Be careful how you buy your bonds. The most popular tickers have four “fatal flaws” that’ll doom you to underperformance at best, or at worst leave you hanging in the event of a market meltdown!

Let’s pick on the widely followed and owned iShares iBoxx High Yield Corporate Bond ETF (HYG) as an example. It has attracted over $15 billion in assets because:

- It’s convenient and as easy to buy as a stock.

- It’s diversified (for better or worse, as we’ll see shortly) with 1,327 individual holdings.

- It pays well, at nearly 6% today.

The accessibility of funds like HYG appears cute and comfortable enough. But remember, ETFs are marketing products. They are designed to attract capital—not necessarily earn you a return on capital.

Big money is spent on television, print and online advertisements. Less cash and thought are put into the actual income strategies that ETFs employ–and their lagging returns reflect it.

Let’s pick on the four biggest flaws most bond ETFs suffer from. Then, I’ll share a superior and just as easy way to buy bonds.

ETF Fatal Flaw #1: Underperformance

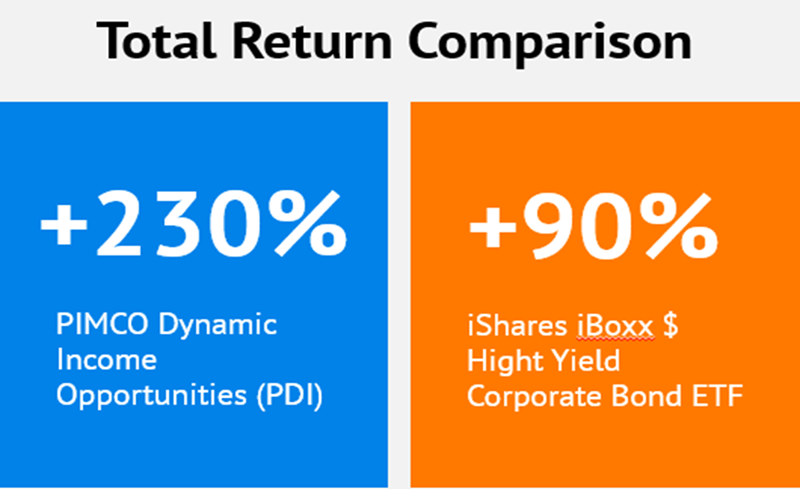

HYG is run by a computer. PIMCO Dynamic Income Opportunities Fund (PDI), on the other hand, is run by a bond-buying genius.

Dan “Beast” Ivascyn leads a fixed-income dream team at PIMCO. When deals become available, he receives the first phone call. PIMCO closed-end funds (CEFs) like PDI directly benefit from Dan’s expertise and connections.

So, it’s no surprise PDI has beaten the pants off HYG since PIMCO launched the fund in May 2012:

ETF Fatal Flaw #2: Wimpy Dividends

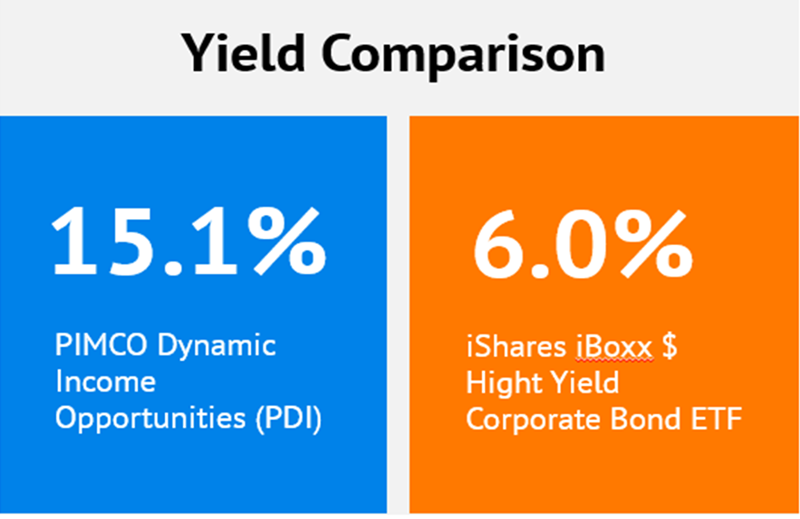

HYG pays 6%. That’s great–for vanilla investors, but pedestrian for us picky contrarians.

PDI yields 15.1% as I write.

Invest $100K in HYG, collect $6,000 per year in payouts.

But plunk $100K in PDI and bank $15,100 in passive income. More than double HYG’s dividends.

ETF Fatal Flaw #3: Ranking the Worst First

“Passive” methods—building portfolios based on rules—don’t work well in the land of bonds because fixed income expertise can’t be readily pre-programmed. Top managers can deliver truly top returns.

Here’s the main reason why bond indexing is bad. Let’s consider stock indexes, which are weighted by company size. Generally, the larger the firm, the more it matters in the index’s performance.

If you “buy by size” in the debt markets, it’s counterproductive. Stock market value for indexes doesn’t include debt, but bond markets are all debt by definition. Follow the computers in Bondville and you’d maximize your exposure to the bonds of the firms that borrow the most money!

That’s the opposite of what we’re looking for in bonds, where our goal is to maximize our “coupon” (the percentage yield) while minimizing our risk.

Let’s pick on HYG again. One of its largest holdings is SiriusXM (SIRI). Now I love SiriusXM radio. But I admit I’m a musical dinosaur–and I’d go broke buying bonds based on my own consumer habits!

(Confession: I’ve been a paying customer since 2013 when my Acura came fitted with Sirius and an extended free trial. I will give Bloomberg Radio the official credit for hooking me even though the “smart money” knows that the “80s on 8” station is indispensable too!)

Catching Asia Market’s Open on My Commute Home

Vehicle drivers have more audio options today. It’s easy to connect a mobile phone via Bluetooth, for example. SiriusXM’s “gravy train” of old users like me with ingrained habits is increasingly compromised.

As a result, SiriusXM takes on lots of debt—$9.2 billion to be specific—to keep the party rolling. How many people younger than your editor are opting for the SiriusXM installation on their new cars? These are not my favorite bonds.

And investors buying HYG are not going through this thought process!

ETF Fatal Flaw #4: False Sense of Liquidity

And here’s the “market meltdown” kicker on why you should always avoid bond ETFs:

They are subject to meltdowns if panic selling occurs.

Here’s why. If you sell HYG today, you’ll get your money in exchange for your shares. And it will be iShares’ problem to settle up their end (by selling those SiriusXM bonds and more).

Problem is, we’re talking about bonds rather than stocks here, and there is no readily available liquid market for that SiriusXM paper. Which means if a lot of selling occurs, HYG itself may take a hit if it has to unload its bonds at a discount (say, 70 or 80 cents on the dollar) to meet investors’ withdrawals.

CEFs like PDI don’t have this problem. They have fixed pools of assets, which help their managers ride out ups and downs. As long as they buy good bonds that are funded by reliable cash flows, they’ll be fine.

Pro Tip: There’s a Better Way to Buy Bonds

Fund selection matters more than ever today. Because the real opportunity in bonds right now isn’t trading them for price gains—it’s locking in serious income streams.

Funds like PDI are among my favorite holdings for anyone looking for steady, meaningful yield.

They deliver the kind of income most traditional bond funds simply can’t match—while being just as easy to buy as any stock.

More importantly, they allow income investors to do something incredibly powerful:

Live comfortably on dividends alone… without drawing down principal… without worrying about outliving your savings.

In fact, this idea—building a portfolio that pays our bills without forcing us to sell assets—is the cornerstone of my No Withdrawal strategy.

Please read on and I’ll share the details with you.