How To Live off

$500,000 Forever

In this income investing report, you’ll learn…

- Bank $40,000 annually for every $500,000 you invest,

- The 3 safest closed-end funds that pay up to 9%,

- The best way to buy “preferred” stocks for 8.4% dividends, and

- What 2 recession-proof REITs offer 7.6% average payouts.

Fellow Income Investor,

A half-million dollars is a lot of money. Unfortunately, it won’t generate much income today if you limit yourself to popular investments.

The 10-year Treasury has “rallied” to barely 2.5%. Put your $500K in them and you’re well below the single-person poverty level at $10,000 annually. Yikes.

Dividend paying stocks are masquerading around as bond proxies for this reason. But they still don’t yield enough. Vanguard’s popular Dividend Appreciation ETF (VIG) pays 2%. The iShares Select Dividend ETF (DVY) pays 3% – better, but that’s still just under the poverty level for two people at $15,000 per year.

When investment income falls short, retirees sell their investments to supplement the income. Of course the problem here is that when capital is sold, the payout stream takes an immediate hit – so that more capital must be sold next time, and so on.

Avoid the Share Selling “Death Spiral”

Some financial advisors (who are not retired themselves, by the way) say that you can safely withdraw and spend, say, 4% of your retirement portfolio every year. Or whatever percentage they manipulate their spreadsheet to say.

Problem is, in reality, every few years you’re faced with a chart that looks like this. Your dividends are fine, but your stock price tanks big!

Chevron’s Dividend Was Fine – Its Stock Wasn’t

When dividends aren’t enough, you need to sell shares for money to live on. Not good – it means you sell more shares of stock when prices are low, and less when prices are high.

Remember the benefits of dollar cost averaging that built your portfolio? You bought regularly, and bought even more when prices were low? In this case, you’re forced to sell low.

The Reliable Retirement Solution:

Dividends Only

Instead of ever selling your stocks, you should instead make sure you live on dividends alone so that you never have to touch your capital.

This is easier said than done, and obviously the more money you have the better off you are. But with rates and yields so low, even rich guys have a tough time living off of interest today.

You can actually live better than they can off of a (much) more modest nest egg if you know where to look for lesser-known, meaningful and secure yield. I’m talking about annual income of 6%, 7% or even 8% – so that you’re banking up to $40,000 each year for every $500,000 you invest.

And you’ll never have to touch your nest egg capital – which means you’ll never have to worry about stock prices.

The only thing you need to concern yourself with is the security of your dividends. As long as your payouts are safe, who cares if your stock prices swing up or down on a given day?

Most investors know this is the right approach to retirement. Problem is, they don’t know how to find 7% and 8% yields to fund their lives.

And when they do find high yields, they’re not sure if these payouts are safe. Will the company or fund have enough cashflow to pay the dividends into the future? And how sensitive are these payouts to interest rate increases?

Let’s walk through my three favorite vehicles in the investment universe for income today. Regular stocks won’t let you live on dividends alone – but these secure, underappreciated payout strategies will.

And we’ll put a special focus on the interest rate question, which is mistakenly believed to be a threat by headline-focused investors.

“Dividends Only” Vehicle #1:

Closed-End Funds

Some closed-end funds (CEFs) paying up 7%, 8% or even 9% can be good income candidates – if you choose wisely.

You’re probably familiar with their mutual “cousins”. Closed-ends are a bit different. While mutual funds tend to buy individual stocks and mirror the market, CEF managers tend to have wider mandates and longer leashes. A top CEF manager takes advantage of this flexibility to generate alpha.

He might buy safe sovereign debt in Australia when investors are scared of Asia altogether, and lock in secure 6% yields. Or he might buy preferred shares issued by JPMorgan paying 6.1% annually – a deal not available to an individual investor like you or me (more on this in a minute).

A savvy closed-end manager can even borrow cheaply and juice returns. CEFs borrow at rates tied to Libor (the London interbank offered rate) – good living today with the international benchmark at just 0.86%. The “spread” turns already good yields into great ones.

If you feel trapped “grinding out” dividend income with classic 3% or 4% payers, you can double your payouts (or better) immediately by moving to CEFs. And you can often make the switch without actually switching investments.

For example, American International Group (AIG) investors can potentially trade in their 2% dividend yields for the Gabelli Dividend & Income Trust Fund’s (GDV) 6.8% payout. AIG is GDV’s largest holding amongst a list of blue chip payers plus dividend growers like Wells Fargo (WFC) and Verizon (VZ).

Superstar money manager Mario Gabelli runs his namesake GDV. He combines his yields with growth and leverage to create his outsized yield – which he delivers investors every month, to boot.

Sounds like a sweet deal, right? His investors get the benefit of a legendary money mind along with his access to ideas and cheap money.

And there are funds that deliver even more “alpha” than GDV – which means they pay more, and offer more potential upside. I’ll highlight three of my favorite plays in this space in a moment.

It is bizarre that many first-level investors spent much of 2016 and 2017 running away from closed-end funds, claiming that their “free leverage lunch” is nearing an end with higher rates on the horizon. Plus, they say these funds are going to see more competition from other fixed income assets looking increasingly attractive, making them less so.

The result? Many funds are selling at bargain prices today thanks to the headline worry that higher rates hurt CEFs. But that’s just not true.

Libor – the rate CEFs borrow money at – is tied closely to the Fed funds rate. And the last time the Fed hiked its significantly, CEFs did just fine.

In June 2004, Fed chair Alan Greenspan began boosting rates from then-historic lows. Over a two-year period, he increased the federal funds rate from 1% to 5.25%. An earthquake.

How’d CEFs perform? Three prominent funds – Gabelli’s along with the Calamos Strategic Total Return (CSQ) and the Eaton Vance Limited Duration Income Fund (EVV) – all outperformed the market during this 2-year span!

Higher Rates No Problem for Top Closed-Ends 2004-06

And wait ‘til you see the three closed-end picks I have for you. These “slam dunk” income plays pay 7%, 8% and even 9% dividends.

Plus, thanks to these unfounded interest rate fears, they trade at steep discounts to their net asset value (NAV) today. This means we’re buying their underlying assets for just 85 or 90 cents on the dollar.

Which means these funds are perfect for your retirement portfolio because your downside risk is minimal. Even if the market takes a tumble, these top-notch funds will simply trade flat … and we’ll enjoy those 7% to 9% yields.

Most likely, they’ll jump 10-15% to close the “free money” discount … and we’ll still collect those fat dividends!

I’ll share the details on my three favorite CEFs in a minute – but let’s get into our next strategy.

“Dividends Only” Vehicle #2:

Preferred Shares

You can double your yields, and actually reduce your risk, by trading in your common shares for preferreds. Most investors only consider “common” shares of stock when they look for income. These are the shares in a company you receive when you place an order with your broker.

Problem is, most dividend darlings don’t pay much on their common shares today. You’ll be hard pressed to find a dividend aristocrat with a yield above 3% or a P/E ratio below 20 – evaporating business models or not!

A Bear Market in Common Yields

A company will issue preferred shares to raise capital. In return it will pay regular dividends on these shares – and as their name suggests, preferreds do receive their payouts before common shares. They typically get paid more, and even have a priority claim on the company’s earnings and assets in case something bad happens, like bankruptcy.

So far so good. The tradeoff? Less upside. But in today’s expensive stock market, it may not be a bad trade to make. Here’s an example that would roughly double your current dividends.

Common shares of JPMorgan (JPM) – which I like and own warrants on – pay 2.9%. Not bad, but you could more than double your yield by buying JPM’s “Series Y” preferred stock offering for 6.1% annually.

Series what? That’s a big problem with preferred shares – they are often complicated to purchase without the help of a human broker.

In a minute I’ll show you how to purchase my favorite preferred funds for 7.4% and 8.4% yields in a minute. The best management teams buy mostly floating rate bonds – which will buffer their portfolios as interest rates rise. It’s important to stick with the experts and avoid convenient ETFs, which aren’t “smart” enough to do this.

“Dividends Only” Vehicle #3:

Recession-Proof REITs

Real estate investment trusts, or REITs, can be powerful investment vehicles for safety and high yield. Legally required to return 90% of income to shareholders, these firms find high-quality real estate opportunities while providing investors to opportunity to be a landlord with the liquidity – and convenience – of a stock.

The result is higher payouts than the broader market. The Vanguard REIT Index ETF (VNQ) pays 4.3% today, a little more than double the S&P 500 (which it’s doubled up in its 12 years since inception):

Twice as Good as Stocks

The financial talking heads claim that REIT profits will be crushed as rates rise. It sounds reasonable enough, because these firms do benefit from cheap borrowing. However it’s a lazy explanation, and not actually true for many REITs over any meaningful time period.

Let’s go back to the 2004-06 period in which Greenspan hiked. He boosted the federal funds rate from 1% to 5.25% while the 10-year Treasury glided higher from 4.5% to 5.15%.

Terrible time for REITs, right? Wrong. The Vanguard REIT Index ETF (VNQ) actually returned 48.1% including dividends over this time period, crushing the 14.6% gain by the S&P 500:

REITs Crushed Other Stocks as Rates Rose…

Last year at this time, we were having the same conversation we are right now. REITs were supposedly “done” because the Fed was about to raise rates in December. The hike happened, but REITs still beat the broader stock market over the ensuing 12 months:

REITs Weren’t Exactly “Done”

Some REITs are relatively recession-proof. For example, self-storage REITs like Public Storage (PSA) can actually see an uptick in demand when economic trouble strikes. For example, in 2008 when millions of Americans were losing their homes, demand for self-storage went up as people abandoned their underwater houses and looked for a place to keep their valuable possessions.

As much as I’m intrigued by self-storage, my two favorite hidden gem REITs operate healthcare facilities that are in constant demand – namely skilled nursing facilities and hospitals.

Skilled nursing is a particularly hot area. These homes provide the highest level of care an older adult can receive while still living independently. Residents generally get their own room, their own bed, and a private bathroom. Many folks are able to enjoy their remaining years here in relative comfort.

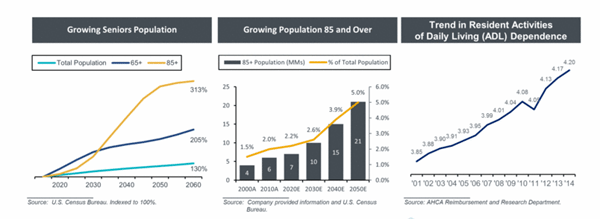

While demand is going to keep climbing thanks to a demographic megatrend (with the 65+ population set to double in the years ahead)…

The Senior Population is Just Beginning to Boom…

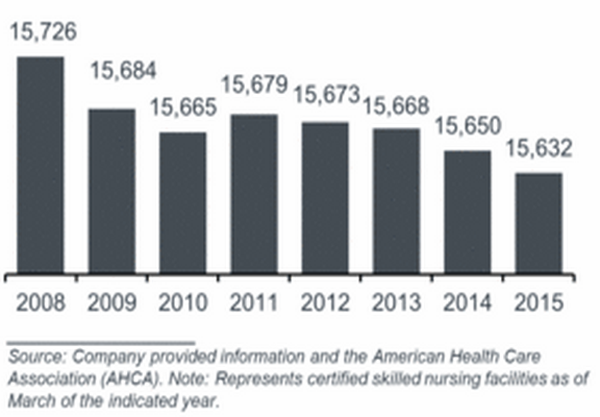

The supply of skilled nursing facilities is actually decreasing. We have less of them today than we did in 2009!

… While Skilled Nursing Supply is Actually Decreasing!

Rising demand and falling supply have these specialty providers well positioned to grow their dividends in the years ahead no matter what happens in the election, economy or stock market.

They are the perfect examples of hidden gems the masses are slowly starting to uncover. But both are still better bargains than the big names held by VNQ. They pay yields between 7.4% and 8% – nearly double the ETF – and one firm is actually increasing its quarterly dividend every single quarter!

An Average 8% Yield, With Upside

It’s only a matter of time before other investors ditch their paltry 3% and 4% payers and find their way over to these “slam dunk” income plays, so the time to buy is now, while they still trade at deep discounts to NAV and FFO.

That’s why I’ve prepared three in-depth guides, outlining each of the strategies I mentioned above…

Special Report #1

The first is called the “Monthly Dividend Superstars: 8% Yields With 7-15% Upside.”

Inside you’ll find the ticker symbol, my buy-up-to price and in-depth backstory on each of my three favorite CEFs, including:

- The global infrastructure play that pays 7% annually and sells at a 7% discount to net asset value (NAV).

- The brainchild of the one of the top fund managers on the planet that pays 8.7%

- And an 8.9% payer with heavy insider buying over the last 12 months.

Special Report #2

The second guide is called Preferred Shares: Looking Past Common Dividends for 8.4%.

Inside you’ll find my favorite fund for investing in preferred shares, along with its management profiles and investing strategies.

The fund pays 8.4% today. High yield is great, but its best quality may be its lack of correlation with the broader stock market. The shares this fund owns are preferred in every sense of the world – meaning it gets paid its fat dividends no matter what the broader market does.

Special Report #3

Finally your third guide, Recession Proof REITs: 2 Plays With 7.6% Yields and 25% Upside, will discuss my two favorite REITs. They include:

- The 7.4% payer that’s delivered an 86% total return in recent years and shows no sign of slowing down.

- The 8% dividend machine that’s raised its dividend the last 19 quarters in a row.

In each report you’ll get the rationale behind where, why and how to profit. In short, everything you need to know about these stocks before you invest a single penny.

How to Get All 3 Reports Absolutely Free

To access all three reports, Monthly Dividend Superstars, Preferred Shares and Recession Proof REITs at no cost whatsoever, I simply ask that you take a risk-free trial of my research service, The Contrarian Income Report.

I created The Contrarian Income Report to help self-directed investors uncover overlooked and under-appreciated income plays before Wall Street and the mainstream herd bid them up.

Every new investment I recommend pays 6% or better, including three funds in our portfolio that each deliver nearly 9% income right now – and they pay out monthly.

As I write this, my five favorite “best buys” are paying between 6% and 9% and our entire portfolio sports an average yield of nearly 8%!

Meanwhile, the S&P 500 pays a meager 1.9% on average, and the 10-year Treasury bond barely 2.3%. Most investors could double – or even triple – their income overnight without taking heart-stopping risks!

But don’t take my word for it. Here’s what some of my subscribers have to say about these recommendations:

Craig R. from Pennsylvania told us:

“Just wanted to write and let you know I’m very pleased with my subscription to your services… Keep up the good work! I sleep better at night not worrying about the daily gyrations of the market. I’m very glad I found your service.”

J.C. in California wrote:

“I love your insights and as a financial advisor the way I invest my clients’ money many of your newsletters provide me with new ideas to explore and work hand in hand with my value approach. You make my job easier and I appreciate that.”

Scott G. from Indiana said:

“We have been extremely pleased with Brett’s Contrarian recommendations and have friends getting ready to join! We are lifers!”

Richard W. from Massachusetts wrote in to say:

“I have subscribed to several of the biggest advisory services (a couple are even ‘lifetime’ subscriptions) but those from Contrarian Outlook are my favorites and the only ones I actually act on these days.”

Tom I. from Florida told us:

“I’m very happy with your service. It solved my retirement income dilemma which is an incredible relief. Thank You!”

But that’s not all, because…

Safe Yields Are Only the Beginning

In addition to my favorite REITs with 7.6% average yields, the closed-end funds paying nearly 9%, and the 8.4% Preferreds, your your risk-free trial includes a whole lot more…

- You’ll have immediate access to all of the picks in the members-only portfolio, including my exact buy & sell recommendations and buy-under prices.

- Get new income investing ideas on stocks I’ve been watching and analysis of major market events delivered straight to your inbox every single week.

- Never worry about missing out on breaking news on our portfolio stocks. I’ll have an eye on all of them 24/7 and will send a flash alert right away if there’s ever any change in our position.

- On the first Friday of each month you’ll receive my monthly research bulletin, including new portfolio additions, updates on existing positions and an overview of trends and events that may affect our holdings.

- Day or night, you can always log into our password protected members-only website to access all of our resources, archives, special reports and the full portfolio.

- If you ever have questions about your subscription, you can email our customer service team anytime, or call our New York office during regular business hours without waiting on hold or navigating those annoying phone menus.

- You won’t need to spend hours in front of a computer screen researching stocks. I’ll take care of all the work and send out new recommendations as they become worthy of your investment dollars, as well as keep you up to date on our existing holdings.

Now, the regular member price to join The Contrarian Income Report is $99 per year.

With everything that’s included I’m sure you’ll agree it’s well worth the cost. Heck, the three reports you’ll get absolutely free are worth three times that much.

And even a small position in any one of the picks mentioned above will easily cover that in just the first few months.

Imagine 7%, 8%, even 9% dividends rolling in from these picks, and then watching them appreciate as mainstream investors realize what they’ve been missing and inevitably pile back in.

But it’s important that I earn your trust and you have the chance to see exactly how profitable this service can be.

So I’ve arranged for a small number of investors to take 60% off the regular price and try out The Contrarian Income Report for just $39.

And to ensure you have no reason not to try this service out, I’m going to include two more bonus reports just for giving it a shot…

Bonus #1: The Dirty Dozen: 12 Dividend Stocks to Sell Now

I come across countless opportunities begging for your investment dollars every single day. Sadly, many of the juiciest dividends are ticking time bombs just waiting to go off.

This report reveals the 12 biggest potential disasters on my watchlist, including some of the most popular names on the street. Can you guess…

… which corporate services giant pays a dividend 3 times greater than earnings with borrowed money?

… the multinational manufacturer paying out nearly 90% of its earnings while EPS has been on a steady 27% decline since 2011?

… the toy company on a 3-year losing streak yet paying over 4.6% while its product line falls further and further out of favor?

Make sure you’re not holding any of these losers when they finally make the decision to cut payouts and share prices plummet!

Next, you’ll get your very own copy of my personal playbook…

Bonus #2: Second-Level Investing: Your Guide to the Contrarian Money Machine

Many super-investors agree that you’ll never beat the market by following the herd. They tout the virtues of contrary thinking, but I’ve yet to hear any one of them specifically outline how they go about finding under-appreciated stocks with low valuations.

And that’s exactly what you’ll get with this step-by-step contrarian guide.

For the past decade I’ve been refining a system that identifies and selects the top contrarian candidates for investment. By following these steps, you’ll be able to find the types of stocks that Warren Buffett, George Soros, Howard Marks and many other greats only wish they could invest in.

Now, there’s just one more thing I’d like to include…

Our Ironclad 100% Money-Back Guarantee

I’m so confident you’ll enjoy (and profit from) this service that I’m going to give you 60 days to try The Contrarian Income Report absolutely risk-free.

Here’s how it works…

Start your membership today. Download your special reports, read the latest issue and start tracking a few winners in the portfolio that catch your interest.

Then, sit back and enjoy the next couple of issues of The Contrarian Income Report, check out my weekly column and all of the other member benefits.

If, after nearly 2 months, you don’t feel the advice has more than covered your cost, or if it’s just not right for you, simply let me know and I’ll issue a full refund.

That’s 100% of your money back, no questions asked.

Plus you’re welcome to keep all five special reports with my thanks for trying it out.

So, you get a 60% membership discount, my three latest investment reports, weekly email updates and alerts, and a 100% money back guarantee.

I don’t see how you can lose here, so click the button below to get started right now.

In the coming months, many investors will struggle to get by on their paltry 2% and 3% payers, holding their breath for the next signal from Washington on the state of the economy, fearful of what might happen in China & Europe.

But my Contrarian Income Report readers and I will rest easy thanks to our super-safe “Dividend Only” portfolio and enjoy 8% dividends with 10-20% gains over 12 months.

Are you going to join us?

Yours in profits,

Brett Owens

Chief Investment Strategist

The Contrarian Income Report

P.S. Since my recommendations are contrary to prevailing popular beliefs, they have a habit of rallying quickly as soon as the mainstream herd catches on to what they’ve been missing. I encourage you to get started right now so that you can get in at a good price!

P.P.S. Remember, your risk-free membership comes with the names and full details on my top 3 closed-end funds paying up to 9%, average dividends of 7.6% from my top REIT plays, and Preferreds that will hand you 8.4%. Even a small position in any one of these picks will easily cover a full year’s membership… most likely before your 60 day trial even ends!