Millions of investors are making a critical mistake that could leave their finances vulnerable—and at the worst possible time, too.

That error? Clinging to so-called “rules of thumb” that sound useful, but are so broad as to be almost irrelevant—even dangerous, depending on your personal circumstances.

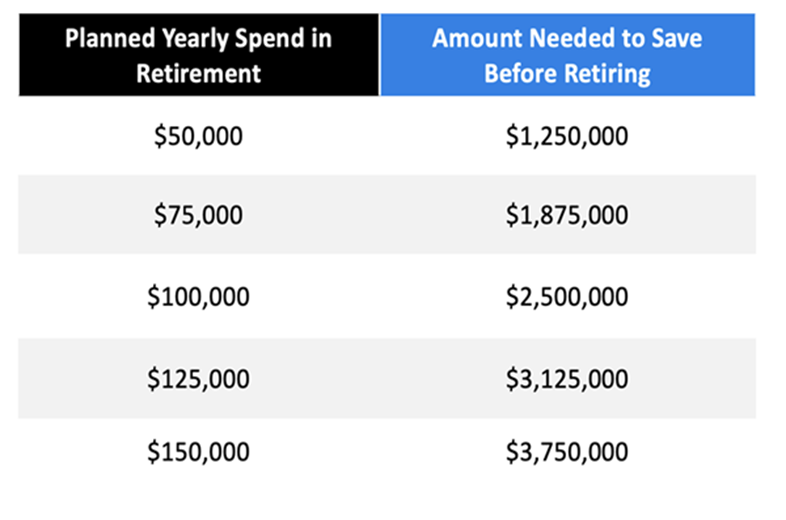

Consider the so-called “rule of 25,” which is as simple as it is deceptive. It simply states that, before we retire, we should have saved up 25 times the yearly amount we plan to spend in retirement.

That’s a lot! The chart below matches up how much a retiree plans to spend (setting aside inflation to make things a bit simpler) to see how much they’d need to save, going by this “rule.”

Now let’s say our hypothetical investor earns $100,000 a year and saves 20% (much more than the average American does) to get to retirement quickly. At that rate, assuming an 8.5% return from stocks (around the market’s historical rate of return), it’s going to take a bit over 29 years to get to retirement.

If you’re young, that might sound like a long time, and if you’re older, you might think you don’t have enough time to get there. In both cases, though, this anxiety is built on a false premise, because the “rule of 25” has been debunked by none other than its original author.

William Bengen invented the related “4% safe-withdrawal rate” based on historical research in 1994. What it basically means is that you need to have 25-times your retirement spending saved up for retirement. If you have less, you face the risk of running out of money when you’re very old, exactly the worst time to be broke.

However, Bengen updated his rule to 4.7% in 2022, based on updated data. So problem solved, right? Nope.

I mean, I guess that’s a little reassuring, as we’re now looking at something more like the “21.27-times rule.” Not a nice whole round number, to be sure, but at least it’s more grounded in actual data. But be that as it may, there are still a lot of assumptions in Bengen’s model.

There is, however, a much better alternative.

CEFs: The Key to a Faster Retirement

There are many closed-end funds (CEFs) designed to translate the long-term roughly 8.5% annualized historical returns of the stock market into a regular income stream that retirees can use to replace a salary.

For one example, let’s take the Liberty All-Star Equity Fund (USA), a broad-based equity CEF holding stocks like Microsoft (MSFT), Visa (V), Amazon.com (AMZN), Wells Fargo & Co. (WFC), Broadcom (AVGO) and other stalwarts of the US economy. As I write this, USA “translates” its profits from these stocks into a 10.6% current yield.

On that basis alone, we could say that an investor needs just $943,397 saved, which would take about 17 and a half years to get for someone making $100,000 and saving 20%, compared to the previously mentioned 29 for the so-called “rule of 25.”

Now I know that there are naysayers out there who attack CEFs, saying that these high payouts aren’t sustainable. And yes, USA’s dividend does float some, tied as it is to the fund’s underlying net asset value, or NAV. So let’s look at the history.

USA has been around for 39 years, and has paid about 82.4 cents per share per year on average in payouts in that time. That’s about 11.6% of the $7.13 at which its shares traded back in 1987, while the fund’s lower market price (since it gives out all of its profits as dividends) meant investors could get in or out of USA whenever they wanted.

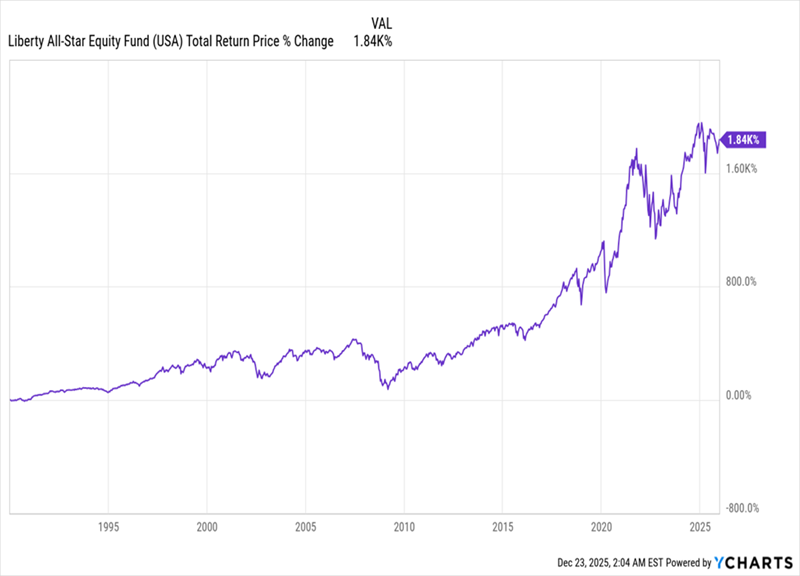

USA’s Price Chart Looks Worrying …

Now that lower market price may look like a concern. But USA gave retirees enough passive income to maintain their financial freedom throughout the end of the Cold War, the dot-com bubble, the housing bubble and Great Recession, and of course the slow recovery of the 2010s and the pandemic and its aftermath.

And here’s the real takeaway: This chart shows us what would’ve happened if an investor had reinvested their dividends back into USA.

… Until You Add the Dividends Back In

That’s a staggering 1,840% profit over several decades, thanks to this fund’s ability to “translate” profits into dividends that investors can either put back into the fund or use to pay the bills. USA, and funds like it, give us that choice.

4 MORE CEFs That “Translate” Gains Into CASH (They’re Top Picks for 2026)

I don’t know about you, but I’d rather not have to risk selling any shares into a selloff to keep my bills paid. That not only shrivels your income stream but your upside, as well.

That’s why we love CEFs like USA. With their 9%+ yields, these funds pay us enough in dividends to pay our bills, no matter what the market is doing.

This is exactly what my top 4 CEFs for 2026 are designed to do. Together, they yield a rich 9.2%, and they hold the top blue chip stocks, bonds and real estate investment trusts (REITs).

All 4 of them are ripe for buying now, as the calendar flips to the new year. Click here and I’ll walk you through each of these 4 solid income (and growth!) picks and give you a free Special Report revealing their names and tickers.