Bonds are back, baby. Let’s talk about three funds that pay—between 8.3% and 10.9%.

Plus, they are trading for less than the fair value of their parts. It’s free lunch time in Bondland.

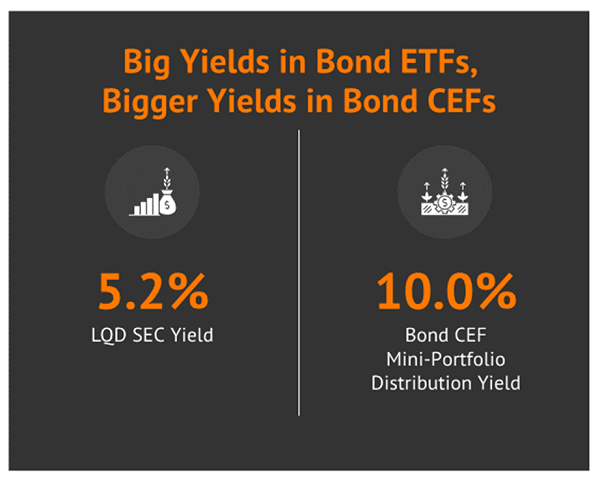

Of course not all bond funds are created equal. ETFs serve their purpose, but closed-end funds (CEFs) are where the payout party is at. Value plus yield at the CEF café.

Most ETFs are tied to an index. Which means they are run by rules and robots. Boring.

CEFs tend to be actively managed, meaning “bond brains” are able to adjust their portfolio from defensive to offensive as the investing environment shifts. They can also use leverage to boost their returns. This can cut both ways, but when money is cheap, we like managers who lever up.

CEFs simply pay more, too. Let’s pick on iShares iBoxx $ Investment Grade Corporate Bond ETF (LQD), one of the higher paying ETFs. However, LQD pays barely half of the CEF three-pack we’re about to discuss.

Again, these funds each trade at discounts to their net asset value (NAV). Which means we can buy $1 in assets for less than a dollar. Sweet.

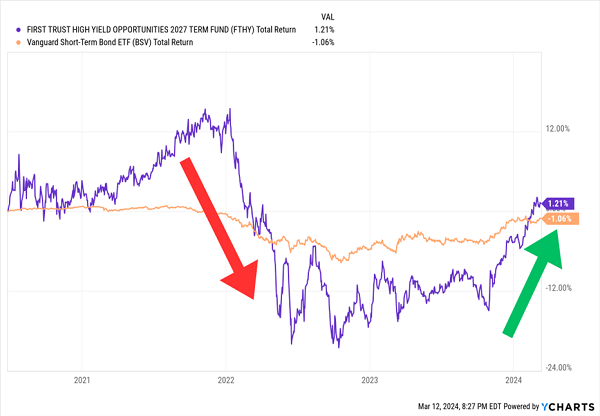

First Trust High Yield Opportunities 2027 Term Fund (FTHY)

Distribution Rate: 10.8%

The First Trust High Yield Opportunities 2027 Term Fund (FTHY) is more of a tactical play than a long-term holding. It won’t exist past 2027!

FTHY’s managers are required to hold at least 80% of assets in below-investment-grade (junk) debt. Currently, that number is closer to 85%, with the rest of assets held in senior loans.

The fund’s average maturity is on the shorter end, at just less than 4.5 years, so you won’t necessarily get the same amount of wiggle you’d get from funds more sensitive to the longer end of the yield curve. Still, FTHY isn’t a bad way to trade the shorter end of the yield curve. Especially given that roughly 20% in debt leverage helps juice its returns.

FTHY is certainly more appealing than plain-vanilla short-term bond funds if your goal is to take advantage of lower bond yields (and thus higher bond prices). A 10.8% distribution, paid monthly, ain’t bad either!

FTHY Shows Early Potential of a Rate-Cut Play

Interestingly, FTHY’s 8% discount to NAV, while nice, is lower than its average—but that’s deceiving, because as a term fund, it should close the gap between now and the end of its term in 2027. (In other words, the discount should narrow, bringing prices up.) The flip side? “The Fund’s limited term may cause it to invest in lower-yielding securities or hold the proceeds of securities sold near the end of its term in cash or cash equivalents.”

In other words, not only can we not buy-and-hold FTHY for very long, but the fund’s ability to outperform could decline as we approach its expiration date.

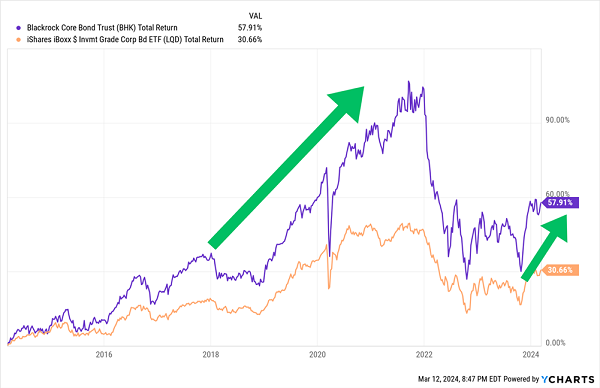

BlackRock Core Bond Trust (BHK)

Distribution Rate: 8.3%

The BlackRock Core Bond Trust (BHK) is a “north-south football” kind of fund that invests at least 75% of its assets in investment-grade fixed income.

Right now, that’s a blend of corporates, securitized products, agency mortgages, government bonds, and some international investment-grade bonds. BHK also currently holds roughly 20% in junk issues.

BHK is where we can start to take advantage of an eventual move lower in long-term rates. Nearly two-thirds of the fund is bonds with maturities of five years or longer, and more than a third is invested in bonds with 10 or more years left. That potential is further magnified by even more debt leverage than FTHY, at 33% as I write this. It’s a portfolio set up to win, and win big, when interest rates are on the decline, much like BHK did for years until the Fed’s latest rate-hiking cycle.

BHK: The Start of a Second Rip?

But BHK isn’t for the faint of heart. We do not want to own BHK when long-term rates are rising.

Also, yes, while this BlackRock fund does trade at a discount to NAV, it’s narrow, at just a hair over 1%. In fact, considering its longer-term average is closer to 3%, we could argue this CEF is pricey at 99 cents on the dollar.

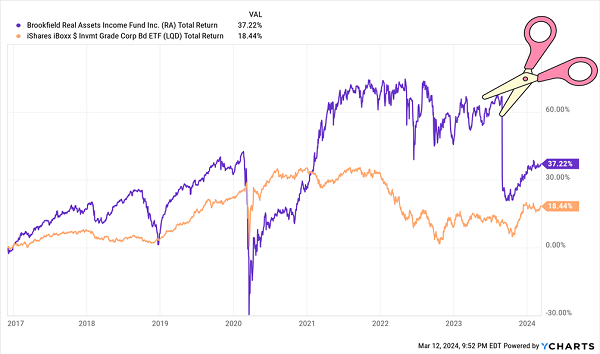

Brookfield Real Assets Income Fund (RA)

Distribution Rate: 10.9%

Brookfield Real Assets Income Fund (RA) is cheap… for a reason. We can buy its assets for 87 cents on the dollar, a 13% discount that seems generous at a glance.

Problem is, despite the name, RA doesn’t invest in “real assets,” but instead in credit of infrastructure, real estate, and natural resources. Roughly 60% of assets are dedicated to corporate bonds in those three areas, while another 33% is stashed in mortgage-backed securities (MBSs). Backing out another 4% in cash, and the paltry remainder is in “real asset” equities.

This used to be a Contrarian Income Report holding, until I sold it in November 2018. At the time, I warned:

“The fund’s generous distribution (10%+) and equally generous discount (6% to 9%) gave us a margin of safety while we awarded their promising management team time to dial in their strategy. But to be blunt, they haven’t.

Their average coupon today pays just 4.8% while they’re on the hook for a 10.4% distribution on NAV. Borrowing cheap money helps fill some of the gap but not enough of it. And the portfolio remains too heavily focused on fixed-rate and longer-duration bonds for my liking.”

For the next five years or so, the monthly dividend remained constant while NAV plunged. Shareholders finally paid the piper in August, when the company announced a 41% cut to the distribution starting in September, sending RA’s stock crashing.

RA Cut the Dividend, And Cut Many Shareholders Loose Along With It

What remains is at least, for now, a more sustainable payout. RA’s distribution is now funded by actual income. The fund also has less exposure to the time bomb that is commercial real estate. Its commercial MBSs make up 10% of assets—better, but not good enough for us careful contrarians.

The Bond Bull: 3 Funds Yielding Up to 12% With Massive Upside Potential

Still, if we want to make hay with the coming bond bull, we don’t want to do it in rehabilitation projects.

We want to do it by owning A+ bond funds with sterling track records.

The bond market has been pulverized in recent years, with many bonds getting slashed by 50% or more—on par with the Dot-Com Bubble bust and Great Financial Crisis!

But fixed income has recently shown flickers of life—a quick reversal that could signal the start of a new “bond bull.”

And I’m getting ready by positioning myself into three funds that not only deliver fat yields of up to 12%, but have massive upside potential, too.

Bonds are throwing off their highest yields in more than a decade! The “Agg” index, with a yield of around 5%, is paying nearly 5x what it did just three years ago.

The Fed has signaled multiple rate cuts—and as you know, when rates head lower, bond prices head higher.

So right now, we have a rare chance to lock in uber-high rates before they disappear, and set ourselves up for price upside when bonds pick up steam. It’s a powerful 1-2 punch most investors don’t think about when it comes to the bond market!

I’m not the only one who has noticed, either. Capital Group, PIMCO, BlackRock … all of Wall Street’s big names, collectively managing trillions of dollars, are starting to notice the potential for a sea change in the coming months.

If things go the way the Fed, the biggest investment firms and I think—well, astute investors can make a boatload of money in the bond market.