This administration is set on cutting interest rates—and they have the tools to do it.

The last thing we contrarian income investors want to do is fight Uncle Sam. Instead, we’re going to front-run his moves with an 11% payer that’s set up nicely for what’s coming.

The reason behind the lower-rate push is pretty obvious: 2026 is an election year, and the administration wants lower borrowing costs heading into the vote.

Bessent, Not Powell (Or Warsh) Is the One to Watch Here

Most people think Jay Powell, or newly nominated Fed chief Kevin Warsh, are the lynchpins here. But when it comes to rates, the real power lies with Treasury Secretary Scott Bessent.

We’ve written before about how Bessent has been issuing the vast majority of Uncle Sam’s debt at short-term rates (controlled by the Fed), then using the borrowed funds to buy up longer-term debt.

This lets the government borrow at short-term rates, which are generally cheaper (hence the pressure heaped on Powell).

But more important for bonds is that Bessent’s moves cut the supply of long-term Treasuries. That drives up demand (and prices), while capping yields in the process.

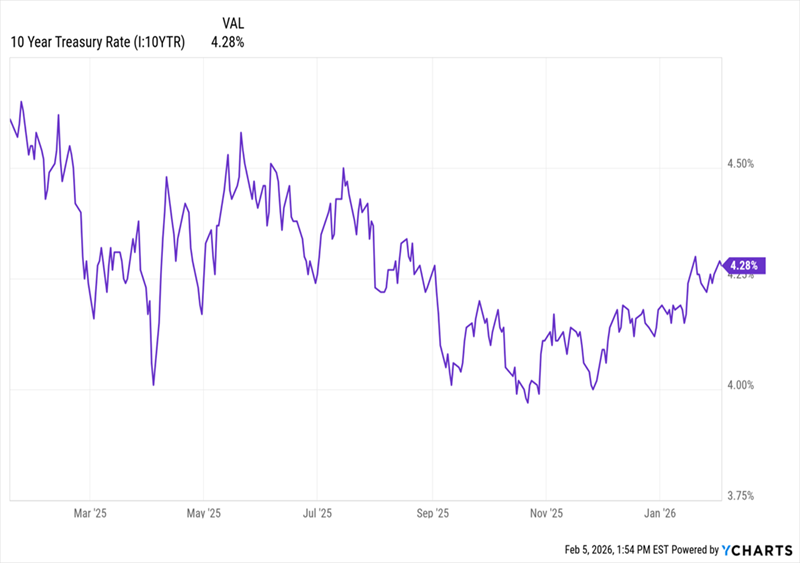

It’s a recycling program for Uncle Sam’s debt! And it leaves even fewer long-dated Treasuries for investors to buy. You can see Bessent’s “yield cap” in action as 10-year yields have bumped up against the 4.6% “ceiling” during the first year of Trump 2.0, before heading lower:

Bessent’s “Yield Control” Clips the 10-Year

This setup—stable or falling Treasury yields—puts a floor, plus some upside, under bonds. And that 11% payer I mentioned a second ago is our go-to here.

Long-Duration Bonds Give This 11% Payer an Edge

The PIMCO Corporate & Income Opportunity Fund (PTY) is a closed-end fund (CEF) that stands out in a rate setup like this for a lot of reasons, but a key one is the long effective maturity on the credit assets in its portfolio—just over seven years as I write this.

That’s important because longer-duration bonds do better in falling-rate environments, as they’re more attractive than new (and lower-yielding) debt issued as rates decline.

Moreover, its effective leverage-adjusted duration is 3.8 years. That’s enough to set the fund up to gain on lower rates without taking on too much risk if rates rise.

With all that in mind, it’s surprising (to me) that PTY is trading at such a bargain right now.

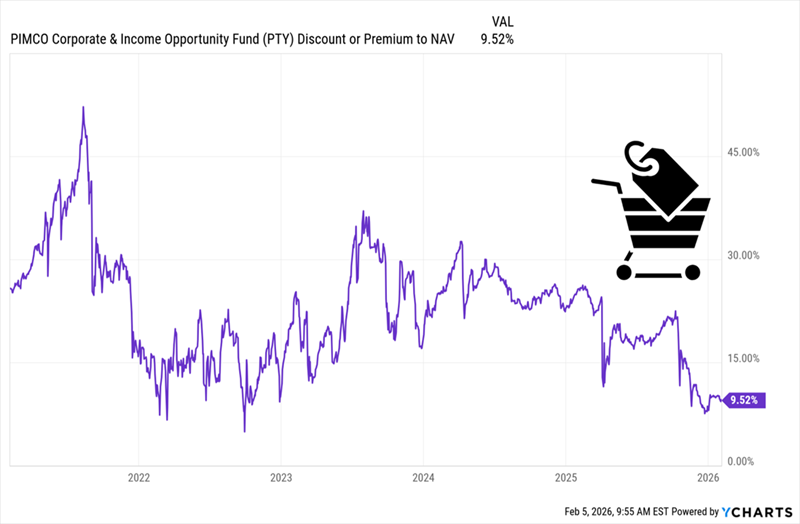

Now, if you’ve skipped ahead and looked at this fund on a screener, you might think I’ve lost my mind. After all, PTY trades at a 9.6% premium to NAV. That means investors are paying just under $1.10 for every dollar of the fund’s assets.

But with CEF discounts, context is key. Because PTY is actually on sale at that level. But to see that, you need to look deeper than that “headline” discount number. As I write this, that premium is lower than it’s been since the bond (and stock) meltdown of 2022.

PTY’s “Discount in Disguise”

That makes zero sense. Back in ’22, inflation hit 9%. You’re telling me that today, with rates primed to go lower, is a worse setup for PTY?

The fund’s discount is obviously overdone. And indeed, if you look closely at the chart above, it looks like it’s carving out a bottom here. But why the premium in the first place?

PIMCO, founded by legendary investor Bill Gross back in the ’70s, has long had a grip on investors’ imaginations, giving the brand an almost superhuman mystique. That’s why PTY—and indeed the vast majority of its funds—trade at premiums.

Gross was replaced by Dan Ivascyn years back, and he went on to nab Fixed-Income Manager of the Year honors in 2013 and be inducted into the Fixed Income Analysts Society Hall of Fame in 2019.

Ivascyn’s team has spread the portfolio across US high-yield debt (39%), emerging markets (13%) and non-US developed markets (16%). The other roughly 32% is in non-agency mortgage-backed securities, investment-grade bonds and other loans.

There’s a lot to like about this split, as the fund’s US bonds stand to gain as rates fall, while its non-US holdings, they get a couple other tailwinds:

- They benefit as US investors look abroad for higher yields, and …

- Any unhedged holdings in its portfolio could benefit as the US dollar falls, as it has lately.

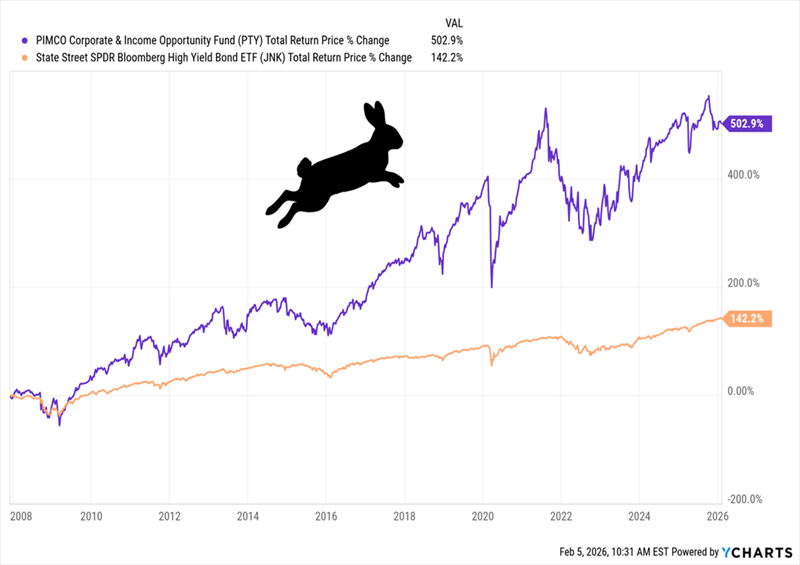

In the long haul, it’s tough to argue with PTY’s performance. The fund has been around since 2002, longer than the benchmark US corporate-bond ETF, the SPDR Bloomberg High Yield Bond ETF (JNK).

In the years since JNK’s launch, it’s clobbered that benchmark. It’s no contest!

PTY Laps JNK—Again and Again

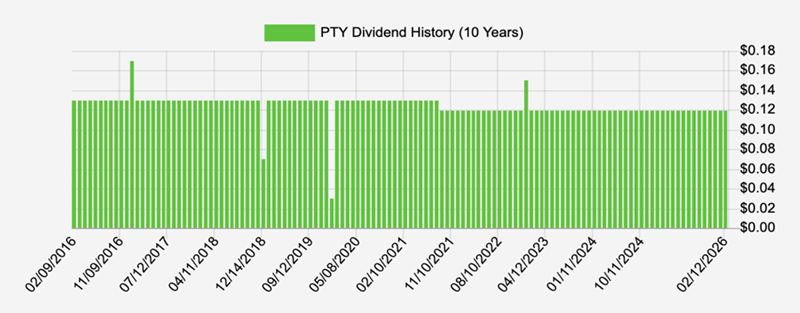

What’s more, reinvested dividends drove pretty well all of that return, thanks to PTY’s huge monthly payout.

A Reliable 11% Dividend

Despite a slight reduction during COVID, this fund’s payout has been holding steady for years, including through the 2022 mess. And besides, its regular special dividends (the spikes and dips above) have gone a long way toward making up for that cut.

And today, with lots of factors putting downward pressure on rates, we can expect a floor under this rich payout, too.

1 Click to “Amp Up” Your Dividends to 14.9% (and Get Paid Monthly)

Dividend payers like PTY are the cornerstone of my “Monthly Dividend Portfolio.” As the name says, this collection of stocks and funds holds assets that pay you every single month.

And big dividends are the order of the day here: This portfolio sports payers with yields as high as 14.9%. And they’re diverse, too, giving us exposure to stocks and bonds from across the economy. That’s a natural “shock absorber,” especially important in wobbly markets like this one.

These stout monthly payers are not just about dividends, either. My research indicates they’re cheap now, setting us up for potential gains to go along with our high dividends.

Don’t miss your chance to buy now, and get lined up for this portfolio’s next round of monthly payouts. Click here and I’ll walk you through my Monthly Dividend Portfolio (with payouts up to 14.9%) and give you a free Special Report revealing the names and tickers of the stocks inside.