Let’s talk about companies that are serious about dividend hikes. I’m talking about recent payout raises of 25%, 67% and even 120%.

Know what happens to a stock that raises its dividend like this? Its shares skyrocket.

Consider Graco (GGG), a company that specializes in fluid-handling systems, serving everyone from homeowners and contractors to industrial and manufacturing businesses. Graco.com delivers one of the most beautifully boring boasts we’ll ever read, showing us the many mundane ways GGG has become a fixture in our lives:

“We pump peanut butter into your jar, and the oil in your car. We glue the soles of your shoes, the glass in your windows and pump the ink onto your bills. We spray the finish on your vehicle, coatings on your pills, the paint on your house and texture on your walls.”

This ubiquitous cash flow powers Graco’s “dividend magnet.” These peanut butter pump and shoe sole sales add up to sweet payouts that Graco raises year after year after year.

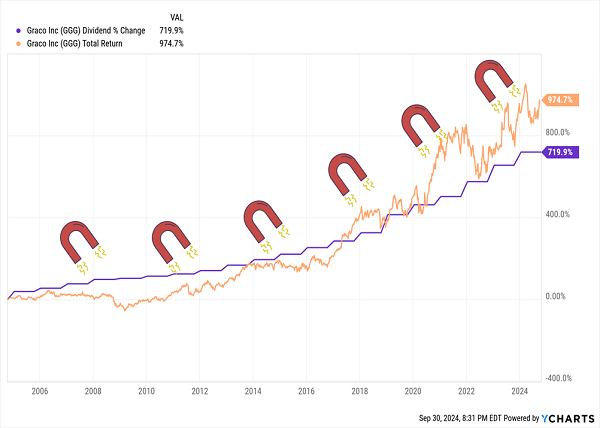

Over the past 20 years, Graco has raised its dividend by 720%. Its share price has followed this payout higher like a magnet. Including dividends, Graco has delivered a total return of 975% over this same time period:

The Dividend Magnet at Work in GGG

Graco’s current dividend of 1%+ helps the company fly under the radar. It puts income investors to sleep! They miss the fact that Graco longs who bought a decade ago are collecting a 5% yield on their cost.

Plus, they have enjoyed some plush price gains.

Where do we find the next Graco? We look at the growing dividends. Let’s be picky and sort through a pile of divvie hikers ranging from 23% all the way up to 120%.

(And oh by the way, these five companies should announce their next payout hike over the next three months. Consider yourself forewarned…)

Deere (DE)

Dividend Yield: 1.4%

2023 Increase(s): 22.5% (across multiple hikes)

Projected Q3 Dividend Announcement: Early December

Deere (DE) is one of the most recognizable brands on the planet, especially for anyone who lives anywhere outside of a bustling city.

Deere is famous for its tractors, but it’s also a global juggernaut in a wide variety of other agricultural machinery, heavy equipment, forestry machines, engines and drivetrains. In fact, it’s so big that, much like some auto manufacturers, it has its own financial services segment that finances sales and leases much of this equipment, and provides wholesale financing to equipment dealers.

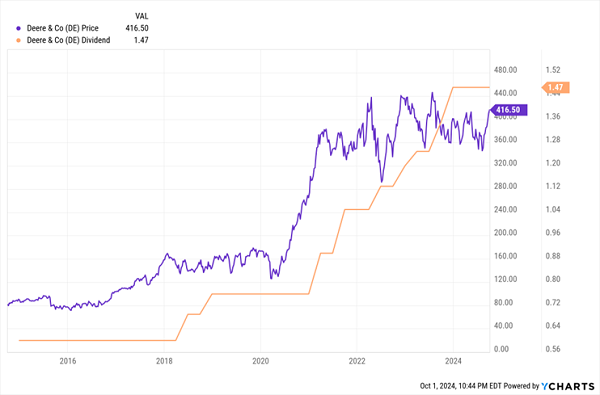

Deere is weathering a difficult 2024 in the midst of a longer-than-average replacement cycle in the agricultural industry. Revenues and earnings alike are expected to materially backtrack for the full year, and could slide some more (albeit at a slower pace) in 2025. That makes its next dividend announcement, expected in early December, all the more interesting.

Throughout the 2010s, investors suffered large periods of stagnant dividends. But Deere’s fortunes exploded for the first few years of this decade, and Deere responded by generously and even aggressively rewarding its shareholders, signing off on multiple dividend hikes each year. Last year’s December hike, to the current $1.47 per share dividend, represented a 22.5% year-over-year boost from the year-ago payout. (Spread across three raises in four quarters!)

That hasn’t been the case in 2024.

If Deere is downshifting to a schedule of annual hikes, early December would mark its next potential raise—and whether it raises (or the size of the raise if it does) could say a lot about the tractor giant’s confidence heading into 2025.

Is Deere’s Dividend About to Go Cold Again?

Equinix (EQIX)

Dividend Yield: 1.9%

2023 Increase(s): 24.9%

Projected Q3 Dividend Announcement: Late October/Early November

Equinix (EQIX) is not just a real estate investment trust (REIT), but one of the world’s largest infrastructure providers, boasting 264 data centers in 33 countries on six continents—an infrastructure supporting more than 10,000 customers and over 472,000 interconnections.

It’s also something of an outlier in the REIT space given its sub-2% yield. (For context, the FTSE Nareit All Equity REIT average yield is roughly 3.7%.) However, it’s not for lack of trying; EQIX keeps raising its payout.

It’s Just That Its Pesky Stock Price Keeps Rising, Too!

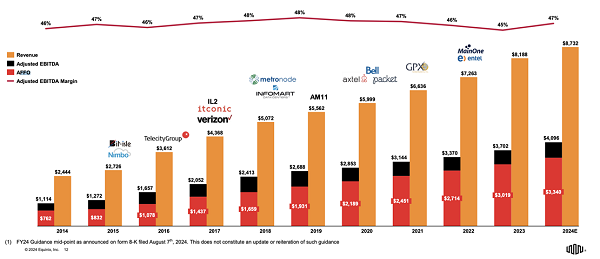

Equinix is far from a stodgy property owner. This tech-forward firm, whose properties benefit from numerous emerging trends (including artificial intelligence) has managed to raise the top line for 86 consecutive quarters, and it boasts some of the most consistent adjusted funds from operations (AFFO) growth in the space.

Source: Equinix Q2 2024 Investor Presentation

As the chart shows, though, Equinix finally stepped up its game last year. After building up a track record of high-single-digit growth, EQIX came out swinging in 2023, authorizing a fat raise of nearly 25% to its current $4.26 per share.

The question now is whether that was a one-time move, or whether Equinix is entering a new phase of aggressive dividend growth. We could get an answer sometime in late October or early November, when EQIX is expected to make its next dividend announcement.

Host Hotels & Resorts (HST)

Dividend Yield: 6.0%*

2023 Increase(s): 66.6% (across multiple hikes)

Projected Q3 Dividend Announcement: Mid-December.

Host Hotels & Resorts (HST) is another REIT, but this one specializes in hotel properties.

Host Hotels & Resorts’ portfolio currently is composed of 81 hotels representing 43,400 rooms. By revenue, Marriott (MAR) properties are the biggest slice of the pie at 62%, followed by Hyatt (H) at 20%. The rest is scattered among the Four Seasons, Hilton (HLT), Accor and others.

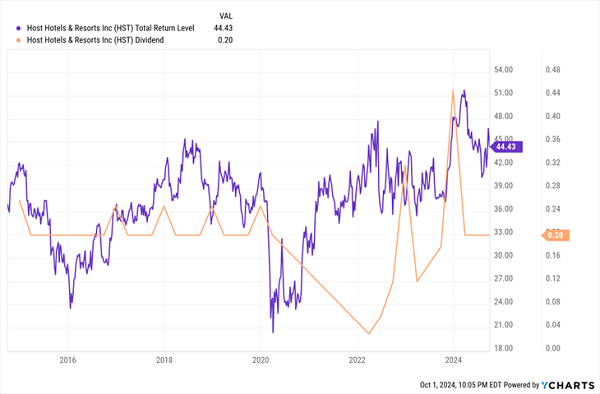

Host was one of many COVID dividend casualties—the company suspended its payout in 2020, then brought it back at a reduced level in 2022. Then it started aggressively raising the dividend every quarter or two.

In July 2023, I previewed the third quarter’s potential dividend hikes. At the time, I said:

“The REIT seems to be deliberately marching toward its old dividend total, with four increases in two years. To reach its pre-COVID dividend levels, it would need to tack on another 5 cents per share—another 33% from current levels.”

It did just that, improving its distribution from 15 cents to 18 cents, and then 20 cents (which was 66% higher than its year-ago payout), across the next two quarters.

Host’s Dividend Is Officially Back to Normal

Thing is, that’s where HST’s dividend has remained for nearly a full year. So, much like Deere, if Host is slowing down to a more orthodox annual raise schedule, we’d likely see that raise announced mid-month this December.

* By the way, those spikes in the chart above are Host’s special dividends. The company had a practice of dishing out extra one-time payments each year pre-dating COVID, and it has resumed the practice along with its regular dividend. And it can be mighty generous—all told, Host’s regular dividend translates to a 4.6% yield, and the special boosts that to 6%. Host also tends to announce that special distribution in December.

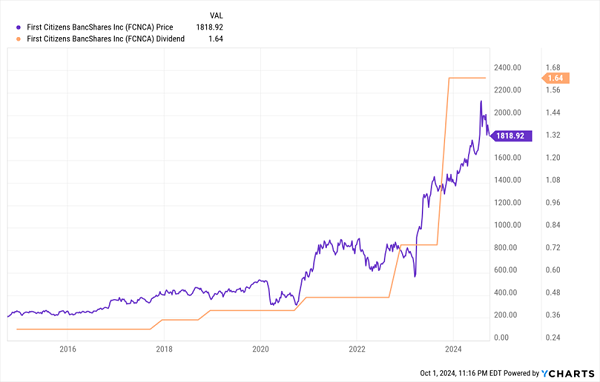

First Citizens BancShares (FCNCA)

Dividend Yield: 0.4%

2023 Increase(s): 119%

Projected Q3 Dividend Announcement: Late November

First Citizens BancShares (FCNCA) would seem like just another of the nation’s many regional banks. It predominantly operates as First Citizens Bank, which provides a variety of personal, small business, commercial and wealth products and services, ranging from free checking accounts to institutional asset management.

It’s possible you haven’t heard of First Citizens Bank.

But it’s very likely that you’ve heard of the bank First Citizens acquired in March 2023: Silicon Valley Bank.

SVB, which predominantly dealt with startups and tech firms, became the country’s third-largest bank failure after a classic bank run. In a matter of days, SVB was put under FDIC control. A few weeks after that, First Citizens purchased Silicon Valley Bank and assumed the majority (but not all) of its deposits and loans.

The collapse could be largely chalked up to a hyperconcentration in clients and, frankly, horrible timing. But SVB’s growth-minded business is a boon within the much more diversified First Citizens. The regional bank’s revenues tripled last year; net income jumped by more than 10x.

FCNCA then rewarded shareholders in late 2023 by announcing a 119% jump in the dividend, to $1.64 per share. (This, a year after a very generous 60% hike in 2022!) And it’s still splashing cash, announcing a $3.5 billion share buyback in July.

Silicon Valley Bank Ended Up Making Someone Richer: FCNCA Shareholders

That level of growth obviously will be much more difficult to come by unless First Citizens can somehow get its hands on another transformative acquisition target. The likeliest next dividend announcement date, which should come sometime in late November, could tell us exactly how optimistic FCNCA is about additional upside from here.

Korn Ferry (KFY)

Dividend Yield: 2.0%

2023 Increase(s): 120% (across multiple hikes)

Projected Q3 Dividend Announcement: Late November/Early December

Korn Ferry (KFY) is a global provider of consulting services. That includes things like org structure, culture, performance and development, executive search and talent acquisition services, as well as platforms that help companies build engagement surveys, develop sales strategies, and gather data that educates employee compensation programs.

This is a cyclical business, so KFY understandably hits the occasional growth snag, but broadly speaking, the arrow has been pointed pretty reliably northward for decades.

The dividend, on the other hand, has been nothing but chunky.

But What a Ride It Has Been!

Korn Ferry initiated a dividend program in 2015 with a 10-cent-per-share payout, then proceeded to keep that distribution level for another five years. Finally, in 2021, it got the ball rolling again—and that ball has really started to roll downhill. The dividend of 37 cents per share is now 270% higher than it was at the start of 2021. Its raise to 33 cents announced late last November represented a 120% jump from the prior year’s payout.

KFY is now raising every couple of quarters (including a 12% bump to the current 37 cents announced in June). If it keeps up with its current semiannual pace, look toward late November or early December for a possible hike.

It could be a telling hike, too. On the one hand, KFY is coming off a disappointing fiscal 2024 (Korn Ferry’s fiscal calendar ends in April) that saw both the top and bottom lines contract. But Wall Street largely expects a rebound this fiscal year and next. Another big hike could signal that the pros have the right idea, and that last year was just one of the occasional hurdles KFY has to clear.

A Simple, Safe Way to Lock In 15% Yearly Returns … For Life!

The dividend growers above aren’t exactly perfect, but they’re still excellent examples of the right strategy—a simple but potent two-step recipe for success that has proven itself to investors again, and again, and again:

- Step 1: Buy aggressive dividend growers that are actually expanding their businesses, too.

- Step 2: That’s it! There is no Step 2! Just keep targeting elite dividend growers!

If you invest your money with corporate managers who both effectively deploy capital for growth and know how to reward shareholders, you will clobber the market on a regular basis—and better still, as the years roll on, more and more of those returns will come from cold, hard cash.

You can put this income-printing strategy to work today with a simple-to-manage, easy-to-understand group of just 5 specific tickers that are quietly handing investors a steady 15%, 17%, 21% or more every year—and growing income streams!