Let’s talk about monthly dividend payers today because, well, why waste our valuable time with stocks that only pay quarterly?

I selected five for our review. We’re talking sixty dividend payments per year from this group. The most generous stock dishes an elite 8.6% annually. (The “laggard” yields a respectable 6.5%.)

Why don’t more companies pay monthly? The answer is predictable and disappointing.

Wall Street runs on a quarterly system. US-listed companies are required by the SEC to provide quarterly financial updates. So, most management teams pay their dividends quarterly as part of this process.

Hence, we salute the suits in shining armor who make the extra effort to pay us every single month. The result is a triple-play advantage for us as income investors:

- A perfect match for retirement expenses. Financial advisors will often suggest building a “dividend calendar.” They say buy certain stocks based on when they pay their quarterly dividends to ensure a more consistent stream of dividends through retirement. But this is difficult to accomplish, it can require investing in stocks we wouldn’t buy otherwise, and a dividend cut or suspension will result in even “lumpier” dividend schedules.

Source: Income Calendar

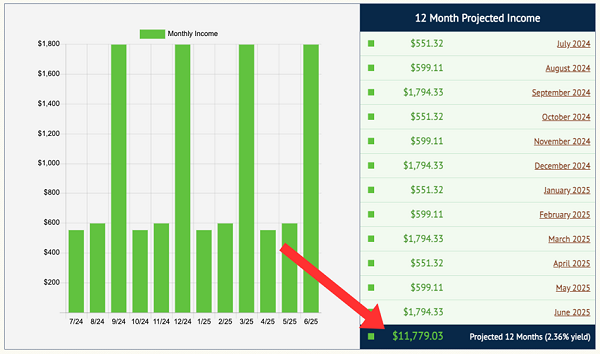

Monthly dividend stocks, on the other hand, let us build a smooth, predictable stream of income. We collect the same check every month, then use that to pay our various bills (which also come every month). Just consider the five stocks on my radar—which have an average headline yield of nearly 7%, but as I’m about to show you, some actually pay even more than that!

Source: Income Calendar

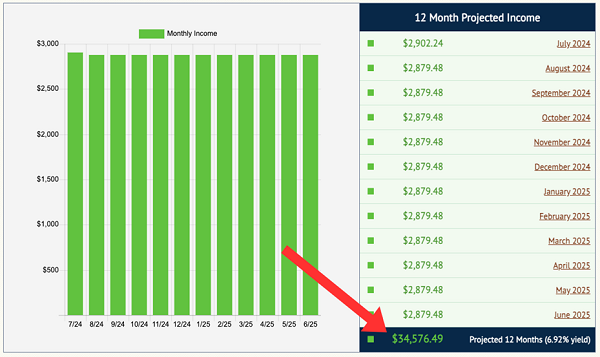

- Higher yields. Sometimes much higher yields. Monthly dividend stocks aren’t required to pay more than your typical quarterly payer—but in most cases, they do it anyway. Most monthly payers are found in high-yield categories such as real estate investment trusts (REITs), business development companies (BDCs) and closed-end funds (CEFs). As you can see in the Income Calendar above, the 5-pack of monthly payers I’ll share with you today yields a whopping 6.9%—five times better than the S&P 500! That’s crucial—with enough yield, we can retire on dividends alone.

- A compounding edge over time. On the rare occasion that financial pundits actually discuss monthly dividends, most of them forget about one other advantage: compounding. A monthly dividend stock gets cash in an investor’s hands more quickly than any other stock, which means they can put it to work sooner, which means it can compound faster. A massive edge? No. But more is always more.

Despite all these advantages, we can’t just go and buy every monthly dividend stock we come across. Even companies with high, frequent payouts can be riddled with warts. So we need to look at these 6.5%-8.6% monthly payers with a critical eye to make sure they’re dividend studs—and not dividend duds.

EPR Properties (EPR)

Dividend Yield: 7.8%

Let’s start with a nearly 8% yielder that’s also been perking up of late.

EPR Properties (EPR) is an “experiential” REIT with a portfolio of roughly 360 locations, including theaters, lodging, resorts, fitness clubs, driving ranges, ski resorts, even museums and private schools. It seemed like a potential star in the 20-teens as Americans prioritized experiences over possessions—until COVID buckled its knees. EPR shares were gutted, and the REIT briefly suspended its payout before bringing it back at roughly two-thirds its pre-COVID levels.

EPR’s performance of late can largely be chalked up to optimism that the Federal Reserve will finally begin reducing its benchmark interest rate in September; 10-year Treasury yields have been retreating for months now, and REIT shares are responding in kind.

But the reason to keep an eye on EPR in particular is that it seems poised to begin turning one of its most nagging weaknesses into a strength—or at least less of a weakness.

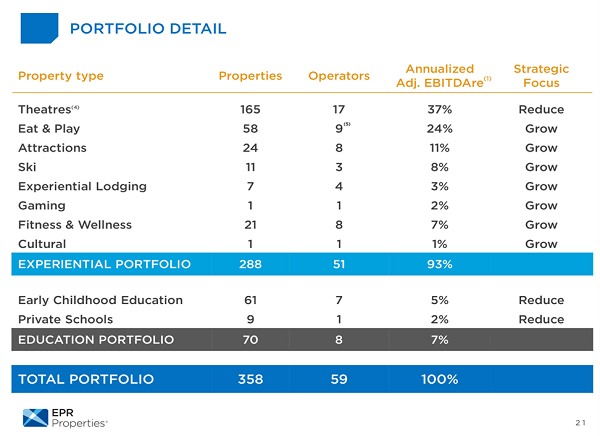

One of the biggest weights around EPR’s neck in recent years has been its theater segment, which was particularly hard-hit during COVID. EPR has been working to reduce its exposure, but with theaters still accounting for 37% of adjusted EBITDAre, it can still capture some of the rebound in theaters as Americans return to the movies.

Movies Still Dominate the EPR Portfolio

Source: EPR Properties Investor Presentation, Q1 2024

Expectations for North America’s box office are perking up: 2024’s gross is expected to come in at or slightly above $8 billion, and that number is projected to improve to nearly $9 billion next year. Also, EPR should benefit from a 7.5% rent increase on its AMC Entertainment (AMC) master lease, slated to go into effect in the third quarter of 2025.

Meanwhile, EPR hiked its monthly dividend by 3.6% earlier this year—its first raise since 2022—and shares are still trading for below 9 times “funds from operations as adjusted” (FFOAA), which is just EPR’s fancy way of saying adjusted funds from operations (AFFO).

Apple Hospitality REIT (APLE)

Dividend Yield: 6.8%*

Another high-yielding, monthly-paying REIT with some giddy-up is Apple Hospitality REIT (APLE), whose properties house 224 hotels in 87 markets across 37 states and the District of Columbia. The vast majority of those properties are split between Hilton (HLT) and Marriott (MAR) branded hotels, with a peppering of Hyatt (H) hotels.

I’ve previously said about Apple:

APLE’s focus on select-service hotels is ideal given their high margins, and it has access to not just cities but high-end suburbs, which is a nice diversifier. Its broader industry is trickier. An economic slowdown could affect hotels (and thus hotel REITs like Apple Hospitality), and high interest rates can also weigh heavily on the cost of capital.

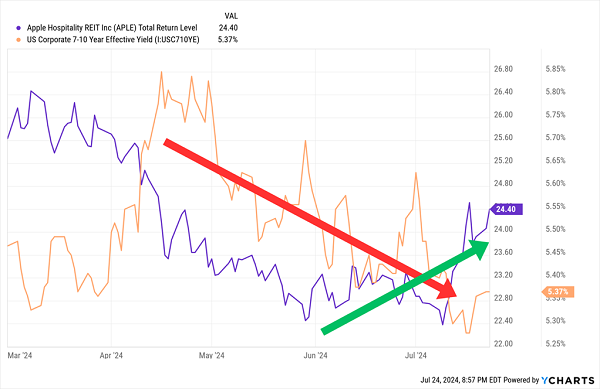

Those headwinds have largely kept APLE shares on the mat, but as rate anxiety eases, Apple Hospitality’s stock is finally climbing.

Rise and Shine, APLE Shares!

A couple other qualities?

Apple Hospitality is one of the most acquisitive names in the space, as it flips out of older hotels and into newer ones. And yet it’s not going out over its skis—net total debt to total capitalization is just 27%, and nearly 80% of its outstanding debt is effectively fixed.

Meanwhile, APLE’s dividend is extremely well-covered at just 60% of modified funds from operations (MFFO). And while that payout hasn’t budged since 2022, management is clearly keen on the idea of sharing more. The vast majority (6.5%) of Apple’s yield is from the regular dividend; the remaining basis points come from a 5-cent-per-share special dividend paid out at the start of 2024.

Permian Basin Royalty Trust (PBT)

Dividend Yield: 6.5%

Royalty trusts don’t really do much. They hold royalty interests in assets (often natural resources like energy commodities or minerals). These royalties generate income, some of which is then redistributed to investors—usually resulting in pretty high yields.

What’s interesting about Permian Basin Royalty Trust (PBT) is that, unlike some other royalty trusts, it doesn’t require a messy K-1 tax form, just a 1099. Also, unlike many other royalty trusts, there is no “end date” that will force a liquidation. Instead, PBT will only liquidate if unitholders vote to liquidate, or if PBT’s gross revenues from royalty properties fall below $2 million annually in two consecutive years.

Permian Basin Royalty Trust’s principal assets are a pair of net overriding royalty interests in Texas properties, both carved out by Southland Royalty Company. The first is a 75% interest from Southland’s fee mineral interest in Waddell Ranch properties, and the second is a 95% interest from Southland’s major producing royalty properties in Texas.

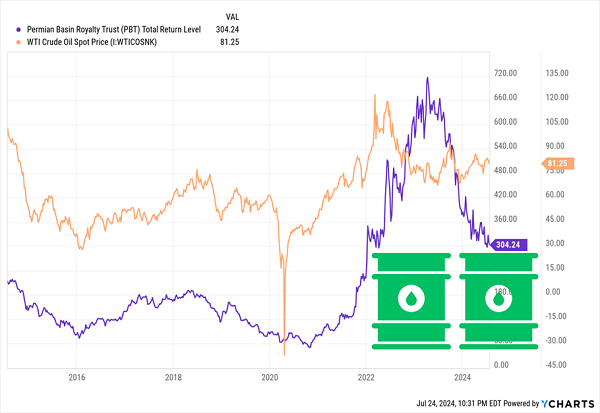

While PBT is technically an oil-and-gas trust, roughly 85% of its revenues come from oil—thus, oil prices are what matters. Like with traditional energy E&P stocks, Permian Basin Royalty Trust roared as demand bounced from the COVID bottom and as Russia’s war with Ukraine sent oil prices ever higher. Prices have moderated since then, sending PBT shares to the ground.

The question is: What’s next?

Is PBT Finally Finding Support?

The answer lies in a host of macro factors, including Chinese economic strength, Middle East conflict and U.S. inventories—the same factors we’d watch for most oil-price-dependent energy stocks.

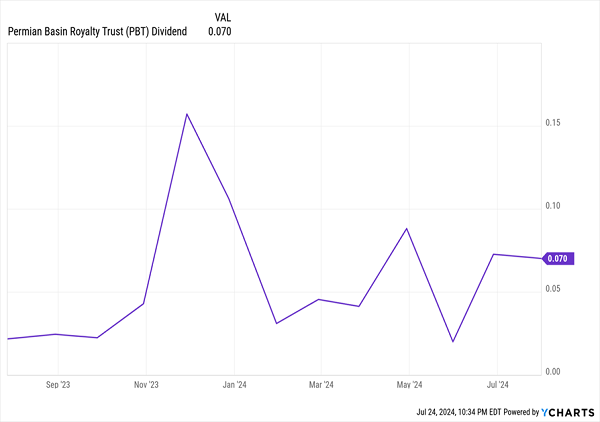

I think the chart income investors should be more interested in is the one tracking Permian Basin Royalty Trust’s dividend:

PBT Plays Payout Pinball

Let’s look for more consistent dividends instead.

Gladstone Investment Corporation (GAIN)

Dividend Yield: 8.6%*

It’s hard to beat the yields offered up by business development companies (BDCs). But I’ll be blunt: It’s a difficult industry, and there are a lot of losers, so we really need to watch our step.

One BDC I’ve been keeping my eye on is Gladstone Investment Corporation (GAIN), which is part of the Gladstone family of businesses that also includes Gladstone Commercial (GOOD), Gladstone Capital Corporation (GLAD) and Gladstone Land Corporation (LAND).

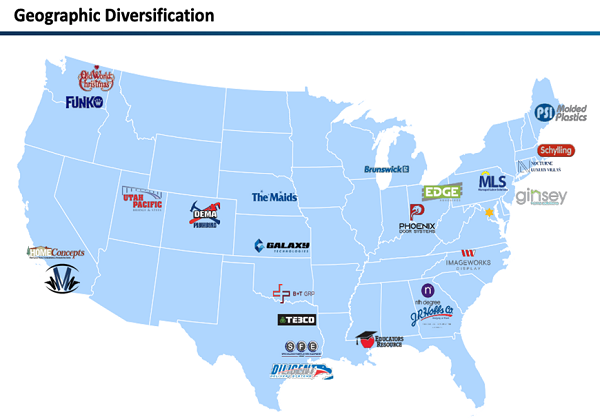

Remember: BDCs provide capital to small and midsize businesses that often go ignored by banks. GAIN prefers debt investments, though it will also deal in equity. Its target portfolio company will generate $4 million to $15 million in annual EBITDA, have a proven business model, stable cash flows, and minimal market or technology risk. Geographically speaking, you can find Gladstone Investment portfolio companies all over the map:

Source: Gladstone Investment Investor Presentation, Q4 Fiscal 2024

GAIN boasts a strong track record of net asset value (NAV) growth, including a 12% year-over-year jump in its fiscal year ended March 2024, and NAV growth in three of the past four years.

Happily, Gladstone’s regular dividend is much more consistent than PBT’s. But because it pays supplemental dividends, too, it’s still a moving target—for better or worse.

GAIN pushes nearly every penny of its net investment income (NII) into its regular dividend, which has been fixed at 8 cents monthly since 2022—good for a 6.9% yield at current prices. And whenever it’s able, it pays out supplemental distributions. Those special payouts can be downright spectacular, with GAIN delivering a total yield of nearly 17% the last time I reviewed the stock. But you’ll notice the yield is down to 8.6%. That’s because Gladstone Investment hasn’t paid a supplemental dividend since 2023.

I wouldn’t expect that to last forever—GAIN frequently uses realized gains from company exits to fund its supplementals, and last quarter alone, Gladstone reported nearly 88 cents per share of net unrealized appreciation.

Just understand what you can count on when budgeting your monthly income, and what might be considered “extra.”

One last note: GAIN has outperformed the BDC industry by a few points since the COVID lows. It’s a well-run BDC, but it also trades like one. It’s currently priced at 103% of NAV, so shares aren’t exactly cheap.

Main Street Capital (MAIN)

Dividend Yield: 8.2%*

GAIN might demand a little premium for quality, but Main Street Capital (MAIN) demands a king’s ransom.

The question we have to answer is: Is it worth the cost to lock down one of the BDC industry’s rare blue chips?

Main Street Capital provides debt and equity capital solutions to lower-middle-market companies, and debt financing (primarily floating-rate first lien senior secured debt) to middle-market firms. A typical holding will generate annual sales of $10 million to $150 million, as well as annual EBITDA of roughly $3 million to $20 million.

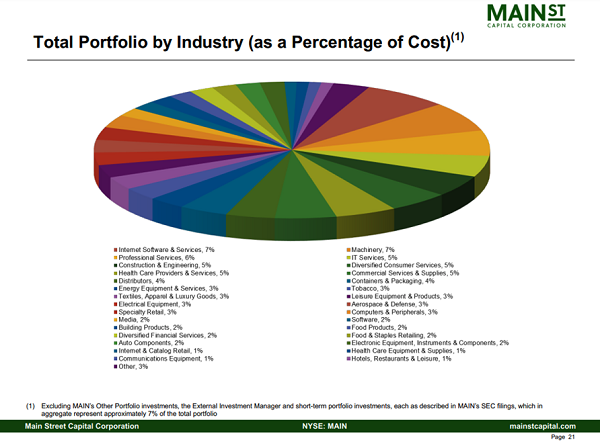

Currently, its portfolio is made up of 191 companies, with the largest one representing less than 4% of total investment income.

Source: Main Street Capital Q1 2024 Presentation

It’s difficult to express just how excellent its fundamentals typically are. Its most recent results include 8% year-over-year NAV growth, a return on equity of more than 17%, Street-beating NII, and “net distributable investment income” (a MAIN-created metric) that topped its own guidance. Balance sheet leverage crept higher quarter-over-quarter but is still better than most of its peers.

Main Street’s typically stellar results feed a generous dividend program that includes regular monthly payouts and supplementals. Its regular dividends come out to a respectable yield of 5.9%. Add up its special dividends from across the past 12 months, and you get another 2.3% worth of yield for a tasty 8.2%.

I’m sure we’re all shocked to find this all translates to best-in-class returns.

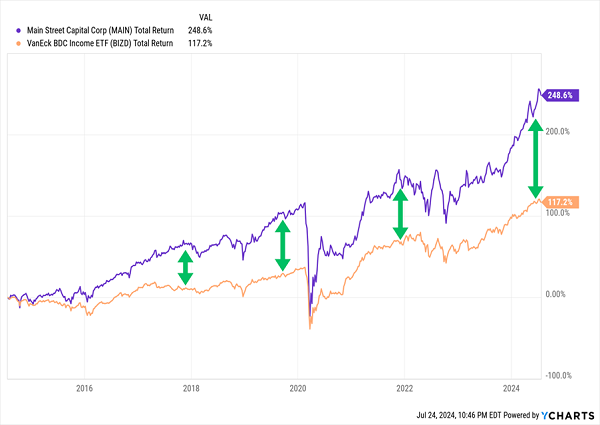

Main Street Keeps Putting More Room Between It and the Competition

So, what could we expect to pay for this kind of dominance? A 5% premium? A 10% premium?

Don’t I wish.

Late last year, MAIN shares traded at a 45% premium to NAV. Back in April, I noted that shares had expanded to a 63% premium. And as I write this, that valuation has plumped even further—to a wild 70% premium to NAV.

Earn a Reliable 8%+ in Retirement—Paid MONTHLY

Main Street has unquestionably walked the walk. I wouldn’t bet against it. But buying a stock that’s trading for 70% more than it’s worth is a gamble not many of us are willing to make as we build our retirement portfolios.

I will say this, though: While MAIN’s price isn’t right, its yield sure is.

In fact, that’s exactly the level of income production I demand (and get!) from the beautifully boring, high-yielding, and much more reasonably priced blue chips I hold in my “8%+ Monthly Payer Portfolio.”

But where this portfolio differs from other high-income strategies is that it’s not just about high income.

These holdings are “steady Eddie” stocks that don’t make us slap the panic button in bear markets.

They also boast meaningful price upside, which means we can keep growing our nest eggs well after we’ve quit our jobs.

Put simply: This is how we win in retirement.

Many retirement plans build your nest egg, only to turn around and ask you to bleed that same nest egg dry as you age.

But the income this portfolio can generate is so rich, it can sustain a retirement on dividends alone.

If you have a million dollars to work with, that 8% baseline will net you $80,000 a year. But even if you’re well behind on your retirement savings—say you only have $500,000 to work with—you could still generate a roughly $40,000 annual income stream.

That’s $3,330 every month in regular income checks!

Can your current portfolio deliver that level of income? If not, it’s time to make a change. Click here to learn everything you need about these generous monthly dividend payers right now!