We received many thoughtful questions after last Wednesday’s “options for income” editorial. (If you missed the original piece, you can read it in its entirety here.)

Many of you are understandably interested in my favorite strategy for generating thousands of dollars in extra income each month regardless of what happens with the S&P 500. After all, it’s a great time to consider alternative cash flow options that don’t depend on this bull market motoring ahead for many more years.

So if you’ve dabbled with the idea of selling options for income, and you’re not exactly sure how to get started, I hope this discussion can help you get started with this excellent (and safe) income strategy.

Q: What amount of capital do you need to generate meaningful income by selling options?

Most stocks and funds that pay 10% or more are dangerous buys. Which means, if you require double-digit yields to fund your income needs, you’ll need to do something different.

I’ve found it is possible to generate 15% to 20% cash returns annually by selling put options on high quality dividend payers and growers. This means a $100,000 portfolio will net you $15,000 to $20,000 per year. A million dollars devoted to this would pay you a sweet $150,000 to $200,000 or more per year.

Q: Does that need to be all cash, or can I use margin?

It’s possible to use margin – but I don’t recommend it.

Why? Mostly because it’s not necessary. If you can generate 15% to 20% safely, why pile more chips on the table than you have in your pocket?

When we sell put options for income, our goal is to generate 15% to 20% in all market environments with minimal downside. This means keeping enough cash on hand to buy shares outright if they are “put” to us.

Q: What happens when the stock price dips below the option’s strike price?

When we sell puts, we are giving the buyer the option to assign us the shares at any time. They have the right to take our shares off our hands, but they’re not obligated to.

In most cases, options are not exercised until they expire. Which means if you sell a put option next month, and the stock drops below the strike price, you won’t be assigned shares unless they remain there through the option’s expiration.

Q: How often do you have shares put to you?

Speaking from experience, my Options Income Alert subscribers have been assigned shares less than 20% of the time. Which means more than four out of five trades have expired worthless – good news for us as options sellers because it means we keep the income free and clear.

This “assignment rate” is heavily dependent on the particular strategy being used. In my case, I’m employing a conservative strategy that targets 15%+ annual returns.

It’s possible to target higher returns and premiums, but that usually means more assignments. Meanwhile an even safer strategy could increase that initial “win rate” even further, but it would likely mean lower returns.

When shares are assigned, it’s not the end of the trade either. From there, I usually sell covered calls on the new shares (which were purchased at a discount already) to generate more income.

Q: Would you please explain covered calls? What are the mechanics?

Covered calls are the other side of the coin from puts. Here, we are selling the stock’s upside in exchange for income. When shares exceed the call’s strike price, they are “called away” from us at that price (again, usually when the call expires). We get to keep the price gains up to the strike price, plus the call premium that we collected.

Q: Would you ever sell a position outright instead of selling a covered call against it?

Unless the story changes, I will sell a covered call. After all, this is a stock we wanted to own anyway – and we were now able to buy it at a discount. There’s no reason to sell. Why not hold while selling covered calls to keep the income stream going?

The exception would be no longer wanting to own the stock. If the story changes, then it’s best to just sell the shares and move on to the next trade.

Q: Do we need to worry about earnings announcements (since this increases volatility)?

There’s a tradeoff for options that span an earnings announcement. Because this event has the potential to send shares higher or lower, option premiums tend to be higher.

Being a conservative practitioner, I usually avoid earnings announcements. It’s easier to bank premiums and watch option prices decay without drama. No news is good news.

That said, everything should be considered on a stock-by-stock basis, and there are exceptions.

Q: How are dividends handled? Do I owe them when selling puts?

Us put sellers are “dividend neutral” – we don’t owe the dividend (as short sellers do).

If we are eventually put shares, we will then be “long” the stock

Q: What is your recommended options trading platform?

Any online broker is fine. Most likely, however, you’ll need to complete their options application.

It’s a form that’s supposed to make you aware of the fact that options are “risky.” Of course you’re not going to be buying options, which is the dodgy side of these trades.

No matter, a completed agreement is required to buy or sell. If you have trouble locating your broker’s options section, give them a ring and ask them to email or snail mail you a copy of their options agreement.

Q: This all sounds too good to be true. What is the real downside risk, and how do you protect against it?

By selling put options, we are already reducing our risk. Would you rather buy stocks at full price, or at 3%, 4% or even 5% discounts?

The key is that we’re only selling puts on stocks that we’d be happy to own anyway. This means we either keep the premium free and clear, or we get to buy at a bargain price.

Trades can be spaced out to normalize for market volatility. Rather than selling a bunch of puts at once, sell them at normal intervals (ie. weekly). It’s the equivalent of dollar-cost averaging on the buy side.

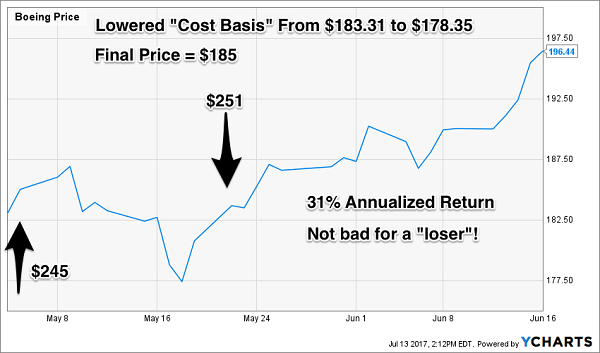

Also when shares are assigned, covered calls can help further reduce your cost basis. And the lower you can drive your cost basis via cash you collect now, the lower your risk.

Here’s an example featuring Boeing (BA). By lowering our cost basis by nearly $5 per share, we were able to turn an initial “loser” into a 31% annualized gain.

Q: Can you share your historical trades and track record?

Since inception, my Options Income Alert subscribers have averaged an annualized 18.6% return per trade. We’ve been generating cash flow every week from the options market for more than two years. Our 109 trades-to-date have navigated two sharp pullbacks (including our current one) successfully.

Our historical trades and current open trades are available to paid subscribers. You can take advantage of our current 60-day risk-free trial by clicking here and scrolling down to the bottom of the page.

If you’re interested in following my trades and “options for income” strategy, please don’t delay. We only open up this service a few times each year. This window will be shutting down shortly, and I’m not sure when my publisher will re-open the service. We cap our subscriber count so that everyone has the opportunity to execute the trades I recommend.

I’ll be emailing out our next income next week. Don’t miss it! Click here to be added to our Options Income Alert email list now.