One of the most expensive mistakes CEF investors make? Chasing a fund’s discount.

That would be the discount to net asset value (NAV).

A big discount has a lot of appeal because it essentially means we can buy a CEF’s assets—stocks, bonds, REITs, utility stocks, you name it—for less than we could if we bought them ourselves on the open market.

So it makes sense that we should always go for the CEF with the biggest discount, right? After all, CEFs pay dividends north of 8%, on average—with the portfolio of my CEF Insider service paying even more: 9.3% as I write this.

And a big discount sets up the possibility of strong price gains to go along with those high payouts.

This is, in fact, the right way to look at CEFs—to a point. But it’s not enough on its own; when we see a big discount (or an oversized dividend, for that matter), we do still need to dig deeper to see what’s behind it.

That’s because a discount is sometimes big for a reason. And if a big discount never narrows, then it can’t provide that additional upside burst we want to see. In fact, it could turn out to be an anchor on our gains.

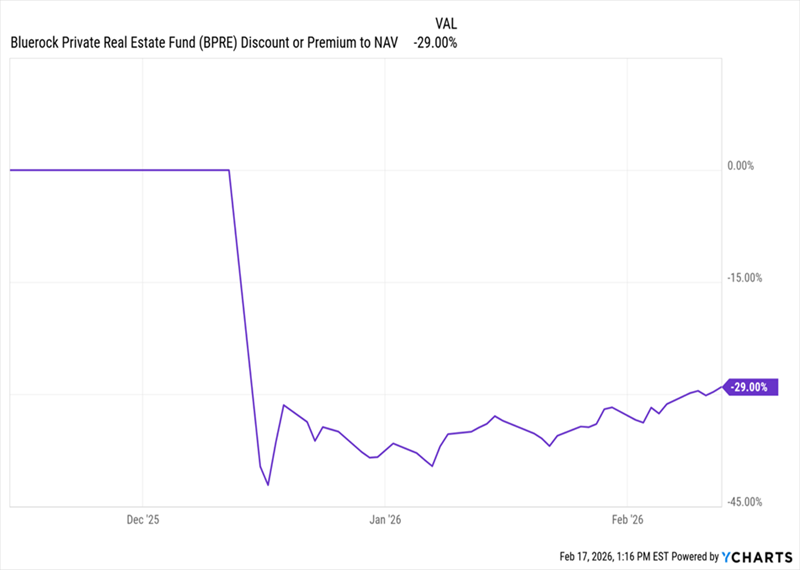

To see what I mean here, let’s look at two CEFs at different ends of the discount spectrum: the Bluerock Private Real Estate Fund (BPRE), with a 29% discount as I write this, and the Reaves Utility Income Fund (UTG), with a much narrower 1.1% discount.

The question here is straightforward: “Why is the gap between these two funds’ discounts so big?”

In part, it’s because of BPRE’s unique history, which I discussed in detail in an article in early January. The story boils down to this: Management switched BPRE from an unlisted, privately held fund to a publicly traded one. And investors, concerned about the illiquidity of the fund’s private-real-estate assets, balked and sent it to a deep discount.

So is this an opportunity for us?

Simply put, no. For one, you can see from the chart below that after the fund’s discount dropped below 40% right after its IPO, it has stayed more or less stuck at those deep-in-the-cellar levels.

BPRE’s Discount Goes Into Deep Freeze

This doesn’t give me a lot of hope that this discount will get to reasonable levels anytime soon. Sure, it’s edged up a bit from the depths, but it still has a long way to go before it gets into the 10%-or-less zone where a lot of CEFs trade.

And that’s just the start.

Another reason for that discount could be something else, beyond liquidity concerns—namely that nearly 10% of the CEF’s assets are parked in a money-market fund.

Source : BlueRock Private Real Estate Fund

This might not seem like a problem at first. But keep in mind that this fund, like all funds, charges fees, so investors are literally paying the managers to hold cash here. So BPRE is not giving us 100% exposure to private real estate, as the name claims.

Which begs the question: Why does management feel it needs to have all this cash on hand? Remember, this fund is supposedly focused on private real estate, which has become controversial recently over concerns about liquidity.

In other words, this is a speculative asset class to hold right now, in a CEF that pays a high 7.8% dividend. With that in mind, it’s hard to see this cash holding as anything other than management buying time—using these funds to cover the payout until it’s forced to sell assets. That does not bode well for dividend sustainability in the long run.

Now, whether that scenario ultimately plays out or not remains to be seen, but it’s another reason why we shouldn’t expect the fund’s discount to climb out of the dungeon anytime soon.

What About UTG?

Now let’s turn to UTG, which is different in many ways, even before we look at the discount.

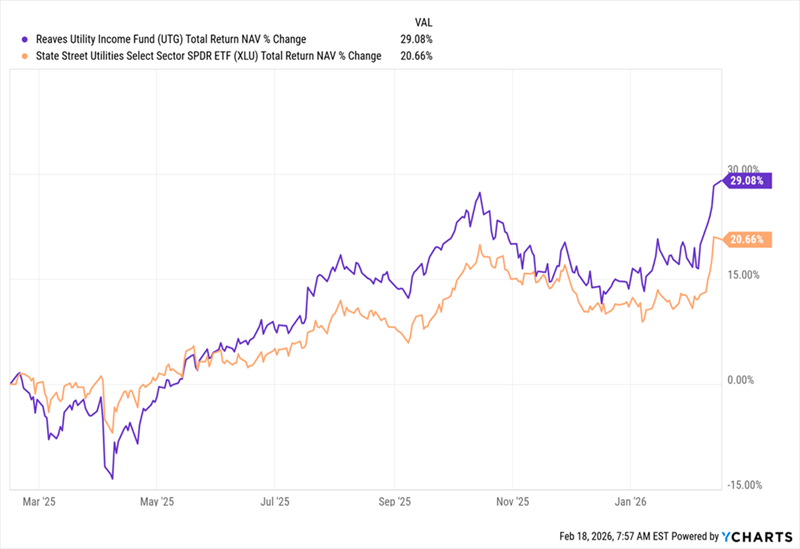

UTG’s Return Accelerates

Here we see the fund’s performance over the last year (in purple) against that of the benchmark index fund for utilities, the State Street Utilities Sector SPDR ETF (XLU), in orange.

There are two things to note here: First, this is a total NAV return, so the portfolio’s fundamental performance, not the market price (which is the return we get on the fund).

UTG also has a strong performance over the last decade, returning about 11% annualized in that time on a total market return basis. XLU is similar, at about 10.9%. But we still prefer UTG for a simple reason: It’s giving us more of its return in cash, with a 5.9% current yield, compared to just 2.5% for XLU. And the fact that it can outrun XLU in bursts—as it is now—adds even more appeal.

That’s not the best part, though. UTG’s portfolio diversifies across utility companies from across the country, from Florida-based giant NextEra Energy (NEE) to Maryland’s Constellation Energy (CEG).

And, unlike with BPRE, UTG is fully invested in operating businesses:

UTG’s Basket of Utility Stocks

Source: utilityincomefund.com

In light of all that, UTG’s smaller discount makes sense. The market has priced this fund near its NAV because, well, it’s a great utility fund that gets you exposure to the sector while crushing the index’s 2.5% yield.

One final note: As appealing as that 5.9% is, it’s actually low compared to the CEF average and to our CEF Insider portfolio’s average of 9.3%. So while UTG is a good fund to buy now, despite its smaller discount and dividend yield, there are plenty of other options if you want more income now—and deeper discounts, too.

Your Next Big Dividend “Paycheck” Is Around the Corner (59 More to Come!)

What if I told you that in addition to strong dividends at big—and authentic—discounts, we’re also going to turn more (maybe even all) of your portfolio into a monthly dividend machine?

I’m talking about a continuous cash stream that rolls into your account 5 times a month, for a total of 60 dividend “paychecks” over the next 12 months.

Your average yield? 9.3%.

That’s exactly what I want to help you do. And the 5 monthly paying funds I’m pounding on today hold the key. They boast:

- High, strong yields. That’s right: 9.3% on average. So we’re getting $9,300 a year on every $100K invested here.

- Instant diversification: These 5 funds come from across the market, holding the top stocks, bonds, REITs and more.

- Deep discounts, which will help drive their prices higher as these unusual markdowns slam shut.

I’ve prepared a full investor report that takes in you inside these 5 monthly payers and shows you exactly how they’ll kickstart your 60-dividend income stream for the next 12 months. Click here to read it and get a free Special Report revealing these 5 funds’ names and tickers.