerage account. Together they can give your income portfolio tremendous diversification and the type of ongoing income that will hold up no matter what happens with inflation or the Fed.

Taken together, these 5 picks line up perfectly with the high yielders in your next bonus report:

Extra Bonus #2: The Perfect Income Portfolio

In your second guide, you’ll get all the details of what I call the “Perfect Income Portfolio.”

Step-by-step, I’ll show you exactly how to set up your portfolio for maximum income without taking on additional unnecessary risk.

And, if you follow the simple steps laid out, I’m confident you’ll be able to enjoy an income stream that far exceeds what most folks who buy the typical S&P 500 stock earn.

This report includes investments that have passed my strict due-diligence process—including one of the best ways I’ve ever seen to invest in utilities (which I’ve picked for further gains as interest rates move lower in the longer term).

This fund pays a rich 7.2% today, holds some of the strongest electrical utilities in the country and trades at a bargain valuation (even though most investors don’t realize it). Its bargain status won’t last as rates tilt lower, pulling more investors toward its healthy payout.

Extra Bonus #3: The Dirty Dozen: 12 Dividend

Stocks to Sell Now

As much as I love a fat payout, I never let myself forget that an extraordinary yield can be a warning sign of a stock in trouble.

A high yield that was too good to be true is easy to spot in hindsight. But when a cut, and the resulting share price plunge, are unfolding, most “yield junkies” are intoxicated and just can’t let go … and ride the stock to the bottom.

I’m afraid we’re in for just that scenario with the 12 popular income stocks in this report.

Like a popular toy maker yielding 3.3%. Too bad it’s stuck in the world of “physical” games and toys, as most kids now get their fix online…

Or the global shipping company that’s one of the last firms anyone would expect to cut dividends. But tariffs and a weak job market are weighing on its shipping volumes, and cash flow. The stock yields 6% today, but don’t fall for that high yield. It’s on very thin ice…

Or a landlord that rents the vast majority of its properties to the federal government. That used to be a sign of a conservative investment, but today, with Uncle Sam running a massive deficit and looking to slash costs, it’s anything but…

Another is a high-yield ETF that pays a ridiculous 60% (not a typo!). But it’s returned a shadow of what a simple index fund has since inception a bit more than two years ago, even with dividends included. That’s just a precursor of even worse returns to come.

If you hold any of these stocks — and it’s likely that you do — I urge you to dump them immediately.

Now, there’s just one more thing I’d like to include …

Our Ironclad 100% Money-Back Guarantee

Sure, investing in the stock market comes with some inherent risk and not all recommendations will be winners.

But my long track record of uncovering safe, steady dividends with the potential for serious capital gains (through some of the most vicious market reversals in history) speaks for itself.

The only question is whether this sort of investing is right for you.

Well you can find out without risking a cent … because I’m also going to give you 60 days to try Contrarian Income Report absolutely risk-free.

Here’s how it works …

Start your membership today. Download your special reports, grab a position in our 12%-yielding fund before the next payout deadline, read the current issue and start tracking a few portfolio picks that catch your interest.

Then sit back and enjoy the next couple of issues of Contrarian Income Report, check out my weekly column and all of the other member benefits.

If, after two months, you don’t feel the advice is right for you, for any reason at all, simply let me know and I’ll issue a full refund.

That’s 100% of your money back, no questions asked.

Plus you’re welcome to keep all four special reports with my thanks for trying it out.

Here’s a breakdown of everything you get when you join Contrarian Income Report today:

- Report #1: The One 12% Dividend to Own Now

- Report #2: 5 ‘All-Weather’ Dividends Paying Up to 10.1%

- Report #3: The Perfect Income Portfolio

- Report #4: The Dirty Dozen: 12 Dividend Stocks to Sell Now

PLUS…

- All past issues and reports

- 12 monthly research bulletins

- Weekly market overviews

- Flash alerts

- Private Webcasts

- A 24/7 members-only website with first-rate service

To sum it up, you get a 60% membership discount, four essential investment reports, new issues every month, weekly email updates, flash alerts, live webcasts and more.

All with a 100% money-back guarantee.

Simply click the button below to claim everything right now:

4 Special Reports, a Full Year of My Premium Newsletter, and a Bunch of Other Perks and Benefits for Just $39

One last time, add it all up and you get:

- The One 12% Dividend to Own Now

- 5 ‘All-Weather’ Dividends Paying Up to 10.1%

- The Perfect Income Portfolio

- The Dirty Dozen: 12 Dividend Stocks to Sell Now

- Plus a full-year membership to Contrarian Income Report

That’s a total value of $495 for just $39 – a 92% total discount!

And I’m confident you find it’s more than worth it.

And remember, you are fully covered by my 60-day money-back guarantee!

You have nothing to lose…

Well, except missing out on dozens of under-the-radar income ideas that could get your retirement back on track – or even ahead of schedule.

All you have to do is click the button below to get started now:

Stop struggling to get by on 2% and 3% yielders, hoping that runaway deficit spending, trade wars (or actual wars!) or the Fed don’t trigger another market crash.

It’s up to you to protect yourself, your family and your hard-won portfolio.

No one else will do it for you.

So join us today with Contrarian Income Report tap into my top 12% payer, along with the 20+ other recommendations with current dividend yields of 8%, 9%, 12% and more!

Yours in profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

P.S. These contrarian plays have been known to rally once the herd catches on to what they’ve been missing. I encourage you to act now to make sure you get in on this solid 12% income play at a bargain.

© BNK Invest, Inc. – All Rights Reserved – Legal Information