Iran War volatility has tossed finance stocks “out with the bathwater.” It’s giving us a nice “second chance to buy” my favorite finance-focused dividend.

That would be the John Hancock Financial Opportunities Fund (BTO), which yields 7.7% today and, as we’ll see, trades at a discount that’s double what most investors think it is.

Why April 2026 Could Be April 2025 Redux (But With a Faster Rebound)

To see why I think the market is making a mistake when it comes to finance stocks, let’s rewind to last year, when stocks sold off on the so-called “Liberation Day” tariffs.

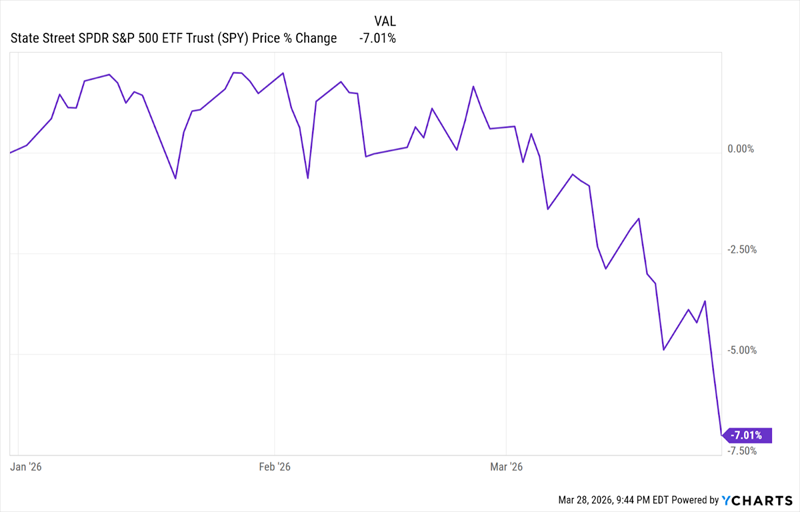

From the Spring 2025 Selloff …

That selloff has actually looked a lot like this one so far, with a similar depth:

… to Its 2026 “Twin”

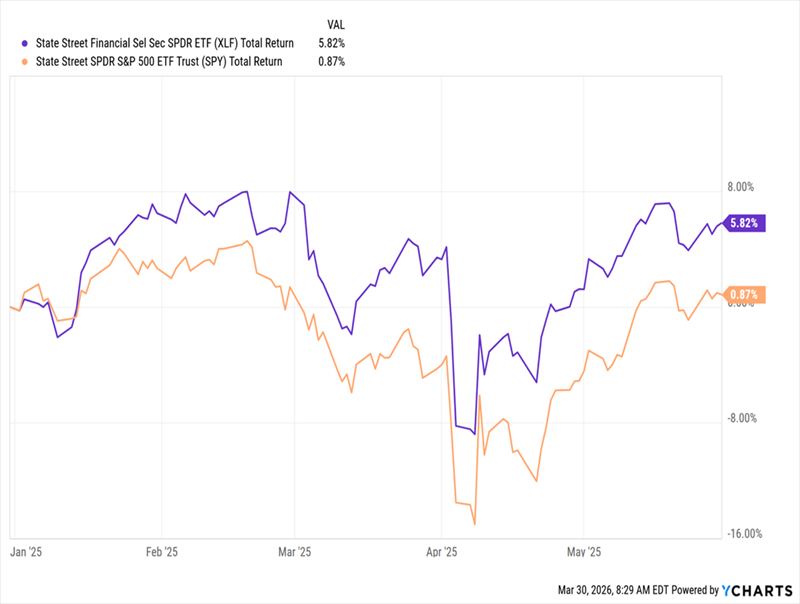

Here’s what I really want to draw your attention to: In 2025, the finance sector—shown by its benchmark ETF in purple below, didn’t fall as hard as the rest of the market, and soared on the other side:

Finance Beat the S&P 500 in the 2025 Plunge …

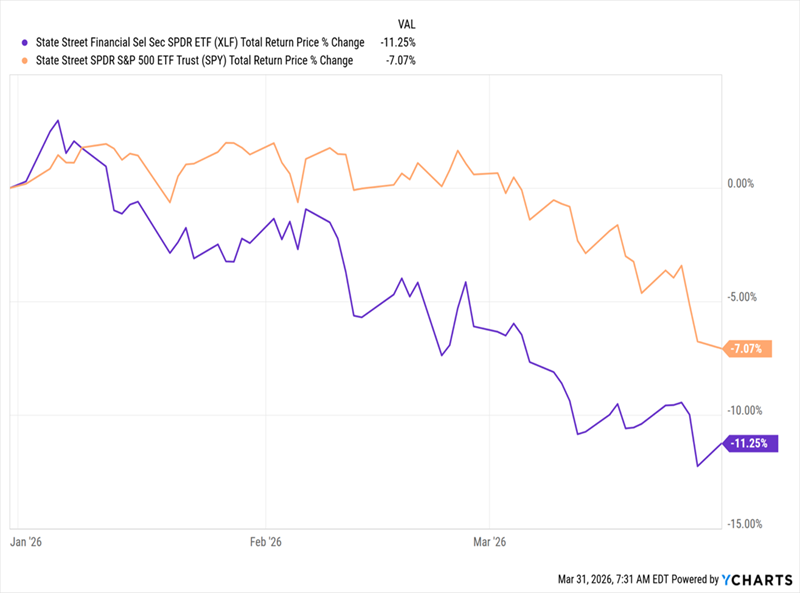

Fast-forward to this year, and finance stocks are being hit harder in the Iran War fallout, falling much further than the market since the start of the year.

… And Looks Like a Coiled Spring This Time Around

That’s excessive, in my view, and positions the sector for a stronger rebound this year. That’s because, at their core, both of these selloffs are about one thing: inflation. Last year, the driver was thought to be tariffs. This year, it’s oil prices.

And last year, it was hard to tell which sectors could win as the administration brought in tariffs on everything from lumber to car parts. This year, it’s easier to peg a winner: oil stocks, which have already surged.

That ship, of course, has already sailed for us, and we never chase trades at CEF Insider. But finance is setting up to be our still-discounted play here, as it’s poised to benefit from two trends stemming directly from the oil-price surge.

First, continued oil-price volatility—almost certain, no matter when the war ends—will drive higher commodities-trading revenue for banks. And if higher oil becomes a “new normal,” oil producers (most of whom are generally cautious about committing to higher production) will eventually expand output—and will of course look for financing to do so.

And then there’s a third angle few investors have even thought of.

Airline-Fuel Hedging Could Be Set for a Comeback

Years ago, airlines used derivative contracts on oil to hedge their exposure to energy prices. Intermediaries (banks, in other words) took a fee for this, alongside other players, like hedge funds. But these programs were expensive to run, so most airlines have wound down their hedging programs over the last decade or so.

But now it seems they’re thinking about doing it again:

“US airlines abandoned the practice of hedging against fuel costs long ago. With oil prices surging following US-Israel strikes ?on Iran, they could be looking at a big bite out of their bottom line in the event of a lengthy conflict that keeps prices elevated for months.”

This March 6 report from Reuters tells us that there may be more demand for options in the future, which is good news for the financial sector broadly.

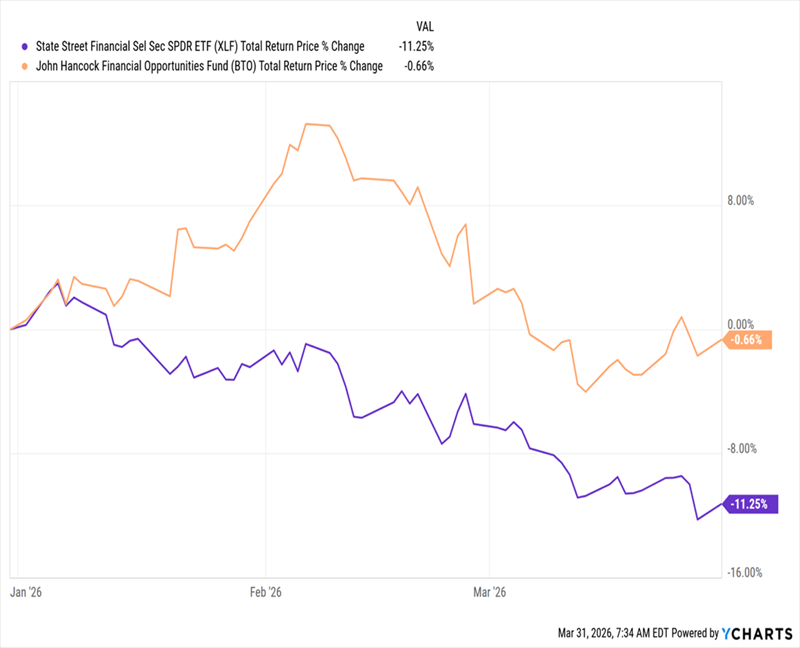

Which brings me back to BTO, which is roughly flat this year (shown in orange below), on a total-return basis as of this writing, compared to the more than 11% decline we’ve seen from the financial sector as a whole:

BTO Falls Less Than Finance …

That’s the kind of resilience we want to see from a CEF in this environment.

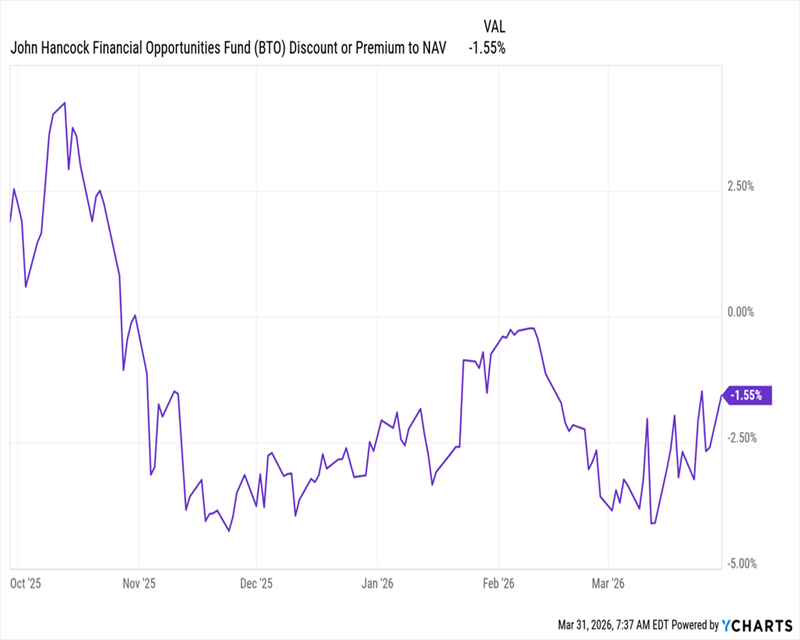

And here’s where things get interesting: Even though it’s held up better than the sector, BTO has remained a bargain by another key metric: the discount to net asset value (NAV, or the value of its underlying portfolio).

… While Keeping Its Discount

As you can see above, the fund now trades at a bit less than a 2% discount. And that discount is actually much larger in real terms, because BTO’s valuation is normally well above par, averaging a 3.9% premium over the last five years. Indeed, you can see in the chart above that it’s fallen from around that level just six months ago.

BTO is also notable in that it holds mainly regional banks, and while they may not be as exposed to things like airline fuel hedging, they stand to gain on improving prospects across the sector as a whole. Those in energy-producing areas are likely to do better, like Hancock Whitney (HWC), BTO’s No. 7 holding, based in Gulfport, Mississippi.

Moreover, regionals let us better diversify across the sector, while keeping our focus on the US, the world’s largest oil producer, which accounts for 95% of BTO’s portfolio.

The fact that regionals have been caught in the downdraft that’s affected the whole sector is an opportunity for us to get BTO at a 7.7% yield and that “larger-than-it-looks” discount. This way, we’re setting ourselves up for higher income and potential gains as that markdown moves back to a premium, where it belongs.

5 More “Tossed With the Bathwater” Monthly Dividends Yielding 9.7%

In times like these, a growing 7.7% dividend can bring us a lot of peace of mind. But the beauty of CEFs is we can get dividends that are even higher—and pay us every month, too.

That’s right in line with our monthly bills, of course. And if you want to reinvest, great! Monthly payouts let you do so even faster.

For all of these reasons (and more!) I’m urging all investors to take a close look at the 5 bargain CEFs in my “9.7% Monthly Dividend Portfolio” now.

As the name says, these 5 funds drop 9.7% payouts (or $4,042 a month on every $500K invested) into your account.

What’s more, these funds sport big discounts to NAV now, thanks to current volatility. That lets us lock in that high average payout and opens the door to future gains as these unusual discounts slam shut.

Time is of the essence here, and I don’t want you to miss out on these high-yielding monthly payers. Click here and I’ll tell you more about them and give you a free Special Report revealing their names and tickers.