Today I have a sweet dividend “double shot” for you: The first? A 2.8% payout set to grow thanks to AI—and take the stock price up with it.

The second gives you high payouts now, in the form of a monthly-paid 7.8% divvie that also looks set to head higher.

Both of these tickers are cheap. In fact, they (and the sector they’re in) could very well be the last bargains on the board as the bull runs into its fourth (!) year.

Pharma Goes From “Dead Money” to the Next AI Winner

These two dividend plays are on sale because they’re often lumped in with drug stocks—a sector that’s lagged for years.

There have been exceptions, like Eli Lilly & Co. (LLY), whose Mounjaro and Zepbound GLP-1 weight loss drugs have helped the stock overtake that of Novo Nordisk (NVO) maker of Ozempic and Wegovy. Beyond that, breakthroughs have been thin on the ground. That’s why pharma has been “dead money” for years now.

Well, that and politics.

Remember, Trump 1.0 kicked off the insulin caps. Biden’s Inflation Reduction Act followed with price limits on 10 blockbusters starting in 2026—a potential $160-billion profit hit. Then Trump returned and aimed to tie US drug prices to the lowest in the world.

But on cue, pharma did what it always does: It lobbied. The lobbyists not only slowed the political avalanche—they pushed it back up the mountain.

Sure the White House struck headline-friendly deals with Pfizer (PFE), AstraZeneca (AZN) and other big pharma firms. The optics looked tough on pricing. But the fine print rewarded these companies for their co-operation with faster FDA reviews and more predictable reimbursement structures.

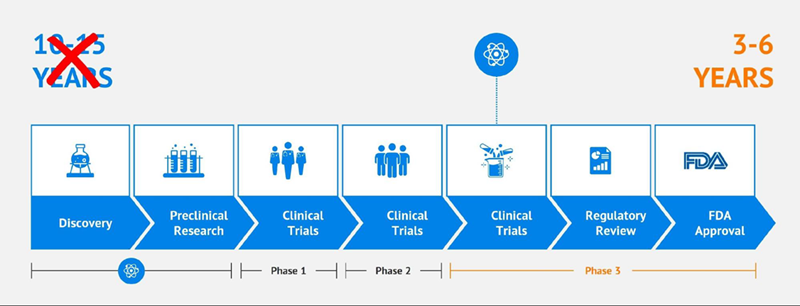

Now, drugmakers are looking to AI, which could cut drug development by up to nine years.

A Building Wave of Breakthroughs

Pharma is one place where we can clearly say there’s no AI bubble. Which is funny, because it’s where the tech can drive some of the biggest gains.

What’s the potential here? Enormous.

Right now, designing a drug and getting it through clinical trials takes 10 to 15 years and costs around $2.5 billion, according to research from Springer Nature. With AI, pharma companies can develop new treatments with far less “trial and error” than human scientists alone. That cuts risk and cost and amplifies these experts’ work.

As a result, industry experts now say the drug-discovery cycle will likely be chopped from 10 to 15 years to just six! That’s critical because patents only last 20 years, so the faster a drug gets out the door, the more its maker can sell before generics eat its lunch.

The bottom line? Pharma profits are poised to pop!

But we’re not going to try to pick the next big winner. Why bother when we can buy into companies that make what every drugmaker needs? I’m talking medical-equipment makers, our favorite “pick-and-shovel” plays on AI-driven drug research.

BDX Is Cheap—and Headed for a Unique “Value Unlock”

Let’s start with Becton, Dickinson & Co. (BDX), whose products are hospital mainstays: syringes, needles, catheters and the like, as well as blood-flow monitors.

Those give BDX revenue that will float higher as the population ages. Then it adds growth from its Life Sciences division, maker of products pretty well every lab needs, like flow cytometers, used to analyze immune cells, cancer cells, and biomarkers.

BDX also makes specimen-collection systems, as well as devices for cell imaging, analysis, genetic testing and other critical lab functions. As AI helps scientists develop more new drugs, demand for these products will grow.

Waters Deal Adds Growth, Streamlines BDX

The company is merging its bioscience and diagnostics businesses with Waters Corp. (WAT), where they’ll match up nicely with Waters’ gear. Waters focuses on equipment in areas such as chromatography (separating and identifying components in a mixture), lab automation and mass spectrometry (breaking down a molecule’s structure).

Management sees the deal doubling the size of the market open to Waters, to $40 billion, and teeing up 5% to 7% yearly growth. BDX’s shareholders will hold 39.2% of the merged company, and Waters investors will hold the rest. That’s just fine; it keeps BDX in the game as AI paces drug development higher. And it lets BDX tighten its focus, too.

The topper? When the deal closes around the end of the first quarter, BDX will get $4 billion in cash. Management will send half of that to shareholders as share buybacks and use the rest to pay down debt.

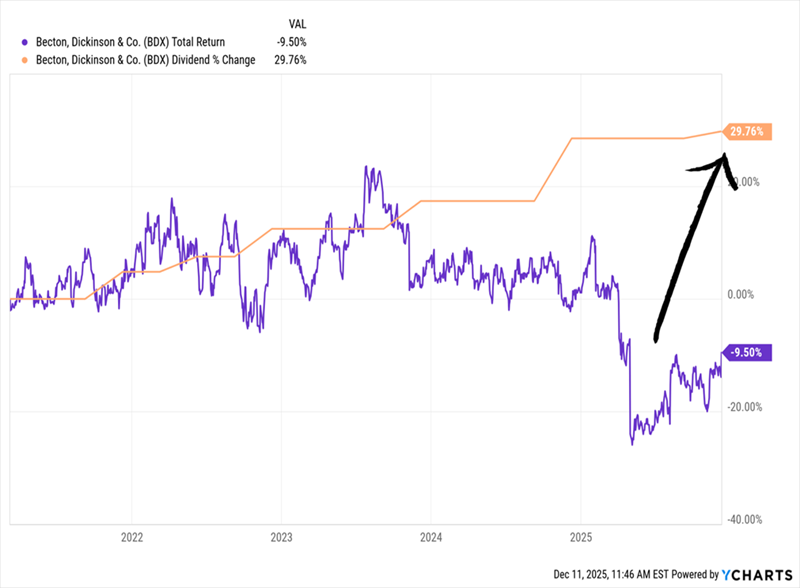

Buybacks cut the number of shares outstanding, boosting earnings per share and dividends, as they leave BDX with fewer shares on which to pay out. That should help BDX’s share price close the gap with its payout growth, which it had been tightly tracking until a disappointing earnings report in May sent the stock tumbling.

BDX’s “Dividend Lag” Says It’s Oversold

As demand for Becton’s products rises, through both its remaining products and its Waters stake, it’ll support dividend growth. Investors will notice (they always do!) and bid the stock up, closing the gap between BDX’s price and dividend.

While we wait, we can be assured that BDX’s payout is built on a strong foundation, accounting for just 45% of free cash flow. That makes now a good time to consider the stock. But if you’d prefer a more diversified medical-device play, we’ve got one teed up for you. It pays more than BDX’s 2.8% yield, too.

An “All-in-One” Medical Device Play With a 7.8% Dividend

I know a lot of readers prefer closed-end funds (CEFs), for good reason: big dividends! And CEF-land has given us a fund perfect for this “dumpster-dive” moment in pharma: the 7.8%-paying BlackRock Health Sciences Fund (BME).

BME’s portfolio is a who’s-who of medical-device makers. What’s more, Becton Dickinson is not a top-10 holding (it’s No. 16, at 1.88% of assets), so you could pick up BME and BDX without overly exposing yourself to that one stock.

Meantime, BME’s top holdings do include medical-device kingpins like Abbott Laboratories (ABT), Thermo-Fisher Scientific (TMO) and Boston Scientific (BSX). Drugmakers like Lilly and Amgen (AMGN) also show up.

We love CEFs because they generally have a fixed share count for their entire lives, so they can trade at a premium or discount to their net asset values.

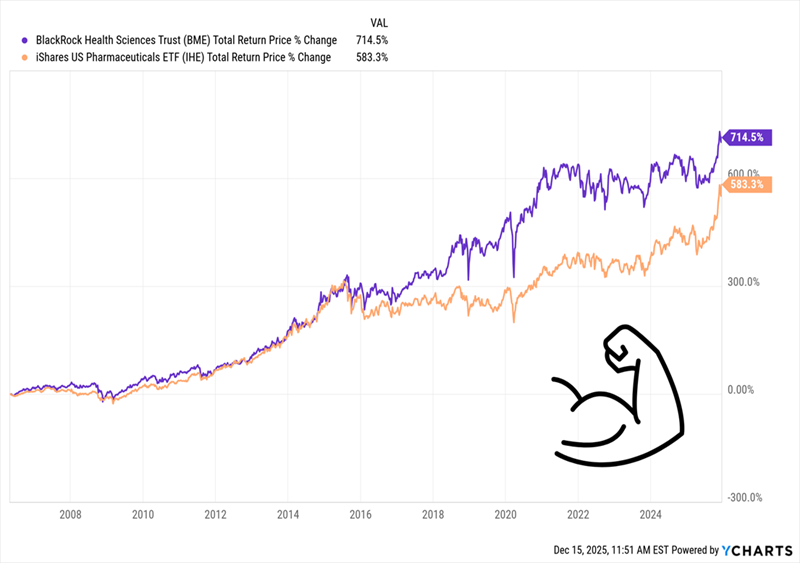

It’s here that we see how much investors have lost the plot on pharma. As I write this, BME trades at an 8% discount to NAV, far below its five-year average of 2.9%. That primes it for gains from our “AI-powered” drug-development wave, boosting its lead on the benchmark iShares US Pharmaceuticals ETF (IHE) since the ETF’s inception in May 2006:

BME’s Closing Discount Could Widen This Healthy Lead

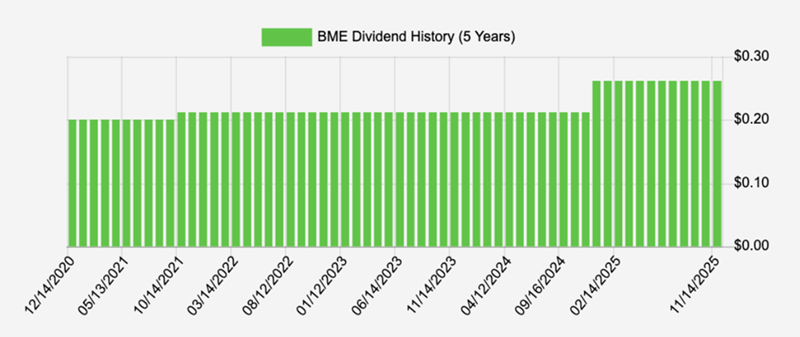

Let’s wrap with that 7.8% divvie, which pays monthly. It’s also grown nicely in the last five years.

A (Monthly-Paid) 7.8% Dividend That Grows

Source: Income Calendar

As AI boosts drug development, I expect BME’s payout to climb higher. That would draw in investors, closing its “discount window” and putting upward pressure on the share price. Buying now lets you lock in a 7.8% dividend before that happens.

5 MORE Urgent Buys Yielding 9% (and Paying Us Every Month)

BME is a terrific example of what we love about CEFs: They let us tap trends like the AI-driven pharma boom while paying us huge dividends—at a discount, to boot!

Monthly payouts are key, too. No matter what markets are doing, we know our next cash payout is only 30 (or 31) days away, and our yield is much higher than most investors get from “mainstream” stocks.

BME is just the start—I’ve assembled a portfolio of monthly dividend payers I want to show you now. These stocks and funds kick out a rich 9% dividend, on average. The kicker? We’re getting the chance to buy these stout monthly payers cheap, too.

I want to make sure you have access to these stout monthly income funds as we head into 2026. Click here for details and my free Special Report revealing their names and tickers.