Today we’re going to discuss a 6%-paying fund that’s quietly built a portfolio perfectly tuned for the rest of the 2020s.

Few investors realize it … yet. Which is why we can grab this 6% payer (whose payout looks set to grow from here) at a 10% discount to its “true” value.

The fund in question is the Sprott Focus Trust (FUND), a closed-end fund (CEF) managed by Whitney George. He’s a manager you may have heard of: George is known for the profits he’s earned over the decades by focusing on two key areas: energy stocks and small caps.

Source: Sprott Inc.

You can see that reflected in FUND’s portfolio, the top-10 holdings of which are shown above. Familiar big caps are here, such as ExxonMobil (XOM), as well as mid-caps like manufacturer Westlake Corp. (WLK) and smaller fry, like Canadian contract driller Major Drilling Group—market cap: $1.24 billion—and mainly domestic food maker Cal-Maine Foods (CALM), with a $3.75-billion market cap.

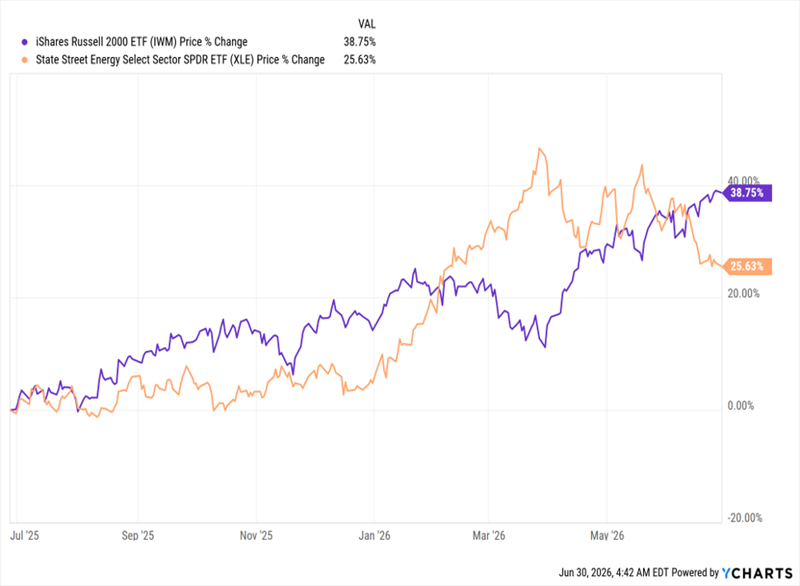

It’s a good time to tilt toward George’s two specialties right now, because the benchmark ETFs for energy stocks (shown in orange below) and small caps (in purple) have been on a roll this year:

Energy Stocks, Small Caps Fly Through the First Half of ’26

When it comes to small caps, shown by the iShares Russell 2000 ETF (IWM), this short-term performance is compounded by the fact that, over the very long term, these companies (again, with IWM in purple below) outrun the benchmark S&P 500 ETF, the State Street SPDR S&P 500 ETF Trust (SPY), in orange.

Big Gains From Small Caps

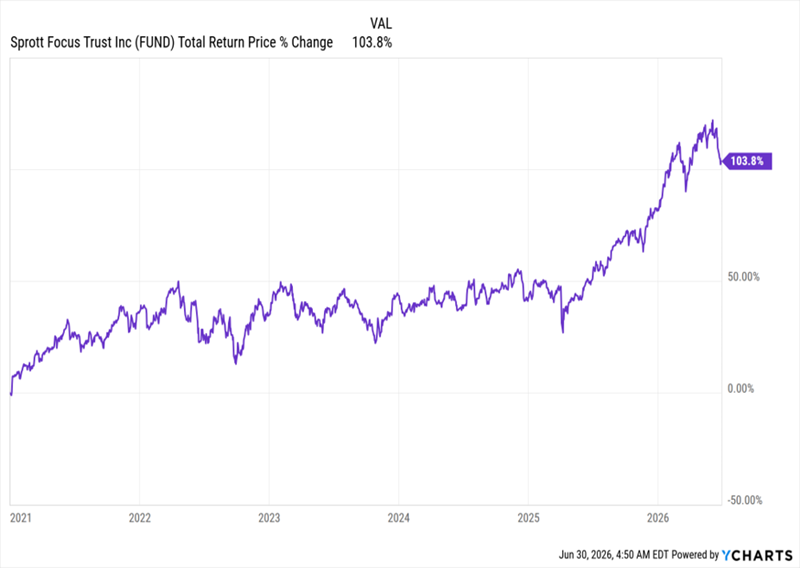

However, this was not true in the 2010s, when the S&P 500 edged out smaller firms. That, in turn, weighed on FUND, until it began to edge higher earlier in the 2020s and really took off starting in early 2025.

FUND Gains Slowly—Then All at Once

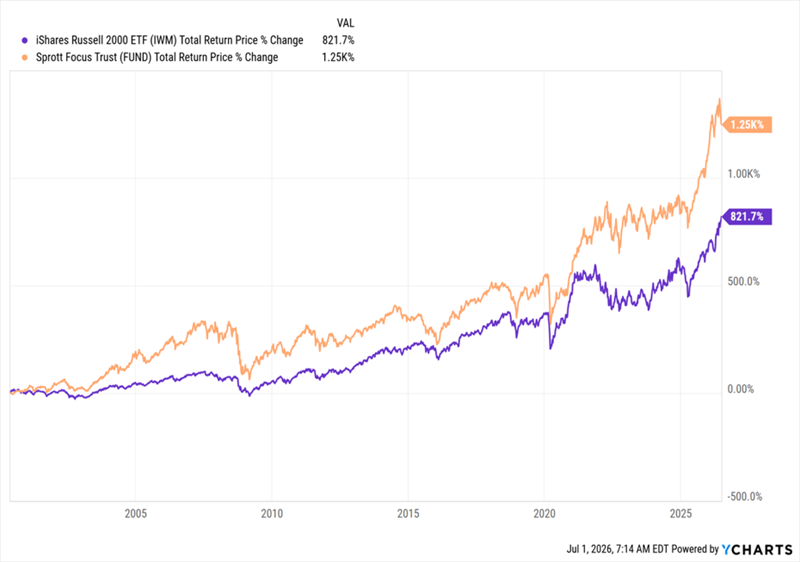

This is a return to form, as George’s fund has been outperforming the small-cap benchmark ETF for a long time. If we go back to when that ETF went public, we can see that FUND (in orange below) has been outrunning it for its entire life.

FUND Crushes Its Small-Cap Benchmark

I expect that performance to continue as small caps return to their long-term dominance over their larger cousins. Moreover, FUND’s mix of small- and mid-cap companies, along with energy stocks, makes it a particularly savvy way to grab energy exposure. That’s because its smaller stocks outperform the benchmark over time, providing some cushion for its more-volatile energy holdings.

The classic case of this in action came during the pandemic, when oil prices, of course, briefly went negative. That was enough to send the energy-stock benchmark to a 50% loss—but not FUND: It only briefly turned negative in that time.

This makes sense: As COVID shut the world down, the focus shifted to more domestic-focused companies that didn’t have to worry about globe-spanning supply chains. Those tend to be small caps.

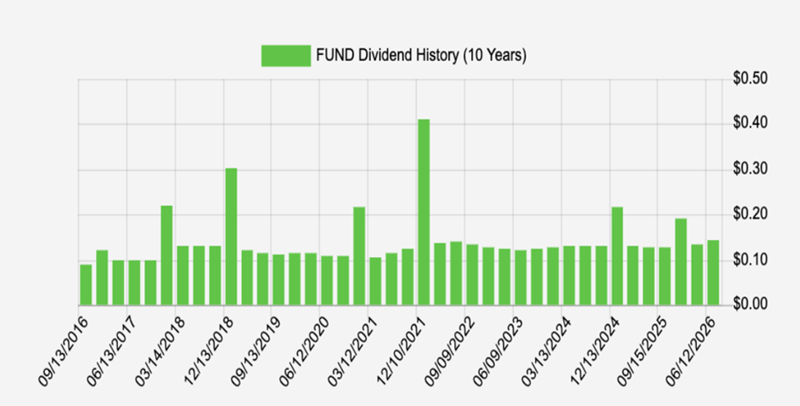

Plus, there’s the income, with FUND paying out that rich 6% payout mentioned earlier.

Source: Income Calendar

Now, 6% sounds like a lot, but remember that FUND has been hiking payouts for a decade now, and handing out big special dividends here and there, too (those are represented by the spikes in the chart above).

These payouts are possible because FUND’s NAV keeps rising, and the fund’s mandate is to pay an annualized rate of 6% of the rolling average of the fund’s NAV over the last four quarters, so a higher NAV will mean bigger payouts.

In other words, since that 6% yield does not account for those special dividends, that yield is best thought of as a floor—and one that’s likely to rise.

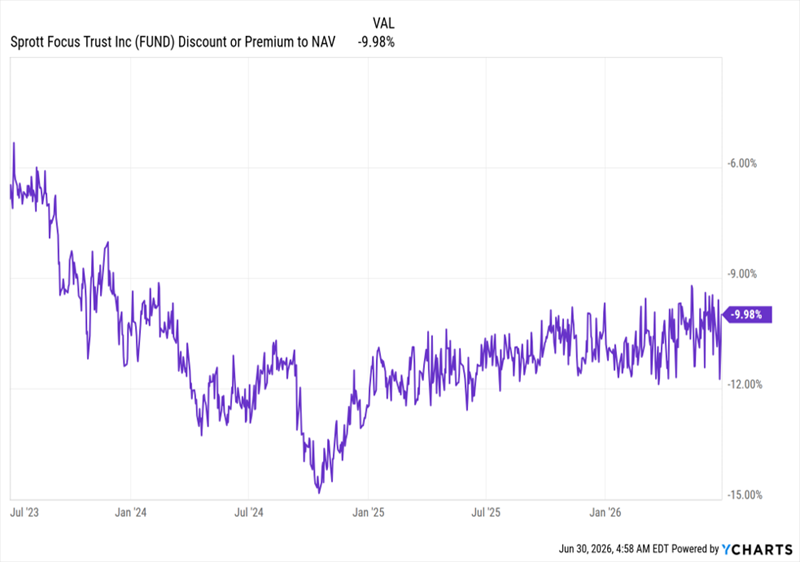

FUND’s Discount Slowly Narrows

This is especially true when we remember that FUND has a nearly 10% discount to net asset value (NAV, or the value of its underlying portfolio), but that discount bottomed out in mid-2024 and is now slowly moving back toward par. However, it’s still below the 9% level, so it may be some time before the markdown truly shrinks and we get some “closing-discount” gains on top of those generated by the fund’s portfolio.

But that’s fine. Because that 6% yield is safer thanks to this discount, since it also means management needs to earn just a 5.5% total annualized return on the NAV to sustain the 6% dividend yield, which is calculated on discounted market price.

The story gets even better, since FUND’s total NAV return over the last three years is 14.4% on an annualized basis, or nearly triple what it needs to sustain payouts. No wonder George has tossed out so many big special payouts over the last few years.

This also suggests that more such payouts are on the horizon. This fund is worth considering before the next one is announced, which will likely cause the discount to shrink further—and propel the price higher as it does.

These 5 Overlooked Funds Pay Dividends 60 Times a Year, Yield 9.7%

Buy FUND today and I expect you’ll be looking at a much higher yield than 6% on your original buy in just a few years.

But you don’t have to wait that long. I’ve got a “60 Paycheck” Income Plan that will pay you a lot more than 6%—a 9.7% yield, to be exact—starting in just a few weeks.

This unique income stream is generated by 5 monthly paying funds that, between them, yield that rich 9.7% on average.

With one payout from each of them every month, you’ll be grabbing 5 “paychecks” every 30 (or 31) days here—or 60 payouts a year! Plus these funds are cheap now, putting solid upside on the table.

Now is the time to buy these 5 unique monthly payers. Click here and I’ll tell you more about them and give you a free report revealing their names and tickers, so you can collect your first monthly “paycheck” within weeks.