Let’s talk about convertibles for a second—but not the car with a removable top that everyone thinks of when they hear that word: I’m talking about convertible bonds.

I know, a bit less flashy, right? The name causes most folks’ eyes to glaze over, but there is a (very) exciting part to this convertible-bond story: massive dividend yields. And I’m not talking the type of so-called “high” yields you get on regular stocks (3% or 4%). Or even corporate bonds, many of which pay out in the 6% to 7% range these days.

I’m talking really high yields here. Like 12% yields.

I think you’ll agree that the idea of getting $100 per month for every $10,000 invested is far from dull! In my opinion, the potential for financial freedom such an income stream offers far outweighs the joys of a convertible car (which isn’t all that fun, to be honest: I’ve owned two in my lifetime and didn’t really enjoy either).

So what is a convertible bond, exactly? Simply put, these are debts issued by companies that, in the right circumstances, let the creditor convert (hence the name) that debt into equity. In other words, we can lend money to a company and, if the company does well, we can decide to change our debt into shares.

The benefits of this are often underestimated. You can manage the risk of losing money by lending money to a firm and then, when the risks seem smaller and the opportunity bigger, take a bigger position by owning stock outright, thanks to the convertible bond’s rules.

Big companies regularly use convertible bonds to raise money when they’re particularly confident they can grow their business beyond the credit market’s expectation. This often happens when companies are about to expand or overtake a competitor in some way, but they can’t prove it to the bank quite yet.

Companies are getting more into convertible bonds these days, so there are a lot more of them available, with issuances up sharply from 2022.

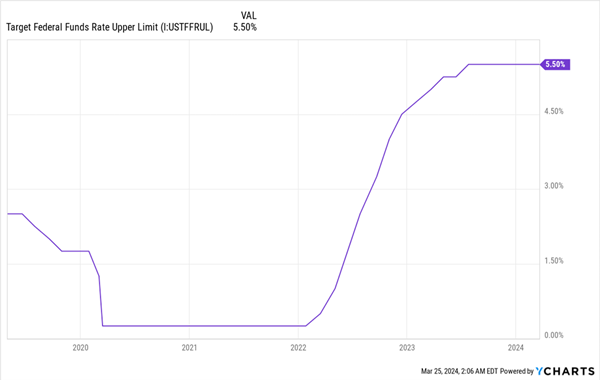

One of the reasons behind this increase points to a mispriced opportunity. Of course, no one needs reminding that interest rates have soared. As a result, companies are looking for alternatives to the high rates the bond market demands. Enter convertibles.

Higher Rates Make Convertibles Appealing

By offering the ability to convert a bond into stock, companies can get a discount on the interest they pay. That’s caused established, highly rated firms to consider convertibles instead of the regular corporate bonds they likely issued in the low-rate 2010s. PG&E Corp. (PCG) and Uber Technologies (UBER) are two large firms that have switched to convertibles in recent months, according to the Financial Times, and both are saving money by doing so.

The best way to play this opportunity is through high-yielding closed-end funds (CEFs) that focus on convertible bonds. The equity upside and relative stability of convertible-bond prices help sustain these funds’ outsized dividends, and the sheer number of new issuances gives CEFs’ human managers (key when it comes to picking the right convertibles) plenty of options when adding to their funds’ portfolios.

3 Convertible-Bond CEFs to Consider (in Order of Risk—and Yield)

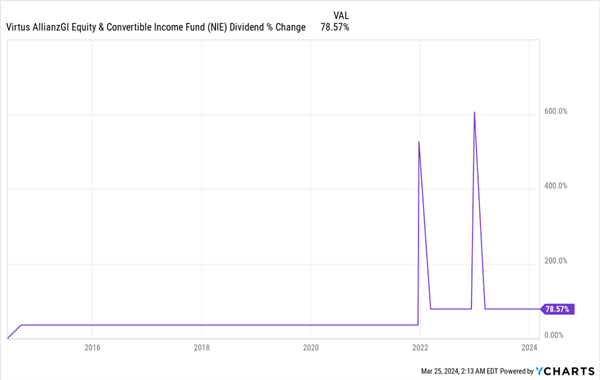

Let’s start with the Virtus Equity & Convertible Income Fund (NIE), which yields 9% and trades at a whopping 11% discount to net asset value (NAV, or the value of the convertible bonds it holds). It’s been (wrongly) handed that deep discount even though it’s not only never cut its generous payouts since the Great Recession, but it has recently aggressively grown its regular quarterly payout and delivered two huge special dividends in recent years.

NIE’s Reliable Income Stream

More on NIE in a sec, first let’s jump ahead a bit, to our second option.

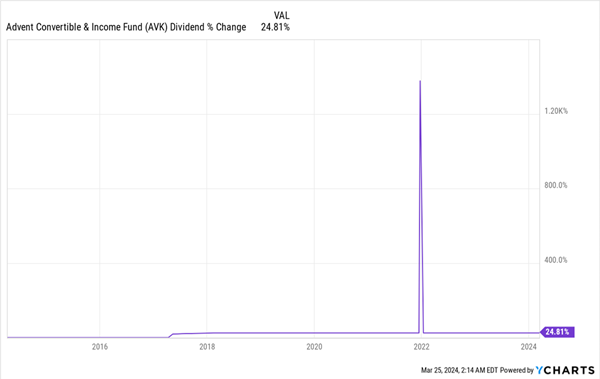

If you want a bit more income but don’t want much more risk of a dividend cut, the Advent Convertible and Income Fund (AVK) is a strong pick. With an 11.8% yield and a 5% discount, AVK is underpriced, given its focus on convertibles and the fact that it’s also raised its regular dividend in the last decade (though not by quite as much as NIE).

AVK Combines a High Yield and Dividend Growth

Let’s pause here for a moment and consider what an 11.8% yield really means. An income stream like that means you can retire with a six-figure income—that’s $100,000 per year in payouts—with less than $900,000 invested. And that income stream is solid, as you can see from the chart above. This is a rarity ( to say the least) in the investment world.

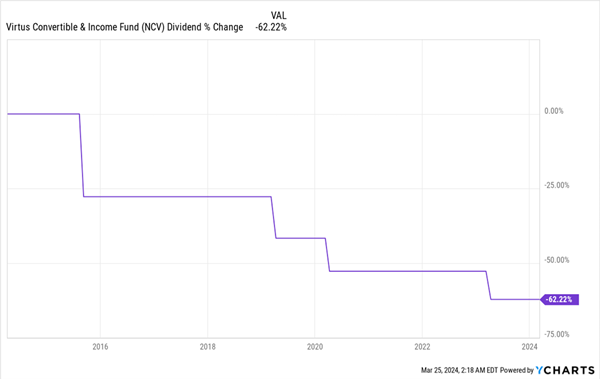

And there are even bigger yields to consider, like the 12.4% payout on our final CEF, the Virtus Convertible & Income Fund (NCV). That kind of yield makes a six-figure income attainable with just about $807,000 invested. Again, this is an incredible income stream, made even more incredible by the fact that NCV is currently discounted by 12.4%.

But there are risks.

NCV’s Dividend Stair-Steps the Wrong Way

As you can see, NCV has aggressively cut payouts in the last decade. In defense of the fund’s managers, however, NCV also invested heavily in corporate bonds when interest rates were very low and was overpaying investors in the early 2010s, requiring many cuts later in that decade to adjust. Now that rates are higher, the cut in 2023 may be NCV’s last in a while.

But the word “may” is critical here. There is a very high risk of seeing your income stream shrink with this fund. But that’s not the only risk.

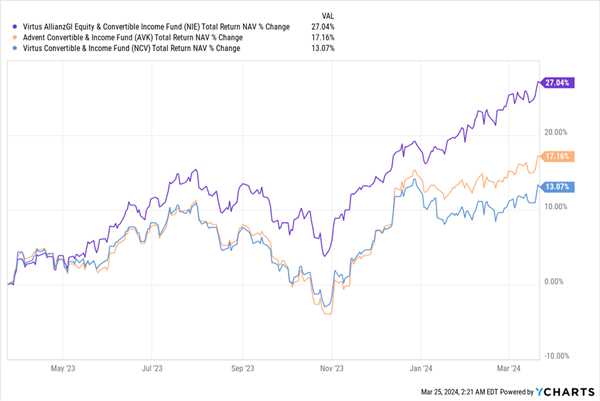

NCV Trails Our Other 2 Funds in the Short Run …

Above we can see the total-NAV-returns (or the gains and dividends on their underlying portfolios) of our three convertible-bond funds. Total NAV return is a good barometer of the quality of a CEF’s management.

As you can see, NIE (in purple above) is taking full advantage of the opportunities of the post-2022 market, NCV (in blue) is playing catch up, and AVK (in orange) is in the middle of the pack. So NIE has clearly been the better option.

Thanks to its focus on combining convertible bonds with equity (which separates it from AVK and NCV, which combine convertibles with corporate bonds), NIE has been able to play the gains in the convertible and stock markets. That’s worked well for its portfolio so far, and may continue to for a while, more than compensating investors for its lower yield, as it’s done for a long time.

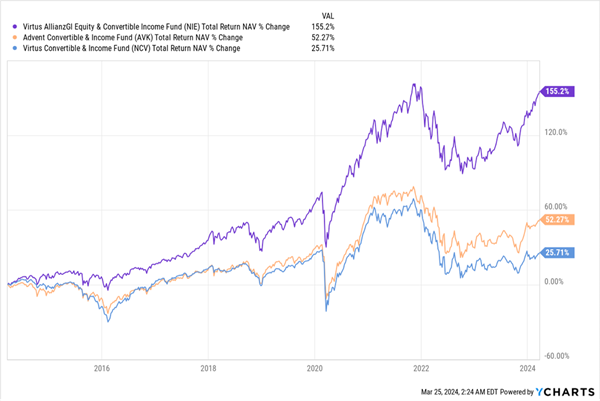

… And the Long Run, Too

Will NIE’s portfolio continue on this trajectory? For the short term, the answer seems quite clearly yes, but over the long term, it depends on whether (and more likely when) the Fed cuts interest rates or not in 2024—and how the bond market responds.

The “Rate-Proof” CEF Portfolio: 4 Funds Paying $10,200 in Dividends Per $100K Invested

The state of interest rates is something I watch closely—and always account for when recommending CEFs to investors.

And the likelihood is that rates are set to fall, though maybe not as far in 2024 as most folks think. Which is why I’ve pulled together 4 CEFs that stand to gain no matter what rates do in the next few months.

If rates remain elevated, these 4 income plays have more time to snap up the stocks, bonds and real estate investment trusts (REITs) they specialize in at bargain prices.

If rates fall sharply, those assets will take off, as they all tend to trade inversely to interest rates.

The kicker? Either way, by buying now, we’re locking in a combined 10.2% yield for ourselves. That’s $10,200 in dividends a year on every $100K invested!