How to Live Off

$500,000… Practically Forever

In this income investing report, you’ll discover…

- How the 4% Rule and 60/40 Portfolio are now dead.

- 12 popular dividend disasters you need to dump right now.

- How you could bank tens of thousands of dollars in yearly dividend cash for every $500,000 invested, and …

- 3 incredible monthly payers dishing out dividends up to 16.2%.

Dear Reader,

A half-million dollars is a lot of money. Unfortunately, it won’t generate much income if you limit yourself to popular mainstream investments.

The 10-year Treasury pays around 4.4% as I write this. That’s not bad, historically speaking, but put your $500K in Treasuries and you’re only looking at $22,000 in investment income, right around the poverty level for a two-person household. Yikes.

And dividend-paying stocks don’t yield nearly enough. For example, Vanguard’s popular Dividend Appreciation ETF (VIG) pays around 1.5%. Sad.

When investment income falls short, retirees are often forced to sell their investments to supplement their income.

Of course, the problem here is that when capital is sold, the payout stream takes an immediate hit – so that more capital must be sold next time, and so on.

Avoid the Share Selling “Death Spiral”

Some financial advisors (who are not retired themselves, by the way) say that you can safely withdraw and spend, say, 4% of your retirement portfolio every year. Or whatever percentage they manipulate their spreadsheet to say.

Problem is, in reality, every few years you’re faced with a chart that looks like this.

General Mills’ Dividend Kept Growing – Its Stock Plunged

As you can see, the dividend (orange line above) is stable, even growing modestly — but you’re selling at a 48% loss!

In other words, you’re forced to sell more shares to supplement your income when they’re depressed.

Remember the benefits of dollar-cost averaging that built your portfolio? You bought regularly, and were able to buy more shares when prices were low?

In this case, you’re forced to sell more shares when prices are low.

When shares rebound, you need an even bigger gain just to get back to your original value.

The Only Reliable Retirement Solution

Instead of ever selling your stocks, you should instead make sure you live on dividends alone so that you never have to touch your capital.

This is easier said than done, and obviously the more money you have, the better off you are. But with yields on S&P 500 stocks pretty low these days (around 1% on average), even rich folks are having a tough time living off of interest today.

And you can actually live better than they can off of a (much) more modest nest egg if you know where to look for lesser-known, meaningful and secure yield.

I’m talking about annual income of 8%, 9% or even 10%+ so that you’re banking $50,000 (and potentially more) each year for every $500,000 you invest.

You and I both know an income stream like that is a very nice head start to a well-funded retirement.

And it’s totally scalable: Got more? Great!

We’ll keep building up your income stream, right along with your additional capital.

And you’ll never have to touch your nest egg – which means you won’t have to worry about or running out of money in retirement, or even the day-to-day ups and downs of the stock market.

The only thing you need to concern yourself with is the security of your dividends.

As long as your payouts are safe, who cares if your stock prices swing up or down on a given day?

Most investors know this is the right approach to retirement.

Problem is, they don’t know how to find the yields of 8%, 10% and higher to fund their lives.

And when they do find high yields, they’re not sure if these payouts are safe. Will the company or fund have enough cash flow to pay the dividends into the future?

And how sensitive are these payouts to the latest headline, Fed policy change or unrest on the other side of the globe?

We’ll talk specific stocks, funds and yields in a moment.

But first, a bit about myself.

My name is Brett Owens. I first started trading stocks in college, between classes at Cornell.

My name is Brett Owens. I first started trading stocks in college, between classes at Cornell.

I graduated cum laude with an industrial engineering degree — which is actually pretty popular with Wall Street recruiters.

But I couldn’t stand the thought of grinding it out in a cubicle for 80 hours a week. So I moved to San Francisco and got into the tech scene.

A buddy and I started up two software companies that serve more than 26,000 business users.

The result was a nice chunk of change coming in … and I had to decide what to do with my money.

I had seen plenty of young “techies” come into sudden cash and burn through their windfall in a year, ending up right back where they started.

That was NOT going to be me. I already had dreams of living off my wealth one day, decades before I retired.

I got plenty of cold calls from brokers wanting to “help” me. But I knew that nobody would care as much about my money as me.

So I went out on my own and invested my startup profits in dividend-paying stocks.

I’ve been hunting down safe, stable and generous yields ever since, growing my wealth with vehicles paying me 8%, 9%, even 10%+ dividends.

Over the past 15+ years, I’ve been writing about the methods I use to generate these high levels of income.

Today I serve as chief investment strategist for Contrarian Income Report — a publication that uncovers secure, high-yielding investments for thousands of investors.

Since inception, my subscribers have enjoyed dividends 5 times (and much more!) the S&P 500 average, plus big annualized gains!

And that brings me to a crucial piece of advice…

The ONE Thing You Must Remember

If I could leave you with just one nugget of investing wisdom today, it would be to NEVER overlook the incredible wealth-building power of dividends.

Few investors realize how important these unglamorous workhorses actually are.

Here’s a perfect example…

If you put $1,000 in the dividend-paying stocks of the S&P 500 back in 1973, you would have had $100,634 by the end of 2024, or 100x your money.

But the same $1,000 in the non-dividend payers would have grown to just $8,880 — 91% less.

That’s why I’m a dividend fan.

The stock market is a fantastic wealth-building machine, but it doesn’t always go straight up!

There have been plenty of 10-year periods where the only money investors made was in dividends.

And that’s what gives us dividend investors such an edge.

When you lock in an 8%+ yield, you’re booking an income stream that’s bigger than the stock market’s long-term average return right off the bat.

Of course you can’t just buy every ticker symbol out there with a flashy yield, or you’ll get burned pretty fast.

So let’s wipe the false promises of mainstream finance from our minds and start thinking the “No Withdrawal” way…

Step 1: Forget “Buy and Hope” Investing

Most half-million-dollar stashes are piled into “America’s ticker” SPY.

The State Street SPDR S&P 500 ETF (SPY) is the most popular symbol in the land. For many 401(K)’s, this is all there is.

And that’s sad for two reasons.

First, SPY yields just 1%. That’s $5,000 per year on $500K invested… poverty level stuff.

Second, consider a hypothetical year when, say, SPY fell 20%, not at all out of the question, given the multiyear run stocks have been on. Just from that alone, your $500K would be slashed to $400K.

SPY was down nearly 20% that year. That is no bueno, because that $500K would have been reduced to $400K.

The last thing we want to do is lose the money we’re getting in dividends (or more) to losses in the share price. Which is why we must protect our capital at all costs.

Step 2: Ditch 60/40, Too

The 60/40 portfolio has been exposed as senseless.

Retirees were sold a bill of goods when promised that a 60% slice of stocks and 40% of bonds would somehow be a “safe mix” that would not drop together.

Oops.

Inflation — plus an aggressive Federal Reserve, plus a (thus far) persistently steady economy — drop-kicked equities and fixed income before they went on a serious bull run in 2023, 2024, 2025 (with a brief interruption for the April “tariff tantrum”) and into 2026.

It just goes to show that bonds are not the haven guaranteed by the 60/40 high priests. They could easily plunge just as hard (or harder) than stocks in the next economic crisis.

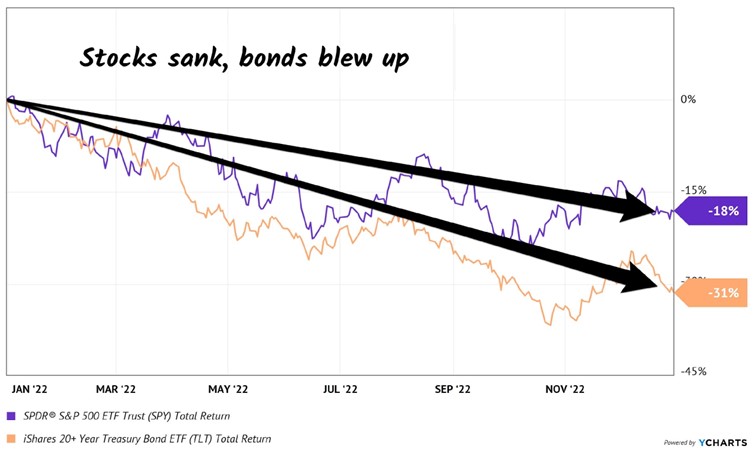

Just like they did in 2022 (sorry, we’re only going to spend one second on that disaster of a year). US Treasuries plunged, which resulted in the iShares 20+ Year Treasury Bond ETF (TLT) getting tagged.

Sure, it still paid its dividend. But even including payouts, the fund was down 31% — worse than the S&P 500. Ouch!

When stocks and bonds are dicey, where do we turn? To a better bet.

A strategy to retire on dividends alone that leaves that beautiful pile of cash untouched.

Step 3: Create a “No Withdrawal” Portfolio

My colleague Tom Jacobs and I literally wrote the book on a dividend-powered retirement.

In How to Retire on Dividends: Earn a Safe 8%, Leave Your Principal Intact, we outline our “no withdrawal” approach to retirement:

- Save a bunch of money. (“Check.”)

- Buy safe dividend stocks with big yields

- Enjoy the income while keeping the original principal intact.

To make that nest egg last, and our working life worthwhile, we really need yields in the 7% to 10% range. We typically don’t see these stocks touted on Bloomberg or CNBC, but they are around.

Of course, there are plenty of landmines in the high-yield space. Some of these stocks are cheap for a reason. Which is why we need to be contrarian when looking for income.

We must identify why a yield is incorrectly allowed to be so high. (In other words, we need to figure out why the stock is priced so cheaply!)

As I write, the top 10 payers in my Contrarian Income Report portfolio yield about 11.4% on average.

On every million dollars invested, this dividend collection is spinning off an incredible $114,000 every single year!

And you don’t have to be a millionaire to take advantage of this strategy.

A $750k nest egg would generate $85,500 annually…

$500K could hand you $57,000…

You get the idea.

The important thing is that these yields are safe, which creates stability for the stock (and fund) prices attached to them.

We want our income, with our principal intact.

It’s really the only way to retire comfortably, without having to stare at stock tickers all day, every day.

Now, many blue-chip yields are reliable. They just need to hit the gym and bulk up a bit. Here’s how we take perfectly good, yet modest, dividends and make them into braggarts.

Step 4: Supersize Those Yields

Mastercard (MA) is a near-perfect dividend stock. Its payout is always climbing, having nearly doubled over the last five years. (MA shareholders, you can thank every business that accepts Mastercard for your “pennies on every dollar” rake.)

Cash, of course, has been on the way out for years, a trend that was accelerated during the pandemic. Still, there’s plenty of it in use in the developing world, giving Mastercard plenty of additional upside.

Beyond that, the company makes money selling security software and deep-dive analytics on shopping patterns to retailers, banks and even governments.

Mastercard and close cousin Visa (V) are also turning their vast networks toward stablecoins, which are cryptocurrencies mainly pegged to the US dollar.

They’re used mainly for settling international transactions without having to go through regular banks, and Visa and Mastercard, which both run the “plumbing” of the global payment system, are nicely positioned here.

We expect more dividend hikes as a result of these moves. The only chink in MA’s armor? Everyone knows it is a dynamic dividend stock. So it only yields 0.7%. Investors keep bidding it higher, knowing that the next dividend raise is just around the corner.

So, the compounding of those hikes makes MA a great stock for our kids and grandkids. You and I, however, don’t have the time to wait for 0.7% to grow. And $3,500 in dividends on a $500K investment simply won’t get it done.

Let’s instead consider top-notch closed-end fund (CEF) Gabelli Dividend & Income Trust (GDV), managed by legendary value investor Mario Gabelli.

Mastercard is one of Gabelli’s largest holdings. But we income investors would prefer GDV because it boasts a healthy dividend right around 6.4%, paid monthly, more than 9 times what Mastercard pays (and this is low in CEF-land; other funds, like the next one we’ll talk about, pay nearly double that).

And as I write this, thanks to the conservative folks who buy CEFs, we have a rare opportunity to buy Mario’s portfolio for just 89 cents on the dollar.

Yup, GDV trades at an 11% discount to its net asset value, or NAV. It’s a way to boost MA’s payout and snag a discount, too.

Where does this discount come from?

CEFs are like their mutual fund cousins, with one exception: they have fixed pools of shares, so they can (and do) trade higher and lower than their NAVs, or “fair” values (the value of their holdings minus any debt).

As contrarians, we can step in when they are temporarily out of favor, like after a pullback, when liquidity is low, and buy them at generous discounts.

GDV holds more blue-chip dividend payers alongside MA, such as American Express (AXP), Microsoft (MSFT) and JPMorgan Chase & Co. (JPM). And with GDV, we have an opportunity to purchase them at an 11% discount.

These high-quality stocks wouldn’t normally qualify for our “retire on $500K” portfolio because everyone in the world knows they are strong long-term investments.

Even though these companies are constantly raising their dividends, constant demand for their shares keeps their prices high (and current yields low). So they never meet our current-yield requirement.

GDV does. The fund pays a monthly dividend that adds up to a nice 6.4% annual yield.

Let me give you one more idea (and this is where that much larger payout comes in): the Eaton Vance Tax-Managed Global Diversified Equity (EXG) is another CEF with a similar blue-chip dividend portfolio.

But EXG generates even more income than GDV by selling covered calls on the shares it owns.

More cash flow means a bigger dividend — and EXG pays an already terrific 8.2%!

So we buy and hold EXG and GDV forever, merrily collecting their monthly dividends along the way, right?

Not quite.

In bull markets, these funds are great. But in bear markets, they’ll chew you up.

Step 5: Protect That Principal!

Back when the Fed was printing money like crazy, my CIR readers will fondly recall that we held GDV and EXG together, collecting monthly dividends plus price gains that added up to 43% total returns over 15 months.

Then, when the Fed started hiking rates in early 2022, we sold, just before both funds plunged, a situation that would have slashed our gain from 43% to a mere 13%.

We Sold EXG and GDV Just Before They Plunged

For whatever reason, “market timing” is a taboo phrase among long-term investors. That’s a shame because it’s quite important.

We saw a similar setup with Williams Companies (WMB), which we bought way back in September 2020, when the world was shut down and not long after oil prices went negative.

At the time, the stock yielded a rich 7.7%.

Fast-forward to October 2024, and the strengthening US economy had boosted oil and natural gas demand. Oil, for its part, had recovered to around $75 a barrel.

Those gains helped send WMB’s shares higher, and its dividend yield down to 4.2%.

That was our cue, so we sold WMB and took a 172% total return off the table, with 118% in price gains and the rest in reinvested payouts:

Our Formula For 172% Returns

As these examples show, by aligning our dividends with the market backdrop, we can safely grow our principal and protect those gains, too.

Step 6: Start Here to Retire on $500K

So if the “tried and true” money advice — like the 60/40 portfolio and the 4% rule — has been properly exposed as broken…

Where do we go from here?

Well, imagine your portfolio in just a few days or weeks from now spinning off 8%, 9% and even double-digit dividends all the way up to 16.2%, with the reliability of a Swiss watch… with many of my recommendations paying every single month no less!

No more worrying how much is coming in next month.

No more worrying about the Fed’s next move. Or the next inflation or jobs report. Or overseas conflicts sending oil prices soaring — and stock markets tumbling.

No more worrying about outliving your nest egg.

Let me tell you more about my solution — what I call the “No Withdrawal Portfolio.”

Better yet, I want to give you the names of my favorite stocks and funds to buy right now…

Yields Up to 16.2%, With Upside

To make it easy to transition into this new way of investing… where you are buying “bird in the hand” cash flows… instead of stocks that you just hope will go up… I’ve prepared two in-depth guides that hone in on the strategies I mentioned above…

Special Report #1:

Monthly Dividend Superstars: Yields Up to 16.2%, With Double-Digit Upside

This is where you’ll find the bargains that investors are leaving on the table in their misplaced fear of the Fed, interest rates, policy shifts out of DC or other headline-driven concerns.

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on my three favorite CEFs:

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on my three favorite CEFs:

- A well-hedged 16.2% payer in one of the most in-demand sectors right now,

- The brainchild of one of the top fund managers on the planet, throwing off an amazing 12% yield,

- And a 9.1%-yielding healthcare fund quietly positioned to profit as AI slashes drug development timelines in half—trading at a 9.5% discount to its true value.

Special Report #2:

The Perfect Income Portfolio

In this guide, you’ll get all the details of what I call the “Perfect Income Portfolio.”

Step-by-step, I’ll show you exactly how to set up your portfolio for maximum income without taking on additional unnecessary risk.

And, if you follow the simple steps laid out, I’m confident you’ll be able to enjoy an income stream that far exceeds what most folks who buy the typical S&P 500 stock earn.

This report includes investments that have passed my strict due-diligence process—including one of the best ways I’ve ever seen to invest in utilities (which I’ve picked for strong gains as interest rates move lower).

This fund pays a rich 7.2% today, holds some of the strongest electrical utilities in the country and trades at a bargain valuation (even though most investors don’t realize it). Its bargain status won’t last as rates inevitably tilt lower, pulling more investors toward its healthy payout!

I’ll walk you through each recommendation, giving you a clear, concise and easy-to-understand breakdown of exactly why I see these as “perfect” income plays.

How to Get Both Reports Absolutely Free

To access both reports, Monthly Dividend Superstars and The Perfect Income Portfolio, at no cost whatsoever, I simply ask that you take a risk-free trial of my research service, Contrarian Income Report.

I created Contrarian Income Report to help investors uncover overlooked and underappreciated income plays before Wall Street and the mainstream herd bid them up.

People often ask me, “I get the income part, but where does ‘contrarian’ fit in?”

My answer is simple: You’ll never beat the market by following the herd.

If you buy the same investments as everyone else, you’re going to have the same results as other people — which are always mediocre. This is why my advisory is defiantly contrarian.

It all boils down to one simple principle: If you want to make money, really big money, do what nobody else is doing.

Contrarian investing is probably the simplest, sanest, most powerful and reliable money-making technique ever devised to buy low and sell high. It works in any market, from stocks and bonds to gold and real estate — because human nature is the same everywhere.

You don’t need special training. All you need is an independent mind, a bit of patience and an ounce of courage.

If you want to buy low and sell high, you must force yourself to buy when everybody, including yourself, is feeling discouraged — when the news is bad. That’s likely to be the bottom. And you should sell when everybody is excited and the news is good, because that’s likely to be the top.

Right now, we’re holding a diverse collection of these high-yielding stocks and funds, and you’ll get instant access to each one the moment your no-risk trial starts.

And every new investment you get in Contrarian Income Report comes with a simple goal: it will pay a reliable 5% dividend — or better.

In fact, some holdings in our portfolio go way further than that, delivering 12%+ income right now.

So just by “swapping out” your anemic blue chips for these cash cows, you could double, triple — or even quadruple — your income. And you could do it TODAY!

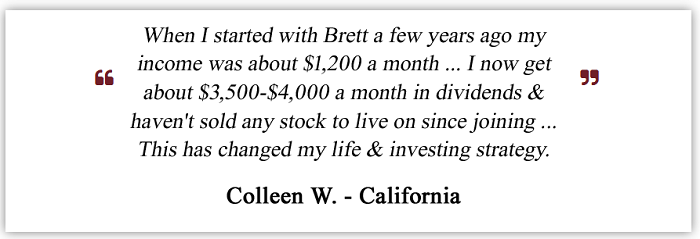

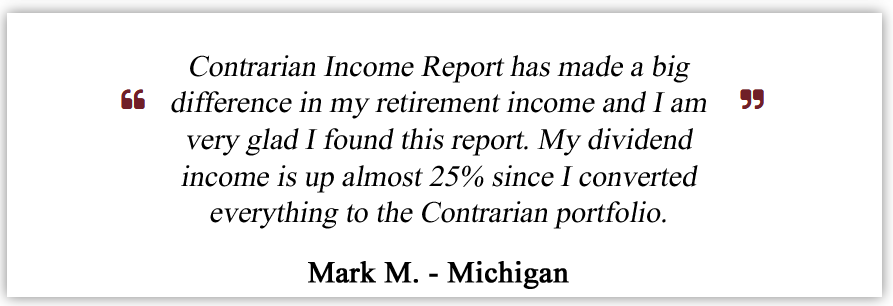

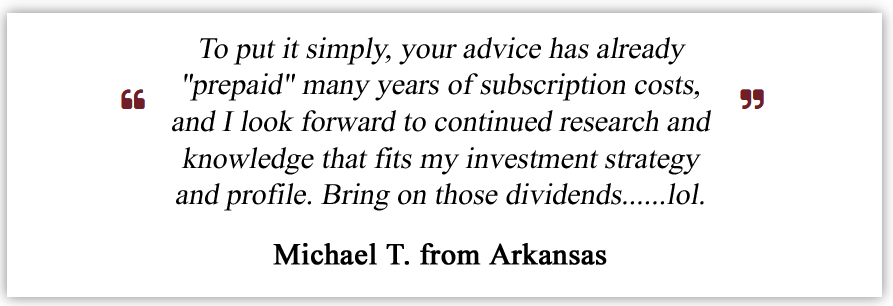

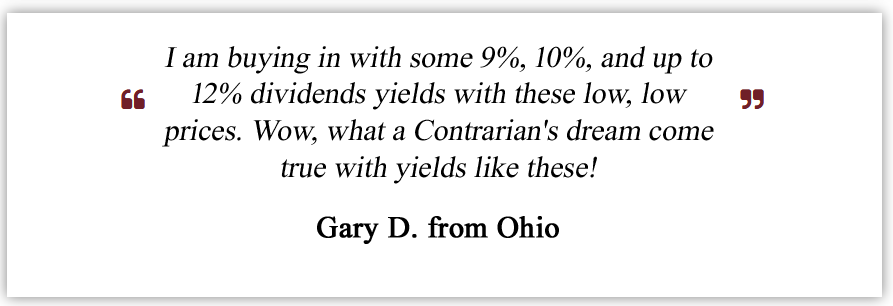

That sort of money can upgrade your lifestyle in a hurry. Take it from my subscribers:

Of course, not everyone follows my recommendations at the exact same time or in the same way. Each member’s personal financial situation is different, so your experience may also be different… but I’m thrilled to say we’ve received dozens more anecdotes similar to these.

Now let’s talk about what you can expect with Contrarian Income Report.

Safe Yields Are Only the Beginning

In addition to my favorite monthly dividends up to 16.2% and my “Perfect Income Portfolio,” your risk-free trial look at Contrarian Income Report includes a whole lot more …

- Full portfolio access. You’ll have immediate access to every pick I make, including my exact buy and sell recommendations and “buy-under” prices.

- New income investing ideas and analysis of major market events delivered straight to your inbox every single week.

- Flash Alerts, with breaking news on our portfolio stocks. I’ll have an eye on all of them 24/7.

- Monthly research bulletins — On the first Friday of each month, you’ll receive my latest research, including new portfolio additions, updates on existing positions and an overview of trends and events that may affect our holdings.

- Members-only website — You’ll get access to a password-protected website where you can access all of our resources: current and past issues, the No Withdrawal portfolio, special bonus reports, and the full portfolio. Whenever you want to check on our recommendations, everything is there for you, day or night.

- Private Webcasts — Several times each year, you can join me for a live, members-only webcast. We’ll run through what’s going on with our holdings and I’ll personally answer your questions.

- VIP Customer Service — If you ever have questions about your subscription, you can email our team anytime, or call our New York office during regular business hours and receive a prompt reply.

- Contrarian Buy Indicator No. 1: My favorite way to “time” a stock buy to cash in on short sellers’ greed.

- Contrarian Buy Indicator No. 2: How to catch a big windfall by following the analysts — just not in the way most people think.

- Contrarian Buy Indicator #3: A classic contrarian signal that tells you when a beaten-down stock is about to rebound.

- Report #1: Monthly Dividend Superstars: Yields Up to 16.2%, With Double-Digit Upside

- Report #2: The Perfect Income Portfolio

- Report #3: The Dirty Dozen: 12 Dividend Stocks to Sell Now

- Report #4: Second-Level Investing: Your Guide to the Contrarian Money Machine

- All past issues and reports

- 12 monthly research bulletins

- Weekly market overviews

- Flash alerts

- Members-only webcasts

- A 24/7 members-only website with first-rate service

- Monthly Dividend Superstars: Yields Up to 16.2%, With Double-Digit Upside

- The Perfect Income Portfolio

- The Dirty Dozen: 12 Dividend Stocks to Sell Now

- Second-Level Investing: Your Guide to the Contrarian Money Machine

- Plus a full-year membership to Contrarian Income Report

Now, the regular member price to join Contrarian Income Report is $99 per year.

That’s a modest sum considering everything that’s included. Heck, the reports you’ll get are worth more than that. They could sell for $99 each, for a total of $198. But today they are all coming to you at no charge.

Imagine 8%, 10%, even 12%+ dividends rolling in from these picks, and then watching them appreciate as mainstream investors realize what they’ve been missing and pile in.

But I want you to see firsthand exactly how profitable this service can be. And I don’t want the subscription fee to get in the way.

So I’ve arranged for new investors to receive an introductory discount of 60% off the regular price and to try out Contrarian Income Report for just $39. (Note: this offer is valid for new subscribers only.)

And to start you off with everything you need to hit the ground running, I’m going to include two more bonus reports…

Extra Bonus #1:

The Dirty Dozen: 12 Dividend Stocks to Sell Now ($99 Value)

As much as I love a fat payout, I never let myself forget that an extraordinary yield can be a warning sign of a stock in trouble.

A high yield that was too good to be true is easy to spot in hindsight. But when a cut, and the resulting share price plunge, are unfolding, most “yield junkies” are intoxicated and just can’t let go … and ride the stock to the bottom.

I’m afraid we’re in for just that scenario with the 12 popular income stocks in this report.

I’m afraid we’re in for just that scenario with the 12 popular income stocks in this report.

Like the landlord that rents the vast majority of its properties to the federal government. Normally, that would make it a safe option, but not with the massive deficit Uncle Sam is running.

Or the high-yield ETF that pays a ridiculous 60%! But it’s returned a mere 10.6% since it was launched a little over two years ago, even with dividends included. That’s a travesty when you consider that the S&P 500 has soared nearly 5X that. And even that meager gain only sets up these buyers for steeper losses when the payout inevitably gets slashed.

Another “dividend disaster” is a popular toy maker yielding 3.3%. Too bad it’s stuck in the world of “physical” games and toys, as most kids now get their fix online.

If you hold any of these stocks, I urge you to dump them immediately.

Next, you’ll get your very own copy of my personal playbook…

Extra Bonus #2:

Second-Level Investing: Your Guide to the Contrarian Money Machine ($99 Value)

While many investing gurus tout the virtues of contrary thinking, they rarely tell you how they go about finding cheap and out-of-favor stocks.

So that’s exactly what you’ll get with this step-by-step contrarian guide. It’s the guts of the system I use to pick stocks in Contrarian Income Report.

Now, there’s just one more thing I’d like to include …

Our Ironclad 100% Money-Back Guarantee

There’s no question that my system works. Sure, investing in the stock market comes with some inherent risk and not all of my recommendations will be winners.

But my long track record of uncovering safe, steady dividends with the potential for serious capital gains (through some of the most vicious market reversals in history) speaks for itself.

The only question is whether this sort of investing is right for you.

Well you can find out without risking a cent … because I’m also going to give you 60 days to try Contrarian Income Report absolutely risk-free.

Here’s how it works …

Start your membership today. Download your special reports, read the current issue and start tracking a few portfolio picks that catch your interest.

Then sit back and enjoy the next couple of issues of Contrarian Income Report, check out my weekly column and all of the other member benefits.

If, after two months, the advice hasn’t more than covered your cost, or if it’s just not right for you, simply let me know and I’ll issue a full refund.

That’s 100% of your money back, no questions asked.

Plus, you’re welcome to keep everything I’ve sent you as a thank you for trying it out.

Here’s a breakdown of everything you get when you join Contrarian Income Report today:

PLUS…

To sum it up, you get a 60% membership discount, four essential investment reports, new issues every month, weekly email updates, flash alerts, live webcasts and more.

All with a 100% money-back guarantee.

Simply click the button below to claim everything right now:

4 Special Reports, a Full Year of My Premium Newsletter, and a Bunch of Other Perks and Benefits for Just $39

One last time, add it all up and you get:

That’s a total value of $495 for just $39 – a 92% total discount!

And I’m confident you find it’s more than worth it.

And remember, you are fully covered by my 60-day money-back guarantee!

You have nothing to lose…

Well, except missing out on dozens of under-the-radar income ideas that could get your retirement back on track – or even ahead of schedule.

All you have to do is click the button below to get started now:

NOW Is the Time to Be an Income Contrarian and Start Your “No Withdrawal” Portfolio…

As I’ve shown you…

The tried and true methods — like the 4% Rule — are broken.

But you don’t need to settle for outdated ideas any longer.

By following my simple system, you can live off dividends alone, without ever having to draw down your principal to cover expenses.

The best way to retire on dividends in this market is to dive into the overlooked, underappreciated income plays you won’t hear about in the mainstream press.

We’re talking stocks and funds that yield 8%, 9%, even 10%+!

I think it’s an easy decision to make…

Especially since I’m offering to send you reports that will give you the exact steps to take to jumpstart your portfolio…

Plus additional recommendations for the next 12 full months…

And all the follow-ups you’ll need to stay ahead of this ever-changing landscape in the markets…

With absolutely zero risk to you!

All you have to do is click the button below:

Don’t struggle to get by on 2% and 3% yielders, crossing your fingers that self-serving politicians, overseas wars or an unexpected bounce in inflation don’t trigger another market crash.

In other words, don’t just hope that stocks will rebound and things will work out. It’s up to you to protect yourself. No one else will do it for you.

Join me and my Contrarian Income Report readers and set yourself up with our secure “No Withdrawal” portfolio… with current dividend yields of 9%+ and upside potential on top of that.

Yours in profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

P.S. These contrarian plays have been known to rally once the herd catches on to what they’ve been missing. I encourage you to act now so that you can get into our newest recommendation while the price is still low and the yield is high.

© BNK Invest, Inc. – All Rights Reserved – Legal Information