We’re not even two weeks into 2026, and vanilla investors have already lost the plot. Their blindness has tossed 3 cheap—and growing—dividends into our laps.

More on this trio below. First, let’s look at 4 things the crowd has totally blown it on:

- The AI boom.

- A revolution in US manufacturing.

- The power of politics to shape markets, and …

- The Venezuela situation.

Let’s start with politics (I promise I won’t linger here for long!) because this year, everything will flow from it.

And, quite frankly, the fix is in here.

Truth is, we’re entering a period of “administered growth”: The administration has made clear that it wants cheaper borrowing costs, lower mortgage rates and less regulation for American businesses.

They’ll get a start via the One Big Beautiful Bill Act, which is set to deliver bigger tax refunds in just a few months. Then there’s the new Fed chief, who will likely push to cut rates right away once Jay Powell’s term ends in May.

And don’t forget, midterm elections! Politics powers payouts, and we know the administration wants a strong economy heading into November.

That’s the background for the opportunity we’re going to talk about today. Our other three drivers flow from it. Let’s get into them—and 3 dividends set to gain from each.

A “Pick-and-Shovel” Play on More—and More Automated—Factories

It doesn’t get much attention, but the real promise of AI isn’t in chatbots—it’s in robotics.

A December report from Manufacturing Automation showed that only 37% of US manufacturers use any real automation. But 73% say they’ll spend more on it in the next three years.

That’s a lot of growth runway.

What’s more, they say the #1 reason they haven’t automated more is because today’s systems don’t work for them. Enter AI, which lets machines adapt on the fly and take on more intricate work. That’ll boost productivity and cut costs.

Throw in lower interest rates and you have a recipe for solid growth here.

That’s a big plus for STAG Industrial (STAG), owner of 601 buildings in 41 states—a total of 119.2 million square feet in all.

STAG is a savvy “pick-and-shovel” play on manufacturing growth. Why would we try to pick winners in this cyclical sector when we can simply buy their landlord? And STAG is full to the brim, with 96.8% of its operating portfolio rented as of the end of Q3.

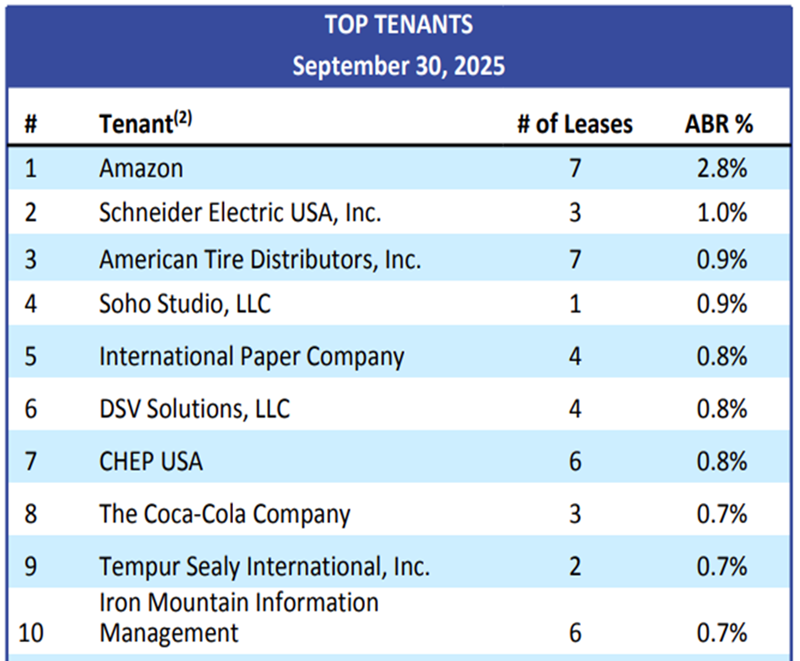

Its portfolio is tuned to the automation and “reshoring” trends washing across manufacturing, too. Look at its top-10 tenants (with, importantly, none making up more than 2.8% of yearly base rent).

Amazon.com (AMZN), whose warehouses are staffed in part by robots stemming from its 2012 acquisition of Kiva Systems , is #1 here:

Source: STAG Industrial Q3 2025 investor presentation

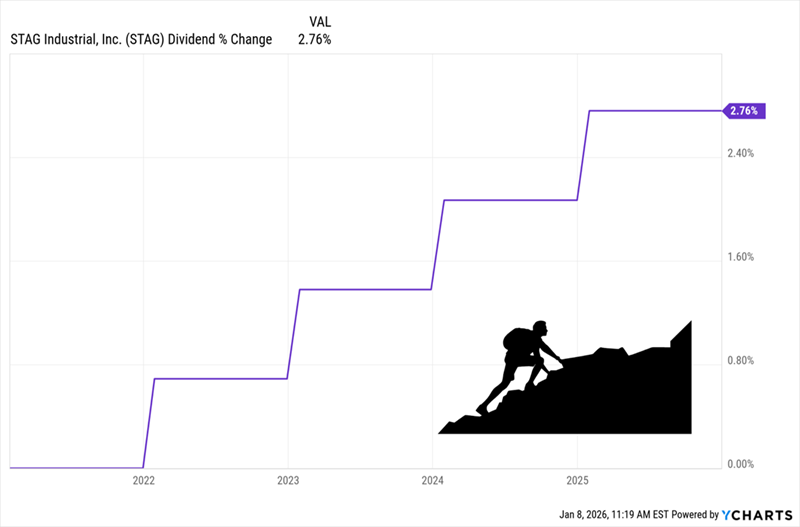

The standout is the dividend, which yields a rock-steady 4%.

Management is conservative with the payout, so we won’t see big hikes here—the divvie is only up about 3% in the last five years—but that payout is reliable, at just around 59% of core funds from operations (FFO).

STAG’s Slow-and-Steady Dividend

Besides, what STAG investors miss in payouts, they tend to make up in gains: Over the last five years, the stock returned 55% with dividends reinvested. With STAG trading at a reasonable 15 times its last 12 months of core FFO, we can expect more upside.

A Second Play on a Strong US Economy

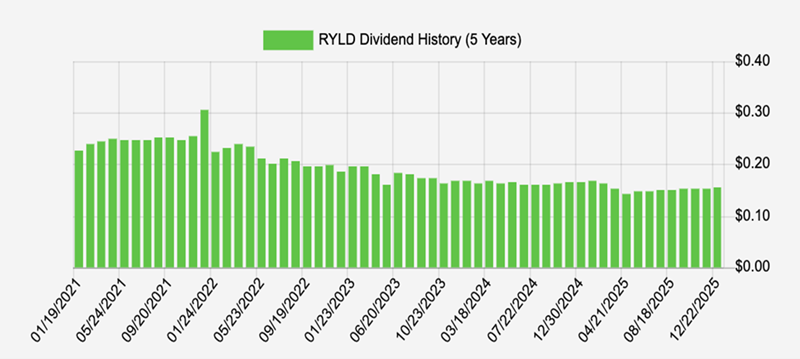

Next up, we’re going to boost our current yield with the Global X Russell 2000 Covered Call ETF (RYLD). The fund yields 11.7% and pays monthly.

Its formula for delivering that payout is simple: It holds a portfolio designed to mirror the Russell 2000 and sells covered-call options on that index. The Russell 2000 is made up of small cap stocks and is mostly US based. That makes RYLD a nice play on US growth, with a hedge against international uncertainty.

The covered-call strategy, meanwhile, is a great way to boost income as it pays the fund a fee whether or not the underlying security is sold—and that fee funds the dividend. This strategy also does well when volatility picks up, which is likely in the coming months.

The result has been a stable dividend that, yes, has been on the downslope in the last few years, but it started to gain after the April tariff panic. I expect that to continue:

RYLD’s Dividend 11.7% Dividend Bottoms, Edges Higher as Worries Mount

Source: Income Calendar

All of this makes RYLD a nice pickup for high income on strong US growth and higher volatility—both of which I expect this year.

Venezuela Strike Put This Canadian Oil Play on Sale

Finally, Venezuela, which Wall Street is treating like the next “black gold” rush. Vanilla investors piled into majors like Exxon Mobil (XOM) and Chevron (CVX) on the first trading day after the capture of Nicolas Maduro.

Trouble is, Venezuela’s oil system has been decaying for decades. It is beyond broken. (Fictional TV “landman” Tommy Norris is not taking a plane south to instantly fix it with a few phone calls, hard lines and Michelob Ultras!)

Look, these investors are right to look beyond America’s borders every once in a while, but in this case, they’re looking in the wrong direction!

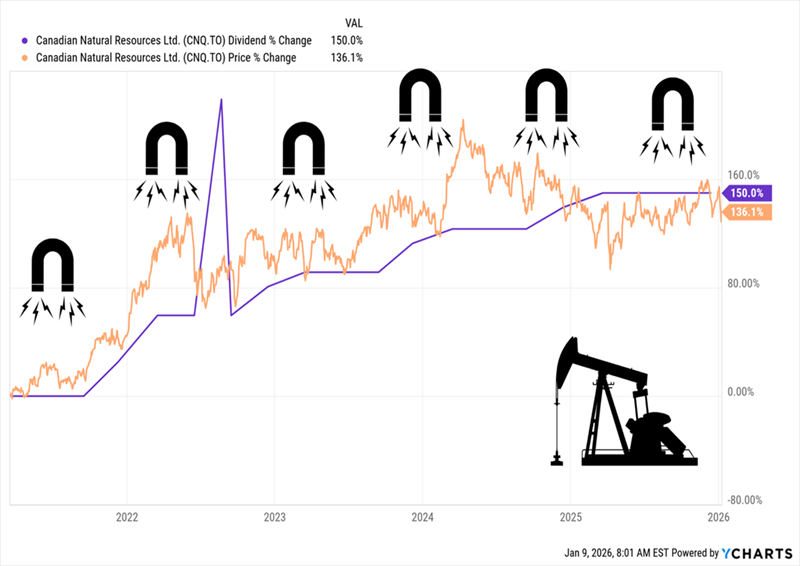

They should be looking north, to the Canadian oil sands, which produce a similar type of heavy crude as Venezuela. Unlike XOM and CVX, oil-sands producers sold off on the Venezuela news, including Canadian Natural Resources (CNQ) the largest producer of heavy crude in Canada.

That selloff was overdone, and CNQ’s shares have rebounded since, but they’re still off their highs and trade at just 13.8-times earnings (note that all figures are in Canadian dollars). That’s cheaper than CVX, at 22.5, and XOM, at 17.6.

Moreover, the company stands to gain as the government of Mark Carney goes all in on infrastructure and shifts toward oil (including a potential new pipeline). Meantime, CNQ yields 5.4%, and the dividend is a reasonable 59% of free cash flow. Production also hit a record in Q3: 1.6 million barrels of oil equivalent per day, up from 1.36 million a year ago. And if you think heavy crude means high production costs, get this: CNQ’s operating costs came in at just $21 a barrel in the quarter.

All of this opens the door to dividend hikes—which would act as a magnet on the share price. Check out how CNQ’s stock followed its dividend higher in the last five years.

Where CNQ’s Divvie Goes, the Stock Follows

Management is also shareholder-friendly, buying back 12% of CNQ’s stock in that time.

So don’t make the mistake of taking the Venezuela situation at face value. It’ll be years, if ever, before it affects the oil markets. And CNQ and its Canadian cousins could actually benefit, as they’re experts at developing oil fields like Venezuela’s.

5 More Buys for 15%+ Yearly Gains (in 2026 and Beyond)

These 3 stocks have proven they can keep their dividends rolling out, no matter what the economy does.

They’re also overlooked and sport the ironclad cash flows (and option strategies, in the case of RYLD) to get through any market shocks. That makes them perfect for Year 2 of Trump 2.0.

And they’re just the start.

Beyond this trio, I’m urging investors to buy 5 other dividend bargains. I’ve got each of these 5 stocks pegged for 15%+ gains in 2026, 2027, and well beyond.

I can’t wait to show them to you. Click here and we’ll walk through each of these 15%+ winners—and I’ll give you their names and tickers in a free Special Report.