When it comes to high-yielding closed-end funds (CEFs), there’s one thing we always need to keep in mind:

Buying “new” CEFs can lock you into a big discount that never disappears.

That’s because, as we’ll see below, in the small world of CEFs, the market’s view of a new fund’s assets is often much less than what management thinks these assets are worth.

When that disconnect happens, big discounts are inevitable. But unlike, say, an established CEF that finds itself temporarily out of favor, the discounts on these new funds are far from being buying opportunities.

That’s because they can take a long time to close—if they ever do.

To show you what I mean, let’s look at the two newest CEFs on the block: the FS Specialty Lending Fund (FSSL), which went public in November 2025, and the Bluerock Private Real Estate Fund (BPRE), whose IPO was in December.

Since it hasn’t been long since either fund hit the market, it’s not surprising that their performance has been muted; BPRE is up about 3% since its IPO as I write this, and FSSL is up about 2.1%. But since we’re talking about less than two months’ worth of performance here, that doesn’t tell us much about each fund’s long-term value.

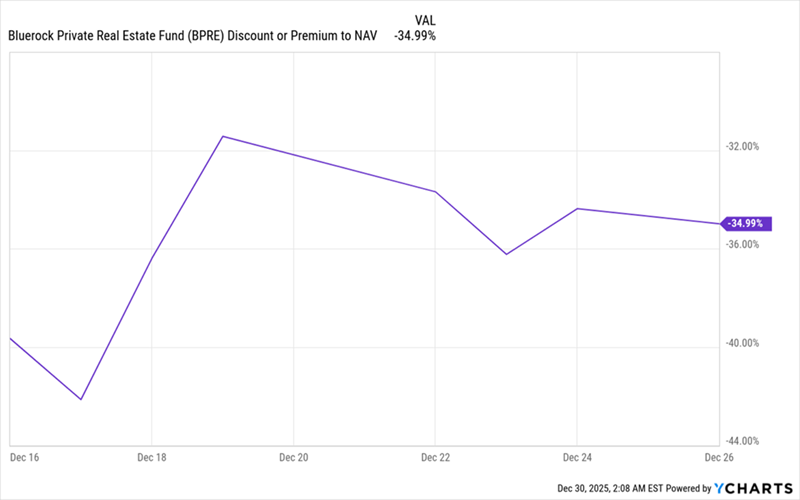

Then there’s BPRE’s discount story.

BPRE’s Massive Markdown

BPRE was originally a private, unlisted fund focusing on private real-estate assets. This meant you couldn’t buy or sell BPRE shares on the market and had to get them from the management firm. Similarly, the assets in BPRE’s portfolio were not easily bought and sold on public markets, making the fund doubly illiquid.

This was by design—it limited the number of investors who could get in or out. But over time, the fund’s investors wanted more liquidity, so management took it public.

When that happened, BPRE’s market price fell to 40% below the value of the assets in the fund’s portfolio. That discount to NAV has recovered a bit, but at 35%, it still makes BPRE the second-cheapest CEF out there. So in other words, BPRE’s earlier investors can sell, but they’d get about 35% less than they thought they would. Yikes!

Now let’s move on to FSSL.

FSSL’s IPO Also Fell Flat (and Its Discount May Not Recover)

Similarly, FSSL went public in November, after operating as a non-traded business development company (BDC)—a type of firm that makes loans to small and mid-sized businesses. As with BPRE, investors wanted the ability to trade the fund more freely, so they asked FSSL to make that happen. And so management went through an IPO.

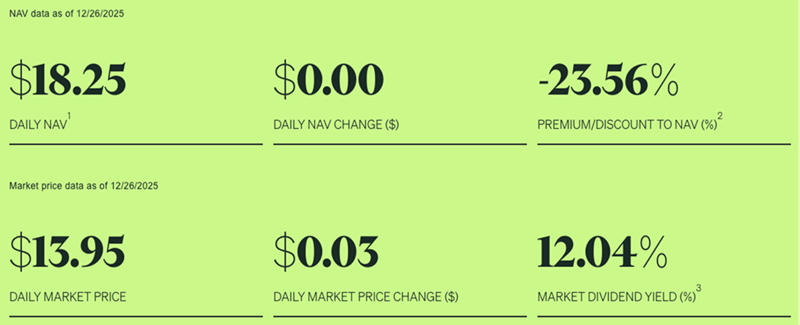

Then the fund dropped to a 23.6% discount, as you can see at the top right below.

Another Big Discount

Source: FS Investment Solutions

A 23.6% discount is a better outcome than we saw with BPRE, but it’s still pretty wide. As with BPRE, the market looked at FSSL’s book of business loans and determined that it was worth $13.95 a share, well below the fund’s in-house view of $18.25.

Again, investors could sell, but they’d do so for much less than they thought they’d be able to.

But with that in mind, if you’re wondering why more investors don’t just take the hit and walk away, the reason is that number in the lower right-hand corner of the image above: FSSL is offering a 12% yield, and big yields appeal to a lot of investors.

However, if FSSL’s assets are worth less than management expected, it’s also possible that FSSL’s incoming cash flow will be less than management expects, too, and dividends will get cut. Risks abound with this one.

A Well-Established CEF That Crushes These Newcomers, Pays a Growing 7.5%

The good news is that these two cases do not reflect all CEFs—far from it! Many CEFs are not heavily discounted. Some trade at premiums, and some trade at a discount now, traded at premiums in the past and may trade at premiums again. That last setup is a perfect opportunity for us to “game” these temporary discounts for gains, in addition to CEFs’ outsized dividends.

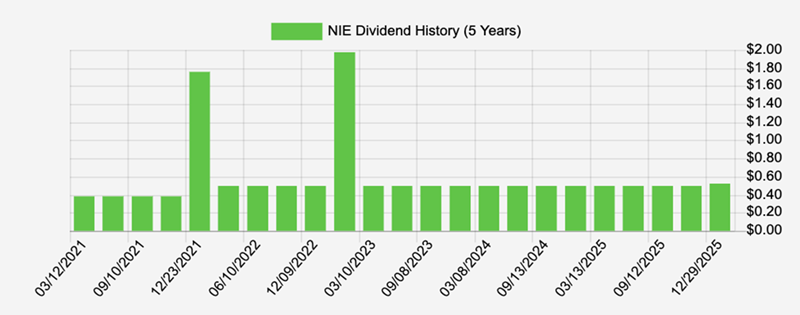

What’s more, many CEFs offer payouts that have been stable or rising for years. Consider the Virtus Equity & Convertible Income Fund (NIE), which I recommended in the March 2022 issue of my CEF Insider service. The fund holds some of the top US blue chips, including Apple (AAPL), Meta Platforms (META), Microsoft (MSFT) and Visa (V).

At the time of my recommendation, NIE yielded 7.6%. It now yields around 8%, thanks in part to a recent payout hike, which you can see at the right side of the five-year dividend chart below.

Source: Income Calendar

This dividend is reliable, and those two spikes are special payouts. Combining the dividends paid and capital gains, NIE is up a tidy 46% since my March 2022 recommendation, as of this writing.

Now here’s the real kicker.

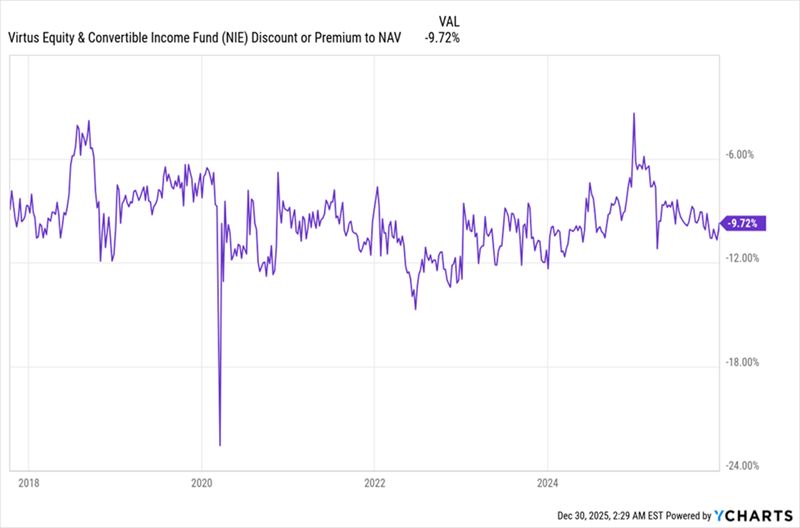

A Tradeable Discount

The fund’s 9.7% discount is a bit narrower than the 10.5% discount at the time of my recommendation. Notice how the discount was largely rangebound, with some spikes to below 7% and a few notable dips under 12%?

That’s the beauty of NIE—while we see it as a long-term holding at CEF Insider, in large part because of its reliable 8% income stream, you could choose to buy when its discount is in double-digits and sell when it’s less than, say, 7%.

You could then rinse and repeat this pattern. And if you combine NIE with another CEF, or other CEFs, with oscillating discounts, you’ve got a proven way to collect a high income stream while profiting from market mispricings.

That type of move is something we regularly do at CEF Insider, but it doesn’t necessarily happen when we simply buy the most heavily discounted CEF on the market. It’s even less likely for those who invest in unlisted CEFs, like the two we mentioned off the top, and wait for them to go public.

Your “Rinse and Repeat” Dividend Plan Starts With These Cheap 9.2% Payers

I want to give you a big headstart on this proven income strategy by giving you the names of my 4 top CEFs to buy now.

These 4 funds kick out a massive average yield (that’s right: a 9.2% dividend). They hold blue chip stocks, REITs and bonds issued by companies you know well. AND they’re cheap now—so much so that I’m expecting 20%+ price upside from them in 2026.

In the coming years, we’ll have plenty of opportunities to “lock in” our gains and move on to the next deep-discounted CEFs!

I’ll tell you more about these 4 powerful dividend plays right here. You’ll learn all about them and receive a free downloadable Special Report revealing their names and tickers.

That’s not all.

I’ll also give you an invitation to try CEF Insider with no risk and no obligation. These 4 funds are all in our portfolio now—and members get immediate alerts when it’s time to sell and flip to our next big yielder!

Don’t miss this chance to collect 9.2% dividends and ride these 4 funds’ discounts to strong gains. Click here and I’ll share our full strategy and give you your CEF Insider and that free Special Report revealing the names and tickers of these 4 funds.