Washington has a debt problem going into 2026. To put it mildly.

Policymakers are desperate to boost demand for US Treasuries. Higher Treasury prices mean lower Treasury yields. Lower yields translate to reduced interest payments for Uncle Sam on his huge federal debt pile.

The interest payments are what policymakers care about. The total debt is mind-blowing and will never be paid down. The interest, on the other hand, is an annual budget item.

How to reduce the interest via lower bond yields? Leave it to the Washington suits, who “did their thing” with the bills coming increasingly due. They engineered new demand for their government IOUs.

This time, they used legal crypto to do it! And this decision will likely light a fire underneath the share price of a digital-dollar dividend magnet we’re about to discuss.

We’ll talk about this 14% payout raiser in a moment. First, a refresher on the GENIUS Act, which President Trump signed in July. It creates the first federal framework for “payment stablecoins”—a polite industry term for digital dollars that are designed to stay stable at $1.

“Stable” because they are pegged one-for-one to the dollar. “Coin” because, well, that is just Silicon Valley slang.

Now these “coins” are not spare change that gets tossed in a cup holder. Stablecoins are issued by banks and fintechs and are used to move dollars 24 hours a day. They are especially useful for fast settlement and cross-border payments, where “old school” methods like wires can be slow and fee-heavy.

As stablecoin use grows, more dollars will sit in the high-quality reserves that back them, such as Treasury bills and cash equivalents. This turns stablecoin growth into a quiet new source of demand for Treasuries.

Uncle Sam is essentially creating demand for the same bonds he issues to fund his lifestyle. He has OK’d digital money—provided that it works for him!

When these new digital dollars move through the economy, someone will have to process the payments, verify them… and take a small fee of course. Which brings us to the biggest beneficiary of this new digital dollar system—Visa (V), the toll collector on nearly every dollar that moves.

In 2026, Visa’s opportunity is more than mere credit card spending. It is building the new bridge between traditional payments and regulated stablecoin settlement.

Last week, Visa launched stablecoin settlement in the US. This is the behind-the-scenes bank-to-bank money movement that happens after you swipe your card.

This business is growing quickly. As of November 30, Visa’s monthly stablecoin settlement volume had already reached a $3.5 billion annualized run rate. The “digital dollar” pipes are live in the US. Now that the pipes work, volume can scale fast. The tolls are being collected, baby.

As more banks and fintech companies issue stablecoins, this number will only grow. Think of a stablecoin like a casino chip—except it’s digital. Inside the “casino” (the stablecoin network), it behaves like money. It’s fast, secure and easy to move. But you still have to get in (swap dollars for stablecoins) and get out (convert back to bank money) when you want to spend in the normal world.

Visa is positioning itself as the cashier’s cage. It’s the bridge that makes these digital dollars usable everywhere.

Visa has quietly built the infrastructure to treat these “digital casino chips” like regular dollars. Two moves last week reinforce this:

- Visa unveiled its new Global Stablecoins Advisory Practice. It’s now the preferred consultant teaching banks, fintechs and merchants how to use stablecoins to move money.

- Visa also launched settlement using USDC (USD Coin), a widely used digital dollar, which means issuers can now settle transactions with Visa using stablecoins. They no longer need to wait for slow wire transfers.

Visa mints over $20 billion in annual free cash flow and spends half on buybacks and dividends. This is what makes Visa’s dividend—and stock price—go, go and go. Over the past five years, Visa’s payout has popped by 84%, pulling its stock higher “like a magnet”:

Visa’s Dividend Magnet is Due

With a fortress balance sheet, Visa can afford to test new payment tech while still feeding shareholders. It’s the rare growth stock that already pays us to wait. Traditionally, Visa’s growth was powered by consumers swiping credit cards. Going forwards, however, the company will profit from a growing money system.

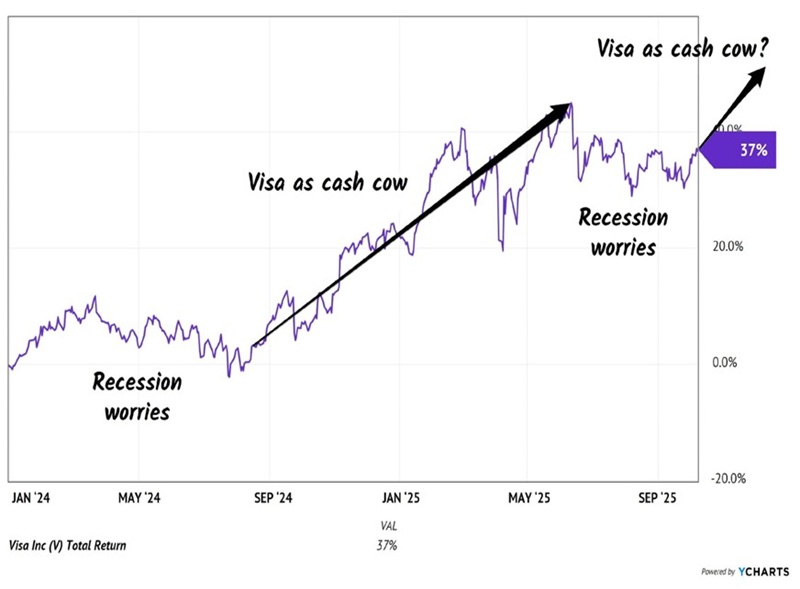

We’re up 30% on Visa since we re-added it to our Hidden Yields portfolio last August. But the stock topped out in June, pulled back and has traded sideways since.

Why? Recession worries are a recurring Visa headwind. Vanilla investors still think this merely a credit card company. They are looking out of the rearview mirror.

We contrarians gladly buy the “bad weather” events for this constant cash cow! Last August, we caught Visa coming out of its latest bout of “recessionitis.” With stablecoins on the horizon, this cash cow is ready to stampede higher:

Alternating “Recession Worries” with “Cash Cow”

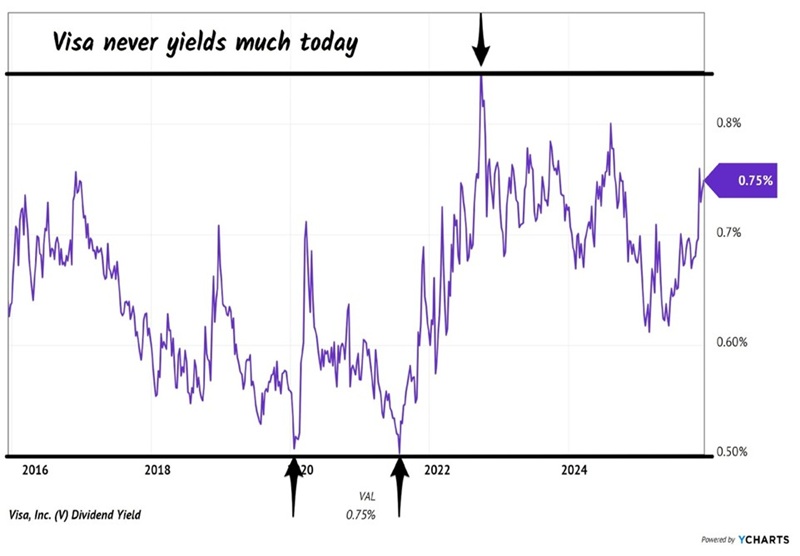

Visa is going to feast on the upcoming digital dollar bonanza. Granted, the current yield on Visa looks sleepy. It yields 0.75% today and to be honest it always pays between 0.5% and 0.85%. So, vanilla investors ignore it.

Visa’s “Sleepy” Current Yield

But then we contrarians peel back the dividend onion.

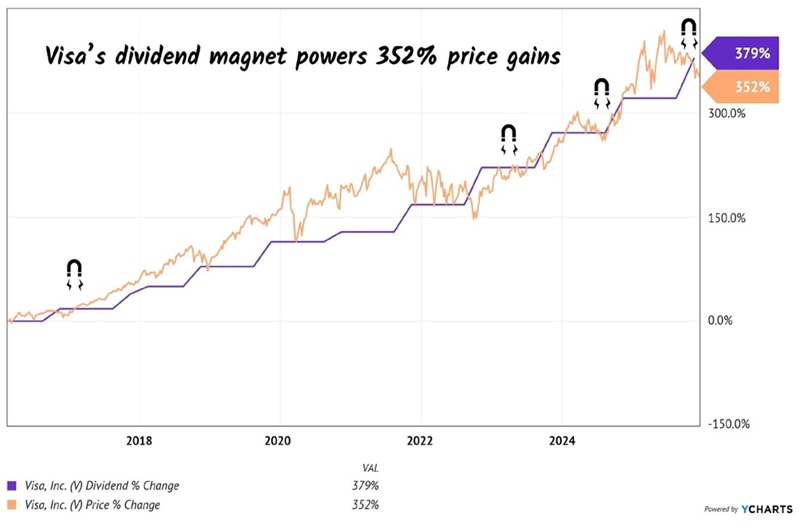

Visa just raised its dividend by 13.6%. This type of generous raise is an annual occurrence. Over the past decade, the payments company has hiked its dividend by a terrific 379%. The annual double-digit raises add up!

And the important phenomenon is the “dividend magnet”—the power that Visa’s payout exerts on its stock price. The dividend literally pulls the price higher, with investors enjoying 352% gains (and 383% including dividends paid):

How a “Sleepy” Dividend Safely Makes Investors Rich

That’s the dividend magnet at work. Rising payouts help patient investors get rich, safely and securely. With this digital dollar catalyst, it’s only a matter of time before higher profits send this payout—and stock price—even higher.

And Visa isn’t the only dividend magnet that is set to soar in 2026. I like five more stocks that will sail regardless of what happens in the broader economy. Click here for my 2026 dividend magnet research.