A multi-year disconnect in high-yielding REITs is about to turn on its head. When it does, these solid income plays are poised to shoot ahead of stocks.

I’m talking about a quick reversal of pretty well everything investors thought had REITs left for dead, interest rate trends and the work-from-home shift among them.

Now is the time to buy. And we contrarian income investors know the play:

At times like these, we look to 8%+ paying closed-end funds (CEFs) to reap the strongest dividends and potential upside.

I say this as REITs, long-time market outperformers, have been stuck in an unusually long slump.

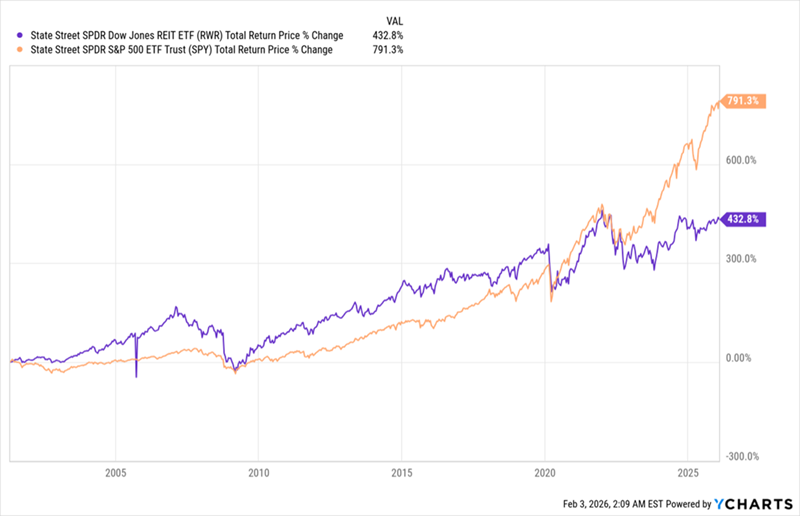

Remember when stocks ricocheted hard after the early days of the pandemic? REITs (with their benchmark ETF shown in purple below, compared to the main S&P 500 ETF, in orange) rebounded, too. But not nearly as much.

REITs’ Slow Recovery

Why REIT Headwinds Are Diminishing—and Setting Up to Reverse

There are lots of reasons why REITs have lagged in the last six years, and none of them are really secrets: Work-from-home hit office demand. Interest rates jumped, hitting REITs’ bottom lines, as these companies borrow heavily to invest in their properties. Lower immigration into the US also had an effect on both housing and workspace demand.

That last point—immigration into America—still applies. But both of those other barriers, which are far more meaningful, have either flipped or are in the process of doing so.

Work-from-home? It’s largely been replaced by either a full-time return to the office or hybrid work. Interest rates? This is where things get intriguing.

Rates Fall, REITs Start to Respond

REITs, as mentioned, borrow to invest in real estate, so rate cuts go straight to their bottom lines. The cuts the Federal Reserve has delivered since mid-2024 (in orange above) have come more slowly than markets expected. So it follows that the boost to REIT profits, and therefore their share prices, is real (purple line), but smaller than investors hoped.

That leaves REITs in a strong position—still underpriced, but starting to show momentum. And with the first month of 2026 now behind us, we can see the current state of play here:

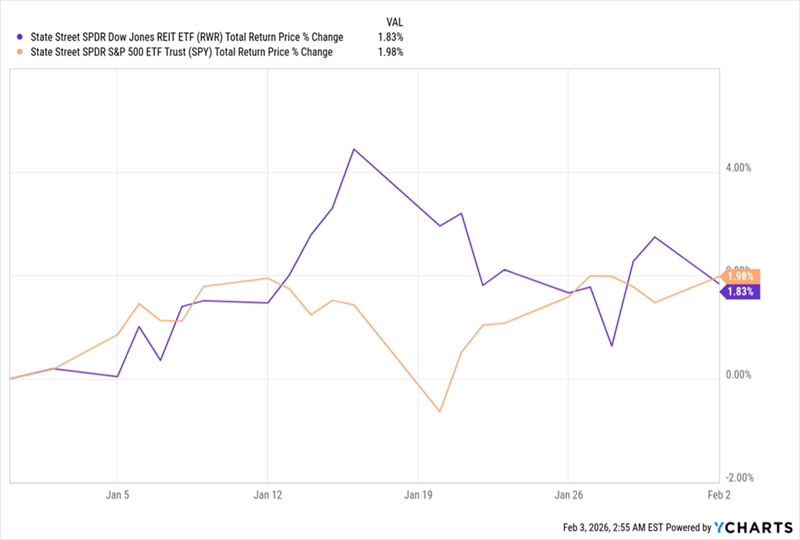

REITs Nearly Reeled In Stocks in January

As you can see, in January, REITs (again with their benchmark in purple above) almost met the stock market’s returns. Now, one month does not make a trend, but that’s a switch from what we saw in 2025, when the S&P 500 gained over 17% and RWR returned a mere 3.2%.

The takeaway: The lead stocks have held over REITs is finally starting to fade.

And if interest rates fall faster than the market expects—quite possible if President Trump’s nominee for Fed chair, Kevin Warsh, is confirmed—REITs could not just match the S&P 500 but beat it this year.

That would finally end REITs’ six-year lag. Let’s buy in before that happens. How?

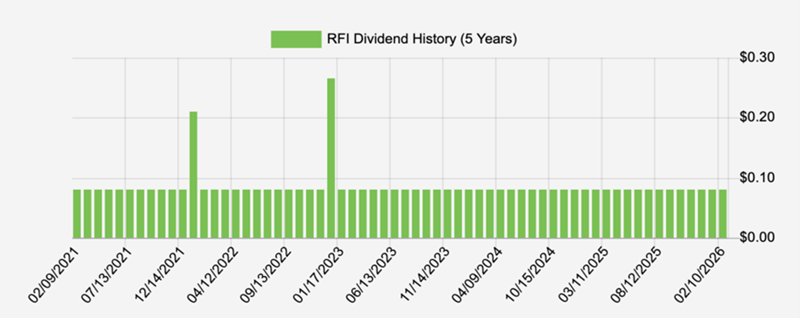

My favorite avenue is through those aforementioned CEFs. Consider, for example, the Cohen & Steers Total Return Realty Fund (RFI), a holding in my CEF Insider service that yields 8.6% as I write this.

The fund is a solid play here, thanks to that 8.6% dividend, which has been rock-steady for years. The fund pays that dividend monthly, to boot.

Source: Income Calendar

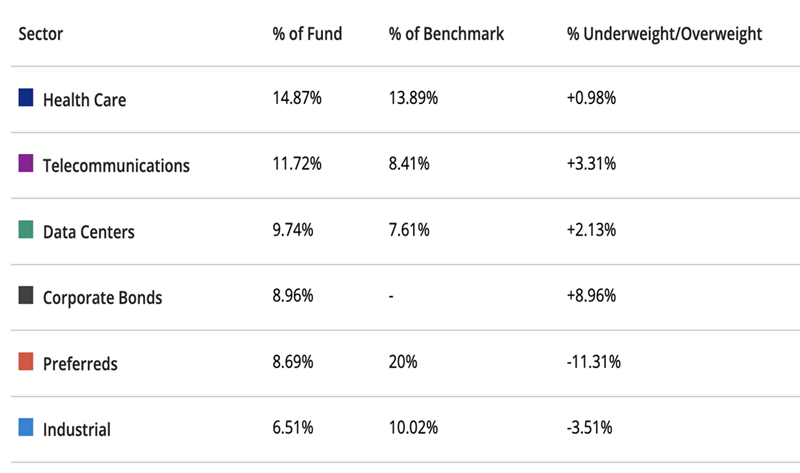

RFI is also nicely diversified, boasting a portfolio that gives us exposure to AI’s infrastructure needs, with significant weightings in data center and communications (think cell-tower) REITs.

Source: Cohen & Steers

It also holds industrial REITs, giving us broad exposure to both the reshoring and automation of factories. That top allocation to healthcare is also a plus, letting us tap into the aging of the US populations—a trend that still has decades to run. Finally, its allocations to bonds and preferred shares add stability.

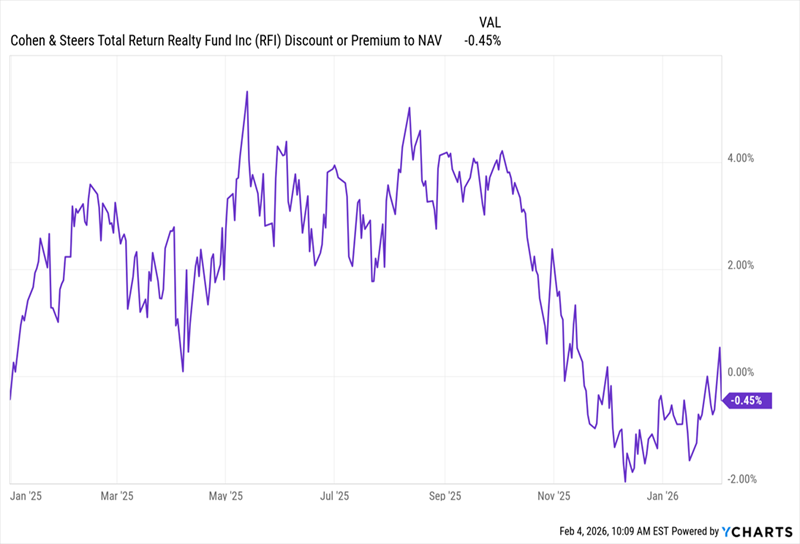

The fund is cheap, too. As I write this, we can buy RFI at a 0.5% discount to net asset value (NAV, or the value of the fund’s portfolio). I know that doesn’t sound like much of a deal, but it’s far below the premiums at which RFI traded for most of last year:

The kicker? That “small” discount is also well below RFI’s average premium of 3.7% over the last five years.

That makes now a good time to buy this overlooked bargain, before other investors pick up on the many tailwinds shifting in RFI’s favor.

5 More “Built-for-2026” Income Plays You’re Not Too Late On (Yields Up to 10.7%)

CEFs are, hands-down, the top plays on disconnects like the one we’re seeing shape up with REITs today, for three reasons:

- CEFs pay us (mostly) in cash, thanks to their rich dividends (around 8% on average).

- CEFs give us a double discount—on both washed-out stocks (or in this case REITs) themselves and on the fund itself through its discount to NAV.

- CEFs put our investments in the hands of a professional who knows their asset class inside and out.

In an exclusive investor bulletin I’ve updated for 2026, I go even more in-depth on 8%+ paying CEFs and show you exactly why these “hidden funds” are perfect for those of us who rely on our portfolios for income (but want strong price gains, too).

I’ll also introduce you to 5 of my top CEF buys for the year (with yields up to 10.7%) and give you a free Special Report revealing these 5 funds’ names and tickers.

It’s a diversified “built-for-2026” wealth- (and income-) building package, and it’s waiting for you now. Simply click here to read the full bulletin and get your free report profiling these 5 CEFs paying up to 10.7%.