Right now, there’s $6.5 trillion in cash sitting on the sidelines—and a big slice of it is about to drop straight into a select group of dividend stocks.

We’re going to “front run” that cash wave today—and set ourselves up for income (I’m talking 6%+ yields here) and gains as this cash wave starts to build.

In a sec, I’ll name two dividend-payers sitting right in the path of this freed-up cash. One is a true “dividend unicorn,” shelling out an outsized 6% payout that grows. The other has doubled its dividend in just the last five years.

Our $6.5-Trillion Dividend Plan

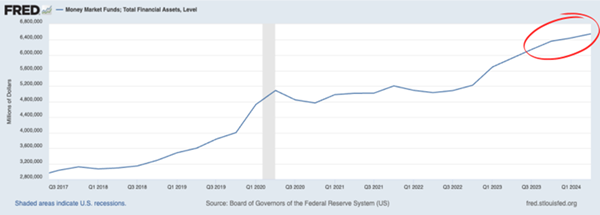

Let’s start by breaking down that $6.5 trillion figure: It’s the amount of cash in parked money-market funds today.

Here’s why a big chunk of it is likely to shake loose: Rates on money-market funds float, and the Fed Funds rate—which Jay Powell, of course, just started slashing—has a strong pull on them.

As yields on money-market funds (and savings accounts and the like) fall, more “new money” will bypass them and go into dividend stocks instead. Meantime, today’s money-market investors will “stretch” for higher yields and payout growth. Here again, dividend stocks will be the beneficiaries.

It’s already happening:

Above you can see the rapid growth in money-market holdings since the Fed started raising rates in early 2022. Since the second quarter of that year—or about two years ago—the total has jumped a staggering 30%, to just over $6.5 trillion.

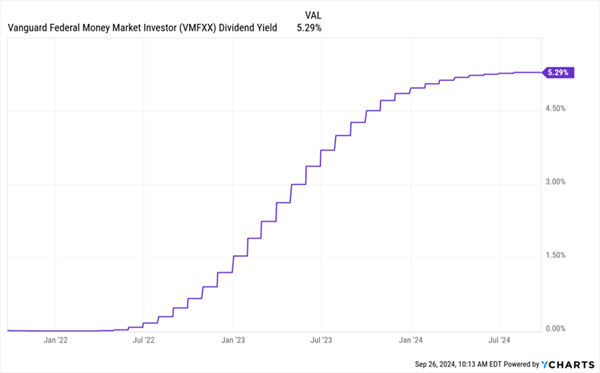

You can also see (at the top right), that the inflow has slowed. It’s no coincidence that’s happened as yields on money-market funds like the popular Vanguard Federal Money Market Investor Fund (VMFXX) flatline:

Money-Market Yields Hit a Wall

You can see the fund’s yield stair-step higher as the Fed hiked rates to 5.25% to 5.5%, then go flat as the Fed held rates from mid-2023 till this month’s 50-point cut.

Here’s What I See Happening Next

Let me be clear: I’m not saying the entire $6.5 trillion is going to go into stocks.

Plenty of folks will always be drawn by the promise of a guaranteed principal. But even if money-market holdings simply drop back to where they were two years ago, we’re talking about $1.5-trillion making a move here.

And that doesn’t include new money that bypasses these lower-paying money-market funds. Or any freed-up cash in savings accounts and CDs as they mature.

In fact, this transition is already happening, and in a surprising place, too: riskier high-yield, or “junk,” bonds.

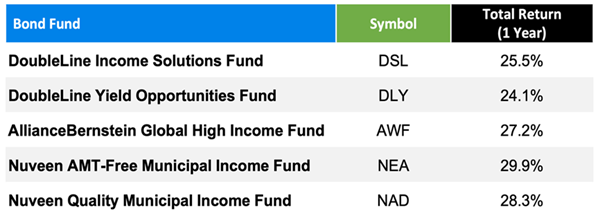

Check out these big gains from the corporate-bond closed-end funds (CEFs) we held in my Contrarian Income Report service from November 2023 to now:

These are big moves for bond funds, especially for our two municipal-bond funds, NEA and NAD. These gains happened in lockstep with the slowing flow into money-market funds, and this trade is still working in our favor—though after these funds’ strong runs, I do rate them as “holds” today.

While we wait, though, let’s dive into those two dividend payers I mentioned earlier.

Pick No. 1: A Payment Processor Primed for a “No-Landing” Economy

Our first stock, payment processor Mastercard (MA) is in the pole position not only as more cash moves into stocks but from another shift few people are talking about.

I’m talking about the rising odds we’ll not get a soft or hard landing in the economy—but no landing at all. In that setup, the economy ticks along and inflation comes back.

Not great, I know, and we discussed it in detail last Tuesday. The upshot is that government spending is out of control, outrunning tax receipts by almost $2 trillion.

Give me an extra $2 trillion and I’ll show you a strong economy! But the resulting monetary inflation could flow back into consumer price inflation—and overwhelm Jay Powell.

This is one reason why those bond funds I mentioned earlier are holds for now. As I said, the trade is still going our way, but we’re watching it closely, as any move toward higher rates would hurt bond prices (as rates and bond prices move inversely).

But the other part of this story—a humming economy—is great for Mastercard (MA), which takes a slice of each payment that rolls down its network.

And talk about pricing power: The credit-card market is basically controlled by four companies: Visa (V), with a 53% share, Mastercard (MA), at 24%, American Express (AXP), at 20% and Discover Financial Services (DFS).

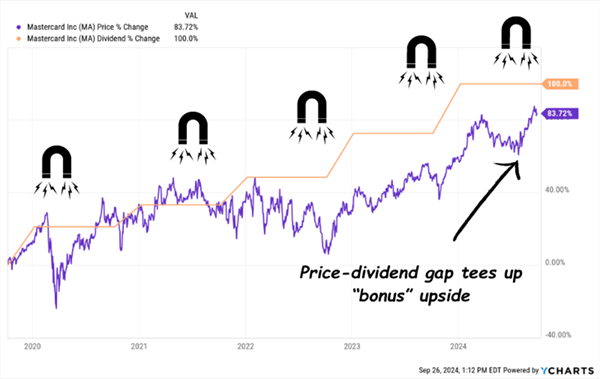

Mastercard doesn’t win many income fans with its tiny 0.5% yield, but payout growth is the story here: This dividend has doubled in the last five years, pulling up the share price with it:

Mastercard’s “Swipe-Powered” Payout

If you’ve followed me for a while, you know I talk a lot about the “Dividend Magnet”—a stock’s tendency to track its payout higher.

You can see it in action here. The current gap between the two is a snapshot of the stock’s upside as it “snaps back” to the payout. The low payout ratio (Mastercard pays just 21% of free cash flow as dividends) virtually locks in further growth, even if I’m wrong and the economy does slow from here.

Pick No. 2: A “High Roller” Dropping Payouts Money-Market Funds Can’t

Mastercard is a great stock, but let’s be honest, it’ll take years for its payout growth to inflate the yield on a buy made today. That’s where casino landlord Gaming and Leisure Properties (GLPI) comes in.

Before you say it, yes, I know a casino stock might sound like an odd pick to attract money-market-fund investors. But I’m pretty sure a growing 6% dividend won’t take long to convince them! And hey, if folks really are migrating to junk bonds from money-market funds, why not a stock like GLPI?

Plus, the stock has lots of strengths that make it far from a gamble (sorry, couldn’t resist).

For one, it’s diversified across the country, with 65 casinos in 20 states. That’s key, because if the job market continues to slow, concerned workers might cancel their Vegas trip, but they’ll likely still hit up their local casino.

Second GLPI’s tenants are signed under “triple-net” leases that provide a stable, predictable income stream.

Moreover, under these leases, the tenant pays the full cost of running and maintaining the company’s properties. Which is great news—can you imagine what this electricity bill looks like?

But the real standout for us income-seekers is that as a real estate investment trust (REIT), GLPI is exempt from corporate taxes so long as it pays out 90% of its profits as dividends. The savings help fund that high payout.

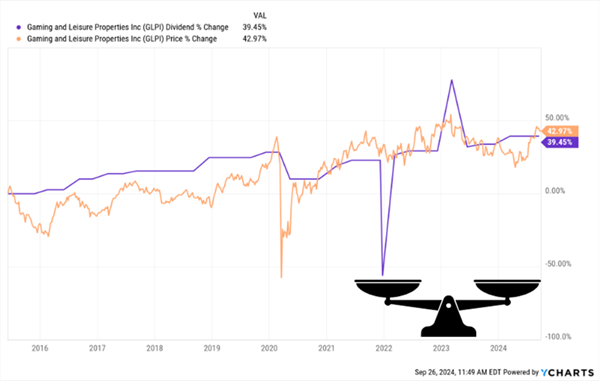

And as mentioned, GLPI has been quick to share its rising cash flow through payout growth—including special dividends (the spikes and dips in the chart below):

A Gamble? Nah. GLPI’s “Payout-Powered” Stock Is Anything But

The REIT’s regular dividend was cut in the 2020 lockdowns, but that’s understandable and the cut was modest: just 14%.

And GLPI quickly got back to its winning ways, boosting the payout since. And as with Mastercard, we’ve got a powerful Dividend Magnet working for us here, too.

More payout hikes are likely. GLPI’s revenue rose 6.7% in the latest quarter, and adjusted funds from operations (AFFO, the key REIT profitability metric) rose 5.6%. The company also pays an estimated 81% of the midpoint of its forecast 2024 AFFO as dividends, a reasonable amount for a REIT.

5 Dividends You Must Buy Now (Before Those “Parked” Trillions Start to Move)

Mastercard and GLPI clearly show the power of the Dividend Magnet. As mentioned, they’re primed to profit as more of that $6.5 trillion in “parked” cash goes looking for higher dividends (and growth).

GLPI is one of the 5 stocks I’m urging investors to buy to take full advantage of this trend. (Mastercard is a great pick, too, but as mentioned, we prefer stocks with slightly higher yields.)

And GLPI isn’t our only option here. I’ve got 4 more “Dividend Magnet” winners I’m telling anyone who will listen to buy now—before the next rate cut drops, prompting more of that $6.5 trillion to start its profitable shift.

Click here and I’ll tell you more about the Dividend Magnet—including how we’ve ridden it to big profits. I’ll also give you a free Special Report revealing all 5 of the Dividend Magnet payout growers (including more on GLPI) I see as URGENT buys to reap maximum returns as more investors hunt for higher payouts (and growth).

As we said, this shift is already starting to happen, and I want to make sure you get a chance to front-run it before it’s too late. Don’t miss out.