Utility stocks have been on a roll as more people come to see them as a way to play AI’s bottomless power demand.

Let me say off the top that this does not mean the “AI-power trade” is played out. Far from it.

But it does mean we need to pick our spots when investing in the sector. To that end, I’m going to give you my two-part strategy on how to approach utility stocks now.

The first part: We go with 8%+ paying closed-end funds (CEFs) to play this sector. There’s a simple reason for that: Utility CEFs pay far higher yields than individual utilities or ETFs.

Second, we’re going to time our moves into utility CEFs to make sure we get these trades right—getting in when value is highest and making our exit when things get overheated.

The best way to show you how this works is to put our strategy in play by stacking up two of the most popular utility CEFs out there (and “popular” is relative, given that the CEF market as a whole is often overlooked).

We’ll walk through each to see which is the better buy—and most importantly, when.

2 Utility CEFs, 2 Big Differences

Our two CEFs are the 10%-paying Gabelli Utility Trust (GUT) and the Duff & Phelps Utility and Infrastructure Fund (DPG), with a 6.3% yield.

Both funds, as their names say, hold critical utility and infrastructure stocks. GUT, for example, leads off its top-10 holdings with Florida-based NextEra Energy (NEE), while also holding fellow large-cap utilities like Duke Energy (DUK) and pipeline operators such as ONEOK (OKE).

DPG holds a similar combo, with a lot of overlapping names in its top-10 holdings. Both funds also focus mainly on the US, with 73% of DPG’s portfolio located here, and 79% of GUT’s holdings.

So, at this point, GUT seems like the better play, right? After all, if you’re getting similar portfolios and similar geographic breakdowns, why not just go for the fund with the higher yield?

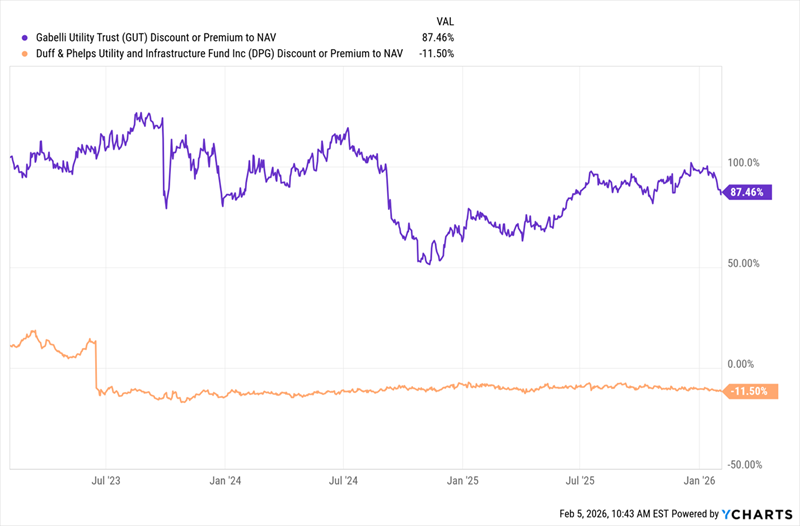

This is where valuation comes in—and here, the differences between the two funds are stark. As I write this, DPG trades at an 11.5% discount to NAV. GUT? An 87% premium!

In other words, investors are paying nearly double what GUT’s portfolio is worth to buy in. That, in one snapshot, is the persuasive power of a 10% payout.

DPG’s Steady Discount, GUT’s Massive Premium

On the surface, then, GUT looks risky: Buy an 87% premium like this one and you’re facing big losses if, say, that premium goes back to par.

But there’s more to the story. Because as you can see above, back in late 2024, GUT traded at a still-large (but much smaller than today) 50% premium before popping back to today’s level. Now, even at a 50% premium, most investors—understandably—would have been put off.

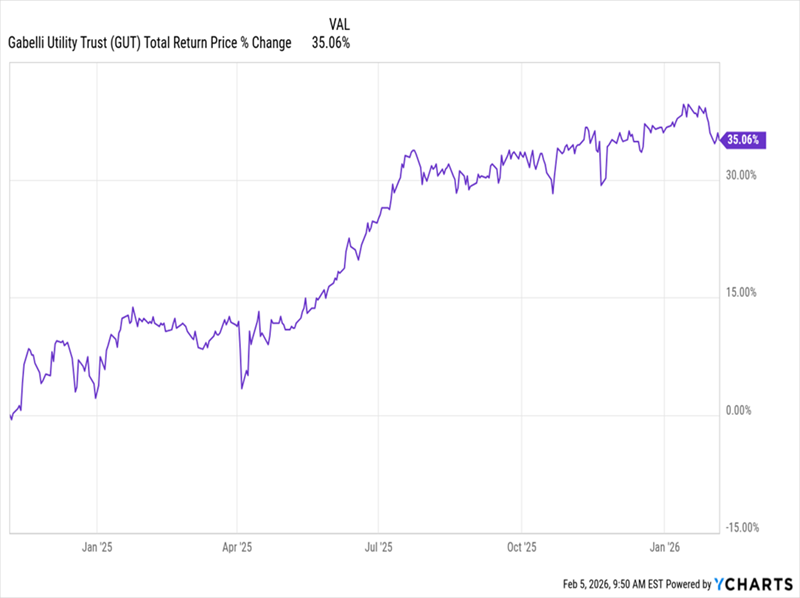

That said, If you’d bought back then, you’d have booked a tidy 35% return up to the time of this writing, even as you bought a “pricey” fund:

The Right Timing Maximizes Profits

Meantime, anyone who bought GUT just four months earlier, when its premium hit its highest level of 2024, would’ve ended up with just a 15% return.

In other words, even an “expensive” CEF can be a smart move if you buy when its premium is at a low point historically.

Keep in mind that, whenever our hypothetical investor bought GUT, they collected that same high yield during their holding period. So they were getting capital gains and a reliable income stream while they waited for their price gains to roll in.

DPG, on the other hand, saw its discount stay more or less static for years, as we saw in the first chart above. That means DPG investors have not had the same opportunity to “swing trade” an ever-changing discount for additional gains. That’s not the only reason why I see GUT as the better utility CEF of these two.

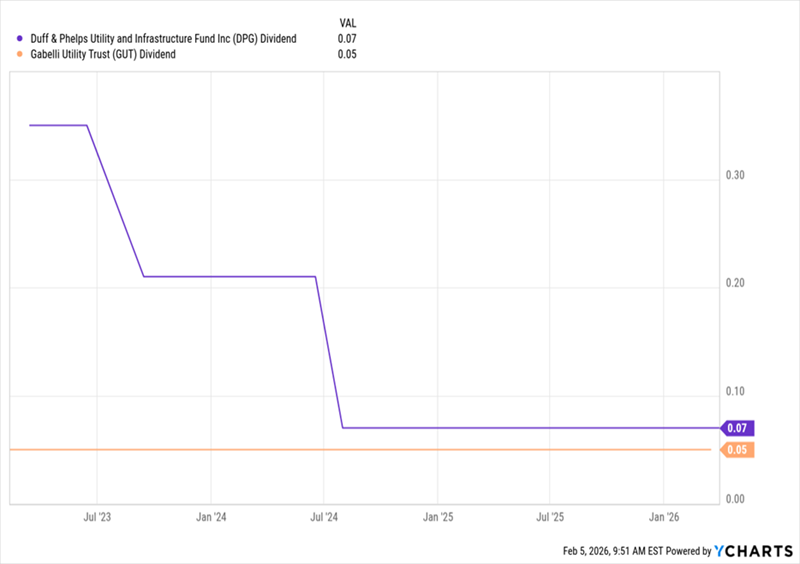

A comparison of the two funds’ dividend histories reinforces my view:

A Falling Dividend Versus Steady Payouts

DPG’s dividends (shown in purple above) have been cut twice in the last three years, while GUT’s payouts (in orange) have been steady. So we can forget about the oft-repeated idea of a double-digit payout being unreliable. As you can clearly see, DPG’s dividend is far shakier, even though it yields a much smaller 6.3%.

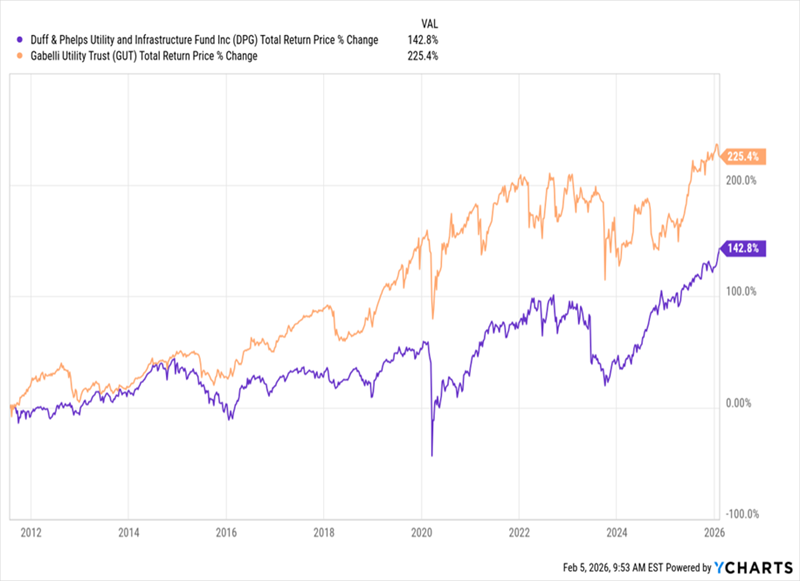

Now let’s do the ultimate test and look at total returns.

Big Gains With GUT

This chart answers the question of why GUT’s premium is so big. In the long run, the fund’s return (in orange above) has soared past that of DPG (in purple), whose persistent double-digit discount makes total sense in light of that.

Where does all this leave us, then? With two conclusions:

- A long-term investment in GUT is a great way to invest in utilities while getting a high, steady income. But …

- GUT’s premium moves around a lot, giving us opportunities to “time” our entries and exits. Now is clearly not the time to buy GUT. But it is a good time to put the fund on our list and consider it when that 87% premium drops in half (or further).

All of this goes to show how powerful a discount to NAV—when viewed in context with that discount’s past movements—can be for generating strong gains in CEFs.

And while we wait for GUT’s premium to fall from the stratosphere to, say, the upper atmosphere, we’ve got plenty of other CEFs to pick from that trade at unusual discounts and pay healthy 8%+ dividends, too.

4 “AI Funds” We Can Play for Closing Discounts—and Big Dividends—Now

Among those are 4 other funds that get us in on AI’s explosive growth at big discounts that are truly unusual—and primed to snap back when the crowd catches on.

And I see that happening sooner rather than later.

Meantime, they pay 8% on average, and the dividends and discounts aren’t the only things that stand out about this quartet.

They also hold shares of both AI developers and users. That last group is key because they’re set to reap the biggest gains as AI cuts their costs and boosts their sales.

These 8%-paying funds are ripe for buying now. Click here and I’ll walk you through them and give you a free Special Report revealing their names and tickers.