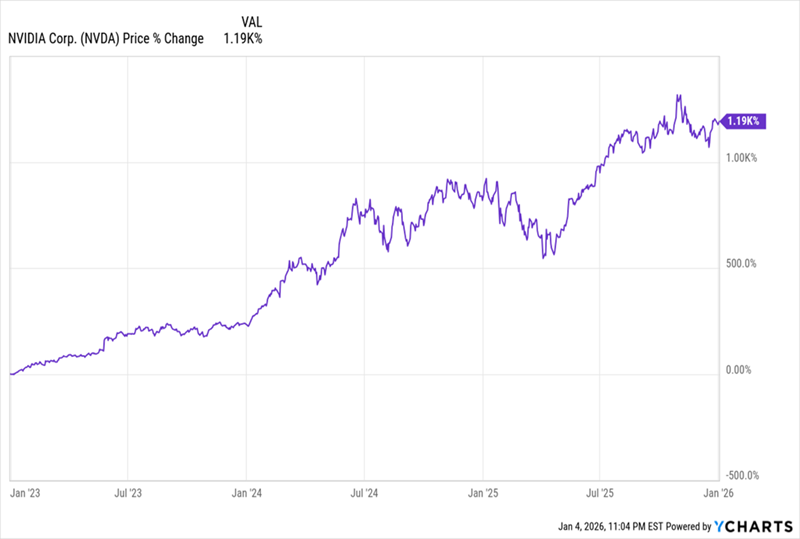

The run that AI poster child NVIDIA (NVDA) has been on these last few years is truly incredible. That’s not news, of course. But what matters now is whether investors are overpaying for that growth—in both NVIDIA and AI as a whole.

NVIDIA’s Monstrous Run

Once a chipmaker known for appealing mainly to gamers, NVIDIA started to climb in 2023, thanks to a new technology only a few people really understood at the time: generative AI.

Then, as AI spread in 2024, hopes—and NVIDIA’s stock—soared. That was followed by more fears of a bubble in AI. As with NVIDIA’s share price, a chart is the best way to do these worries justice:

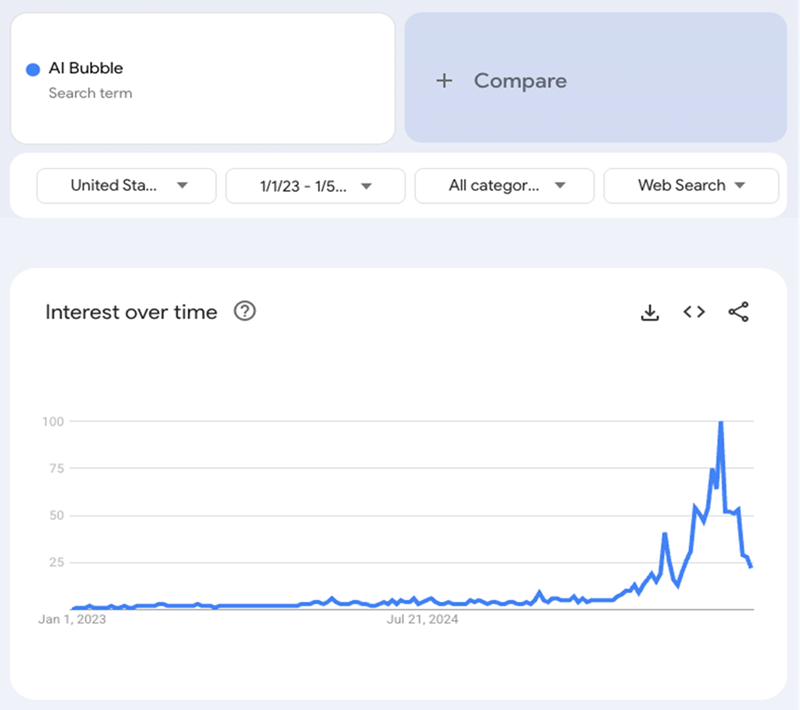

The Bubble in Worries About an AI Bubble

There’s so much discussion of an AI bubble now that we seem to be in a bubble of talking about bubbles! That’s why some advisors are saying that this AI bubble talk is a distraction. I’d agree, as we can’t even be sure this is a bubble—and I’d argue it’s not.

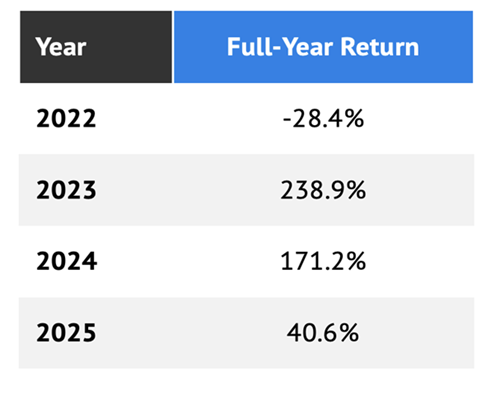

To see why I’m saying this, we need to look no further than NVIDIA shares. Consider this table of their performance in the last four years.

Here I’ve broken out NVDA’s per-year returns since 2022, a year in which the stock plunged alongside all of tech. Note how its biggest year was in 2023, and that its gains have been moderating since?

If this were really a bubble, you’d expect yearly gains to keep building and building until they hit a wall. That’s not the case here. In fact, I’d argue that we’re seeing a massively undervalued company becoming a fairly valued one.

To really unpack this, let’s look at how much investors are paying for NVIDIA’s earnings. We’ll do that by looking at the stock’s price-to-earnings (P/E) ratio (in purple below). As you can see, it roughly matches that of “boring” big-box retailer Costco (COST)!

Is NVIDIA Really Worth as Much as …Costco?

I think you’ll agree that Costco, with its membership-driven revenue, is a pretty reliable revenue generator. This shows that investors are starting to see NVIDIA the same way.

Note also that NVIDIA’s P/E ratio trailed that of Costco for most of 2025.

In other words, this is not a bubbly valuation. And in fact, none of the “Magnificent 7” stocks sport higher valuations than Costco right now. That is, except for Tesla (TSLA), which in many ways lives in its own little world.

To be sure, some aspects of the AI space do look bubbly, like the 700 seed-stage rounds that attracted $10 million or more in 2025. This shows that venture capitalists are indeed making some outrageous bets here.

But that’s not a sign of a bubble. In fact, I heard the same worries about VC overinvestment in the early 2010s (if you don’t remember Juicero, it was a great example of VC silliness), when I worked on Wall Street. The market powered higher anyway.

But what about all the infrastructure investments we hear about, especially around data centers? One report says we saw about a 30% growth rate in data-center spending in the middle of 2025, to about $40 billion on an annualized basis, and the Fed estimates about $41.2 billion. But both sources also cite rapid growth in building back in 2023 and 2024, so the 2025 rate actually moderated compared to 2024.

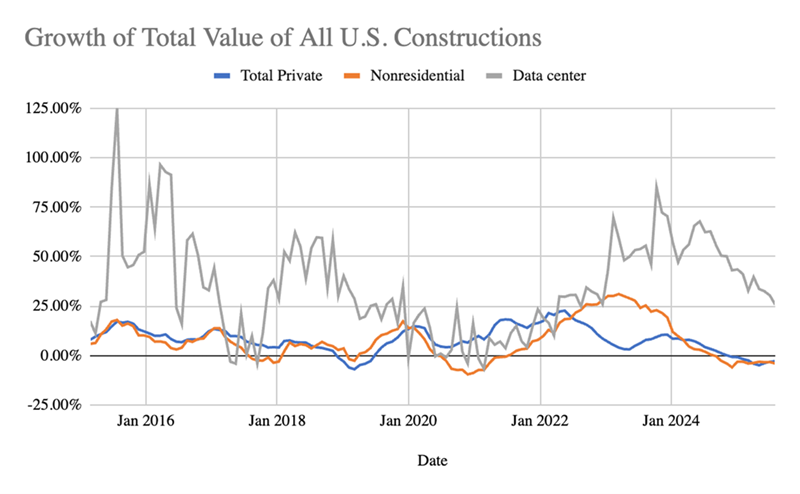

If we look at total private construction of non-residential properties, as provided by the Census Bureau, a similar story appears.

Source: US Census Bureau, CEF Insider

Here we can see spending growth on data-center construction (gray line) far outpacing all nonresidential spending (orange line) and overall private-sector spending (blue) in late 2023 and 2024. That was actually the case in the late 2010s, as well.

In fact, data-center spending looks like it’s simply going back to where it was pre-pandemic. It’s also worth noting that the growth rate has been slowing since peaking in late 2023, much like NVIDIA’s stock-price growth has been moderating since then, too. In other words, this is clearly not a bubble—if anything, the bubbly numbers looked most alarming in late 2023.

How I’m Playing the AI “Non-Bubble”

So what’s the best approach for us here?

For one, the data says this market is not acting irrationally. On the contrary, valuations suggest a mature market, and our best play is to remain fully invested and diversified.

Most people would go with an index fund like the SPDR S&P 500 ETF (SPY) in a situation like this. But we want dividends, and SPY’s sad 1% yield just won’t cut it.

In this market, while we wait for AI to continue its spread through the US economy, getting a big slice of our return in cash dividends is key. That’s why we prefer a closed-end fund (CEF) like the Adams Diversified Equity Fund (ADX), a long-time holding of my CEF Insider service.

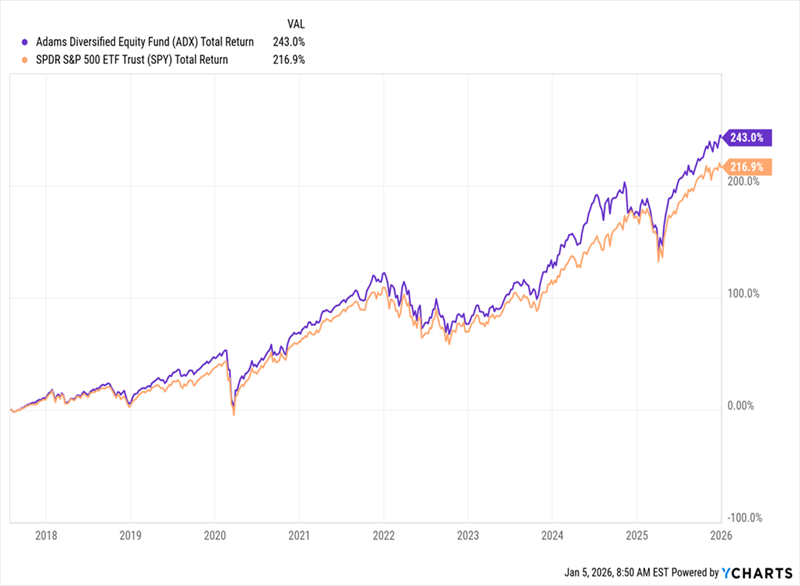

ADX is a proven long-term wealth generator, both in the form of dividends and capital gains. Since we bought the 7.9%-yielding fund in July 2017, it’s returned 243% in gains and dividends, as of this writing, soundly beating the S&P 500.

“Dividend-Powered” ADX Beats the Market in the Long Term …

That’s thanks to management’s stock-picking skills (ADX holds NVIDIA, along with many other top S&P 500 stocks). Their acumen stems from ADX’s long institutional memory: The fund traces its roots back to 1854—yes, the mid-nineteenth century.

And then there’s that income stream, responsible for a big slice of the fund’s total return: ADX’s 7.9% yield is roughly seven times that of the typical S&P 500 stock (note that ADX’s payouts do flex somewhat, based on its portfolio performance).

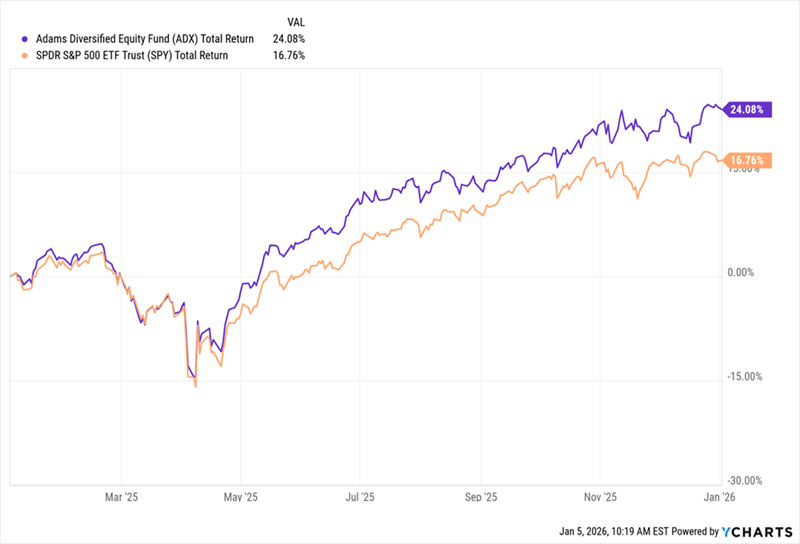

The odd thing about CEFs like ADX is that when investors judge their performance, they tend to only look at price returns, not total returns (including dividends), as we discussed last week. And on a price basis, ADX returned 15.5% in 2025, just less than the 16.4% of an S&P 500 index fund. But add reinvested dividends and you’ll see that ADX (in purple below) easily beat the market.

… And the Short Term, Too

CEFs like ADX are nicely set to keep outrunning a rising stock market. Anyone who’s letting bubble fears keep them out of the market (and this great fund) are missing out—on both the income and the capital gains side.

4 URGENT January Buys to Tap AI’s “Next Wave” (for 8%+ Dividends)

When it comes to AI investing in 2026, one thing is crystal clear: The biggest gains will come from the users of the technology. As we saw with NVIDIA above, the biggest profits in AI developers have already been made.

But luckily for us, these users of AI—those companies that are just starting to see the benefits—include many dividend stocks we all know well.

And when we buy those stocks through CEFs like ADX, we get an extra “bonus”: These funds’ rich 8%+ dividends. I’m not pulling that 8% figure out of thin air: It’s the average yield on my top 4 AI-focused CEFs to buy now.

These 4 funds are dialed into the “next wave” of the AI boom. Between them, they hold a basket of undervalued stocks from across the AI space, including those best positioned to supercharge their profits as they adopt this revolutionary technology.

All 4 funds are cheap now, but that won’t last as the crowd begins to look beyond the popular AI stocks for bargains (and dividends).

The time to buy is now. Click here and I’ll walk you through these 8%-paying AI funds and give you a free Special Report revealing their names and tickers.