There’s an activist story shaking the CEF world right now. And no matter how it plays out, it could lead to shrinking discounts in these high-yielding funds.

We’re going to break down what’s happening today. Then I’m going to give you my favorite way to line yourself up for one-time events like this—an activist play, a takeover, a stock split—in your own portfolio.

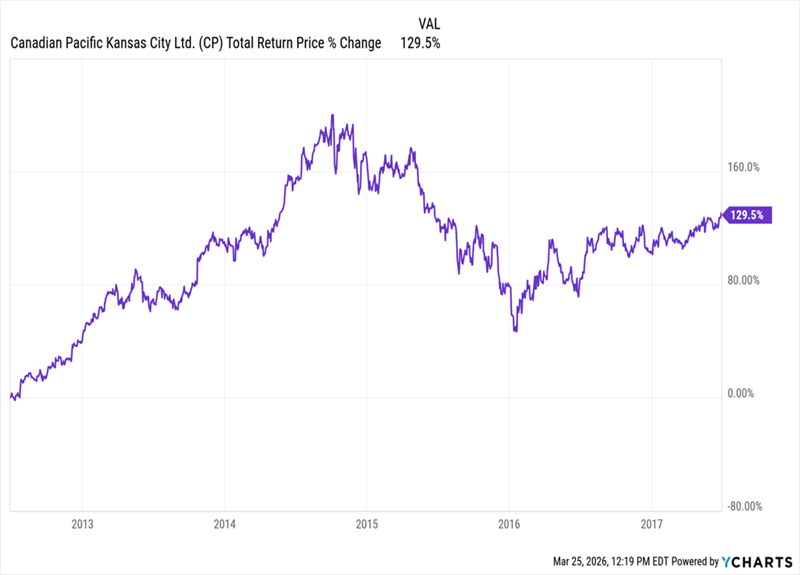

Ackman/CP Was the Classic Activist “Unlock”

One of the most successful activist plays came when Bill Ackman installed veteran railroader Hunter Harrison at Canadian Pacific Railway—now Canadian Pacific Kansas City (CP). Five years later, the stock had more than doubled:

“Classic” Activist Move Ignited CP

But of course, not every activist move is this successful.

Which brings me back to CEFs, and more specifically a faceoff between GAMCO Investors, run by well-known value investor Mario Gabelli, and Saba Capital Management, run by activist investor Boaz Weinstein.

This move, which we discussed in my March 19 article, involves GAMCO aiming to put the vice-president of its Gabelli Utility Trust (GUT) on the boards of two Saba CEFs.

That’s interesting because it’s a bit of a role reversal: GAMCO is more of what I’d call a traditional CEF manager, while Saba focuses more on investor activism.

The question, of course, is: Will adding GUT’s influence to Saba’s funds work?

Last week, we focused more on the Saba funds. Today I want to take a closer look at GUT, which holds major utility and pipeline stocks, like NextEra Energy (NEE), Duke Energy (DUK) and ONEOK (OKE), to see if it’s worth our attention. Then I’ll give you my updated thinking on the GAMCO/Saba situation and my preferred approach to activist moves like this.

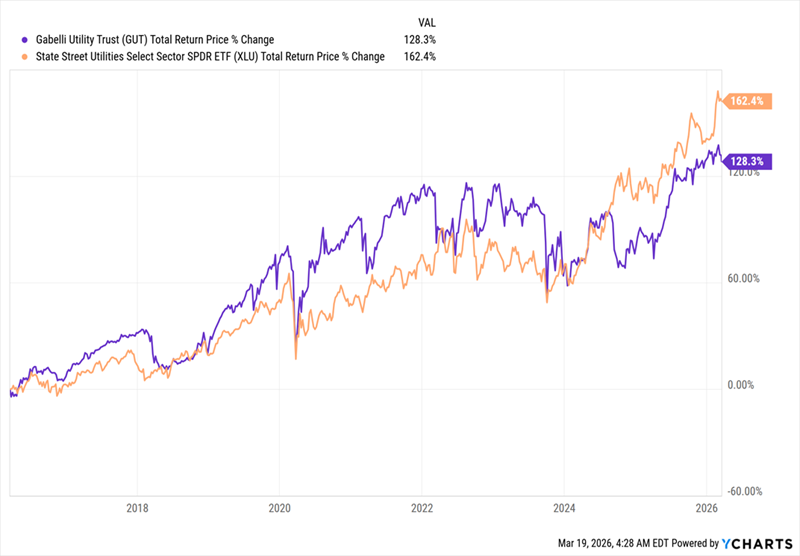

We’ll start with 10%-yielding GUT, whose 10-year total return is shown in purple below.

GUT Gains in the Long Run—But Falls Short of Its Index

In that time, GUT has earned an 8.8% annualized return. That’s strong, but look at the orange line above: As a utilities fund, GUT is best benchmarked to the State Street Utilities Select Sector SPDR ETF (XLU). And as you can see, it has lagged that ETF.

Now, in the case of CEFs, this is often not the fault of the fund manager; Gabelli’s staff are all professional and knowledgeable about markets, after all. And while fees (1.52% of assets, to be precise) could be part of the story, many CEF fees are higher, so that’s likely not the whole reason for the lag here.

Moreover, if you look more closely at that chart, you’ll see that GUT did outperform for a time, so maybe this is just a short-term run of bad luck?

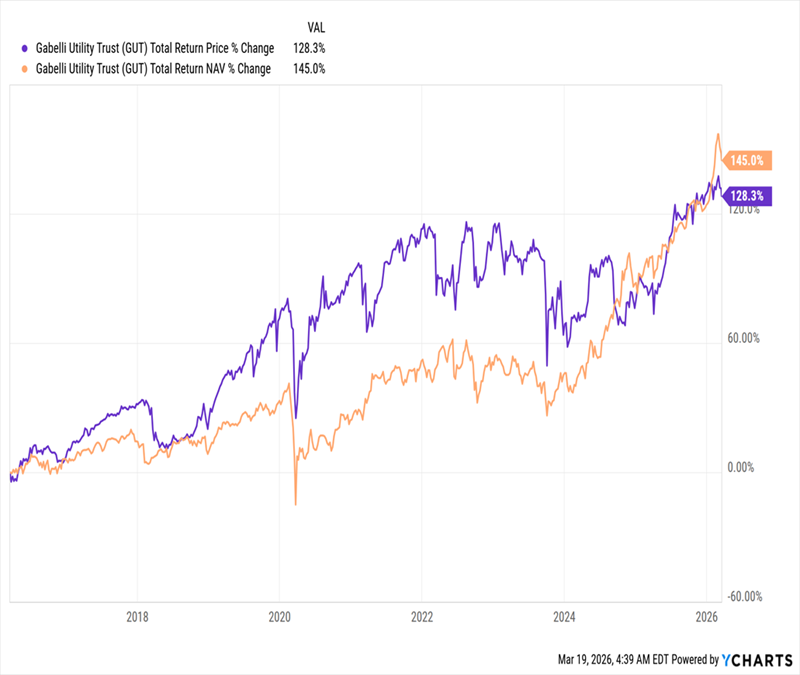

Luckily, CEFs give us a “clean” indicator of management’s skill without sentiment-based swings in a fund’s market price. It’s called the total NAV—or “net asset value”—return, and it’s tied directly to the performance of the fund’s portfolio.

Below we see that GUT’s total NAV return (in orange) did outrun its market price-based return (in purple), but still came up short of the benchmark’s 162% return:

Portfolio Return Improves, But Still Falls Short

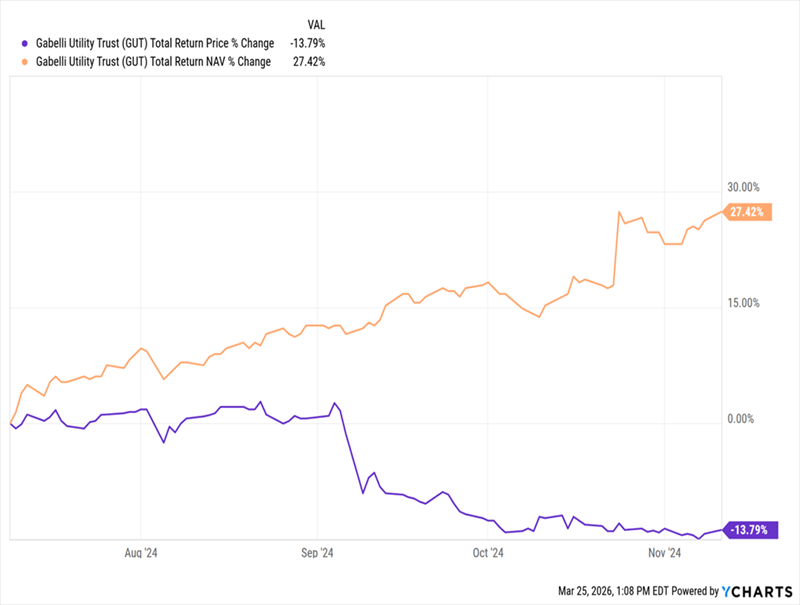

That underperformance is one risk with GUT. The other? The fund trades at an incredibly high premium to NAV—83%, to be exact. Moreover, that premium has varied widely, sometimes topping 100%. The risk here, of course, is that this huge premium collapses. Even a drop to a still-high level of, say, 50%, could entail significant losses for investors, regardless of what management does.

In fact, that’s more or less what happened in mid-2024, when GUT’s premium cratered from around 117% to 52% in four months. The result was a 14% drop in its total return based on market price, even though its total NAV return jumped 27% in that span:

GUT’s Unique Risk: Posting Losses While Its Portfolio Gains

This suggests GUT’s market price performance is at risk due to today’s higher premium. And even if the fund’s team can beat the index on a NAV basis, investors may still lose. So to sum up, I see GUT as a sell now: first because its premium is too high and second because it’s been underperforming on both a NAV and market-price basis.

But What About That Activist Play?

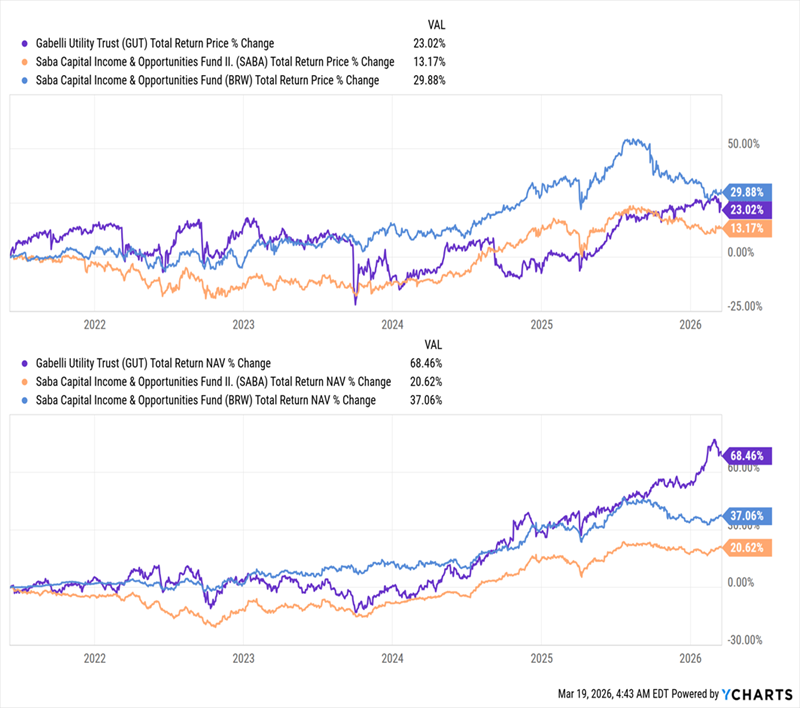

Now let’s go back to GAMCO’s move to put GUT’s vice-president on the boards of two Saba funds: the Saba Capital Income & Opportunities Fund II (SABA) and the Saba Capital Income & Opportunities Fund (BRW). The pitch is that this will help turn these funds’ discounts—both around 13.5% as I write this—into premiums.

But will it? Let’s stack up GUT’s performance with these two funds:

NAV, Market Price Again Tell 2 Different Stories

The top two charts compare GUT (in purple), SABA (in orange), and BRW (in blue) over the last five years. In the top one, we see that GUT has done better than SABA and worse than BRW on a market-price basis. Meantime, GUT has clearly outperformed on a total NAV return basis.

This divergence tells us two things: 1) GUT investors can’t always expect the fund’s returns in the market to flow to them in full. 2) GUT’s management acumen could, in fact, give the Saba funds a boost.

But there’s another factor at play here.

And that is the simple fact that these are very different funds. GUT, as mentioned, holds comparatively steady utility stocks. Saba’s funds, meantime, hold more speculative assets, such as SABA’s position in Alternative Capital Investments Fund III LP (a private fund focused on litigation finance) and the crypto-focused Grayscale Ethereum Classic Trust (ETCG), which is held by SABA and BRW.

That’s a much different proposition than running a utility-focused fund like GUT, and it tells us that even if GAMCO is successful here, it may not benefit investors in SABA or BRW.

How I Prefer to Play Activist Moves

Rather than try to predict activist battles that are already in motion, we aim to get ahead of them by owning the kinds of investments activists target in the first place.

One way to do that is to focus on equity CEFs trading at discounts and managed with an eye toward value. Central Securities Corporation (CET), for example, aims to own shares of undervalued companies generating strong cash flows.

Those include Amazon.com (AMZN), which is cutting costs due to AI and reporting strong sales growth, but has still lagged many of the other Magnificent 7 tech stocks.

These kinds of CEFs offer upside, high—and growing—dividends (CET yields 5.4% today) and value (the fund trades at a roughly 15% discount).

The kicker? The kinds of stocks CET holds are most likely to attract an activist, a takeover offer or other move that could unlock value. These CEFs’ own wide discounts could also attract that kind of attention. That makes focusing on CEFs like these a better way to gain from these kinds of events than trying to guess the next activist target.

These 9.6%-Paying “AI Funds” Are Cheap (and Set to Grab Attention This Spring)

Remember AI? It feels like this revolutionary tech has been lost in the Iran War headlines. But it’s very much out there—quietly blending itself into businesses across the economy every single day.

Cutting costs. Boosting productivity. Generating new leads.

At the same time, shares of AI beneficiaries—both suppliers of this tech and companies using it to streamline their businesses—have been cast aside due to geopolitical headlines. That includes my 4 top CEFs for profiting from the AI revolution.

As I write this, these funds pay an 8.7% yield on average, with the highest payer of the bunch paying a sprightly 9.6%!

All 4 are terrific bargains as the headlines draw investors’ attention to oil. But that won’t last. The time to buy these 4 funds is now. Click here and I’ll tell you more about these 8.7% payers and give you a free Special Report revealing their names and tickers.