Trump 2.0 is now only a bit less than a week off, and things are moving fast.

Here’s one thing I can tell you: While everyone’s talking about tariffs, Greenland and the Panama Canal, what investors—particularly dividend investors—should be talking about is way more “boring”: The yield on the 10-year Treasury note.

Because when the rubber really hits the road on the new administration, it’s the 10-year, more than anything else, that’s going to call the tune here.

And the next move I see it making, which we’ll get into below, is poised to benefit some of our favorite income plays: real estate investment trusts (REITs). We’ll reveal an oversold ticker to target below.

“Don’t Fight the Fed”? Nah. More Like “Don’t Fight the 10-Year”

Lots of people on Wall Street will tell you to not “fight the Fed.” I’d change that slightly, to “Don’t fight the 10-year Treasury rate!”

Point being, investors who are able to smartly read the room and deftly move into (and out of) bonds and “bond proxies” as the 10-year Treasury rate ebbs and flows in the years ahead stand to bag a windfall (and big dividend payouts, too).

Just ask Jay Powell, who’s finally starting to get the picture here.

Truth is the bond market has been tapping Jay on the shoulder for months now. Its message: “Slow your roll, buddy. The job on inflation is not done.”

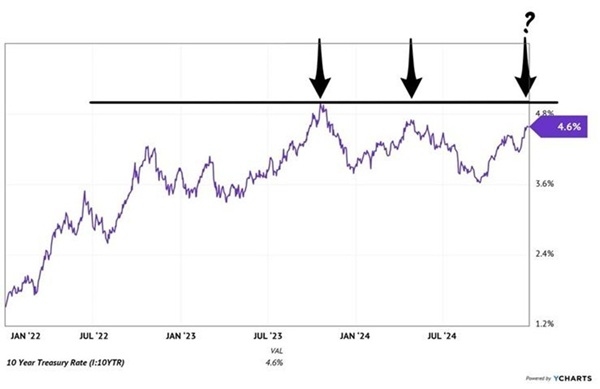

Get this: Since the Fed’s latest rate-cut cycle started, the yield on the 10-year Treasury note—benchmark for consumer and business loans of all sorts—jumped from 3.7% to around 4.6% as I write this.

In other words, interest rates are rising as Jay cuts. What?

Finally, Jay laid down some parental guidance at the last FOMC meeting: Don’t expect another rate cut until inflation numbers improve further.

Funnily enough, Jay’s new-found “adult in the room” attitude just might cement the ceiling on the 10-year Treasury yield. And it was the right call (if a bit late): More easing would hurt the stock market because bond investors would demand higher rates.

A “5% ceiling” on the 10-year Treasury is great news, not only for bonds (which are despised right now) but “bond proxies,” which have also been tossed over the side.

One of those “bond proxies”? REITs, “landlords” who rent out properties ranging from cell towers to warehouses and apartments.

REITs-at-large look attractive here. In the short run, they trade opposite the 10-year Treasury yield, for a couple of reasons:

- REITs pay most of their profits as dividends. So they tap the debt markets often to grow. Higher interest rates mean higher debt costs and squeezed earnings, which mean lower stock prices. Which is why we want to buy REITs when rates top—because their stocks rally as rates decline.

- REITs also see competition from fixed income. Their roughly 4% average yields don’t look impressive with a backdrop of 5% money-market funds. But it’s about to look better when money-market funds pay less.

The main reason why we love REITs? Those dividends! Uncle Sam gives REITs a “hall pass” on corporate taxes as long as they pay out 90%+ of their earnings as dividends.

That makes these landlords essentially “pass-through” businesses: They collect the rent from their tenants, keep enough of it to keep the lights on and the buildings maintained, then pass the rest on to us!

Now, I know a lot of investors love to buy and hold on to REITs for the long haul, in large part due to those high payouts. And the truth is, this is often a good strategy for select REITs—we’ve held plenty of those in my Contrarian Income Report service over the years.

But with the 10-year yield now near what I see as a ceiling, the smart play is to “swing trade” our REIT holdings, riding them up as the 10-year yield eases—pushing up their prices—then stepping out when long rates rise again.

Riding (and Re-Riding) the “Rates-Down, REITs-Up” Teeter-Totter

We’ve played this very shift in my Dividend Swing Trader advisory in the past. In April 2024, we bought Ventas (VTR), a REIT that owns about 1,400 properties. These are the “beachfront properties” of healthcare real estate: senior housing, medical buildings and research centers in major cities across the country.

At the time, the stock was down 13% on the year as long rates rose. But with rates topping, it was time to buy in, so we did. When we took our money off the table a little over seven weeks later, we did so with a quick 11.1% total return (or 74% annualized):

We Banked a Quick 11.1% Total Return From VTR

That, by the way, beat the S&P 500, which returned just 2.5% in that time—a pretty sweet gain from a so-called “sleepy” landlord like VTR.

The company cut its dividend (current yield: 4.2%) during 2020. Today, Ventas easily covers this payout at only 57% of its last 12 months of funds from operations (FFO). That’s very low and safe. With REITs, payout ratios up to 80% or so are fine. Which means Ventas is a strong candidate to begin raising its payout once again.

All of this, plus the fact that the 10-year yield looks to be hitting a ceiling again, makes now another good time to buy Ventas, collect its steady payout and wait for our “10-year-yield-down, REITs-up” shift to run its course.

Do NOT Miss My Next “Quick Profit” Trades (and Crucial Update on Ventas)

VTR is only one short-term dividend trade I’m recommending as we move into Trump 2.0, and I’m lining up more now. I want to make sure you get in on all of them.

Because as I mentioned, I expect market trends to shift quickly in the next four years.

Sad to say it, but retirements will be lost. But fortunes could also be made by those who move deftly enough.

You’ll also discover how to get in on my next short-term dividend buys and get an instant notification of when it’s time to “swing out” of VTR (along with our other picks) and lock in our gains. Don’t miss this critical briefing, which is waiting for you right here.