Dear Reader,

Thank you for requesting your copy of my latest special report, How to Live off Huge Monthly Dividends — Practically Forever.

In addition to your free report, I’ve also arranged for you to receive a complimentary subscription to the Contrarian Outlook email newsletter. Inside you’ll receive my unique “second-level” analysis on dividend payers and growers so that you can maximize your portfolio’s current yield AND position yourself for strong upside, even in this volatile market.

Look for your first issue soon.

In the meantime, enjoy your free special report below.

Yours in payout profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

Brett Owens, Chief Investment Strategist

I don’t know about you, but I’m tired of the endless media reports that say you need a million bucks (and in many cases much more) to retire.

I’m tired of it because seemingly insurmountable figures like these are actively discouraging people from ever leaving the workforce: in July 2025, nearly one in four Americans over 50 polled said they are delaying retirement due to economic concerns.

But I have good news for you: the hyper-inflated numbers these so-called “experts” are throwing around are pulled straight out of thin air. It’s just another example of the lazy thinking that often plagues Wall Street.

The truth is, even after all we’ve been through in the last few years—a pandemic, inflation, trade wars and political volatility at home and abroad—you can still get the retirement you deserve, and on a lot less than the talking heads say you need.

How much less, you ask?

I’m talking about a fully paid-for retirement, with an income stream that outstrips the average wage of the typical working American, on a $700K stake—and possibly as little as $500K.

And get this: You’ll get paid every single month, too.

Best of all, when you buy into the two high-yield corners of the market I’ll show you in this report (and check out the 4 specific names I’ll reveal, yielding up to 8.2% now), you could live on dividends alone—without selling a single stock to generate cash.

Imagine that: With a secure income stream, you can forget about the market’s gyrations. With your capital intact, you could even leave a nice legacy for your kids, grandkids, a charity of your choice—it’s up to you!

Before I go further, I need to tell you something.

This approach isn’t for folks who want to stick with the plain-vanilla stocks most people are content to invest in.

It’s for savvy investors who are willing to invest just a little differently …

… who don’t mind stepping a little outside their comfort zone to bag the steady 8%+ dividends we need to get the retirement I just described.

So if you want to turn back here and continue “grinding it out” with the sub-2% dividends of the S&P 500, I can’t blame you. After all, it’s easy to invest in the familiar.

But those lame payouts mean you’ll have to consistently sell down your portfolio for extra cash in retirement. And it’s only a matter of time before you’ll be forced to do so straight into a downturn, just like many folks have been forced to do in the many pullbacks of the past, like the March 2021 crash, the 2022 mess and even the short-lived “tariff tantrum” in the spring of 2025.

A smooth income stream? Forget about it.

Almost all S&P 500 stocks pay quarterly instead of monthly.

Sure, you could stagger them so your portfolio pays you every month. But that forces you to pick stocks based mainly on their payout schedules, and I think you’ll agree that this is a poor way to build a portfolio. And it still doesn’t really work, as your monthly cash stream would still vary widely from month to month!

If you want to go beyond a chaotic cash stream and bank the outsized dividends you need for a “no-withdrawal” retirement (plus some nice price gains, too), read on.

Real estate investment trusts (REITs) are a natural draw for income-seekers because they usually pay much bigger dividends than the typical stock.

The last few years have been tough on REITs, with shopping malls in particular facing a years-long (and still going!) shift toward online shopping.

And then, of course, there were the pandemic shutdowns and the surging interest rates that followed. (High rates are particularly tough on REITs, which, of course, borrow to buy properties.)

Many REITs showed signs of life in 2024 and 2025 , but they’re still cheap by historical standards. And with lower interest rates likely in 2026 (thanks in part to new leadership at the Fed), the sun is starting to shine on these stocks again.

That setup—falling rates and still-cheap REITs—gives us a nice opportunity here. And this monthly payer looks particularly strong now.

LTC Properties (LTC)

LTC Properties (LTC) owns and invests in 187 senior-care facilities across America. About 62% are seniors’ housing (which help seniors live independently for as long as possible), and the rest are skilled nursing (for more frequent care).

Demographics are key to an investment in LTC, of course, with the REIT in the path of a wave of retirees that will only get bigger in the coming years.

Management has also done a great job managing its cost and risk. About 18% of its portfolio was added in 2025 through an acquisition of 1,580 units in Wisconsin. These properties are run in co-operation with Lifespark, a privately held firm that focuses on senior care. The rest of LTC’s portfolio is held either through triple-net leases (which essentially put all of a facility’s operating costs on the tenant) or through financing arrangements with other operators.

The REIT did a good job of maintaining its dividend throughout COVID, and the payout should find increased stability as demand for space in LTC’s properties allows it to acquire more buildings and increase its rents.

Throw in a high 6.7% yield and we’ve got a “megatrend-powered” payout that can bankroll our retirement by profiting from the wave of retirements washing across the country. Perfect.

Now that we’ve covered off our monthly REIT dividends, let’s move on to another favorite income play of mine—closed-end funds (CEFs), where big yields also abound.

Even better, CEFs give us one-click diversification, thanks to their broad portfolios of corporate bonds, US stocks, REITs and a wide range of other holdings.

We also benefit from their active managers, who have the backing of some of the world’s largest fund companies, like BlackRock. That helps CEFs regularly beat their indexes, particularly in areas like bonds and preferred shares.

I’ve got two CEFs for you to take a look at now. Both offer sky-high dividends:

CEF No. 1: Eaton Vance Tax-Managed Buy-Write Opportunities Fund (ETV)

Let’s start with blue chip stocks, where this fund, from Eaton Vance, a vaunted name in CEFs, plies its trade. ETV focuses on tech, with NVIDIA (NVDA), Microsoft (MSFT), Apple (AAPL) and Alphabet (GOOGL) all top holdings. It then adds its “secret sauce” to hand us an 8.2% dividend that, yes, is paid monthly.

That “secret sauce” is the sale of call options on these holdings. These give the buyer the right (but not the obligation) to buy stocks in ETV’s portfolio at a fixed price and a fixed point in the future.

If the stock hits that price, the buyer may purchase it (in which case it’s “called away,” in option-speak). If not, ETV keeps the shares. No matter what happens, ETV keeps the cash it collects (called a “premium”) for selling these options.

Finally, if you’re concerned about overvaluation in tech, ETV gives us a nice buffer here, thanks to its 8.2% discount to net asset value (NAV, or the value of the underlying portfolio). In other words, we get to buy its portfolio for 92 cents on the dollar. Cheap!

CEF No. 2: Reaves Utility Income Fund (UTG)

Utilities are a top sector for the next 12 months (and beyond) for two reasons: First, they’re a prime play on AI’s voracious appetite for energy. Second, they’re essentially “bond proxies.” That means they’re primed to gain as interest rates fall.

But the main snag with investing in the sector these days is that individual utilities’ dividends are fairly ho-hum, with the benchmark Utilities Select Sector ETF (XLU) yielding just under 3% today. That’s a lot better than the 1% you’d get from the typical S&P 500 stock, but we can do much better still with a smartly managed utility CEF.

Enter the 6.5%-yielding Reaves Utility Income Fund (UTG). The fund holds established regional utilities like nuclear-focused Constellation Energy (CEG), as well as CenterPoint Energy (CNP) and Louisiana-based Entergy (ETR).

And the management team at Reaves, an investment firm with 60 years of history, has delivered upside most investors can only dream of, with the fund returning an outstanding 770% since inception in 2004 (with dividends included—and little drama, to boot).

Best of all, much of that return has been in cash, thanks to UTG’s massive dividend. And you’ve got some reassurance that the fund’s share price will hold its own while you’re collecting that payout in the future:, as utilities have been far less volatile than the S&P 500, historically speaking.

Let’s wrap with business development companies (BDCs), another sweet source of high, and monthly, dividends. These firms, as the name suggests, lend money to small and medium-sized businesses, which often struggle to get loans from traditional banks.

These companies stand to benefit as interest rates fall and economic growth continues to hold up.

Why do I say that? For one, the administration is doing everything it can to stimulate the economy and bring down rates, which explains all the pressure heaped on Jerome Powell lately.

Beyond that, Treasury Secretary Scott Bessent has been effectively “capping” 10-year Treasury yields by borrowing money at short-term rates (controlled by the Fed) and using these funds to buy long-term bonds.

Finally, with midterms on tap, we can expect the administration to keep its stimulus “pedal” to the medal for most of 2026.

All of that (and we haven’t even talked about efficiency gains from AI) bodes well for small-business growth, and BDCs’ loan books.

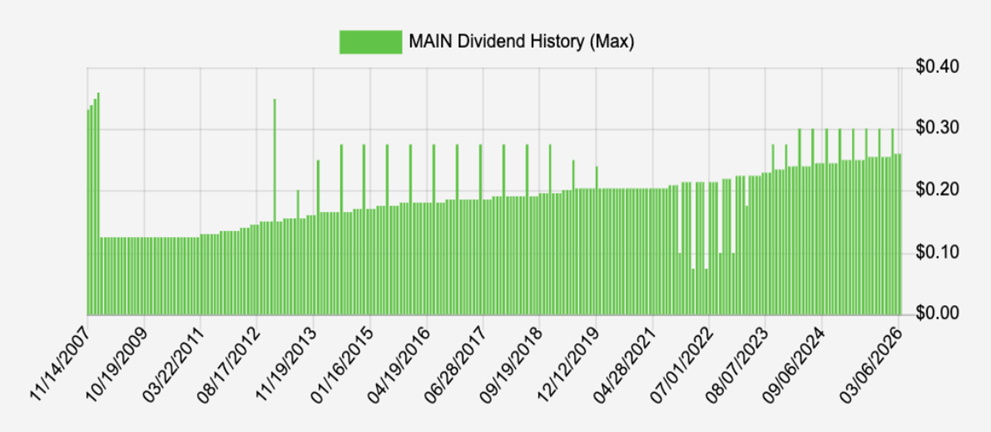

Main Street Capital (MAIN)

Lower rates mean more chances for BDCs to spur new loans—with Main Street Capital (MAIN), one of the biggest BDC players, likely to grab a healthy share.

Another reason why we like MAIN is that, while management doesn’t get specific, it did note in a recent investor presentation that its floating-rate loans “generally” include minimum “floor” rates. That helps it keep its interest income up in a lower-rate environment.

In other words, it’s free to build up the number of loans it offers, while getting assurance if rates fall too low. That’s a big plus, considering most of its loans are floating rate.

Then there’s the 7.1% yield, including MAIN’s regular “supplemental” payouts. Moreover, over its 18-year history, this ironclad lender has never cut or suspended its regular dividend, even during the pandemic or financial crisis. Check out this lovely payout picture:

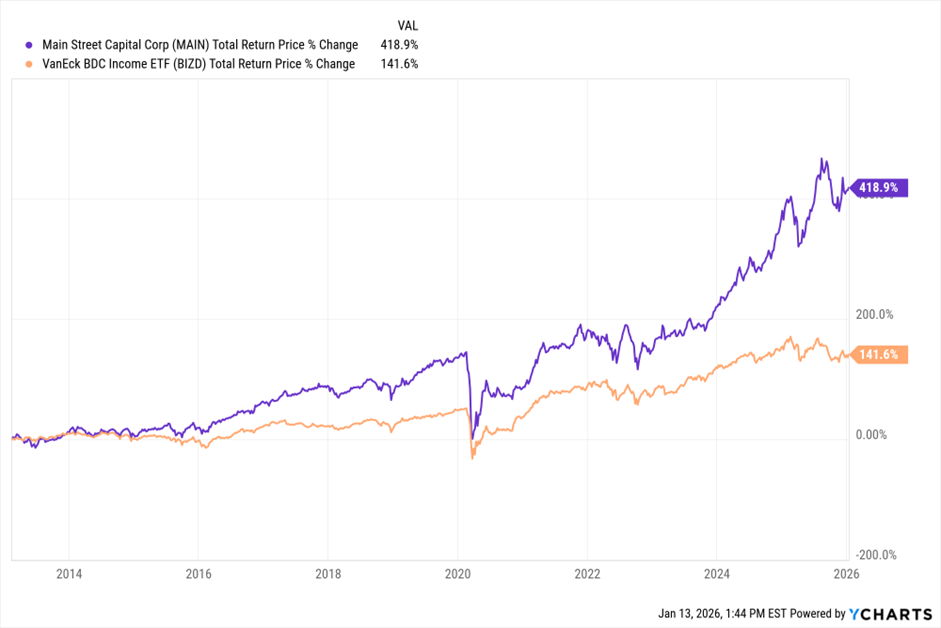

(And to be clear, those dips in the chart above aren’t reductions—they’re those “supplemental” payouts I just mentioned, as are the spikes.) No wonder MAIN has trounced the BDC index fund since that fund’s launch in 2013:

I expect more from this generous payer as rates quietly shift in its favor and the economy stays strong this year. As that happens, mainstream investors are almost certain to notice–and move toward this growing (and monthly paid) 7.1% dividend.

So where does this leave us? With the four picks above, you’d pull in an average yield of about 7%, plus you’d get wide diversification, with exposure to healthcare, blue chip stocks (with a lean toward tech), utility stocks and BDCs

So if you were to invest, say, $700,000—a full $300,000 less than the suits say you need for a healthy retirement—you’d generate around $49,000 in income.

That’s enough to retire on for some folks (or at least let them achieve financial independence by using their dividends to supplement other income sources). Plus you’re positioning yourself to nicely grow your nest egg, too, thanks to all five of our picks’ upside potential.

I think you’ll agree that a $49,000 income stream on a $700K nest egg is a pretty good deal. And the four stocks and funds above are one way to get there.

But they’re just a small taste of what’s possible: because my favorite monthly paying buys will get you that same $49,000 a year on a much smaller stake—possibly just a $500K nest egg.

I’ve put everything you need into a full library of special reports—and I want to give them to you, right now, FREE, starting with…

In this in-depth special report, I’ll reveal three incredible income plays most people don’t even know about.

They’re my absolute favorite investments to keep your nest egg safe while still paying a generous dividend every single month. They include:

- A well-hedged 14.9% payer in one of the most in-demand sectors right now,

- The brainchild of one of the world’s top fund managers that’s throwing off an amazing 9.6% yield,

- And a 9.4%-yielding healthcare fund quietly positioned to profit as AI slashes drug development timelines in half—trading at an 11% discount to its true value.

And because these big dividends compound quickly, they’ll help to turbocharge your net worth.

Imagine, instead of taking whatever returns the S&P 500 is handing out …

You can collect big, sturdy dividends like these and position yourself for 10% potential capital gains every year, to boot.

It makes securing your retirement a heck of a lot easier!

Then, once you’ve lined your portfolio with these superstars, I want to help you clean out any toxic assets that can derail your dreams.

I’ve seen it over and over …

Yield chasers hold onto what they think is a darling dividend payer, only to have it turn around and bite them hard.

Which is why I’ve compiled another special report for you called …

Stocks to Sell Now

High yields can be a warning sign of a stock in trouble.

That’s why I also want to send you another special report: “The Dirty Dozen: 12 Dividend Stocks to Sell Now!”

Inside this report, you’ll discover 12 ticking time bombs that are lurking in the stock market right now.

These are well-known, popular dividend plays that seem like great investments on the surface but are actually highly likely to blow up and lose as much as 20% of their value as a result of the Fed’s decision to keep rates “higher for longer” or other unfortunate economic moves.

Inside “The Dirty Dozen,” you’ll get the names of these 12 doomed stocks, along with a breakdown of why they could implode any day now, wiping out billions in value.

If you hold any of these stocks — and it’s likely that you do — I urge you to move your money to the investments you’ll discover inside my Monthly Payer Portfolio. And you’ll need to do so right now, before they have ANY chance of crushing your retirement dreams.

Then, after these toxic assets are removed from your portfolio, it’s time to start filling it with even more great income plays that can win in any economy.

In this guide, you’ll get all the details of what I call the “Perfect Income Portfolio.”

Step-by-step, I’ll show you exactly how to set up your portfolio for maximum income without taking on additional unnecessary risk.

And, if you follow the simple steps laid out, I’m confident you’ll be able to enjoy an income stream that far exceeds what most folks who buy the typical S&P 500 stock earn.

This report includes investments that have passed my strict due-diligence process—including one of the best ways I’ve ever seen to invest in utilities (in addition to UTG, above).

This fund pays a rich 7.8% today, holds some of the strongest electrical utilities in the country and trades at a bargain valuation (even though most investors don’t realize it). Its bargain status won’t last as rates inevitably tilt lower, pulling more investors toward its healthy payout.

I’ll walk you through each recommendation, giving you a clear, concise and easy-to-understand breakdown of exactly why I see these as “perfect” income plays.

Finally, I want you to have your very own copy of my personal playbook. It’s called…

Many super-investors agree that you’ll never beat the market by following the herd.

They tout the virtues of contrary thinking, but I’ve yet to hear any one of them specifically outline how they go about finding under-appreciated stocks with low valuations.

And that’s exactly what you’ll get with this step-by-step contrarian guide.

By following these steps, you’ll be able to find the types of stocks that Warren Buffett, George Soros, Howard Marks and many other greats only wish they could invest in.

The total value of all these reports I just went over are easily worth nearly $400.

I mean, just think about how these recommendations could potentially secure $3,500 (or more!) every month for the rest of your life on a portfolio of $500,000.

Now that I put it that way, they’re probably worth 10X that amount.

But none of that matters because…

Think of these reports as your jump-start resource. They’ll point you in the right direction.

But I want to be your guide so that you can collect steady monthly dividends not just this year … but every year from here on out.

Throughout the coming years, I’ll tell you exactly which high yielders to buy (and which to sell) so you can collect your healthy monthly payouts with less risk and greater peace of mind.

That’s why I’m also throwing in a 100% risk-free trial to my research service, Contrarian Income Report.

As I mentioned earlier, I’ve spent years scouring all corners of the market uncovering high-yielding investments that are safe enough to retire on.

Each month, I’ll deliver a streamlined intelligence report straight to your inbox. I’ll give you my candid take on what the mainstream is talking about.

And I’ll also tell you about the newest high-yield opportunities I come across.

As I write, our Contrarian Income Report portfolio boasts a diverse portfolio of stout dividends paying 8% on average, with several holdings yielding 9%, 11% and more.

Beats the heck out of the Dividend Aristocrats.

Beats the heck out of Treasuries and CDs.

And it sure beats the heck out of the S&P 500 and its pathetic 1% yield.

Imagine putting these high-yielders to work for you. All of a sudden, the monthly checks start rolling in and you can finally sit back and enjoy life.

Instead of stressing about your portfolio 24/7.

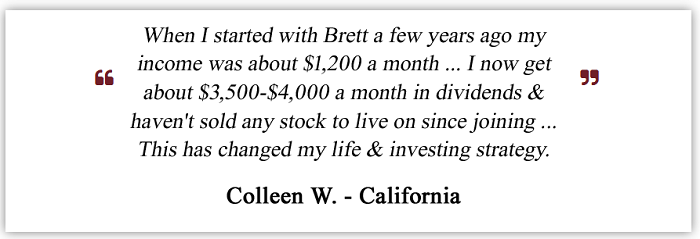

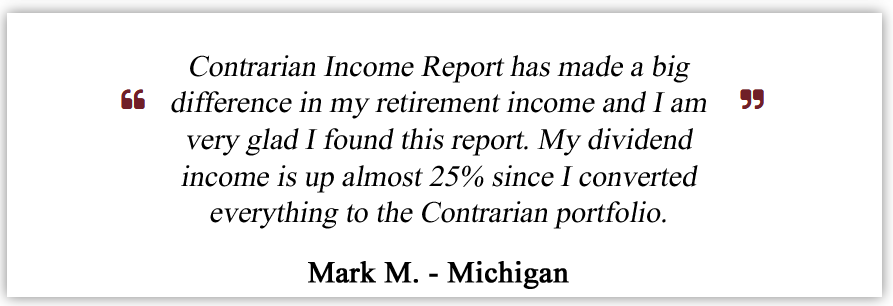

But don’t just take my word for it. I have letters piling up on my desk from happy subscribers.

Let me share a few with you…

Of course not everyone follows my recommendations at the exact same time or in the same way. Each member’s personal financial situation is different, so your experience may also be different… but I’m thrilled to say there are dozens more stories just like these.

Now let’s talk about what you get with Contrarian Income Report.

- Monthly research bulletins: You’ll get my latest high-yield opportunities delivered to your inbox, plus updates on current picks.

- Flash alerts: Any time there’s a change in our position, or general market malarkey happening, you’ll get a flash alert so you know how to respond.

- 24/7 members-only website: You’ll get access to a password-protected website where you can access current and past issues, special bonus reports and all of our current portfolio recommendations.

- Quarterly webinars: About every three months, I hold a private, members-only webinar to answer all your questions, live and unfiltered.

- A dedicated customer-support team: If you ever have questions about your subscription, you can call or email our customer-service team in New York and they’ll be happy to take care of you.

Normally Contrarian Income Report costs $99 a year. In return you’re getting picks that can deliver you thousands of dollars each month in a handbasket.

Still, I know I need to earn your trust and show you just how valuable Contrarian Income Report can be. That’s why I’m willing to offer you an extraordinary deal…

Oh yeah, one more thing…

I’m also going to give you a 60-day, 100% money-back guarantee.

That means you have nearly 2 full months to invest in my recommendations, track their progress, and try out all the tools and resources at your fingertips.

If at any time you don’t feel like my research service is right for you, just contact my team and they’ll refund every cent you paid. No hard feelings. No questions asked.

That’s it.

And all the bonus reports will be yours to keep.

Just my way of saying thanks for trying my service and giving me the chance to serve you.

So one last time…

Here’s everything you get when you join Contrarian Income Report today:

- 12 monthly research bulletins

- My full 9%+ Monthly Payer Portfolio

- Flash alerts

- A 24/7 members-only website

- Report #1: Monthly Dividend Superstars: Yields Up to 14.9% With Double-Digit Upside.

- Report #2: The Dirty Dozen: 12 Dividend Stocks to Sell Now.

- Report #3: The Perfect Income Portfolio: Safely 5X Your Income Today

- Report #4: Second-Level Investing: Your Guide to the Contrarian Money Machine

So you get a 60% membership discount, my five latest investment reports, weekly email updates and alerts and a 100% money-back guarantee.

Click the button below to secure all this for just $39.

In the coming months, many investors will continue to struggle with their paltry 2% and 3% payers, worrying and waiting for the next selloff.

But my Contrarian Income Report readers and I will rest easy thanks to our super-safe “9%+ Monthly Payer Portfolio” and enjoy potential 10% price gains over the next 12 months.

Are you going to join us?

Yours in profits,

Brett Owens

Chief Investment Strategist

Contrarian Income Report

P.S. Remember, your risk-free membership comes with the names and full details on my top 3 closed-end funds paying up to 14.9%. You also get the investments in my “Perfect Income Portfolio,” including that utility fund kicking out a 7.8% payout.

Even a small position in any one of these picks potentially could cover a full year’s membership … most likely before your 60-day trial even ends!

Nothing in Contrarian Outlook is intended to be investment advice, nor does it represent the opinion of, counsel from, or recommendations by BNK Invest Inc. or any of its affiliates, subsidiaries or partners. None of the information contained herein constitutes a recommendation that any particular security, portfolio, transaction, or investment strategy is suitable for any specific person. All viewers agree that under no circumstances will BNK Invest, Inc,. its subsidiaries, partners, officers, employees, affiliates, or agents be held liable for any loss or damage caused by your reliance on information obtained. By visiting, using or viewing this site, you agree to the following Full Disclaimer & Terms of Use and Privacy Policy.