Most people are totally missing the point on the AI trade. To use a hockey analogy (it is the dead of winter, after all!), they’re skating to where the puck is, not where it’s going.

They’re debating whether Meta Platforms (META) or Microsoft (MSFT)—which took a header last Thursday—are spending too much on AI, or whether all of this cash is pumping air into a stock-market bubble. Or whether OpenAI will turn out to be the Netscape of AI—jumping out to an early lead only to lose out to a competitor.

Distractions. All of them.

Big Tech is so 2025. This year, AI isn’t going to be about what might happen. It’s going to be about how this tech is generating real revenue—and profits—now.

Silicon Valley is not going to be the main story here. That’s where the puck is. Where it’s going is to places like insurance, healthcare—even farming.

Let’s focus on that last one for a moment, because us dividend investors want to own stocks in “ag” for two reasons:

- They’re essential: In any economy, people have to eat. Farmers must plant, spray and harvest. We want to own the companies that make those things happen (better still if they’re dividend-growing “utilities” farmers can’t live without, like the stock we’ll discuss below), and …

- They’re, er, ripe to be disrupted by tech like AI, autonomous vehicles, you name it. This is already happening—and it’s not priced into ag firms’ prices yet.

Now, before we go further, I should say that I don’t want you to take my focus on these kinds of stocks to mean we’re buying into all the doom and gloom out there. No way.

Here at Contrarian Outlook, we realize that higher unemployment numbers do not mean we’re headed for a slowdown. They mean businesses are using AI tools to automate work. And fewer workers doing more work is exactly what customers of the company we’re going to look at next want.

Deere Brings AI Into the Field

That would be Deere & Co. (DE). We’ve held the stock in the portfolio of my Hidden Yields service since October 2024. It’s returned 32% for us in that time, as of this writing.

Forget self-driving cars, Deere is testing self-driving tractors. “Autonomy-ready” models (as well as upgrade kits for existing gear) exist right now.

That sounds pretty, well, out there. But when you think about it, it’s really not. A self-driving car, for example, has to deal with all manner of chaos: pedestrians, cyclists, busy intersections and construction, to name just a few.

A tractor? It has a lot less to deal with, moving more or less in a grid as it tills, plants, sprays and harvests. That’s a simpler system to automate, especially when you bring AI to bear, as Deere does.

Orders for Deere’s autonomous tillage machine are opening soon, and the same kind of tech is going into other products, too. Smart sprayers, for example, are equipped with cameras and AI that can identify weeds in a field and spray them directly. According to the company, this tech can cut usage of herbicides by up to two-thirds over traditional spraying.

The great thing about these products from a shareholder perspective is that they’re “sticky”: Once a farmer starts using them (and the software platforms behind them), it’s tough for them to switch to a competitor.

These are precisely the kinds of innovations that let businesses do more with fewer workers—and drive stronger growth. And they’re what mainstream economists, focused as they are on “old-school” jobs reports, are missing.

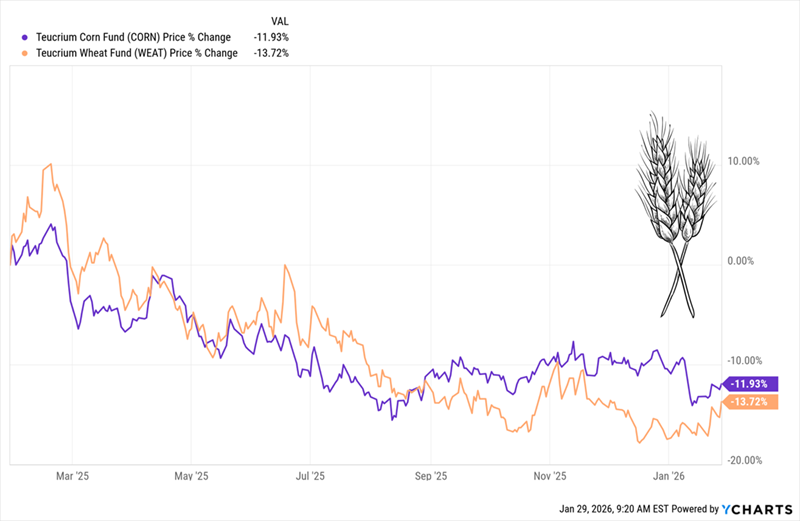

Now, it’s no secret that US agriculture has taken a hit in the last year, with corn and wheat prices dropping, going by the two Teucrium ETFs tracking them, which are reasonable proxies for price trends. Trade wars haven’t helped.

Corn, Wheat ETFs Remain Weak, Setting Up Our Opportunity

All of that has weighed on Deere, but contrarians like us also know that setbacks like these are what creates opportunity. Moreover, in their recent earnings call, management did something interesting: They called the bottom.

They’re telling us 2026 will mark the bottom of the large ag cycle. That doesn’t mean things are instantly rosy. Deere’s own outlook still calls for large ag equipment sales to be down 15% to 20% in the US and Canada.

But we don’t buy Deere when farmers are bingeing at the equipment dealer. We buy when the cycle is in the dumps and ready for its next move up.

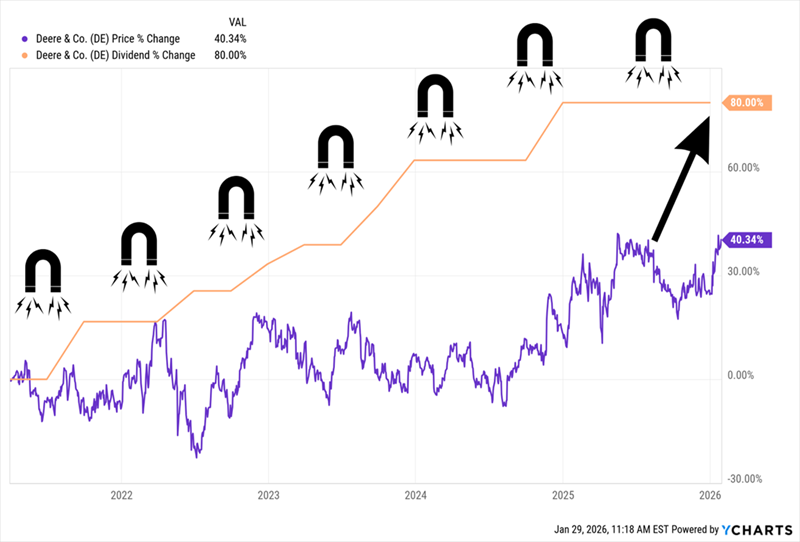

Another upside driver for Deere is the fact that the stock’s price is trailing the firm’s dividend, which has jumped 80% in just the last five years. But as the ag cycle shifts, I expect that to change, and for the stock to keep narrowing the gap, as it has been.

Deere’s Dividend Magnet Starts to Regain Its Pull

We also take comfort in the fact that the dividend is safe and can keep growing, even if the ag cycle takes a little longer to turn, with the payout occupying a reasonable 53% of the company’s last 12 months of free cash flow.

That dividend is also backed by Deere’s strong balance sheet, with around $43 billion of debt, net of cash and short-term investments. That amounts to a reasonable 41% of its assets and an even more modest 28% of its market cap.

All of that said, I expect the stock to move up (and down) over the coming months, as the ag recovery struggles to find its footing, so we do have time to make a move here.

But make no mistake: This management team knows how to navigate tricky commodities markets. It’s only a matter of time before investors give them their due—including their savvy moves into AI and autonomy—and price the stock accordingly.

Deere Is the Kind of Stock We Want to Own, Bull or Bear

We love Deere for all the reasons I just talked about: Its products are essential for farmers. And its new, tech-forward products are making its relationships with them even stickier.

In short, the company is shifting from a cyclical manufacturing stock to a type of tech-driven ag “utility.” That’s exactly the kind of dividend grower we look for in uncertain markets like this one.

In the latest issue of Hidden Yields, I got even more granular on Deere’s prospects, including how I’m positioning it in our broader portfolio as the ag cycle bottoms and AI use grows. I also reveal our exact buy-up-to price on the stock.

You can get this issue, plus two full months of Hidden Yields (with instant access to the full portfolio of dividend growers) when you start a no-risk 60-day trial.

I’ll give you more, too, like my top 5 dividend-growth picks for 2026 (bull or bear) and a free Special Report naming each of these 5 bargain-priced dividend plays.

Here’s how to take advantage:

Simply click here and I’ll walk you through these 5 “must-own” picks for 2026 and give you that exclusive report, as well as your no-risk trial to Hidden Yields—including the latest issue, with my updated call on Deere.