The broader market is expensive right now. Price-to-earnings (P/E) ratios in the 20s and even 30s and higher are the current “norm.”

No thanks—we’ll take a look in the bargain bin.

Today we’ll discuss a four-pack of dirt-cheap dividend payers dishing between 4% and 9.2%. They are much cheaper than their peers. Check it out:

- The S&P 500’s forward P/E (22.2) has only been this high twice in the past 40 years: the COVID bottom and recovery, and the dot-com bubble and burst.

- The small-cap Russell 2000’s forward P/E (26.5) isn’t in as rarefied air, but it’s still near the top of its historic long-term range.

- The Buffett Ratio (3.49) is as high as it has ever been. (The Buffett Ratio is the entire U.S. stock market’s value, as measured by the Wilshire 5000, divided by U.S. GDP.)

By contrast our four-pack pays up to 9.2% and is cheap according to a pair of classic value metrics:

- Price/earnings-to-growth (PEG): PEG measures earnings in relation to expected growth. In short, a PEG of 1 implies a stock is fairly valued. A number over 1 implies it’s overbought, and a number below 1 implies it’s oversold. Every stock we’ll discuss has a PEG below 1.

- Forward price-to-cash flow (P/CF): This looks at how a stock is valued compared to its cash flows. Every stock we’ll discuss has a forward P/CF that either ranks in the cheapest 20% of the S&P 500 (or would if the stock was in the S&P 500).

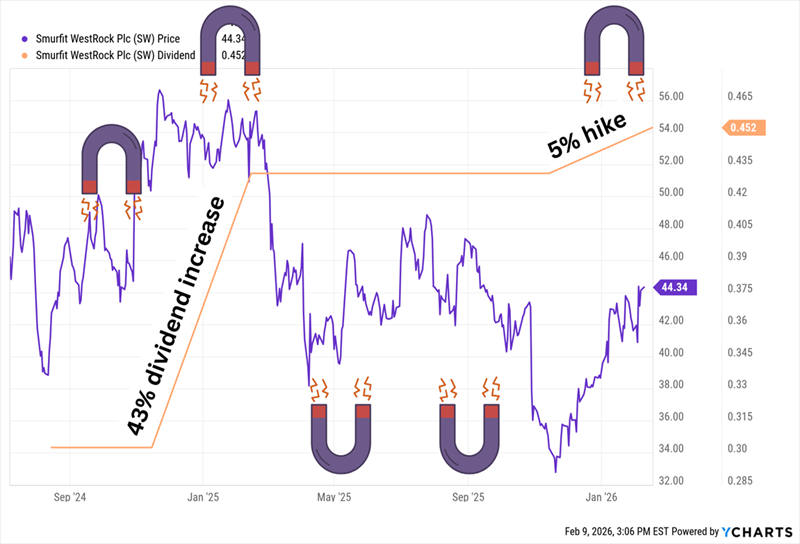

Smurfit Westrock (SW)

Dividend Yield: 4.1%

We’ll begin with Smurfit Westrock (SW), an Ireland-based consumer packaging giant serving 40 countries.

If the name is unfamiliar, that’s because Smurfit Westrock and its SW ticker have only been around in their current form for less than two years; they were created in July 2024 when Smurfit Kappa Group merged with the WestRock Company.

Smurfit produces containerboard, corrugated containers, solid board, kraft paper, graphic board, and a wide variety of other packaging materials, finished products, even packaging machinery. It does so primarily for consumer-facing business such as retail, e-commerce, consumer goods, food and beverage, and foodservice, though it also serves industrial companies.

Boring as it might be, it’s a growth business considering the megatrend in e-commerce driving the need for packaging. Analysts are forecasting a 27% bottom-line improvement for its soon-to-be-announced 2025 full year, and another 23% for 2026. Longer-term estimates peg the company’s annual earnings expansion at more than 30%.

Reality has been different than expectations; sales have grown for years, but profit growth has been inconsistent. As a result, Smurfit Kappa’s and WestRock’s stocks largely delivered up-and-down performance for years prior to the merger, and SW has been volatile but ultimately delivered flat performance since becoming the unified ticker.

Perhaps that’s why Smurfit Westrock trades at a cheap PEG of 0.53 and just more than 6 times cash-flow estimates. Still, those numbers stand in stark contrast to the kinds of growth projections we’d see out of a tech stock. SW has also delivered dividend growth during its short history; a massive 43% at the start of 2025, and a more modest 5% delivered just a few days ago.

After Years of Stagnant Payouts, SW Might Be Reactivating the Dividend Magnet

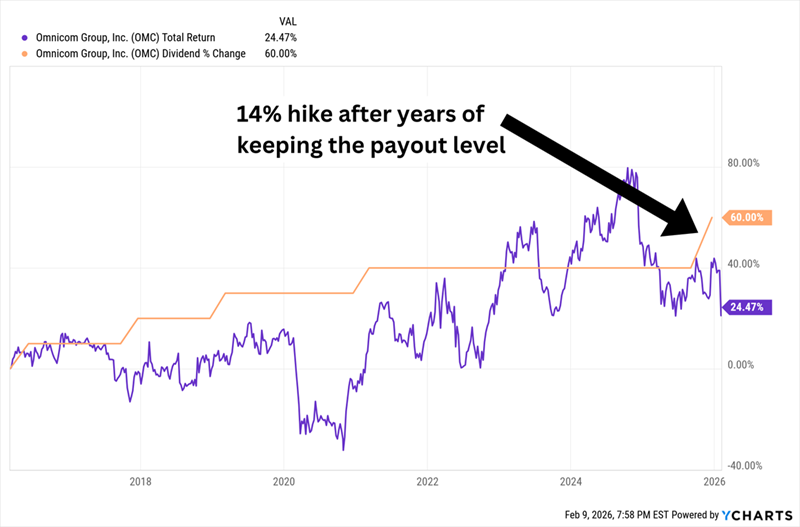

Omnicom Group (OMC)

Dividend Yield: 4.6%

Omnicom (OMC) is a massive global marketing, advertising, and communications firm that operates in more than 70 countries. Its businesses span media planning and buying, public relations, customer relationship management (CRM), advertising and other services.

It’s also a lot bigger than it was just a few months ago. That’s because in November, it closed on its $13 billion-plus acquisition of rival Interpublic Group, making the combined entity the world’s largest marketing and sales company. This business is now a sprawling mass of dozens of brands, including TBWA, McCann, BBDO, Acxiom, DotDotDash, TPN, Flywheel and more.

But while Omnicom has snapped up marketing properties like they were Infinity Stones, it hasn’t done much else. Consider this:

- Trailing-12-month (TTM) revenues are only 6% higher than they were 10 years ago.

- TTM profits are just 19% better

- OMC shares are actually down 6% on a pure price basis.

In fact, I could argue that of everything at Omnicom, its dividend has shown the most improvement over the past decade.

And the Most Recent Pay Bump Might be the Spark Shares Need

Omnicom shares have struggled to gain any meaningful momentum in large part because of continued macroeconomic uncertainty and a constantly changing tariff environment. Ad expenditures, of course, are typically among the first cuts companies make in a downturn, so it’s easy to understand bearishness toward OMC in the current climate. No wonder, then, that shares trade at less than 7 times cash-flow estimates and a thin PEG of 0.61.

That said, OMC’s merger with Interpublic is expected to be accretive to earnings, as well as generate $750 million in savings within two years of the deal’s close.

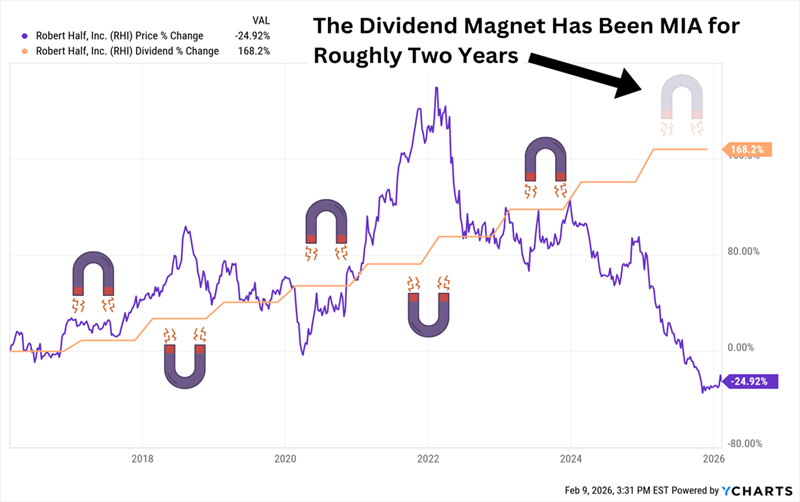

Robert Half International (RHI)

Dividend Yield: 8.0%

Robert Half International (RHI) is one of the world’s largest staffing companies. It predominantly works in three areas: Contract Talent Solutions (placing temporary workers with companies), Permanent Placement Talent Solutions (helping companies recruit and land full-time workers) and Protiviti (consulting services for compliance, finance, HR, legal and more).

We chatted about Robert Half just a few months ago as part of a broader review of companies Wall Street had soured on. Little has changed since; the majority of analysts covering RHI call it a “Hold” (which sounds neutral but is pretty bearish considering analysts tend to grade on a curve), and its “Sells” outnumber “Buys.”

Investors have also voiced their displeasure by hacking away two-thirds of Robert Half’s market cap since the start of 2024. Even then, RHI is value-priced but hardly super-cheap at under 10 times cash-flow estimates and a PEG of 0.95.

Still, the lashing has ballooned RHI’s yield to a fat 8%, so it deserves a little attention.

The primary reason Robert Half has been gutted has been fears that AI will drastically reduce the need for skilled white-collar workers, and thus reduce the need for Robert Half’s services.

Since then, the stock has stabilized, and it even managed an intense (albeit short-lived) surge after the company beat fourth-quarter earnings expectations near the end of January. The company returned to sequential, same-day, constant-currency growth for the first time since 2022, and management says it expects “continued positive adjusted sequential revenue growth for Talent Solutions.”

All of the above suggests Robert Half might be ripe for a rebound. So does the “Dividend Magnet” phenomenon, in which dividend growth should help tug shares higher over time.

RHI’s Dividend Magnet Does Disconnect, But It Usually Snaps Back

But fair warning: Robert Half is expected to under-earn its dividend this year and next. 2026 is a massive gulf, with RHI on pace to pay $2.36 in dividends while posting $1.48 in profits—a payout ratio of 160%! 2027 isn’t as bad, but $2.31 in profits would still fall short of the annual dividend at current levels.

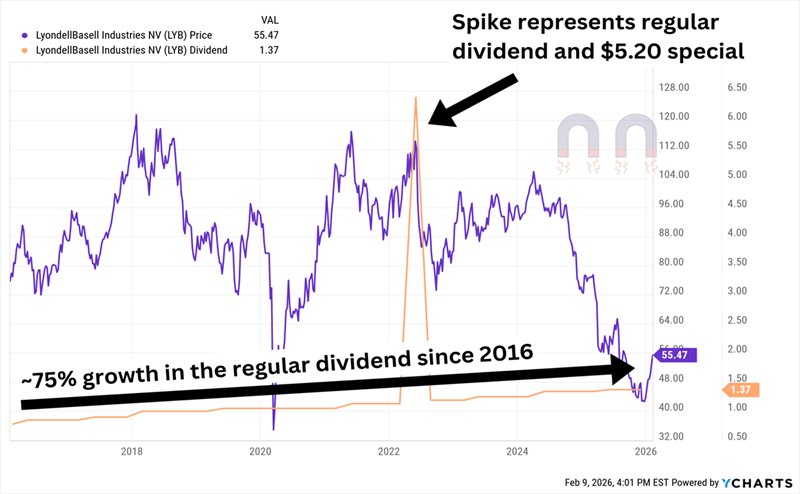

LyondellBasell (LYB)

Dividend Yield: 9.2%

LyondellBasell (LYB) is a Texas-based international chemicals giant that produces materials that provide durability, scratch-resistance and aesthetics to a variety of products, from garden equipment to appliances to furniture. They help produce rigid packaging, bottles and reusable containers in the healthcare industry. And they can improve thermal management, flame retardancy and water resistance in electronics, connectors and water systems.

Despite what appears to be myriad uses for the company’s offerings, LYB shares have been in a tailspin between early 2024 and the end of last year. Tighter regulations in Europe have rattled the entire chemicals industry, prompting LYB to announce in June 2025 that it would sell off four European assets. Inflation in raw materials and energy have also hampered the company.

2026 at least looks like the seeds of change. Despite posting a surprise loss, the company announced it will try to save $1.3 billion by the end of 2026. That helped continue the momentum of what has been a 30% bounce-back since Jan. 1. Yet even factoring in the rebound, shares remain deeply depressed and are worth about half of what they were in April 2024. A PEG of 0.45 and a forward P/CF of less than 9 are both well in value territory. A nearly 10% yield is downright gaudy.

Like Robert Half, the Dividend Magnet has gone completely out of whack. (Note that the chart below is distorted because of a massive $5.20 special distribution that more than doubled the payout for that year.)

LYB Shares Have Fallen Out of Orbit

As with Robert Half, LyondellBasell’s dividend is outpacing its earnings by a wide margin. Its current quarterly rate implies an annual distribution of $5.48 per share. The pros see it earning $2.58 this year (a 212% payout ratio) and $3.82 next (140%). Uh oh.

CFO Agustin Izquierdo recently admitted the company may have to “recalibrate the dividend.” We all know what that means.

This 11%-Paying Fund Is My Top Monthly Dividend Play for 2026

We could close our eyes, plug our noses and pray that LyondellBasell’s 9%-plus yield won’t blow up in our faces.

Or we could lock in an even sweeter 11% …

… from a diversified investment fund …

… that has increased its dividend over time …

… and paid out multiple special dividends …

… and doles out its regular dividends each and every month!

That’s a resume few income investors could resist. And why would we? This fund pays us $1,100 for every $10K we invest, and all we need to do is sit back, relax, and let a skilled manager call the shots.

Like most of the stocks above, this fund has flown well under the radar. But the time to sit up and pay attention is now, so we can start collecting this rich monthly dividend as soon as possible.