At times like these, with the economic outlook uncertain and volatility likely, we want to be certain of one thing: We’re still in stocks (and stock-focused funds)! But of course, we want to make sure we’re tempering our risk, as well.

Because one thing we can be sure of is that any volatility, no matter if it’s tied to an election or any other outside event, will pass. The last thing we want is to be out of the market when it does. (And of course, we want to keep our dividends rolling in, especially in volatile times.)

That brings me to what I want to discuss today—two things, actually.

The first: The fundamentals backing the stock market now (which matter more than anything we’re reading in the headlines). The second: How we’re going to diversify and not only maintain our income stream in the months ahead—but build on it.

Stocks Are Elevated, But Fundamentals Back the Bull

The S&P 500’s surge this year is on its own a clear indicator that stocks are expensive. The index’s price-to-earnings (P/E) ratio confirms it, at around 27 times earnings (over time, anything above 20 is considered pricey).

Is a further breakout possible?

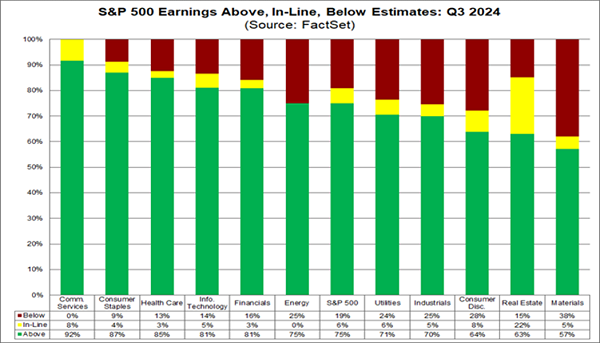

Sure. Because no matter what happens in the next few months, the fundamentals of the economy—and businesses—are strong: Public companies have seen their earnings grow a healthy 5.1% in the third quarter. And according to FactSet, three-quarters of reporting companies have posted earnings above estimates.

As you can see above, earnings gains are strongest in communications services, consumer staples, healthcare, information technology and financials.

That’s a key thing to keep in mind because these are among the more consumer-facing sectors. Meanwhile, firms that provide basic commodities needed for life—industrials, real estate and materials, specifically—aren’t seeing their earnings rise as much.

This typically indicates an economy where companies are growing earnings through rising demand, rather than by having a hold on the country’s infrastructure, which was the case in the post-pandemic years, when these firms had a lot of pricing power.

However, note that fewer than half of consumer-discretionary firms saw sales growth ahead of expectations, showing there is some weakness in the economy. Even so, we’re a long way from that becoming a major issue.

The bottom line is, we’re seeing a mixed picture here. Which means we’ll probably see more market volatility as bits of bad news pop up here and there, offset by the momentum we’re seeing in stocks.

That, in short, leaves us with a clear strategy: Profit from companies’ growing margins while lowering our exposure to the volatile price movements of those firms’ stocks.

That road leads in one direction: toward bonds—particularly high-yield corporate bonds.

The Bond Connection

As I write this, corporate bonds are yielding around 4.7% on average, with high-yield corporate bonds averaging around 7.1%. And as we just discussed, companies’ sales and earnings are rising. Meantime, corporate-bond default rates are falling and are projected to fall further. Those two strengths cut our risk here.

And the high-yield bond market is showing us something very different from the stock market this year:

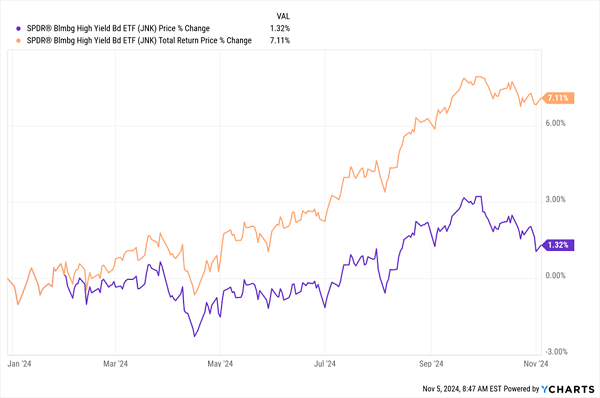

Strip Out the Income and High-Yield Bonds Are Moving Sideways

As you can see in purple above, high-yield corporate bonds, as shown by the market price–based performance of the benchmark SPDR Bloomberg High Yield Bond ETF (JNK), are barely up this year. (Note that this excludes the ETF’s 6.6% yield—the orange line is the ETF’s total return, including that payout).

That more-or-less sideways movement is surprising, since the Fed is cutting interest rates, and lower rates generally mean higher bond prices. Yet the market isn’t pricing those bonds higher in 2024. This is an opportunity for us to get into an underpriced asset class that benefits from the still-strong economy while complementing our exposure to the S&P 500.

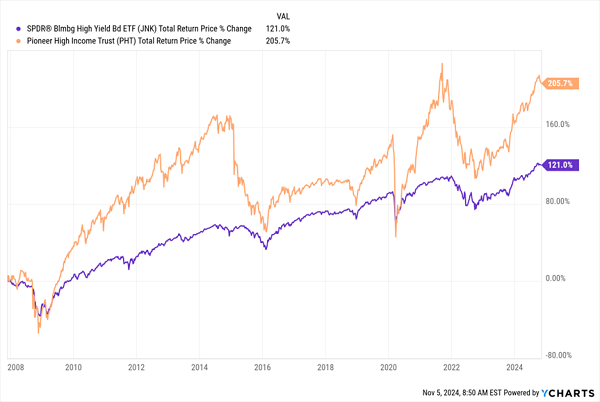

Our favorite way to boost our bond holdings—and get an even higher yield than the index fund—is through CEFs like the 8.5%-yielding Pioneer High Income Fund (PHT). This fund gives you instant diversification through the CEF’s 313 bonds from various issuers across the market. And it’s crushed JNK on a total-return basis since the ETF’s launch in November 2007:

PHT Beats the Index

That’s in large part because PHT is an actively managed fund. And in the cozy world of corporate bonds, this is a big asset, since personal connections matter—and are critical to getting in on the best new issues. JNK and its ilk simply can’t match that edge.

PHT’s portfolio also has an effective duration of 2.54 years, which gives it plenty of time to maintain payouts as rates fall, so its dividend-coverage ratio should stay strong.

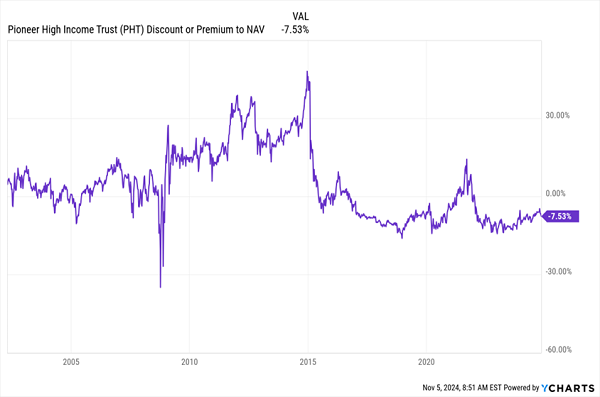

And yet, PHT is undervalued now, trading at a 7.5% discount to net asset value (NAV, or the value of its bond portfolio) as I write this.

Outperformance, a High Yield … and a Big Discount?

Although corporate bonds are paying out more reliably, with higher yields, PHT has a bigger discount than it’s seen for most of its history, including the aftermath of the pandemic and the subprime-mortgage crisis. In today’s strong economy, where more firms are paying their bills on time, this makes no sense.

PHT is just one of many bond CEFs in this position now, so if you’ve been holding off on boosting your allocation to them (and many investors typically do, as they see stocks as less complicated than bonds), now is the time to reconsider.

If stocks take another tumble (and bear in mind that the S&P 500 did erase roughly half of its 2024 gains this summer before bouncing back), bonds can be a lifesaver, providing a solid income stream to get us through volatility. As more investors realize this, they’ll likely bid up PHT to the kind of premiums it saw before the pandemic.

Urgent: Buy These 5 “Safety Net” Funds Now (for 10.5% Yields, Monthly Payouts)

At times like these, stocks and funds that pay dividends MONTHLY give us even more peace of mind than those that simply pay a high yield alone.

Sure, monthly payouts roll in along with our bills, and that’s a very good reason to prefer them. But more importantly, it’s just plain comforting to have that reliable payout coming your way every 30 (or 31) days, rather than having to wait for 90 or more. Especially when the markets are roiling beneath our feet.

That’s why NOW, with so many things seeming uncertain, I’m pounding the table on a diversified collection of 5 CEFs that pay us every single month. And they yield an outsized 10.5% too.

Think about that for a second: Every year, we’re earning more than 10% of the value of our upfront investment in these funds in dividend cash. And that comes our way in the form of reliable payouts that drip, drip, drip into our accounts monthly.

The time to buy these 5 monthly paying CEFs is now, while they’re still bargains. Click here and I’ll tell you more about these 5 “Gibraltar-like” income plays and give you a free Special Report revealing their names and tickers.