Today we’re going to use a simple strategy to (legally!) beat the tax man. The key is a (too) often-ignored group of funds whose dividends are beyond the reach of the IRS.

The low-risk assets behind this income stream really should be part of any income investor’s portfolio. And the three funds we’ll discuss below, which yield up to 7.3%, are a great place to start. Thanks to their tax-free status, their “real” yields will likely be considerably more for us.

Enter “Boring But Beautiful” Municipal-Bond Funds

Here’s the truth on taxes: If you’re an American and you receive any kind of income, you’re going to get taxed. This is a constant of life. But there is one exception: municipal bonds, the income from which is tax-free for most Americans.

That tax-exempt status drives plenty of investors to muni bonds, making them a secret weapon for state and local governments and American industry, as these bonds fund many infrastructure and other public works projects around the country.

It adds up to a big difference-maker for many folks. A municipal, or “muni,” bond yielding 4% might not seem impressive at first glance, but for someone in the top federal tax bracket, this 4% tax-free yield is equivalent to a taxable yield of 6.6%.

And of course, the higher our “headline” muni-bond yields get, the bigger the taxable-equivalent yield: for that same taxpayer in the top federal bracket, for example, 5% yields turn into 8.3% on a taxable-equivalent basis.

Creating Your Own “Tax-Free Income Machine”

The best way to buy municipal bonds is through closed-end funds (CEFs), which give us three key advantages:

- Active management: The world of municipal bonds is challenging for individuals to access, so we want pros from well-established firms like BlackRock, Nuveen and others “running” our muni-bond portfolio for us.

- High yields: Plenty of muni-bond CEFs pay 4%, 5% and more, which, as we just saw, translates into a bigger yield on a taxable-equivalent basis.Discounts to net asset value (NAV): Because CEFs have more or less fixed share counts for their entire lives, they can, and often do, trade at different levels than the per-share value of their portfolios, and regularly at discounts. That lets us buy our “munis” for 90, 85 and sometimes even fewer cents per dollar of assets, as we’ll see in a moment.

With all that in mind, let’s go ahead and create a tax-free income portfolio with just three CEFs, all of which are diversified across municipalities, projects and credit ratings.

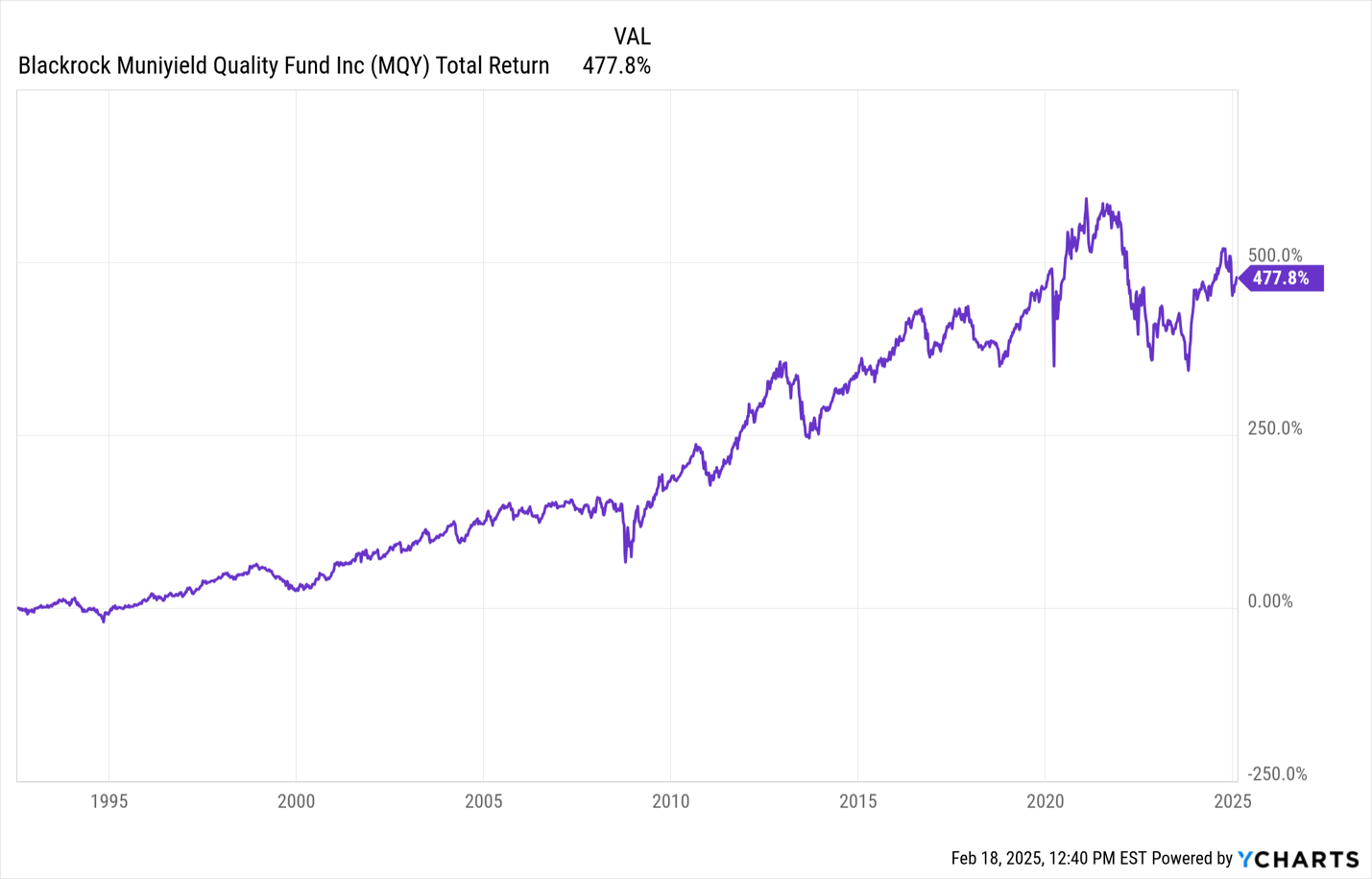

Muni Pick #1: BlackRock MuniYield Quality Fund (MQY)

MQY is notable for its consistent performance and ability to offer tax-free income for a long time, making it a great long-term hold.

MQY’s Long History of Profits

MQY currently trades at a 7% discount to NAV, so we’re paying 93 cents for every dollar of assets with this one. Cheap! Moreover, like all muni-bond funds, MQY dropped in 2022, as interest rates rose. But now, with rates having come down a bit, and likely to move lower over time, the fund is nicely positioned to grind higher, in addition to handing us a nice long-term (and of course tax-free) income stream.

The kicker here is that MQY’s 5.9% yield—already attractive on its own—“converts” to a 9.8% taxable-equivalent yield for top income earners.

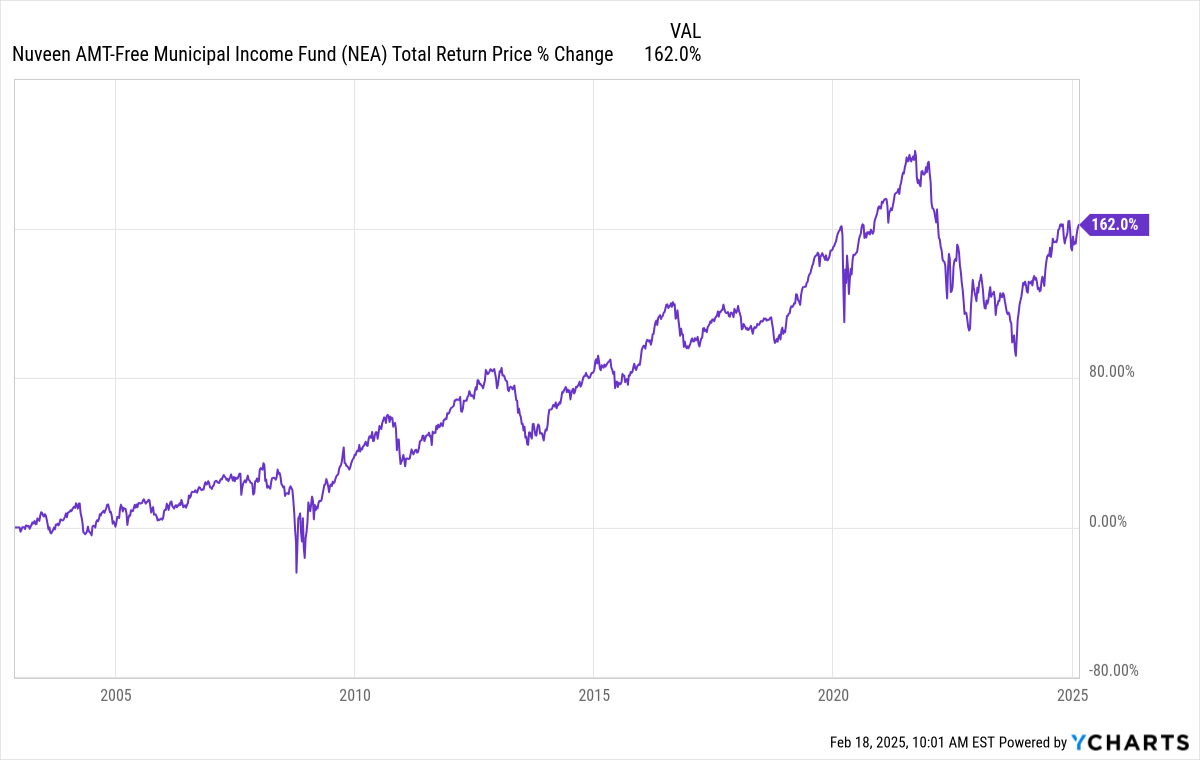

Muni Pick #2: Nuveen AMT-Free Quality Municipal Income Fund (NEA)

Let’s carry on with NEA, known for its strong management team (Nuveen gets access to high-quality municipal-bond issuances early, which is possible thanks to the company’s deep contacts in the muni-bond world and the fact that the muni market is small).

Like MQY, NEA trades at a discount (4.9% in this case) but its yield clocks in at a massive 7.6%, thanks in no small part to higher yields the fund has been able to lock in as interest rates rose and stayed elevated.

And like MQY, this fund has a long track record of healthy total returns, especially for a stable asset class like munis.

NEA Keeps Delivering Income and Gains

Bear in mind, too, that thanks to NEA’s high yield, much of that return has come in the form of dividend cash.

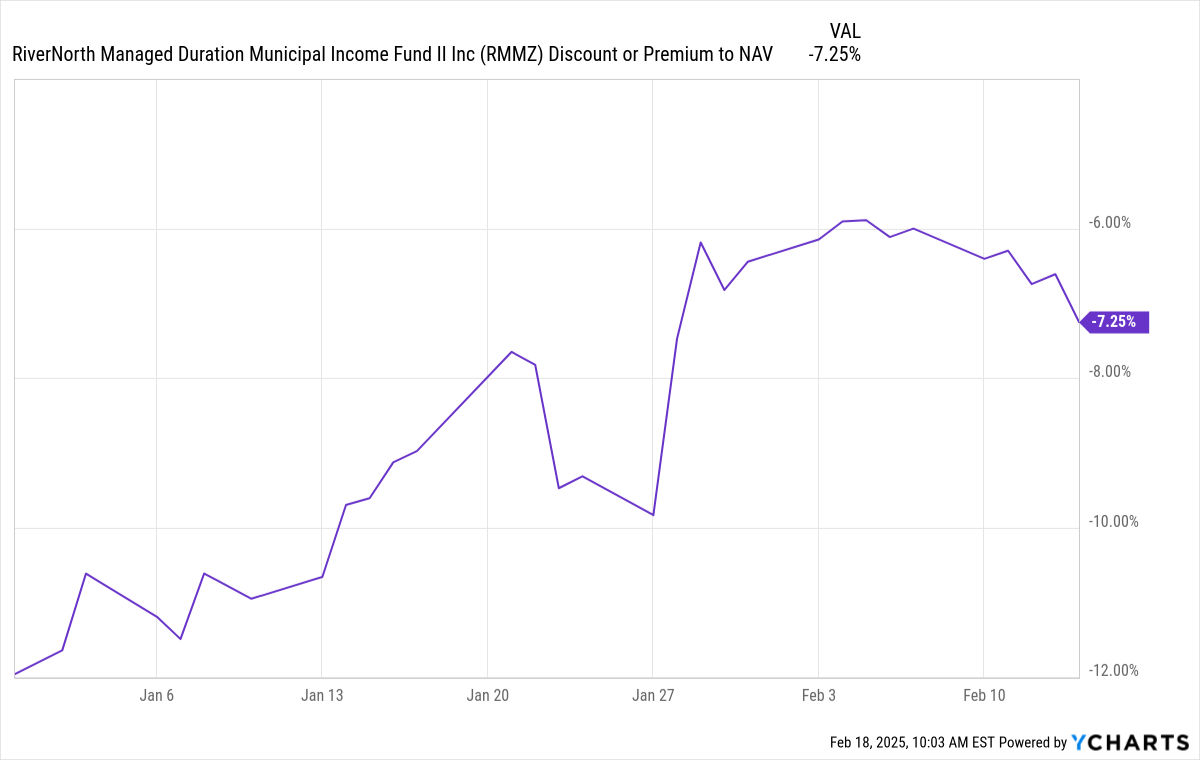

Muni Pick #3: RiverNorth Managed Duration Municipal Income Fund II (RMMZ)

Finally, for further diversification in the muni-bond fund space, consider RMMZ, which has an interesting method of managing duration and credit risk: It buys more individual municipal bonds when the muni market is hot, then leans more into buying other muni-bond CEFs when the market is cold and CEF discounts are unusually wide.

RMMZ’s Clever Approach to Maintaining Income

Source: RiverNorth Capital Management

This fund also trades at a wide discount to NAV—7.4% today—which is yet again a nice bonus for a high-yielding fund. But the real standout stat is RMMZ’s yield: 7.2%. On a taxable-equivalent yield basis, that’s 12%. Plus, RMMZ’s discount to NAV has been eroding, giving investors who buy at a discount the potential to sell at a profit as the discount shrinks.

RMMZ’s Discount Is Evaporating

RMMZ is far from perfect: its payouts were cut at the start of 2025 by two-tenths of a penny, and if that were to happen again, its current yield would “fall” to around 7%, with little effect on that 12% taxable-equivalent yield for our top income earner!

I don’t know about you, but that’s a pretty reasonable “downside” to me. The upside is that these funds all have diversified portfolios in municipal bonds, which sport just a 0.1% default rate across the asset class.

The bottom line: If you need a tax break (and who doesn’t?), these are three funds worth serious attention.

Play Defense With Munis. Then BUY These 10% Dividends for Trump 2.0 GAINS

I know there’s a lot of uncertainty out there, and these 3 muni-bond CEFs, with their stability and huge tax-free dividends, are the perfect way to protect your portfolio.

But we do NOT want to fully pull back into our shell. Because Trump 2.0, despite its disruption out of the gate, is going to set us up with some terrific income (and growth) opportunities in the coming years—and we do NOT want to miss out on those.

This is where my top 5 monthly dividend CEFs come in. They yield an amazing 10% and hold the best stocks, bonds, REITs—and even private equity investments—for big gains in the next 4 years.

And because these 5 stout income (and growth!) plays pay us monthly, we won’t have to wait long to grab our first big payout.