How to Retire on

11%+ Dividends

Paid Monthly

Inside this exclusive report you’ll discover:

- How inefficient markets could help us bank $100,000+ annually.

- 12 popular darlings that are ticking time bombs about to go off.

- The secret to living on dividends alone, without drawing down capital, and …

- 3 monthly dividend superstars paying up to 14.9%!

Dear Reader,

Look, I know I don’t have to tell you that all of our monthly bills are going up—and fast.

Inflation is still too high. And retirees (or those who are hoping to retire) feel it the most.

It’s no wonder more and more people think they’ll never retire.

Especially when the media goes on and on about the massive sums needed to clock out—sums that feel outdated the moment they’re released!

Not so long ago, we used to think a million bucks was enough to retire. Now, it seems paltry.

Well, I’ve got good news for you. You very well may be able to clock out on a realistic amount of money (much less than a million!)

I’m talking about just $600,000 here. And in some parts of the country you could do it on even less.

Got more? Great. I’ll show you how you can retire well on your current stake.

I know that’s a bit tough to believe, but stick with me for a few moments and I’ll walk you through it.

The key is my “9% Monthly Payer Portfolio,” which lets you live on dividends alone—without selling a single stock to generate extra cash.

And you’ll get paid the same big dividends every month of the year—so that your income and expenses will once again be lined up!

This approach is a must if you want to quickly and safely grow your wealth and safeguard your nest egg through the next market correction, too!

This isn’t just a dividend play, either: this proven strategy also has the potential to deliver 10%+ price upside in addition to your monthly dividends.

That’s the Power of Monthly Dividends

We’ll talk more about that price upside shortly. First, let’s set up a smooth income stream that rolls in every month, not every quarter like the dividends you get from most blue-chip stocks.

You probably know that it’s a pain to deal with payouts that roll in quarterly when our bills roll in monthly.

But convenience is far from the only benefit you get with monthly dividends. They also give you your cash faster—so you can reinvest it faster if you don’t need income from your portfolio right away.

More on that a little further on. First I want to show you…

How Not to Build a Solid Monthly Income Stream

When it comes to dividend investing, many “first-level” investors take themselves out of the game right off the hop.

That’s because they head straight to the list of Dividend Aristocrats—the S&P 500 companies that have hiked their payouts for 25 years or more.

That kind of dividend growth is impressive. But here’s the problem: These folks are forgetting that companies don’t need a high dividend yield to join this club—and without a high, safe payout, you can forget about generating a livable income stream on any reasonably sized nest egg.

Worse, you could be forced to sell stocks in retirement—maybe even into the kind of plunges we saw in March 2020 or throughout 2022—just to make ends meet.

That’s a nightmare for any retiree, and leaning too hard on the so-called Aristocrats can easily make it a reality: the ProShares S&P 500 Dividend Aristocrats ETF (NOBL), which holds all 69 Aristocrats, still yields just 2% as I write this.

Solid Monthly Payers Are Rare Birds …

You can certainly build your own monthly income portfolio, and the advantage of doing so is obvious: you can target companies that pay more than your average Aristocrat’s paltry payout.

Trouble is, only a handful of regular stocks pay in any frequency other than quarterly, so we’ll have to patch together different payout schedules to make it happen.

To do that, let’s cherry-pick a combo of well-known payers and payout schedules that line up. Here’s an “instant” 6-stock monthly dividend portfolio that fits the bill:

- Procter & Gamble (PG) and AbbVie (ABBV) with dividend payments in February, May, August and November.

- Target (TGT) and Chevron (CVX), with payments in March, June, September and December.

- Sysco (SYY) and Wal-Mart Stores (WMT), with payments in January, April, July and October.

Here’s what $600,000 evenly split across these six stocks would net you in dividend payouts over the first six months of the calendar year, based on current yields and rates:

You can see the consistency starting to show up here, with payouts coming your way every single month, but they still vary widely—sometimes by $1,425 a month!

It’s pretty tough to manage your payments, savings and other needs on a lumpy cash flow like that.

And the bigger problem is that we’re pulling in $19,100 in yearly income on a $600,000 nest egg.

That’s not nearly enough for us to reach our ultimate goal of retiring on dividends alone, without having to sell a single stock in retirement.

We need to do better.

Which brings me to…

Your Best Move Now: 9%+ Dividends AND Monthly Payouts

This is where my “11% Monthly Payer Portfolio” comes in. With just $600,000 invested, it’ll hand you a rock-solid $54,000-a-year income stream. That could be enough to see many folks into retirement.

The best part is you won’t have to go back to “lumpy” quarterly payouts to do it!

Of all the income machines in this unique portfolio, nearly half pay dividends monthly, so you can look forward to the steady drip of income, month in and month out from these plays.

That’s How This Grandma Makes

$387,000 Last Forever

A while back, I was chatting with a reader of mine who manages money for a select group of clients. He’d been using my Monthly Payer Portfolio to make a client’s modest savings – a nice grandmother who came to him with $387,000 – last longer than she ever dreamed:

“She brought me $387,000,” he said. “And wants to take out $3,000 per month for 10 years.”

The result? The last time I’d spoken with him, it had been over seven years since she started her $3,000 per month dividend gravy train. In that time, she’d taken out a fat $252,000 in spending money.

And that nest egg? She was still sitting on more than $258,000 after seven years and $252,000 worth of withdrawals.

Grandma’s Monthly Dividend Gravy Train

Her investments were paying fat dividend checks roughly every 30 days, neatly coinciding with her modest living expenses. And the many monthly dividend payers she bought dish income that adds up to 8% (or more) per year.

There’s no work to it; these high-income investments provide a “dividend pension” every month.

I’m ready to give you everything you need to know about this life-changing portfolio now. Let’s talk about Grandma’s secret – her high-yielding monthly dividend superstars (which even have 10%+ potential price upside to boot!)

Monthly Dividend Superstars:

11% Average Annual Yields

Most investors with $600,000 in their portfolios think they don’t have enough money to retire on.

They do – they just need to do two things with their “buy and hope” portfolios to turn them into $5,000+ monthly income streams:

- Sell everything – including the 2%, 3% and even 4% payers that simply don’t yield enough to matter. And,

- Buy my favorite monthly dividend payers.

The result? More than $5,000 in monthly income (from an average annual yield just over 11%, paid about every 30 days). With potential upside on your initial $600,000 to boot!

And this strategy isn’t capped at $600,000. If you’ve saved a million (or even two), you can just buy more of these elite monthly payers and boost your passive income to $9,166 or even $18,333 per month.

Now we’re talking!

But if you’re a billionaire, sorry, you are out of luck. These Goldilocks payers won’t be able to absorb all of your cash. With total market caps around $1 billion or $2 billion, these vehicles are too small for institutional money.

Which is perfect for humble contrarians like you and me. This ceiling has created inefficiencies that we can take advantage of. After all, in a completely efficient market, we’d have to make a choice between dividends and upside. Here, though, we get both.

Inefficient Markets Help Us

Bank $100,000 Annually (per Million)

Fortunately for you and me, the financial markets aren’t 100% efficient. And some corners are even less mature and less combed through than others.

These corners provide us contrarians with stable income opportunities that are both safe and lucrative.

There are anomalies in high yield. In an efficient market, you wouldn’t expect funds that pay big dividends today to also put up solid price gains, too.

We’re taught that it’s an either/or relationship between yield and upside – we can either collect dividends today or enjoy upside tomorrow, but not both.

But that’s simply not true in real life. Otherwise, why would these monthly payers put up serious annualized returns in the last 10 years while boasting outsized dividend yields?

For example, take a look at these 5 incredible funds that pay monthly and soar:

This is the key to a true “Monthly Payer Portfolio” – banking enough yields to live on while steadily growing your capital. It’s literally the difference between dying broke and never running out of money!

But I’m NOT suggesting you run out and buy these funds.

Some have been on my watchlist and in our premium portfolios over the years, but I mention them only as examples of the potential ahead.

In a moment, I’m going to show you how to earn a passive $55,000 on a half-million … $110,000 on a million … and even more every year on anything higher. And get paid every month, too.

Plus, you won’t even have to tap your initial capital or “draw down” any of your valuable principal. I’ll even give you the specifics on stock names and tickers to buy. But first, a bit about myself.

My name is Brett Owens and I’m an unabashed dividend investor. Ever since my days at Cornell University and all through my years as a startup founder in Silicon Valley, I’ve hunted down safe, stable, meaningful yields.

My name is Brett Owens and I’m an unabashed dividend investor. Ever since my days at Cornell University and all through my years as a startup founder in Silicon Valley, I’ve hunted down safe, stable, meaningful yields.

For the last 10 years, I’ve been investing my startup profits and finding 7%, 8%, even 10%+ dividends with plenty of double-digit gains along the way. In recent years, I started writing about the methods I use to generate these high levels of income.

Today I serve as chief investment strategist for Contrarian Income Report – a publication that uncovers secure, high-yielding investments for thousands of investors. Since inception, my subscribers have enjoyed dividends more than 4 times the S&P 500 average, plus healthy annualized gains!

Of course, not all high-yield investments are buys. Some are nothing more than dividend traps, paying high stated yields that are simply not sustainable.

But if you know how to navigate the space, you can earn the types of returns and collect the big monthly dividends that my subscribers do – which means you may never have to tap into your retirement capital to pay your bills.

And getting started is easy.

I’ve put everything you need to know in an

exclusive report, Monthly Dividend Superstars:

Yields Up to 14.9% With Double-Digit Upside.

And I want to send it to you today for FREE.

In this private briefing, I’ll introduce you to three incredible income plays most people don’t even know about.

They’re among my favorite investments to keep your nest egg safe while still paying a generous dividend every single month, including:

- A bond fund that’s perfectly positioned as rates head lower and dishes out a sky-high 14.9% dividend.

- The brainchild of one of the top fund managers on the planet that’s throwing off an amazing 11.7% yield.

- And a rock-steady 7.4% dividend whose managers have guided it to an astonishing 1,500% total return since inception.

And because these big dividends compound quicker, they’ll turbocharge your net worth.

Imagine, instead of taking whatever returns the S&P 500 is handing out …

You can collect 8%+ yields on average and position yourself for 10% potential capital gains every year.

It makes securing your retirement a heck of a lot easier!

Then, once you’ve lined your portfolio with these superstars, I want to help you clean out any toxic assets that can derail your dreams.

I’ve seen it over and over …

Yield chasers hold onto what they think is a darling dividend payer, only to have it turn around and bite them hard.

Which is why I’ve compiled another special report for you called …

The Dirty Dozen: 12 Dividend

Stocks to Sell Now

High yields can be a warning sign of a stock in trouble.

That’s why I also want to send you another special report: “The Dirty Dozen: 12 Dividend Stocks to Sell Now!”

Inside this report, you’ll discover 12 ticking time bombs that are lurking in the stock market right now.

Inside this report, you’ll discover 12 ticking time bombs that are lurking in the stock market right now.

Inside “The Dirty Dozen,” you’ll get the names of these 12 doomed stocks, along with a breakdown of why they could implode any day now, wiping out billions in value.

If you hold any of these stocks — and you likely do — I urge you to move your money to the investments you’ll discover inside my Monthly Payer Portfolio.

And you’ll need to do so right now, before they have ANY chance of crushing your returns in the coming year (and beyond).

Then, after these toxic assets are removed from your portfolio, it’s time to start filling it with even more great income plays that can win in any economy.

The Perfect Income Portfolio:

Safely 5X Your Income Today

In this guide, you’ll get all the details of what I call the “Perfect Income Portfolio.”

Step-by-step, I’ll show you exactly how to set up your portfolio for maximum income without taking on additional unnecessary risk.

And, if you follow the simple steps laid out, I’m confident you’ll be able to enjoy an income stream that far exceeds what most folks who buy the typical S&P 500 stock earn.

This report includes investments that have passed my strict due-diligence process—including one of the best ways I’ve ever seen to invest in utilities (which I’ve picked for further gains as interest rates move lower).

This fund pays a rich 7.8% today, holds some of the strongest electrical utilities in the country and trades at a bargain valuation (even though most investors don’t realize it). Its bargain status won’t last as rates inevitably tilt lower, pulling more investors toward its healthy payout.

I’ll walk you through each recommendation, giving you a clear, concise and easy-to-understand breakdown of exactly why I see these as “perfect” income plays.

Finally, I want you to have your very own copy of my personal playbook. It’s called…

Second-Level Investing: Your Guide

to the Contrarian Money Machine

Many super-investors agree that you’ll never beat the market by following the herd.

They tout the virtues of contrary thinking, but I’ve yet to hear any one of them specifically outline how they go about finding under-appreciated stocks with low valuations.

And that’s exactly what you’ll get with this step-by-step contrarian guide.

By following these steps, you’ll be able to find the types of stocks that Warren Buffett, George Soros, Howard Marks and many other greats only wish they could invest in.

The total value of all these reports I just went over are easily worth nearly $400.

I mean, just think about how these recommendations could potentially secure $3,000 (or more!) every month for the rest of your life on a portfolio of $500,000.

Now that I put it that way, they’re probably worth 10X that amount.

But none of that matters because…

I want you to see the entire

9% Monthly Payer Portfolio for FREE.

Think of these reports as your jump-start resource. They’ll point you in the right direction.

But I want to be your guide so that you can collect steady monthly dividends not just this year … but every year from here on out.

That’s why I’m also throwing in a 100% risk-free trial to my research service, Contrarian Income Report.

As I mentioned earlier, I’ve spent years scouring all corners of the market uncovering high-yielding investments that are safe enough to retire on.

Each month, I’ll deliver a streamlined intelligence report straight to your inbox. I’ll give you my candid take on what the mainstream is talking about.

And I’ll also tell you about the newest high-yield opportunities I come across.

As I write, our Contrarian Income Report portfolio boasts a diverse portfolio of stout dividends paying 8% on average, with several holdings yielding 9%, 11% and more.

Beats the heck out of the Dividend Aristocrats.

Beats the heck out of Treasuries and CDs.

And it sure beats the heck out of the S&P 500 and its pathetic 1.1% yield.

Imagine putting these high-yielders to work for you. All of a sudden, the monthly checks start rolling in and you can finally sit back and enjoy life.

Instead of stressing about your portfolio 24/7.

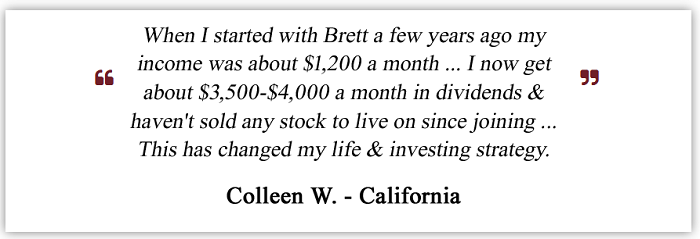

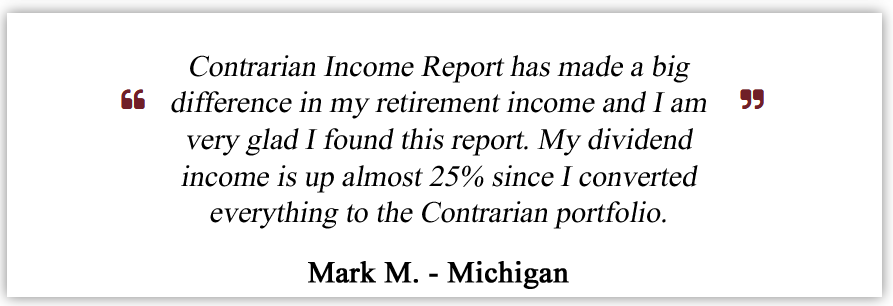

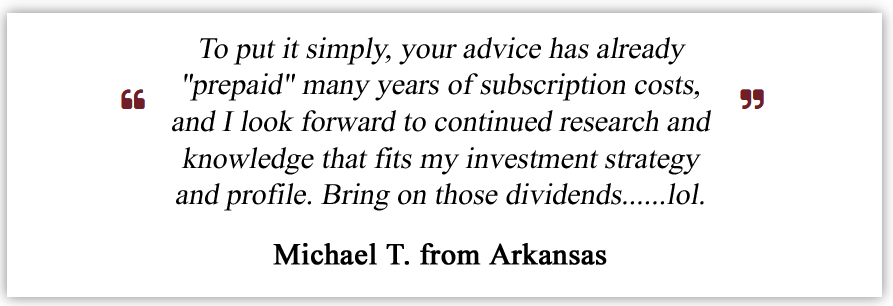

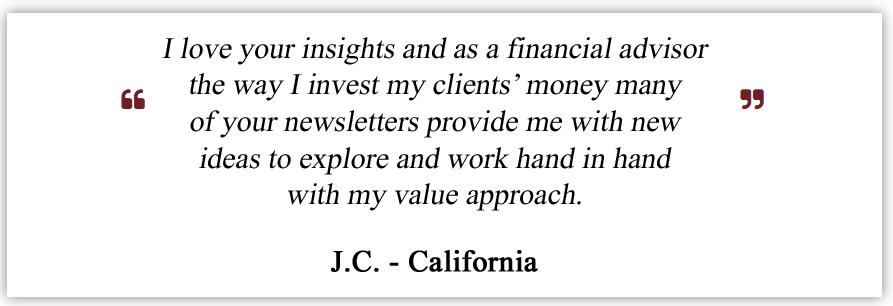

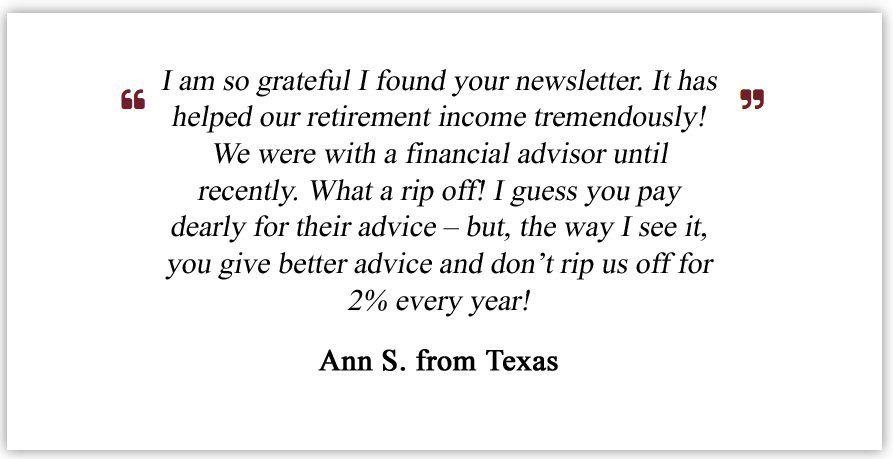

But don’t just take my word for it. I have letters piling up on my desk from happy subscribers.

Let me share a few with you…

Of course, not everyone follows my recommendations at the exact same time or in the same way. Each member’s personal financial situation is different, so your experience may also be different… but I’m thrilled to say there are dozens more stories just like these.

So let’s talk about what you can expect with Contrarian Income Report.

- Monthly research bulletins

You’ll get my latest high-yield opportunities delivered straight to your inbox. I’ll also update you on past investments I’ve recommended. That way you’re never caught holding anything that might cause you to lose your shirt.

- The Monthly Payer Portfolio

Financial advisors live and die by the 4% rule. But my contrarian approach lets you have your cake and eat it, too!

The Monthly Payer Portfolio pays you high enough dividends that you’ll never have to dip into your nest egg. Which is why you’ll want to know about it ASAP!

- Flash alerts

Any time there’s a change in our position, or general market malarkey happening, you’ll get a flash alert so you won’t be blindsided by bad news.

- A 24/7 members-only website

You’ll get access to a password-protected website where you can access current and past issues, the No-Withdrawal Portfolio and special bonus reports. No matter when you like to monitor your investments, everything is there for you around the clock.

- Quarterly Webinars

About every three months, you can attend a live, members-only webinar with me on current portfolio recommendations and get my thoughts on pressing member questions.

- A dedicated customer-support team

If you ever have questions about your subscription, you can simply call or email our customer service team in New York and they’ll be happy to take care of you.

Normally it costs $99 a year to join Contrarian Income Report.

In return, you’re getting recommendations that can deliver you thousands of dollars each month in a handbasket.

Still, I know I need to earn your trust and show you just how valuable Contrarian Income Report can be.

That’s why I’m willing to offer you an extraordinary deal…

You can enjoy an entire year of

Contrarian Income Report for just $39.

That’s 60% off the published price!

Oh yeah, one more thing…

As I mentioned earlier, I’m also going to give you a 60-day, 100% money-back guarantee.

That means you have nearly 2 full months to invest in my recommendations, track their progress, and try out all the tools and resources at your fingertips.

If at any time you don’t feel like my research service is right for you, just contact my team and they’ll refund every cent you paid. No hard feelings. No questions asked.

That’s it.

And all the bonus reports will be yours to keep.

Just my way of saying thanks for trying my service and giving me the chance to serve you.

So one last time…

Here’s everything you get when you join Contrarian Income Report today:

- 12 monthly research bulletins

- The full 11%+ Monthly Payer Portfolio

- Flash alerts

- A 24/7 members-only website

- Report #1: Monthly Dividend Superstars: Yields Up to 14.9% With Double-Digit Upside.

- Report #2: The Dirty Dozen: 12 Dividend Stocks to Sell Now.

- Report #3: The Perfect Income Portfolio: Safely 5X Your Income Today

- Report #4: Second-Level Investing: Your Guide to the Contrarian Money Machine

So you get a 60% membership discount, my five latest investment reports, weekly email updates and alerts and a 100% money-back guarantee.

Click the button below to secure all this for just $39.

In the coming months, many investors will continue to struggle with their paltry 2% and 3% payers, worrying and waiting for the next selloff.

But my Contrarian Income Report readers and I will rest easy thanks to our super-safe “11 Monthly Payer Portfolio” and enjoy potential 10% price gains over the next 12 months.

Are you going to join us?

Yours in profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

P.S. Remember, your risk-free membership comes with the names and full details on my top 3 closed-end funds paying up to 14.9%. You also get the investments in my “Perfect Income Portfolio,” including that utility fund kicking out a 7.8% payout.

Even a small position in any one of these picks could potentially cover a full year’s membership … most likely before your 60-day trial even ends!

© BNK Invest, Inc. – All Rights Reserved – Legal Information