Fellow Investor,

Thank you for requesting your copy of my latest special report, 7 Great Dividend Growth Stocks for a Secure Retirement.

In addition to your free report, I’ve also arranged for you to receive a complimentary subscription to the Contrarian Outlook email newsletter. Inside it, you’ll receive my unique “second-level” analysis on dividend payers and growers so that you can maximize your portfolio’s current yield AND upside, even in this uncertain market. Look for your first issue soon.

In the meantime, enjoy your free special report below.

Yours in payout profits,

Brett Owens

Chief Investment Strategist

The Contrarian Income Report

Today I’m going to take you inside an ignored corner of the market where you can still find cheap stocks throwing off quarterly dividends that grow 10%—and more—year in and year out.

Then we’ll zero in on 7 of these under-the-radar companies, all of which should definitely be on your buy list now. Along the way, we’ll unmask 3 dividend darlings that are actually “yield traps”—their dividend histories make them look tempting … but buying now could be a recipe for steep losses.

The Best-Kept Secret in Stock Investing

So where is this income investors’ wonderland, you ask?

I’m talking about mid-cap stocks, or companies with market capitalizations between $2 billion and $10 billion. They actually form the biggest segment of the market, but you’d never guess that, because for most analysts and investors, stock investing begins and ends with the sacred cows of the S&P 500.

That lack of attention is fine by me, because it gives us a much wider field in which to find overlooked bargains than we’ll ever have in the large cap universe.

Here’s something else few people know: mid-caps have quietly delivered bigger gains than large- and small cap stocks over the past 20 years.

It’s not even close. Here’s how the S&P MidCap 400 Index, with a median market cap of $3.5 billion, has performed compared to the S&P 500 and the S&P SmallCap 600 (with a median market cap of $1.0 billion) over the past 20 years:

Along with reasonable valuations, there’s another ingredient I always add to the mix when I’m combing the mid-cap universe (or any universe, for that matter): a record of surefire dividend growth.

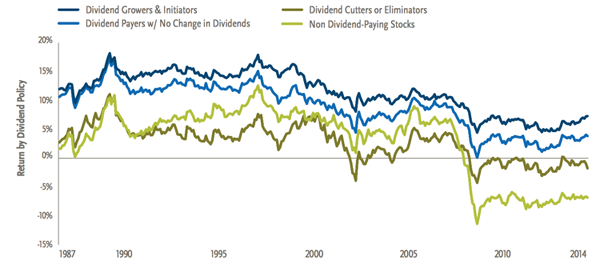

If you’re a regular reader of my articles on Forbes or ContrarianOutlook.com, you know I’m a big fan of dividend-growth stocks. The reason is simple: they outperform all other stocks over time, according to Ned Davis & Associates, whose researchers recently looked at stock returns from January 1972 through December 2014.

The key takeaway? Companies that steadily grew their payouts returned 10.1% on average over that 43-year period, compared to 7.7% for steady dividend payers and just 2.6% for companies that paid no dividend at all.

So it’s a no-brainer that we’d put dividend growth high on our mid-cap shopping list. But let’s make sure we’re careful enough to sidestep dangerous payout traps first – because there are more dividends in danger now than ever before.

3 Dividend Darlings Stocks to Sell Now

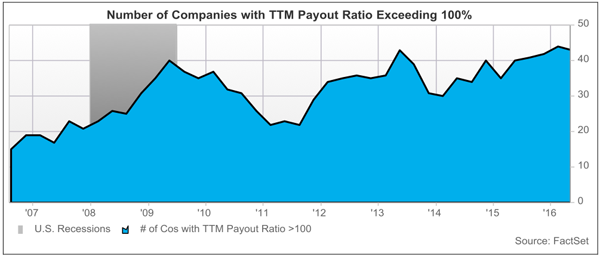

The latest numbers from FactSet show that 42 S&P 500 companies had payout ratios above 100%—so they’re paying out more in dividends than they’re earning.

While that may seem like a small percentage, at just 8.4% of the index, would you get on a plane that had an 8.4% chance of crashing?

I know I wouldn’t.

And yes, it’s also true that not all of these companies will be forced to reduce their dividends. Some will find ways to juice their earnings, either by growing sales, cutting costs, or a combination of the two.

But more and more are going the dividend-cut route. That makes looking beyond dividend yield, at factors like payout ratios, earnings, cash flow and balance-sheet strength more important than ever.

If that sounds like work, don’t worry. I’ve done it for you and have come up with three stocks with particularly wobbly payouts you need to avoid at all costs—or sell them if you already own them. Let’s makes sure we get this toxic trio out of your portfolio first – so that we can free up some capital to add our seven underappreciated dividend growers.

Sell #1: A Classic Yield Trap

Frontier Communications (FTR) is the kind of company you may be tempted to speculate on after a 30% decline in its share price in recent months.

The lure? A hefty trailing-twelve month dividend yield of 12%, which springs straight from the stock’s nosedive. But unless it’s money you’re really happy to lose, don’t take the bait. Because Frontier is far from bottoming, and its dividend is on borrowed time, with the company boasting a negative payout ratio.

When a payout ratio turns negative, it means management is paying a dividend while losing money! That’s about as close as you can get to a dividend cut, something Frontier investors already stomached in 2010 and 2012.

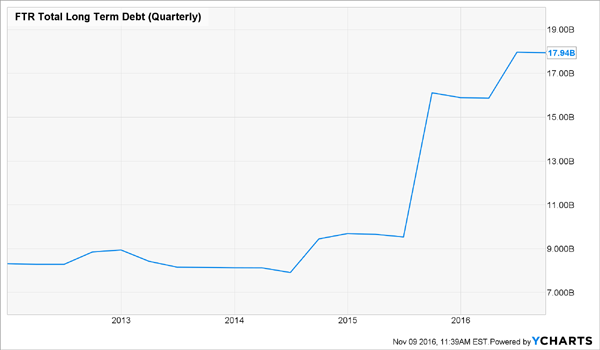

And today’s shareholders can’t count on the company’s balance sheet to back the payout up: FTR’s long-term debt now clocks in at $17.9 billion, or nearly five times its $3.7-billion market cap!

A lot of that debt comes from its $10.5-billion purchase of Verizon’s (VZ) wireline operations in California, Texas and Florida.

Trouble is, these customers are used to a level of service FTR simply can’t provide, which is why 99,000 broadband users jumped ship in the third quarter. The drop came as the two biggest telcos, AT&T (T) and Verizon, added Internet users at a rapid clip.

In hindsight, that exodus should come as no surprise from a company whose customer service ranked dead last among Internet service providers in this year’s American Customer Satisfaction Index.

The bottom line? Buying FTR (or any investment) based solely on a double-digit yield is a big mistake.

Sell #2: Mosaic’s Dividend Drought

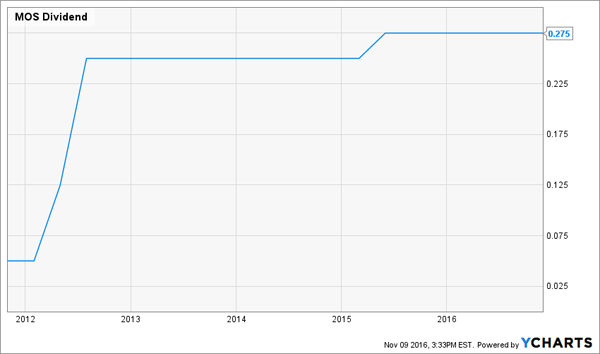

The Mosaic Co. (MOS) boasts a 3.8% trailing-twelve-month yield, which looks great on paper. Too bad it also boasts three dividend cut “warning signs”: falling earnings; a high payout ratio (87.5% of earnings and 128.6% of free cash flow); and a dividend that hasn’t seen a raise since June 2015.

Like all potash producers, Mosaic is struggling with a collapse in potash prices. In Q3, it sold potash for $165 per ton, down from $265 last year. The company expects higher shipments in 2017, but prices will likely stay weak, due to a glut Credit Suisse doesn’t see waning till the second half of 2017 at the earliest. That could push Mosaic’s payout ratio over the 100% “red line”—and put a dividend cut squarely on the table.

Don’t think it could happen? Ask shareholders of fellow fertilizer producers Potash Corp. (POT) and Agrium (AGU), who’ve swallowed dividend cuts of 34% and 27% this year, respectively.

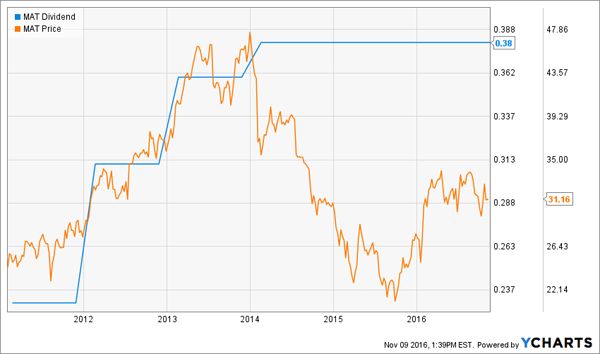

Sell #3: Mattel’s Stealth Dividend Cut

Mattel (MAT) isn’t facing the same level of dividend-cut risk as Frontier and Mosaic—its payout ratio clocks in at 142%, but if the company meets analysts’ expectations of $1.72 in earnings per share in 2017, it would be able to whittle that back to around 88%.

That’s still an alarmingly high figure that, at the very least, rules out a dividend hike in 2017. That would mean MAT’s investors will likely start 2018 collecting the same $0.38 quarterly payout they were back in early 2014!

That not only leaves them exposed to inflation but bodes ill for the stock price, too. Take a look at how the toymaker’s shares rose in tandem with its dividend increases—then dove when the dividend juice went flat:

MAT boasts a high trailing-twelve-month yield of 5% today, but with no dividend growth on the horizon, you can expect to still be yielding 5% on your initial buy two years from now. That makes Mattel a stock you need to keep well clear of your retirement portfolio.

For 100%+ Upside

Buy #1: Better Than Its Blue Chip Peer

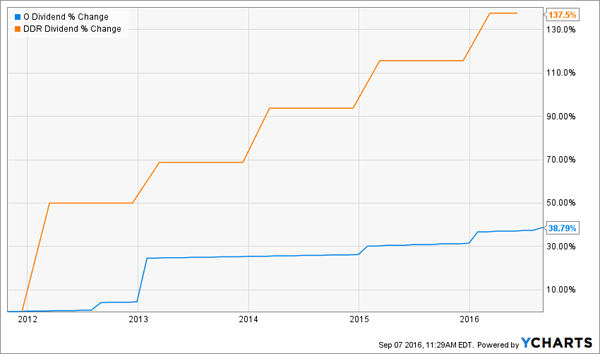

Retail landlord DDR Corp. (DDR) has a market cap of $7.0 billion and 352 malls across the US. It’s also a much better buy than the one name just about everyone thinks of when they think of retail REITs, Realty Income (O) of monthly dividend fame, with an $18-billion market cap and 4,600 properties.

Why do I say that? Because the upstart knocks out the champ in three key areas: dividend yield, dividend growth and valuation. That gives DDR a much surer path to outsized total returns than Realty Income.

DDR starts with a 5.0% dividend yield, besting its large cap cousin’s 4.4%. But dividend growth is where DDR really comes into its own, with a payout that’s skyrocketed 138% in the past five years. That’s more than triple the 39% increase Realty Income handed its shareholders!

Investors usually take notice of payout hikes like that and drive the shares into the stratosphere, but DDR’s rise pales next to Realty Income’s:

That tells me DDR still has lots of room to run as large cap REITs’ pricey valuations send more investors into the mid-cap space. C-level executive Alexander Otto agrees – he has been enthusiastically adding to his already-massive pile of shares this month. He’s been buying alongside other insiders – combined they’ve purchased over 531,000 shares (about $8 million worth) for their personal accounts.

Buy #2: A Mid-Cap Lodging Landlord

Apple Hospitality REIT (APLE) operates 179 hotels across the US under the Hilton and Marriott brands.

Don’t be surprised if you haven’t heard of it; the stock is a new issue, having only begun trading in mid-2015, and only five brokers cover it.

I’ll say upfront that the REIT doesn’t (yet) offer superlative dividend growth, having left its payout unchanged since its IPO, but you’re well paid from the start, thanks to its current dividend, which yields 6.5% and is well covered by FFO.

Here’s why I’m giving APLE the green light now: the REIT recently finalized its cash-and-stock purchase of Apple REIT Ten, which adds 56 hotels to Apple Hospitality’s portfolio.

How did Apple REIT Ten shareholders respond? By selling their new shares and sending APLE down nearly 6%!

Selling pressure like that is far from unusual after a merger, as shareholders in the acquired company suddenly find themselves holding a stock they didn’t pick themselves and hit the sell button to lock in their profits.

The drop is great news for the rest of us, because it’s cut APLE’s valuation even cheaper while pushing its already high dividend yield even higher. Plus, the new assets are a great fit with Apple Hospitality and will increase FFO over time.

Buy #3: An Unloved Dividend Star

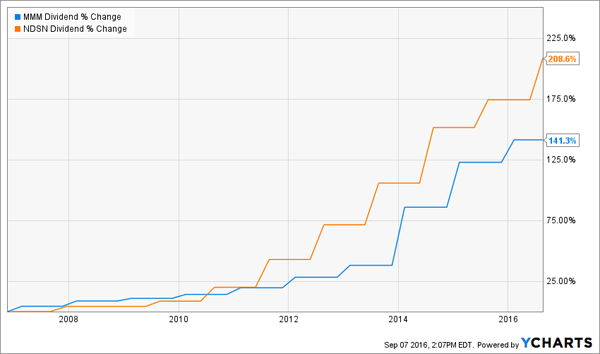

Nordson Corp. (NDSN) and 3M (MMM) both run “boring” businesses: Nordson’s gear dispenses adhesives, industrial coatings, sealants and just about any other fluid under the sun for clients in a range of industries. 3M sells more than 19,000 products in the US alone, ranging from pipe linings and sandpaper.

Something else they have in common? Both are translating steady demand for their products into steady dividend growth, with Nordson’s string of hikes stretching back 53 years, while its large-cap cousin’s goes back 58.

But to stay ahead of inflation and quickly boost the yield on your initial investment, you don’t just need regular dividend hikes, you need big ones, too. Here, Nordson shareholders win by a country mile:

A quarterly payout that’s more than tripled in the past decade makes the stock’s 1% dividend yield much easier to swallow, as you’ll quickly build on it—and overtake the 2.6% 3M pays out today—as the dividend hikes keep rolling in.

Buy Nordson now, before the strengthening US economy drives up demand for the company’s gear—and sends the share price out of reach.

Buy #4: A Retail REIT in the Bargain Bin

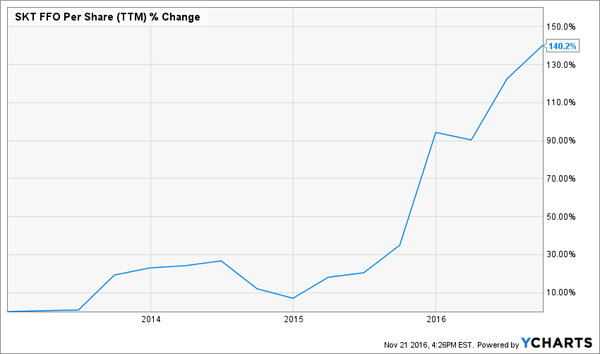

Tanger Factory Outlet Centers (SKT) is also hiking its payout at a rapid clip: in the past five years, the dividend is up 63%. The stock yields 3.8% today.

Tanger owns 42 open-air shopping centers in 21 states and Canada.

Most people think retail REITs will be among the hardest hit when rates rise, because they tend to carry a lot of debt to fund new developments. But this thinking ignores the upside of rising rates: they signal a growing economy, which drives up demand for (and rents on) Tanger’s space.

The REIT is already a top performer in this area, clocking big rent increases on renewed leases in the third quarter, while boosting its occupancy rate to 97.4%. Both factors are translating into skyrocketing FFO:

Even so, management’s staying disciplined: Tanger just opened its latest shopping center, in Daytona Beach, and plans to open two more, in Fort Worth, Texas, and Lancaster, Pennsylvania, next year.

If you’re still worried about rising rates, check out how SKT performed vs. the SPDR S&P 500 ETF (SPY) the last time rates headed up, from July 2004 through June 2006. It wasn’t even close!

If you’d asked me about this one back in June, I would’ve advised putting it on your watch list, but thanks to irrational interest rate fears, SKT is back where it was a year ago.

That’s handing us a rare second chance to buy. Throw in an easily covered dividend and this unsung midcap looks even better.

Buy #5: Come for the Dividend, Stay for the Gains

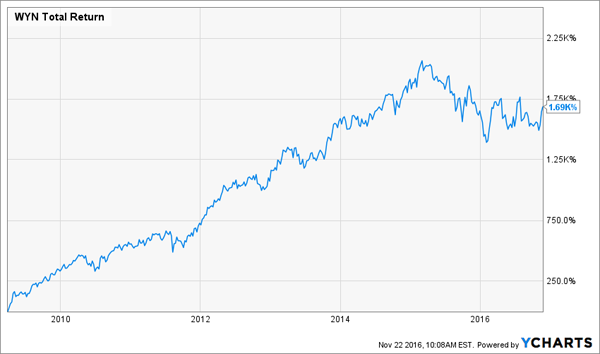

Wyndham Worldwide (WYN) boasts 7,800 hotels and 112,000 vacation-rental properties worldwide. The company has been expanding aggressively in China, where it now has more than 1,000 hotels. That positions it to profit as the country’s business-travel market—which is now the world’s biggest—booms.

To be sure, there are some risks here: Wyndham’s international business does expose it to currency fluctuations, for example, and there’s always the specter of Airbnb.

But this is a management team that knows how to execute: Wyndham launched its streamlined loyalty program last year and has since expanded it to let members use their points on experiences, vacation rentals and time-shares. Membership has surged from 41 million to 48 million members as a result.

Those members give Wyndham an edge over the sharing economy, as does the company’s expansion into other vacation properties beyond hotels.

What’s more, buying now locks in a trailing-twelve-month dividend yield of 2.6%, near highs not seen since April 2009—and investors who bought back then have seen a 1,690% total return in a little more than seven years.

Which brings me to dividend growth.

In the past five years, Wyndham has boosted its quarterly payout by 233%, and further hikes are a lock: the company has paid out just 37.0% of its last twelve months of earnings as dividends, and analysts are calling for a 9.3% increase in earnings per share in 2017.

Buy #6: The Global Engine

Cummins (CMI) makes engines for bulldozers and other heavy gear; industrial generators; and filtration and compression systems.

That makes it a cyclical business, and management would be hard-pressed to name one of its markets—from agriculture to mining and trucking—that isn’t weak right now. For all of 2016, the company forecasts a 10% sales drop.

But the 97-year-old firm is an old hand at navigating downturns, and it’s still generating gobs of free cash flow. It’s also keeping a tight lid on costs and a healthy balance sheet.

That’s let Cummins power up its dividend (which yields a tidy 2.9% today) by an amazing 1,038% in the past decade! And it’s not done yet, with dividends accounting for an easily manageable 53% of earnings and 46% of free cash flow.

A jump in US infrastructure spending could be just the tonic CMI needs. Throw in the fact that each previous revenue downturn has been a great time to buy the stock, and you get a blueprint for major upside:

Buy #7: 5,000 Key Industrial Parts

Parker-Hannifin (PH) is one step up the supply chain from Cummins, peddling the pumps, hoses, filters, regulators and other parts that go into the engines and other products companies like Cummins, Eaton (ETN) and Deere (DE) make.

But those companies can’t hold a candle to Parker when it comes to diversification: the company has 5,000 different parts in its catalog, which gives it a nice recurring revenue stream because equipment always breaks down, no matter what the economy is doing.

Parker also stands out for its whip-smart management team, which is steering through the cyclical downturn with ease. A boost from higher infrastructure spending would fatten its bottom line (and quarterly dividend) even more.

And My 3 Favorite “Accelerating” Dividend Growers With 200%+ Upside

While dividend growth is great, accelerating dividend growth is even better.

In fact, a single dividend hike that’s bigger than the market expects is often enough to light a fire under a stock.

To show you just how much buying “accelerating dividends” can juice your returns, I’m going to do something I don’t normally do.

I’m going to give away one of my best picks—normally reserved just for subscribers to my Hidden Yields research service—free, right here, today.

My publisher isn’t happy about this, but I like this company so much, I want to show it to as many investors as possible. And naturally, I’m hoping you’ll give me the opportunity to show you more double-digit dividend growers just like it.

Yours in payout profits,

Brett Owens

Chief Investment Strategist

Hidden Yields

Nothing in Contrarian Outlook is intended to be investment advice, nor does it represent the opinion of, counsel from, or recommendations by BNK Invest Inc. or any of its affiliates, subsidiaries or partners. None of the information contained herein constitutes a recommendation that any particular security, portfolio, transaction, or investment strategy is suitable for any specific person. All viewers agree that under no circumstances will BNK Invest, Inc,. its subsidiaries, partners, officers, employees, affiliates, or agents be held liable for any loss or damage caused by your reliance on information obtained. By visiting, using or viewing this site, you agree to the following Full Disclaimer & Terms of Use and Privacy Policy.