Wall Street, please. Enough with the narratives.

CNBC and Bloomberg have become the ESPN and Fox Sports of the financial world. Stories are simplified, spun and spoon-fed to the audience.

We thoughtful contrarians can’t stomach this junk any longer!

These “experts” have vanilla investors sweating every headline. The always-impending recession. Job losses. Trade wars. Geopolitical battles. Domestic political dysfunction.

Sure, there’s a kernel of truth to every story. But investors who ride this roller coaster suffer heart palpitations and (worse!) retirement portfolio underperformance. They get scared stiff by the media coverage, sell stocks at the wrong time (near lows) and stay on the sidelines for too long.

Most investors are terrified of a recession because they own things people stop buying when times get tough. We own the things people literally cannot live without—like lunch.

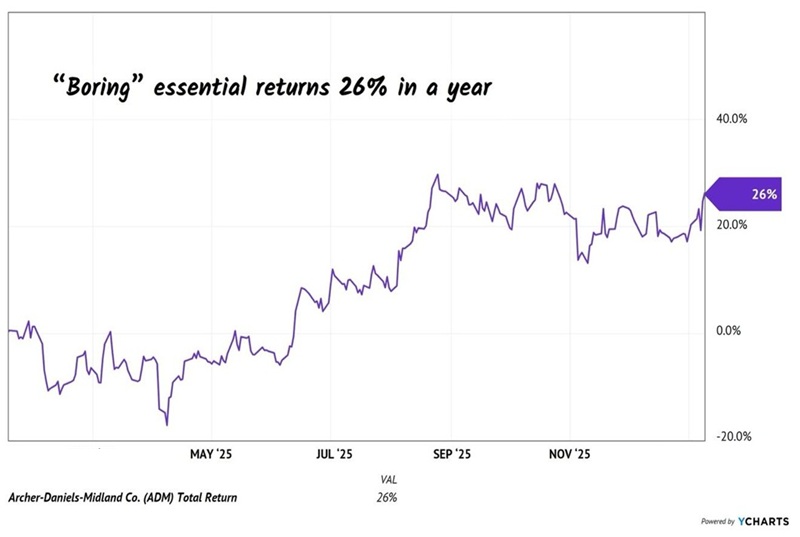

Regardless of what awaits in 2026, people are going to eat. In my Hidden Yields, we played this “three meals a day” trend exactly one year ago and bought the company that processes the corn that goes into everything in the grocery store, Archer-Daniels Midland (ADM).

ADM is a “boring” company that prints cash in any economy. As the broader market chopped and churned over the past 12 months, this underappreciated food trade delivered 26% total returns to HY subscribers. No heart palpitations, just dividends (including one raise!) and price gains:

People Keep Eating, ADM Returns 26%

If you missed that run, I’ll share some good news—you have a second chance. ADM has pulled back in recent months, presenting us with a sweet opportunity to reload for 2026.

The stock topped out in late summer because Wall Street was concerned about low “crush margins,” industry jargon for the profit ADM makes from processing soybeans into meal and oil. Vanilla investors incorrectly saw this as a negative trend and sold the stock.

We careful contrarians know better. Agricultural markets move in predictable cycles. When corn prices are high, farmers plant more acres to chase the profit. That new supply floods the market, prices drop and farmers then plant less or switch crops (to cotton, for example).

Corn and soybean prices have come down in recent years, and the “dumb money” is fleeing the sector. This is exactly when we buy—at a cyclical low, with catalysts lining up to send related plays like ADM higher again.

Because recession or not, people keep eating. The global population is still climbing, adding millions of new mouths to feed every year. Developing nations are becoming wealthier and, with their money, people demand protein.

Raising chickens, pigs and cattle requires massive amounts of feed—mostly corn and soy meal. It takes about six pounds of feed to produce one pound of beef. This “multiplier effect” sets a floor on the corn and soybean fee inputs going forward and, guess what? They’re already about as low as they’re likely to go. It’s not a matter of if grain prices turn higher. It’s when.

Two previous worries for ADM are likely to turn into catalysts. First, policy. The EPA proposed a new Renewable Fuel Standard rule that includes higher biomass-based diesel targets. If approved, this will boost demand for corn and soybeans—and quickly improve those crush spreads. More profit for ADM.

Second, the business is getting leaner, cutting $500 to $700 million in annual costs over the next three to five years. While we wait, this “shareholder yield” monster is maximizing our future profit per share. Management’s aggressive share repurchases power a higher stock price. Over the last five years, ADM has reduced its share count by a fantastic 14%.

These “disappearances” are the quiet driver of total returns. They are the reason we earned 26% in a quiet year for crops. When ADM buys back its own stock, it reduces the number of shares outstanding. Every remaining share then owns a larger slice of the profit pie. This is how earnings per share (EPS) can increase, even if total earnings stay flat.

As we speak, ADM is using this “mini dip” in the stock price to buy back even more stock on the cheap. These smart shoppers know their stock is cheap and they are gobbling it up before crop prices rally.

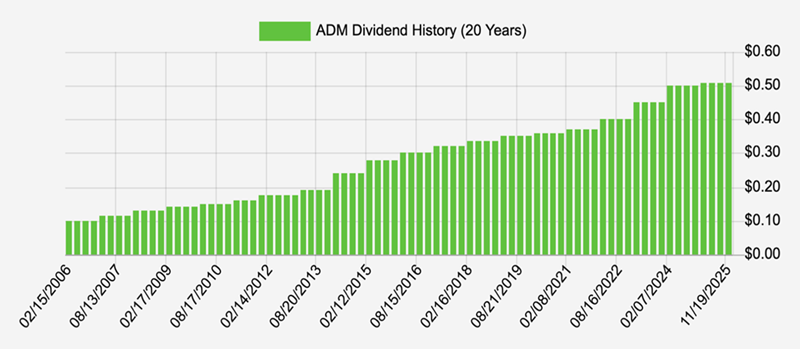

Finally, there’s the dividend. ADM is a “Dividend King,” meaning it has raised its payout for more than 50 years in a row. Which means that through the inflation of the 1970s, the dot-com bubble, the Great Recession and COVID, ADM never missed a raise.

Last 20 Years of Dividend Kingpinning

I imagine it’ll do just fine through ’26, too—bull or bear!

ADM checks all the boxes we look for in Hidden Yields. Its products are essential. It’s boring. It’s bulletproof. It has plenty of upside and it generously pays us a 3.5% yield while we wait. And by the way, ADM is due to hike its dividend in the weeks ahead, making this is our last chance to “front run” the raise. Let’s not dilly-dally!

And ADM isn’t alone. I have identified five more “essential” stocks that are trading at similar valuations to where ADM was last January. These are recession-resistant dividend growers that are positioned to return 15% (or more) in the year ahead, regardless of what the economy does.

These are not the stocks you’ll see discussed on CNBC. They are too boring for TV! But they are exactly the kind of stocks that build real retirement wealth.

Start your risk-free trial to Hidden Yields here and you’ll receive immediate access to my “Recession-Proof Retirement” plan and see my five favorite “essential” dividend stocks ready to rally in 2026.