“Merci beaucoup,” your dividend strategist said as he handed three suitcases to his to-the-Paris-airport Uber driver. (I was very proud of myself. Eight days and basically Parisian…)

“Francais?” the driver called my bluff.

“Ah no,” I admitted, hands up, waving off the offer. “She does!” I quickly scapegoated my wife. Who, to her credit, speaks French reasonably well. But the driver was flying with his urgent ask.

Fortunately for phones. She didn’t know what he was asking either, but his phone was translating into English in real time:

There is a bug in my application. Can we cancel the ride?

Then he punched a number into a calculator. 90.

I assumed two things:

- He was asking for 90 euros, which was a better deal than the $118 USD Uber had just quoted me. According to my in-head exchange rate.

- The “bug” was Uber’s cut from a lucrative airport ride. Our driver wanted to keep the entire fare. Fair enough, monsieur!

“Oui. No problem,” I replied, using my best French accent for problem. (Why? I have no idea.)

Jacques canceled the ride on his end. I canceled my Uber on mine. All good. Until 56 minutes later as we pulled up to CDG Airport and I checked my Uber app:

You have been charged $118. Please rate Jacques 1 to 5 stars.

Uh oh. Here we go. I showed Jacques my screen. He had no clue what I was getting at, so we tag-teamed it back to his translate app.

“No, it is impossible,” he said with confidence, pulling out his I’ll-take-your-credit-card-now machine. “Im-po-see-bleh.”

OK, well—mentally I was doing the math. Worst case I was out another 90 euros if I had to double pay to get my family off the scene gracefully. Not great but po-see-bleh. A pricey lesson, though not one I expected to receive in a legitimate tourist hub like France.

Fortunately, Jacques was right. I checked my Uber history—no charge. The completed ride confirmation was also a bug. (Ha! What are the odds?!) I handed him my credit card and capped the exchange with my go-to line:

“Merci beaucoup.”

Two bugs in one transaction. One imagined (let’s be honest) and one real. The latter was fixed with further investigation.

Which dovetailed right into my 9.5-hour airplane work session. (No movies for yours truly on the return flight!)

First up, our boy the “Bond God” Jeffrey Gundlach just made a scene at a very public investing conference. He blasted semi-liquid private credit funds, the $1.5 trillion corner of Wall Street that financial advisors have been quietly stuffing retirees into for the last few years.

Gundlach chastised them for only being liquid when you don’t need the money. He even compared today’s setup to the dot-com bubble and the pre-GFC mortgage market.

Real financial “system bug?” Or imagined? Let’s discuss what it means to be “semi-liquid.” (Hint: It’s a little sketchy.)

Apollo Debt Solutions (ADS) is one such semi-liquid fund. With $14.7 billion you might suspect ADS would be plenty liquid, but you would be wrong. The fund received redemption requests for 11% (!) of its outstanding shares in Q1. Apollo capped withdrawals at 5%, though, and shareholders got back about 45 cents on every dollar they asked for. The rest stayed locked in the fund. Im-po-see-bleh, management said when asked for coin.

This is exactly what Gundlach railed about. The money is available when times are good and when they’re not, you can claim 45 cents on every dollar you rightfully own. Yikes.

Another offender is Blue Owl Tech Income Corp (OTIC). This $6 billion fund had a good thing going, lending to high-margin software companies. Then, AI came along and brought competition to business apps that previously enjoyed competitive moats—and high subscription prices. New coding tools allow non-developers to “vibe code” apps from scratch, which means they can dictate to the AI what they want their app to be and essentially “vibe” their way to a product. Very cool for the user, and quite problematic to the entrenched software vendor.

The entire software sector fell out the window earlier this year on vibe-coding concerns and investors asked for their money back. Requests totaled nearly 41% of all shares outstanding! No way enough buyers would satisfy that selling demand. The fund looked dead…until management pointed to a 5% cap on redemptions. (“So long, suckahs!”—The Management)

Cliffwater Corporate Lending Fund (CCLFX), the biggest of the trio at $32 billion, delivered the biggest dividend disaster. Investors asked for 14% back, the fund honored 7% and then cut its payout by 11.3%. At which point, on cue, S&P Global Ratings revised Cliffwater’s outlook to Negative. (Analysts and ratings agencies love piling on.)

The headlines are ugly. And yes, Gundlach is rightfully hyperventilating about these offenders, but there are some perfectly good payout babies in this bathwater.

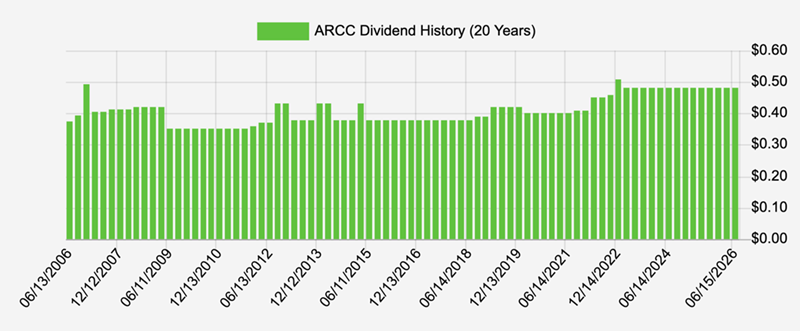

Ares Capital (ARCC) is the largest business development company—private lender to businesses—on the public market. What separates ARCC from the sketchier lenders is disciplined underwriting that’s passed every down-market test since 2004. Their non-accruals—loans where borrowers stop paying—have averaged 2.8% since the Great Financial Crisis.

The BDC industry averages 3.8% non-accruals, so ARCC’s advantage of 100 basis points has compounded sweetly over 22 years. ARCC has only cut its dividend once, in 2009, when the entire credit world was on fire. The team marked their book to its new cheaper reality, trimmed the payout from $0.42 to $0.35 and resumed growing it when the world settled down. Today’s quarterly sits at $0.48—the highest in the company’s history. ARCC yields a terrific 10.6% today.

The Great Financial Crisis is Barely a Blip

(Note: ARCC has paid periodic special dividends on top of its regular quarterly payout. Hence the mini spikes above.)

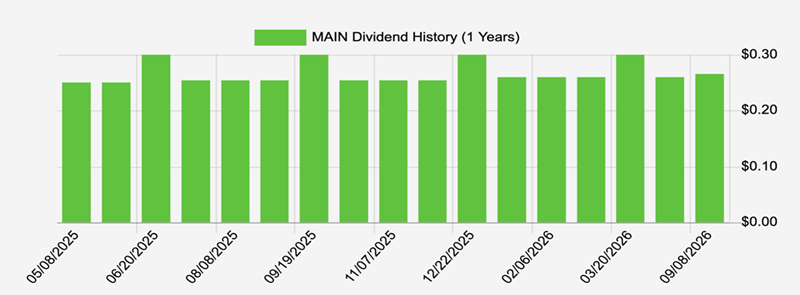

Then there’s Main Street Capital (MAIN), our monthly-paying BDC. We added it to our Contrarian Income Report portfolio in May 2025. Subscribers have collected $4.27 per share in dividends in twelve months. Add in some price gains and they’re up 13% from this income machine which oh, by the way, yields an elite 8.2% including special dividends.

And while everyone in semi-liquid private credit land cuts payouts and slams gates, MAIN celebrates Opposite Day, growing its monthly dividend without a break since the 2007 IPO. What’s MAIN’s secret? Equity stakes.

MAIN doesn’t just lend money. It takes equity positions alongside its debt in many deals. That dual-engine structure is unusual among public BDCs. ARCC, for example, focuses on senior secured first lien loans. They collect interest, period. MAIN collects interest and shares in the upside when its borrowers thrive.

In 2025, those equity stakes threw off $77 million in realized gains plus $150 million in fair value appreciation. That’s the source of the monthly dividend growth and the periodic special dividends on top.

Plus, the folks running MAIN do something crazy. Insiders own 4.11% of the company, roughly 3.7 million shares. They run the place like they own it, because they do! You just don’t see this in BDC land.

1 Year of MAIN Monthly Divvies

ARCC and MAIN don’t have bugs. They’ll give you your money back anytime. But why would you want it, when you can leave it with these dividend machines that keep that wealth compounding.

This is exactly the kind of distinction that separates safe income from dangerous income. Contrarian Income Report readers received both ARCC and MAIN with full underwriting analysis, buy-up-to discipline and the framework to know which “private credit” funds they should never touch.

When the next semi-liquid PC fund cuts, gates, or marks down—and there will be a next one—CIR subscribers will keep cashing their dividend checks!

Plus, most of these payments arrive every 30 days—click here to learn about my favorite Monthly Dividends up to 11%.