New tariffs. A government shutdown. A brutal selloff in the software sector with speculation that AI will eat everything in its wake.

Concerned about a pullback? An outright bear market? Fair enough and, if so, let’s talk about beta.

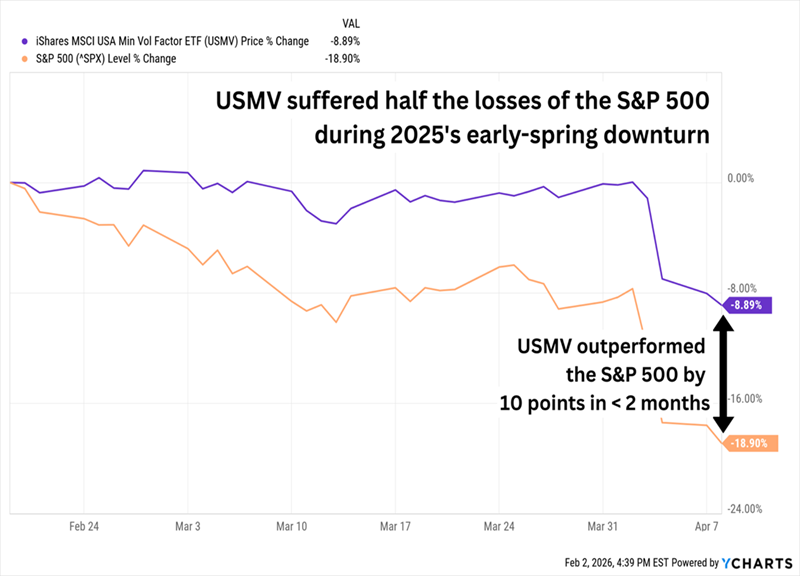

Low beta stocks are our best friends for surviving a bear market. Stocks with betas below 1 are considered less volatile than the overall market. For example, we’d expect a stock with a beta of 0.5 to drop only half as much as the S&P 500 during a pullback.

Let’s consider low-beta fund iShares MSCI USA Min Vol Factor ETF (USMV), which did its job in the leadup to the “Liberation Day” panic last year. The S&P 500 dropped 19% while USMV shed only 9%:

Low Beta Fund Beat the Market

And that’s just a simple fund. We can do even better if we cherry pick our favorite low-beta dividend payers.

The idea, of course, is not to lose money. It’s to make money regardless of what happens in the broader market. To do this we’ll consider six low-beta stocks yielding 5.8% to 8.4%.

First up is Apple Hospitality REIT (APLE, 8.1% dividend yield), featured in my recent breakdown of generous monthly dividend payers. The hotel real estate investment trust is low drama, boasting tranquil 1- and 5-year betas of 0.73 and 0.83, respectively.

Moving on to aisle five we have Campbell’s Co. (CPB, 5.8% dividend yield), which now boasts a tasty yield. Unfortunately the big divvie is due to a rough three-year price decline.

Unfortunately, CPB Took the Other Route to a High Yield

Can Campbell’s turn the corner? The company is more than Campbell’s soup—its wide portfolio of grocery staples includes Pepperidge Farm baked goods, Goldfish and Lance crackers, Cape Cod and Kettle Brand chips, and Prego pasta sauces, V8 vegetable juices, and Pace salsa, among others. This diversification should be a strength, but the company has struggled virtually across the board amid constant inflation, cautious consumers willing to go private-label to save money, and its own increasing input costs. It has made a few acquisitions in recent years to spur growth—most notably, its 2024 acquisition of Sovos Brands that brought in the fast-rising Rao’s pasta sauce and Michael Angelo’s frozen meal brands.

CPB is expected to rebound next year. Analysts believe Campbell’s will post declines on both the top and bottom lines in 2026. But the dividend—which CPB improved in 2025 for the first time since 2021—is well-covered at about 65% of this year’s meek earnings estimates. The stock’s 1- and 5-year betas of 0.06 and -0.04 would normally be encouraging for defense hunters, but in Campbell’s case, they reflect lethargy more than stability.

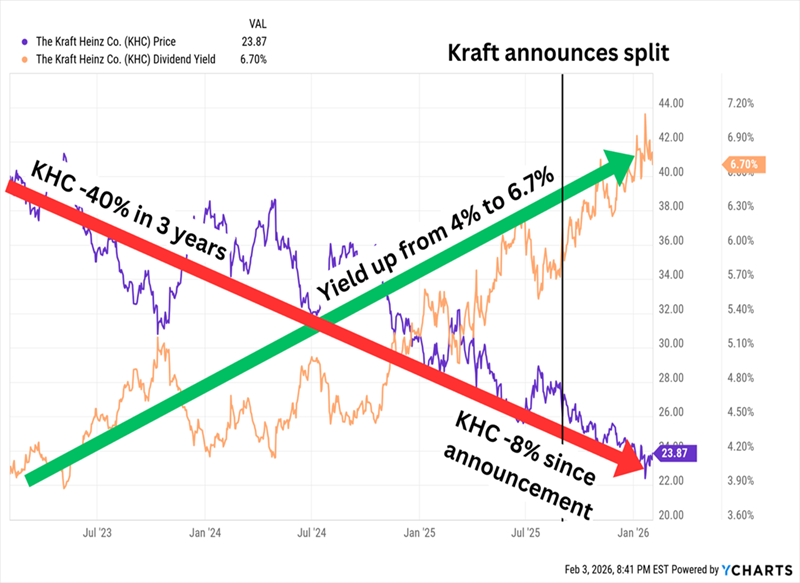

Speaking of beat-up consumer staples names, let’s check in on Kraft Heinz (KHC, 6.7% dividend yield), which we discussed with other dividends that were circling the drain last summer.

Kraft has since announced it’s splitting its business into:

- “Global Taste Elevation Co.”: A “roster of iconic brands and local jewels,” including billion-dollar brands Heinz, Philadelphia and Kraft Mac & Cheese. We frequently see corporate splits divide a company into a growth arm and a more stable, cash-generating arm; Global Taste Elevation is expected to be the former.

- “North American Grocery Co.”: A “portfolio of North American staples” that includes its own trio of billion-dollar brands—Oscar Mayer, Kraft Singles, and Lunchables. This is likely to be the stodgier (but perhaps better-paying) arm.

We’re constantly told that M&A is great for “unlocking shareholder value.” This has not been the case with Kraft.

Kraft is a Gooey Mess

Like with Campbell’s, its marginal 1- and 5-year betas of 0.07 and 0.05 signal low volatility but not in a good way. The patient is on life support.

And now, it appears the Kraft bear crowd will add a very big name: Berkshire Hathaway (BRK.B). New CEO Greg Abel recently signaled that he could be exiting the company’s 27.5% stake in the company, making an SEC filing to register the potential resale of up to 325 million shares. That doesn’t necessarily mean Berkshire will sell, but it does set the company up to do so.

Our final food name is Flowers Foods (FLO, 8.4% dividend yield), another down-on-its luck grocery presence.

Flowers is a bakery giant whose businesses can largely be split into bread (Wonder, Sunbeam, Nature’s Own, Dave’s Killer Bread, among others) and snacks (Tastykake, Mrs. Freshley’s and more). But all of that is the “Branded” segment, which makes up about two-thirds of revenues; the remaining third is generated by an “Other” segment that includes private-label brands and other business.

FLO is facing many of the same pressures as the aforementioned staples companies, but it’s also more susceptible to improving health trends and GLP usage. And it has piled up heavy debt, too. The company is also subject of a case—Flowers Foods v. Brock, which will determine whether last-mile drivers are exempt from the Federal Arbitration Act—heading to the Supreme Court next month.

So despite what its 1- and 5-year betas (0.12 and 0.33) might otherwise suggest, shares have cracked under heavy pressure—though that has lifted the yield to nearly 9%.

This Stock Could Use Some Yeast

Not all of that yield jump can be chalked up to stock losses—Flowers has been stubbornly raising the dividend against the tide. But I have to wonder whether management knows something that my calculator doesn’t—its 24.75-cent quarterly dividend comes out to 99 cents per share annually. FLO is expected to earn $1.03 this year and 98 cents in 2027. S&P Global Ratings has noticed: Late last year, the debt-scoring agency lowered its rating on Flowers from BBB to BBB-, which is the lowest tier of investment-grade.

That said, the stock is dirt cheap. Shares trade at half the company’s sales, and FLO’s revenue mix is increasingly leaning into the higher-margin, higher-growth Branded segment. There’s light at the end of the tunnel—whether or not it’s the headlights of an incoming train remains to be seen.

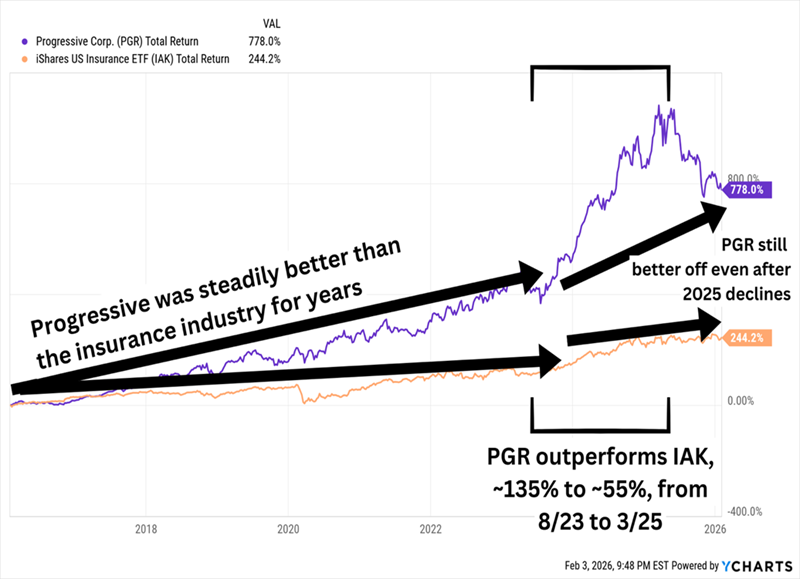

Speaking of “Flo,” let’s look at Progressive (PGR, 7.0% dividend yield), which is admittedly on the schneid itself. But unlike our troubled consumer staples stocks, PGR merely appears to be reverting to the mean after break-neck share growth.

PGR Has Been Working Off High Valuations for a Year

Progressive writes personal auto, residential property, business general liability, commercial property, and workers compensation insurance, among other policies. We’ve previously bagged 87% gains on this stock in my Hidden Yields service, and it remains on my watchlist today.

Artificial intelligence (AI) is changing a lot of industries. Most people immediately think tech—but anyone who knows an actuary or two knows that AI is coursing through the insurance business, too. Progressive, for instance, is currently using AI to refine Snapshot—its program that adapts rates based on real-time data from a customer’s car—as well as to analyze photos of damage to speed up claims.

Like with the staples companies, Progressive’s modest 1- and 5-year betas (0.54 and 0.31) more so reflect its struggles than anything else, but PGR has historically been a smooth operator.

But the high yield? That’s new. And it might—or might not—be fleeting. PGR pays a nominal quarterly dividend of a dime per share that comes out to a yield of about 0.2%. However, it has also been paying increasingly large special annual dividends in each of the past three years; its most recent distribution of $13.60 per share cranked that annualized payout up to 7%. It’s probably not an ideal situation for anyone relying on regular income, but it’s a nice kicker for anyone focused on total returns.

But as I said before, it’s on my watch list, and I’m still watching. Despite its selloff, PGR still trades at 4 times book.

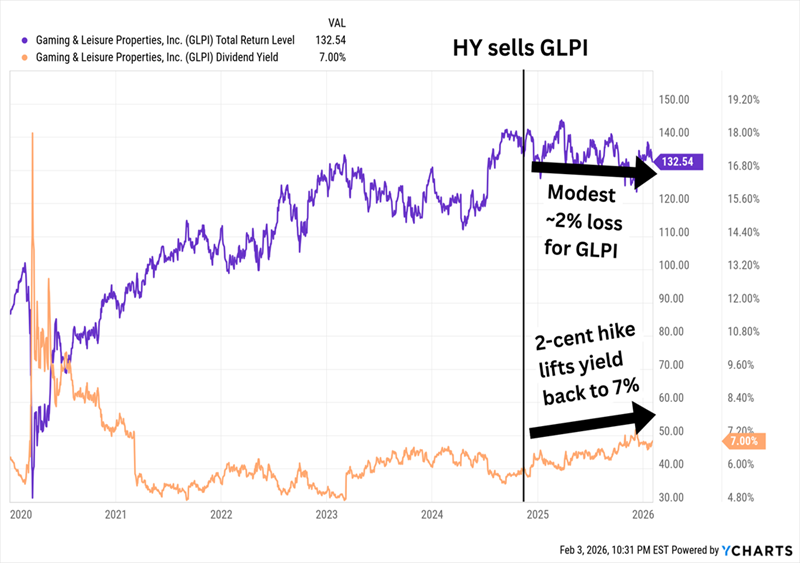

My Hidden Yields service also has a brief history with Gaming & Leisure Properties (GLPI, 7.0% dividend yield), a casino and gaming REIT with 69 assets under brands such as Caesars Entertainment (CZR), PENN Entertainment (PENN), Boyd Gaming (BYD), and more. GLPI stands out from other gaming names in that it has extremely little exposure to the hub of American casinos, Las Vegas—its only property there is The Tropicana. Instead, its properties are spread across 20 states, from New Mexico to Ohio to Rhode Island.

We held GLPI for a little more than a year between 2023 and 2024 before collecting a tidy profit. And despite selling just as the Fed started cutting its target rate (generally good for REITs), the stock—even including its sizable dividend—is sitting on a small loss since then.

The House Has Held GLPI to Roughly Breakeven

Here, though, GLPI’s 1- and 5-year betas (0.17 and 0.68) are actually proof that GLPI has largely been hanging tough. The past year-plus especially has been brutal on the gaming space between a stiff decline in international tourism and a tougher economic backdrop holding back domestic gamblers.

There’s no sign of weakness in Gaming & Leisure Properties’ capital plans, with the company primed to spend more than $3 billion over the next two years while still keeping a reasonable amount of leverage. Meanwhile, GLPI’s dividend surpassed its pre-COVID-cut heights years ago, and it keeps growing, including a roughly 3% hike last year. The current 78-cent quarterly payout comes out to roughly 75% of adjusted funds from operations (AFFO) estimates, which is plenty safe in REIT-speak. Shares trade at less than 11 times those estimates, too.

5 Stocks We Want to Own in 2026 (Bull or Bear!)

I’ve already talked about two companies we’ve turned a profit on through Hidden Yields.

Do you want to know what names are next?

You can get my latest issue of Hidden Yields—which includes a granular look at an AI play out in farm country—plus two full months of Hidden Yields (with instant access to our full portfolio of dividend growers) when you start a no-risk 60-day trial.

I’ll give you more, too, like my top 5 dividend-growth picks for 2026 (bull or bear) and a free Special Report naming each of these 5 bargain-priced dividend plays.

Here’s how to take advantage:

Simply click here and I’ll walk you through these 5 “must-own” picks for 2026 and give you that exclusive report, as well as your no-risk trial to Hidden Yields—including the latest issue, with my updated AI farm call.