Introducing…

The Secure 7%

“No Withdrawal”

Retirement Portfolio

Now you can retire on dividend income alone –

without ever touching your capital…

Dear Reader,

First the bad news: If you are relying on rising stock prices to get you through retirement, you are asking for trouble.

“Buy and hope” is never a good idea, but when stocks are tumbling, as they have in the past year, it could prove to be absolutely devastating.

Stocks are down double digits from the start of 2022, and this time, we can’t expect the Fed to come riding to the market’s rescue.

That’s because the so-called “Fed put,” or the tendency of the central bank to backtrack on policy tightening when the market falls a certain amount, is dead!

With 7% inflation, Fed Chair Jay Powell can’t afford to let up on the gas when it comes to rate hikes.

We’ve never seen anything like this before. And unless something changes fast (the war in Ukraine or central bank policy being good examples), millions of Americans could see their retirement accounts permanently dented.

So… if there was ever a time to step off the stock market roller coaster… and lock in a reliable income stream from dependable dividend payers, it’s now.

But living off dividends has its own challenges. Yields are still in the tank, despite the recent stock-market declines.

The S&P 500 pays 1.7%. On a million-dollar portfolio, that’s a lousy $17,000 per year. Pathetic.

The good news is that I can show you how to get a 300%+ raise and pocket a 7% yield instead. That’s $70,000 in passive income on a million bucks, or $35,000 annually on $500K.

But first let’s debunk the logical – but wrong – assumption that most dividend investors make.

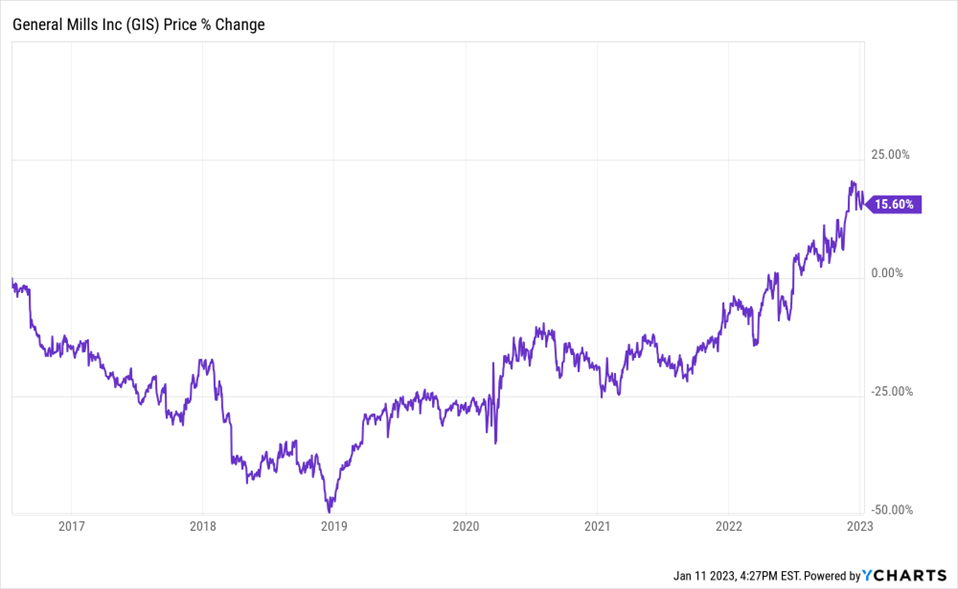

They look at a “consumer staple” like General Mills (GIS), see it paying a “generous” 3%, and think it’s a good buy. But anyone who bought this “safe” stock at its peak in 2016 has had to stomach a 50% price drop, and it’s still up just 15.6% in more than 6 years!

Problem is, these investors are looking at the wrong chart.

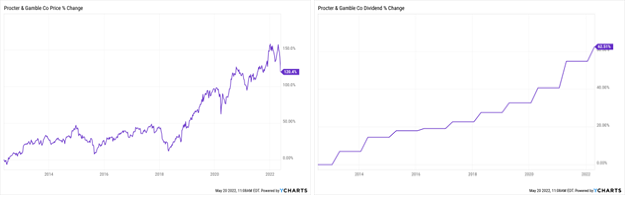

Check out these two charts. Which would you rather rely on?

The chart on the right, of course. It has increased steadily for the past 10 years. It shows the dividends paid by Procter & Gamble (PG). Its jittery companion on the left is PG’s stock price over the same period.

If you’re like most investors, you’re probably looking at the chart on the left. Which means you’re exposing yourself to short-term price risk to collect a 2.4% dividend.

There are two issues with this approach. First, you’re putting your retirement portfolio—and your entire standard of living—smack dab in the path of a stock-market crash (which will take down PG, too).

This brings me to the second – and much bigger – problem: You’re risking WAY too much for a lousy 2.4%!

Even if you buy $1 million worth of PG, you’re only collecting $24,000 a year. That’s about the same as your neighborhood Starbucks barista makes!

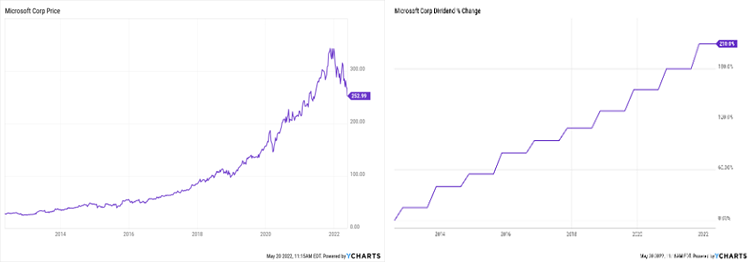

Now how about these two charts?

The chart on the left is the stock price of Microsoft (MSFT) over the past decade. Anyone who bought and held did fine – and also enjoyed the steady dividend growth on the right. In fact, they’re now pocketing a 10% yield on their initial investment – nice.

But what if you didn’t buy Microsoft a decade ago? Where do you put your “new money” to work for income? After all, MSFT only yields 1% today, and the shares are at risk of further declines as Fed rate hikes squeeze tech firms’ profits.

Even the “Dividend Aristocrats”

Can’t Do the Job

When it comes to dividend investing, many “first-level” investors head straight to the list of Dividend Aristocrats—the S&P 500 companies that have hiked their payouts for 25 years or more.

That kind of dividend growth is impressive. But here’s the problem: a company doesn’t need a high yield to join this club.

The S&P 500 Dividend Aristocrats ETF (NOBL), which holds all 68 Aristocrats, yields just 1.9%!

So a million bucks in NOBL will only give you a $19,000 yearly income stream.

To make ends meet, you’ll be forced to sell some of your shares for expenses. Speaking of which …

Most financial advisors pitch a “4% withdrawal rate”. These guys (who have not successfully retired yet themselves, by the way) say that you should supplement your dividend income by withdrawing 4% or so of your capital a year. Looks good on paper, but in reality they are hiding some disastrous market math …

In fact, the 4% rule’s creator, William Bengen, recently admitted that he’s not financially comfortable in retirement …

The 4% Withdrawal Plan Is

Reverse Dollar Cost Averaging (Not Good!)

Here’s the fatal flaw with the 4% withdrawal strategy. Every few years, you’re faced with a chart like this, and you have to sell a stock when it’s dipping:

Instead of selling high, you’re selling low!

This is exactly the wrong time to sell. Remember the benefits of dollar cost averaging that built your retirement portfolio by giving you more shares when prices dipped? This is the same phenomenon, but in reverse!

With a 4% withdrawal portfolio, where you routinely withdraw a fixed amount of money from your assets you siphon off more shares when prices are low and fewer when prices are high. It’s a recipe for running out of money.

What you should be doing – especially with the stock market having gone through a severe correction in 2022 – is transitioning your portfolio away from the casino of stock prices into the steady staircase of dividends.

Basically, it’s time for a paradigm shift.

Instead of investing in the stock market, you need to be investing in the dividend market.

When you shop for dividends, you lock in rising cash flows that you can spend forever.

Look, it’s not your fault that the Fed crushed savers by lowering interest rates to near zero and keeping them there for way too long, stoking inflation in the process.

But in this “new normal,” Wall Street’s “magic 4% rule” – the fantasy that you can draw down 4% of your portfolio every year after you retire – is asking for trouble.

The better way? Create a portfolio that actually generates meaningful income. Ditch the aristocrats that pay you like you’re making lattes for a living, and secure yourself a 3-4X pay raise while still keeping your capital intact.

Allow me to introduce you to…

The 8% “No Withdrawal”

Retirement Portfolio

The solution is a No Withdrawal portfolio that relies entirely on dividend income and leaves your principal 100% intact. Of course, the trick is finding yields high enough to make that work.

You have to go off the beaten path here. Because the only time you’ll find blue chips yielding good money is after they’ve crashed.

You could look at alternative retirement products, such as annuities, where you swap your capital for an income stream. But in most cases you are giving up your principal while being charged outrageous fees. These vehicles usually don’t account for cost of living increases. Plus you’re trading in your legacy – and your grandchildren’s inheritance.

However there are three other vehicles available today that pay reliable yields of 6%, 8%, 10% and even higher.

They have market caps between $1 billion and $3 billion. So they’re plenty liquid enough for you and me, but not for the massive institutions that hold two-thirds of all shares in public stocks. Combined they make up only a fraction of the stock market’s total capitalization – so they don’t get much coverage from the financial media, either.

And that makes these ignored corners of the markets ideal hunting grounds to bag secure yields with stable prices and even 7% to 15% upside in many cases.

Plus, you won’t have to tap your initial capital or “draw down” any of your priceless principal.

I’ll even give you the stock names and ticker symbols to buy to make this happen. But first, a bit about myself.

My name is Brett Owens. I first started trading stocks in college, between classes at Cornell.

My name is Brett Owens. I first started trading stocks in college, between classes at Cornell.

I graduated cum laude with an Industrial Engineering degree — which is actually pretty popular with Wall Street recruiters.

But I couldn’t stand the thought of grinding it out in a cubicle for 80 hours a week. So I moved to San Francisco and got into the tech scene. A buddy and I started up two software companies that serve more than 26,000 business users.

The result was a nice chunk of change coming in … and I had to decide what to do with my money.

I had seen plenty of young “techies” come into sudden cash and burn through their windfall in a year, ending up right back where they started.

That was NOT going to be me. I already had dreams of living off my wealth one day, decades before I retired.

I got plenty of cold calls from brokers wanting to “help” me. But I knew that nobody would care as much about my money as me. So I went out on my own and invested my startup profits in dividend-paying stocks.

I’ve been hunting down safe, stable and generous yields ever since, growing my wealth with vehicles paying me 6%, 7%, even 8%+ dividends.

In recent years, I started writing about the methods I use to generate these high levels of income.

Today I serve as chief investment strategist for Contrarian Income Report — a publication that uncovers secure, high-yielding investments for thousands of investors. Since inception, my subscribers have enjoyed dividends 4 times the S&P 500 average, plus big annualized gains!

And that brings me to a crucial piece of advice…

If I could leave you with just one nugget of investing wisdom today, it would be to NEVER overlook the incredible wealth-building power of dividends.

Few investors realize how important these unglamorous workhorses actually are. Here’s a perfect example…

If you put $1,000 in the dividend-paying stocks of the S&P 500 back in 1973, you would have had $89,420 by the end of 2021, or almost 90x your money. But the same $1,000 in the non-dividend payers would have grown to just $9,890 — 89% less.

That’s why I’m a dividend fan. The stock market is a fantastic wealth-building machine, but it doesn’t always go straight up! There have been plenty of 10-year periods where the only money investors made was in dividends.

And that’s what gives Contrarian Income Report readers such an edge. When you lock in an 8% yield, you’re booking an income stream that’s bigger than the stock market’s long-term average return right off the bat.

Of course you can’t just buy every ticker symbol out there with a flashy yield, or you’ll get burned pretty fast.

But I’ve discovered that if you stick to three overlooked corners of the market, you could collect big dividends with much less need to tap into your savings to pay your bills. Isn’t that what we all want?

Now let’s look at the first way to secure those big payouts…

“No Withdrawal” Stealth Play #1:

Closed-End Funds

If you feel trapped “grinding out” dividend income with traditional 2% or 3% payers, you could double your payouts by moving to closed-end funds (CEFs). In fact, you can often make the switch without actually switching investments.

For example, JPMorgan Chase (JPM) investors can trade in their 2.9% yield for the Gabelli Dividend & Income Trust Fund’s (GDV) 6.2% payout. And guess what? One of GDV’s largest holdings is JPM!

GDV is run by superstar money manager Mario Gabelli. He uses a modest amount of leverage to create his outsized yield — which he delivers every month (unlike most funds, which only pay quarterly). It’s a sweet deal.

Retail investors have been running away from closed-end funds like this one for the past few years. A lot of these funds borrow money to jack up their yields… and investors were afraid that Fed rate hikes would end this “free lunch,” hurting CEFs.

But that’s just not true.

The last time the Fed rates surged, CEFs ended up doing just fine. In June 2004, Fed chair Alan Greenspan began boosting rates from then-historic lows. Over a two-year period, he increased the federal funds rate from 1% to 5.25%. An earthquake.

How did CEFs perform? Three prominent funds — Gabelli’s, along with the Calamos Strategic Total Return (CSQ) and the Eaton Vance Limited Duration Income Fund (EVV), were around back then — and all outperformed the market during this two-year span.

What’s more, when the Fed inevitably starts cutting rates again, CEFs will get an extra upside boost as their borrowing costs and the yields on so-called “safe” investments like Treasuries (which are competitors to CEFs) fall.

And wait ’til you see the three closed-end picks I have for you. They are yielding up to an incredible 11%.

Plus they trade at attractive valuations, which suggests further upside from here.

These discounts could add to these funds’ appeal (and help reduce their downside) in a pullback, too, as they get even cheaper (and more appealing to income-seekers, who’d be tempted to pile in).

Either way, we’ll still collect those fat dividends!

I’ll share the details on my three favorite CEFs in a minute — but first, let’s get to our next strategy.

“No Withdrawal” Stealth Play #2:

Collecting Rising Rents

It’s not the flashiest way to grow your wealth, but more Americans have become wealthy thanks to real estate than any other investment. In fact, seven out of every 10 American millionaires owe their wealth to the steady appreciation of property values.

Unfortunately, most investors never venture beyond owning their own home. It takes a good chunk of change to get started in real estate… and being a landlord can be a real headache.

But in the past few decades, a Wall Street invention called the real estate investment trust (REIT) has radically changed the work/profit equation. By pooling a group of income-producing properties and selling shares of the pie to small investors, it has opened the high-stakes world of commercial real estate to everyone.

There’s no easier way to be a landlord than buying into one of these REITs. You can instantly own shopping centers, office towers and apartment buildings… and pocket the cash these tenants are paying.

It’s the fun part of being a landlord, without the hassles or headaches.

What I love about REITs is that the IRS lets them pay ZERO income taxes as long as they pass on the bulk of their earnings to shareholders. So they collect the rent, pay their bills and send what’s left to you as a dividend. As a nice bonus, your REIT income is taxed at a lower rate than regular rental income.

What’s more, because REITs tend to “zig” when other investments “zag,” they are a great way to diversify your assets, reduce your volatility and improve your overall returns. Meanwhile, you’ll be getting more than twice the payout of the broader stock market.

All of which means… if you don’t have a burning desire to change light bulbs and play landlord yourself, it’s smarter to simply sit back, make a few clicks and buy real estate stocks instead of physical properties.

But it pays to be choosy here. There are more than 200 REITs trading on US exchanges. Some have bloated expenses, and a few have dangerous levels of debt.

We’ve boiled the universe down to our favorite REIT: a rock-solid, well-priced, proven performer paying north of 5% and with plenty of upside as demand for industrial space surges. More details on them in a minute; let’s first talk about our third strategy…

“No Withdrawal” Stealth Play #3:

Hidden Stocks

It’s no secret that investors like to brag.

They like to own the hottest company, the flavor of the month, the stock that’s barreling higher every day, and they love to tell everyone they own it.

But here’s the thing … more often than not, investors are buying these stocks too late. They’re buying into the hype at the exact same time as everyone else. And they usually sell at the worst time.

I don’t like “hot” stocks.

Sure, you might get in on the next Netflix or Apple, but the odds are stacked against you from the get-go. Because the truth is, for every home run there’s another thousand you’ll lose big with.

That’s why I focus on what I call “Hidden Stocks.”

These are the underappreciated, downtrodden stocks that almost nobody knows or cares about…

Hidden Stocks tend to be rock-solid companies with huge cash reserves, the ability to adapt to changes in the economy and long histories of paying ever-increasing dividends…

But because they’re in an underappreciated, overlooked or “boring” market, their share prices are often undervalued.

Which means you can add these Hidden Stocks to your portfolio at low prices and tuck them away — potentially for years — while they continue to pay their dividends.

And I’ve found a near-perfect “Hidden Stock” that I’ll share with you in just a moment.

Now let’s see how you can get hold of my complete No-Withdrawal Portfolio research today, including names, tickers and buy prices.

Up to 11% Yields, With Upside

To make it easy to transition into this new way of investing… where you are buying “bird in the hand” cash flows… instead of stocks that you just hope will go up… I’ve prepared two in-depth guides, that hone in on the strategies I mentioned above…

Special Report #1:

Monthly Dividend Superstars: Yields Up to 11%, With Double-Digit Upside

This is where you’ll find the bargains that investors are leaving on the table in their misplaced fear of the Fed.

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on my three favorite CEFs:

- A well-hedged 11% payer in one of the most in-demand sectors right now,

- The brainchild of one of the top fund managers on the planet throwing off an amazing 10 yield%,

- And a rock-steady 8.8% dividend whose managers have guided it to an astonishing 1,300% total return since inception.

Special Report #2:

The Perfect Income Portfolio

In this guide, you’ll get all the details of what I call the “Perfect Income Portfolio.”

Step-by-step, I’ll show you exactly how to set up your portfolio for maximum income without taking on additional unnecessary risk.

And, if you follow the simple steps laid out, I’m confident you’ll be able to enjoy an income stream that far exceeds what most folks who buy the typical S&P 500 stock earn.

This report includes investments that have passed my strict due-diligence process—including an industrial REIT yielding 5.3% whose properties are in high demand across the US.

The reason? Geopolitical turmoil is prompting more American companies to move their production home, and straight into our pick’s warehouses!

I’ll walk you through each recommendation, giving you a clear, concise and easy-to-understand breakdown of exactly why I see these as “perfect” income plays.

How to Get Both Reports Absolutely Free

To access both reports, Monthly Dividend Superstars and The Perfect Income Portfolio, at no cost whatsoever, I simply ask that you take a risk-free trial of my research service, Contrarian Income Report.

I created Contrarian Income Report to help investors uncover overlooked and underappreciated income plays before Wall Street and the mainstream herd bid them up.

People often ask me, “I get the income part, but where does ‘contrarian’ fit in?”

My answer is simple: You’ll never beat the market by following the herd.

If you buy the same investments as everyone else, you’re going to have the same results as other people — which are always mediocre. This is why my advisory is defiantly contrarian.

It all boils down to one simple principle: If you want to make money, really big money, do what nobody else is doing.

Contrarian investing is probably the simplest, sanest, most powerful and reliable money-making technique ever devised to buy low and sell high. It works in any market, from stocks and bonds to gold and real estate — because human nature is the same everywhere.

You don’t need special training. All you need is an independent mind, a bit of patience and an ounce of courage.

If you want to buy low and sell high, you must force yourself to buy when everybody, including yourself, is feeling discouraged — when the news is bad. That’s likely to be the bottom. And you should sell when everybody is excited and the news is good, because that’s likely to be the top.

Right now, we’re holding a diverse collection of these high-yielding stocks and funds, and you’ll get instant access to each one the moment your no-risk trial starts.

And every new investment you get in Contrarian Income Report comes with a simple goal: it will pay a reliable 5% dividend — or better.

In fact, some holdings in our portfolio go way further than that, delivering 10%+ income right now.

So just by “swapping out” your anemic blue chips for these cash cows, you could double, triple — or even quadruple — your income. And you could do it TODAY!

That sort of money can upgrade your lifestyle in a hurry. Take it from my subscribers:

Now not everyone follows my recommendations at the exact same time or in the same way, and each member’s personal financial situation is different. So your experience may be a little different … but I have dozens more stories just like these.

But that’s not all, because …

Safe Yields Are Only the Beginning

In addition to my favorite monthly dividends up to 11% and my “Perfect Income Portfolio,” your risk-free trial look at Contrarian Income Report includes a whole lot more …

- Full portfolio access. You’ll have immediate access to every pick I make, including my exact buy and sell recommendations and “buy-under” prices.

- New income investing ideas and analysis of major market events delivered straight to your inbox every single week.

- Flash Alerts, with breaking news on our portfolio stocks. I’ll have an eye on all of them 24/7.

- Monthly research bulletins — On the first Friday of each month, you’ll receive my latest research, including new portfolio additions, updates on existing positions and an overview of trends and events that may affect our holdings.

- Members-only website — You’ll get access to a password-protected website where you can access all of our resources: current and past issues, the No Withdrawal portfolio, special bonus reports, and the full portfolio. Whenever you want to check on our recommendations, everything is there for you, day or night.

- Quarterly Webinars — About every three months you can join me for a live, members-only webinar. We’ll run through what’s going on with our holdings and I’ll personally answer your questions.

- VIP Customer Service — If you ever have questions about your subscription, you can email our team anytime, or call our New York office during regular business hours and receive a prompt reply.

- Contrarian Buy Indicator No. 1: My favorite way to “time” a stock buy to cash in on short sellers’ greed.

- Contrarian Buy Indicator No. 2: How to catch a big windfall by following the analysts — just not in the way most people think.

- Contrarian Buy Indicator #3: A classic contrarian signal that tells you when a beaten-down stock is about to rebound.

Now, the regular member price to join Contrarian Income Report is $99 per year.

That’s a modest sum, considering everything that’s included. Heck, the reports you’ll get are worth more than that. They could sell for $99 each, for a total of $198. But today they are all coming to you at no charge.

Imagine 5%, 10%, even 11% dividends rolling in from these picks, and then watching them appreciate as mainstream investors realize what they’ve been missing and pile in.

But I want you to see firsthand exactly how profitable this service can be. And I don’t want the subscription fee to get in the way.

So I’ve arranged for new investors to receive an introductory discount of 60% off the regular price and to try out Contrarian Income Report for just $39. (Note: this offer is valid for new subscribers only.)

And to start you off with everything you need to hit the ground running, I’m going to include two more bonus reports…

Extra Bonus #1:

The Dirty Dozen: 12 Dividend Stocks to Sell Now ($39 Value)

As much as I love a fat payout, I never let myself forget that an extraordinary yield can be a warning sign of a stock in trouble.

A high yield that was too good to be true is easy to spot in hindsight. But when a cut, and the resulting share price plunge, are unfolding, most “yield junkies” are intoxicated and just can’t let go … and ride the stock to the bottom.

I’m afraid we’re in for just that scenario with the 12 popular income stocks in this report.

I’m afraid we’re in for just that scenario with the 12 popular income stocks in this report.

Like a widely-held REIT that has massive exposure to the ongoing retail apocalypse…

Or a popular electronics retailer whose shelves are overstuffed with inventory, just as high inflation and a possible recession are prompting consumers to limit their spending…

I also have several more REITs on my “soon-to-fail” radar…

One cut its dividend three times in 2020 and hasn’t budged on moving it back toward pre-cut levels…

Another is a mall landlord that looked like a big winner from COVID reopenings but is now competing with even more muscular online retailers.

Really, the dangers are spread all over the market right now — from a high-yielding food maker company to a major media conglomerate.

If you hold any of these stocks — and it’s likely that you do — I urge you to dump them immediately.

Next, you’ll get your very own copy of my personal playbook…

Extra Bonus #2:

Second-Level Investing: Your Guide to the Contrarian Money Machine ($39 Value)

While many investing gurus tout the virtues of contrary thinking, they rarely tell you how they go about finding cheap and out-of-favor stocks.

So that’s exactly what you’ll get with this step-by-step contrarian guide. It’s the guts of the system I use to pick stocks in Contrarian Income Report.

Now, there’s just one more thing I’d like to include …

Our Ironclad 100% Money-Back Guarantee

There’s no question that my system works. Sure, investing in the stock market comes with some inherent risk and not all of my recommendations will be winners.

But my long track record of uncovering safe, steady dividends with the potential for serious capital gains (through some of the most vicious market reversals in history) speaks for itself.

The only question is whether this sort of investing is right for you.

Well you can find out without risking a cent … because I’m also going to give you 60 days to try Contrarian Income Report absolutely risk-free.

Here’s how it works …

Start your membership today. Download your special reports, read the current issue and start tracking a few portfolio picks that catch your interest.

Then sit back and enjoy the next couple of issues of Contrarian Income Report, check out my weekly column and all of the other member benefits.

If, after two months, the advice hasn’t more than covered your cost, or if it’s just not right for you, simply let me know and I’ll issue a full refund.

That’s 100% of your money back, no questions asked.

Plus you’re welcome to keep all four special reports with my thanks for trying it out.

To sum up, you get a 60% membership discount, my two latest investment reports, two more bonus reports, weekly email updates and alerts, and a 100% money back guarantee.

I don’t see how you can lose here. Click this button and get started right now.

Don’t struggle to get by on 2% and 3% yielders, crossing your fingers that self-serving politicians, geopolitical disasters or overzealous interest rate hikes don’t trigger another market crash.

In other words, don’t just hope that stocks will rebound and things will work out. It’s up to you to protect yourself. No one else will do it for you.

Join me and my Contrarian Income Report readers and set yourself up with our secure “No Withdrawal” portfolio… with current dividend yields of 7% and upside potential on top of that.

Yours in profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

P.S. These contrarian plays have been known to rally once the herd catches on to what they’ve been missing. I encourage you to act now so that you can get into our newest recommendation while the price is still low and the yield is high.

© BNK Invest, Inc. – All Rights Reserved – Legal Information