Will the stock market finish the year higher or lower?

Who cares?!

Paying attention to “the market” is a hopeless effort in 2025. The explosion of AI implementation plus the policies from Trump 2.0 are creating winners and losers in the economy.

So why buy a basket when we can cherry pick the undervalued front runners?

Even better? Some are cheap! As I write, four big dividend payers (dishing divvies between 5% and 6%) are trading at bargain-basement valuations. Let’s start with the most established of the four-pack, trading for less than its annual sales…

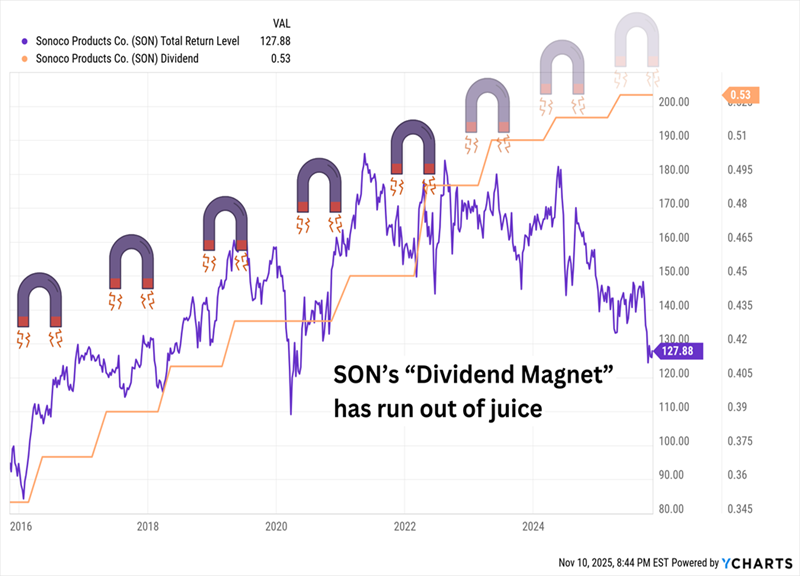

Sonoco Products (SON)

Dividend Yield: 5.2%

Sonoco Products (SON) is a packaging dinosaur turned value play. This 126-year-old firm is cheap at 6.5-times earnings, has a 42-year raise streak rolling and is still unloved after a messy Eviosys deal ruffled Wall Street’s feathers.

The business itself is beautifully boring. Sonoco is a global packaging company that produces both consumer packaging (rigid paper products, steel containers, plastic containers and the like) and industrial packaging (paperboard tubes, protective packaging, recycled paperboards). It also deals in displays and packaging supply-chain services. And thanks to last year’s acquisition of Eviosys, it’s now the world’s largest metal food can and aerosol packaging manufacturer.

Sonoco yields 5% right now, and the stock is cheap by just about any measure we could want, including forward price-to-earnings (P/E, 6.5), price-to-sales (P/S, 0.7), price-to-cash-flow (P/CF, 7.0) and price/earnings-to-growth (PEG, 0.7) thanks to a sharp pullback:

Sonoco’s Dividend Magnet is Due

Sonoco’s shares have taken several hits over the past couple years, including initial skepticism over the Eviosys deal and high costs and slack demand—the latter two of which contributed to a recent quarterly miss and lowered full-year guidance. Tariffs have also hampered the company more than many expected.

Still, expectations for both the top and bottom lines are pointed in the right direction, and Sonoco boasts a streak of 42 consecutive increases to its dividend (on an annual basis).

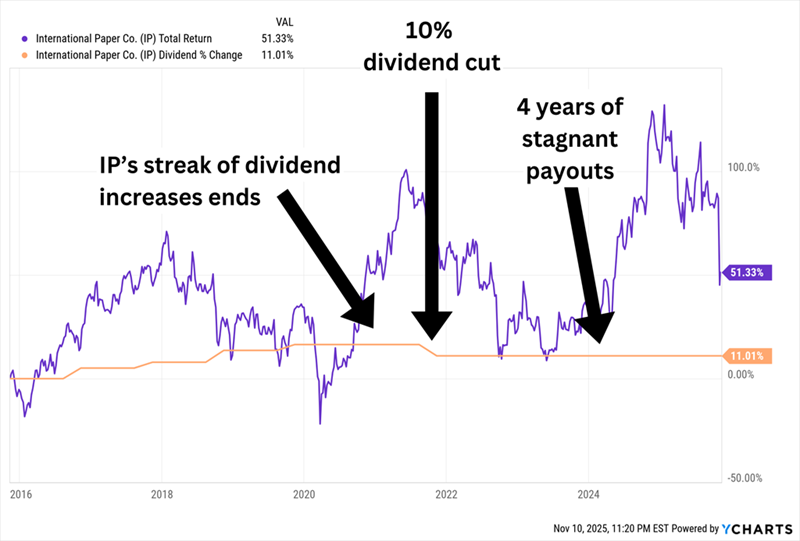

International Paper (IP)

Dividend Yield: 4.9%

Another paper giant trading at pulp-level prices, International Paper (IP) fetches just six-times cash flow, pays a 5% yield and is hated enough to be a contrarian setup. IP produces and sells linerboard, whitetop, and saturating kraft paper, among other packaging products. It’s also a major player in pulp, which is used in a variety of personal-care products, construction materials, paints and more.

IP has suffered similar issues to Sonoco—namely, higher input costs, softer demand, and tariffs. Continued economic uncertainty also doesn’t bode well for the company’s near-term prospects.

Those headwinds forced International Paper to lower guidance for 2025 and 2026; “Macro conditions in North America and EMEA [Europe, Middle East and Africa] continue to be challenging,” CEO Andy Silvernail said in the post-earnings call.

A big dip has IP trading at just 6 times cash flows and a PEG of 0.26, not to mention it has raised its payout to nearly 5%. But that’s the only thing bringing up its yield.

International Paper’s Dividend Has Been Flat for Years

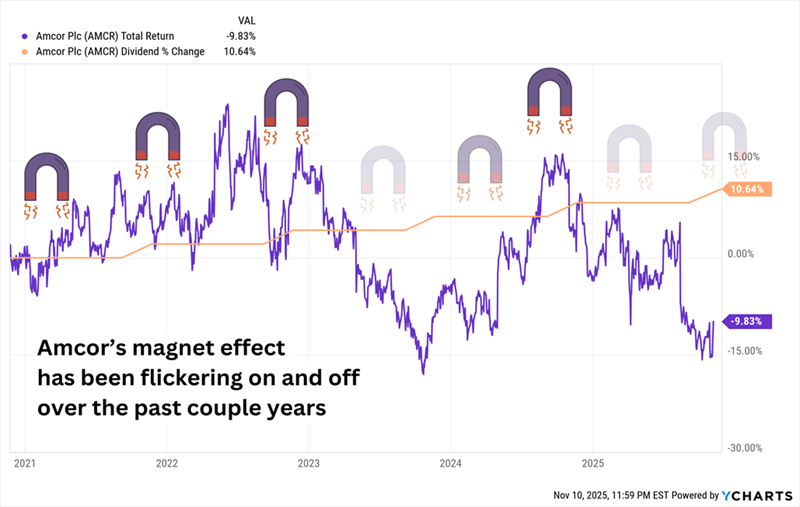

Amcor (AMCR)

Dividend Yield: 6.2%

Amcor (AMCR) is a 41-year dividend grower hiding in plain sight. Its own merger hangover has the stock cheap while its payout has climbed past 6%.

Amcor makes a number of food-related packaging products, including high-barrier paperboard trays for beef and meats, glass dressing bottles, overwrap for home and personal care. Its products are also used in garden and outdoor products, agriculture, pet care, healthcare, even building and construction.

It’s a Dividend Aristocrat with 41 years of dividend growth under its belt. It’s a low-volatility stock, too, with a beta of 0.7 (a beta of less than 1 is considered less volatile than a benchmark; in this case, the S&P 500). And its value metrics are decent to downright attractive, including a P/CF of about 6, forward P/E under 11, and a PEG just slightly below 1. And it now trades at a yield north of 6%.

Every one of those metrics is better than when we checked in over the summer.

Amcor has delivered a pair of reports since then, including a lousy final quarter of its fiscal 2025 that showed the company is leaning heavily on synergies from its merger with Berry Corp. to help offset weakness in its legacy divisions, and a lackluster Q1 for its fiscal 2026 in which it met earnings estimates but continued to struggle with weak volumes.

And unlike many other Aristocrats, its stock price has become somewhat untethered from its dividend growth.

Consistent Dividend Growth, But Inconsistent Stock Movement

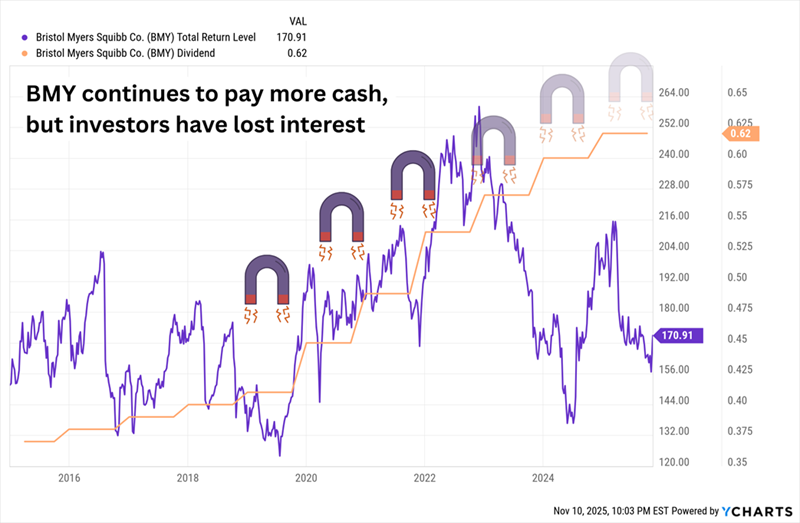

Bristol-Myers Squibb (BMY)

Dividend Yield: 5.2%

Bristol-Myers Squibb (BMY, 5.2% yield) is big pharma with a small multiple! It trades under eight-times earnings and pays 5.2% while Wall Street frets over patent cliffs. BMY however boasts a deep stable of more than 30 products that includes cancer treatments Revlimid and Opdivo, and the anticoagulant Eliquis.

Recently we discussed BMY as one of a few health care stocks that still had a pulse amid a weak year for the sector. The company has since reported an upbeat quarter on the back of strong results for Reblozyl (for anemia due to lower-risk myelodysplastic syndromes) and Camzyos (for symptomatic obstructive hypertrophic cardiomyopathy).

Bristol-Myers’ Dividend Magnet Has Powered Down, Too

Partnerships with BioNTech (BNTX) and Bain Capital (BCSF), plus potential blockbuster Opdivo Qvantiq can help soften the blow when Opdivo’s key patent expires in 2028. BMY “pipeline believers” can receive a 5.2% divvie while they wait for this cheap (P/E 8) stock to roll out new pills.

How About a Growing Dividend That Already Pays 11% Instead?

One of the best opportunities among dividend growers right now isn’t a stock—it’s a fund that checks off more boxes than just about any other investment right now:

- It pays 11%

- Its dividend is growing

- It pays us each and every month

- It occasionally pays us special dividends, sweetening the yield pot even more

- It’s diversified

- And it’s cheap

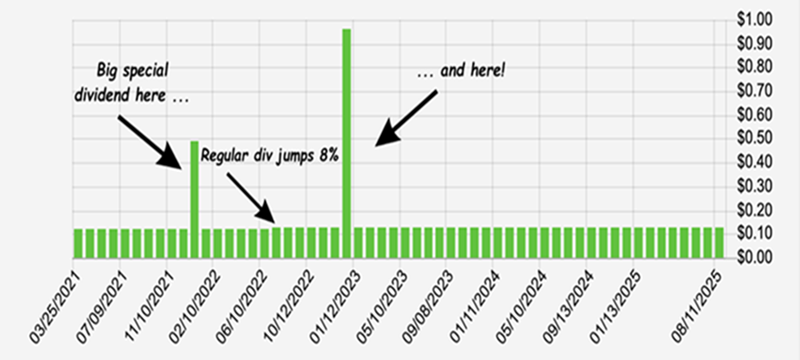

One of the Biggest Monthly Dividends I’ve Ever Seen—and It’s Growing

This one is, hands-down, my top buy, and the time to buy this one is now.

Don’t miss out. Click here to learn more about this life-changing 11% dividend and download a free Special Report revealing its name and ticker.