The Dow Jones Industrial Average itself yields modestly, but the Dogs of the Dow 2026 pack more dividend bite. The index’s top payers dish up to 6.8%. Collectively, they provide 3X more yield than the miserly S&P!

We’ll review every one of the Dow’s 10 Dogs (and their dividends) in a moment. First, a refresher on how the “Dogs of the Dow” strategy works:

- After the final close of 2025, we identify the 10 highest-yielding stocks in the Dow Jones Industrial Average.

- The strategy buys all 10 stocks in equal amounts and holds them for the full calendar year.

- At the end of the year, the stocks are sold. And the next 10 highest-payers are purchased.

The strategy works because it is contrarian. High yields for blue chips are a signal of value. These stocks aren’t going out of business—they are merely out of favor.

Are America’s blue chips going out of business in 2026? I think not. So “the Dogs of the Dow” suggests we buy these stocks when their prices are lower, their yields are higher, and the chances of a bounce-back are elevated—it’s the contrarian way!

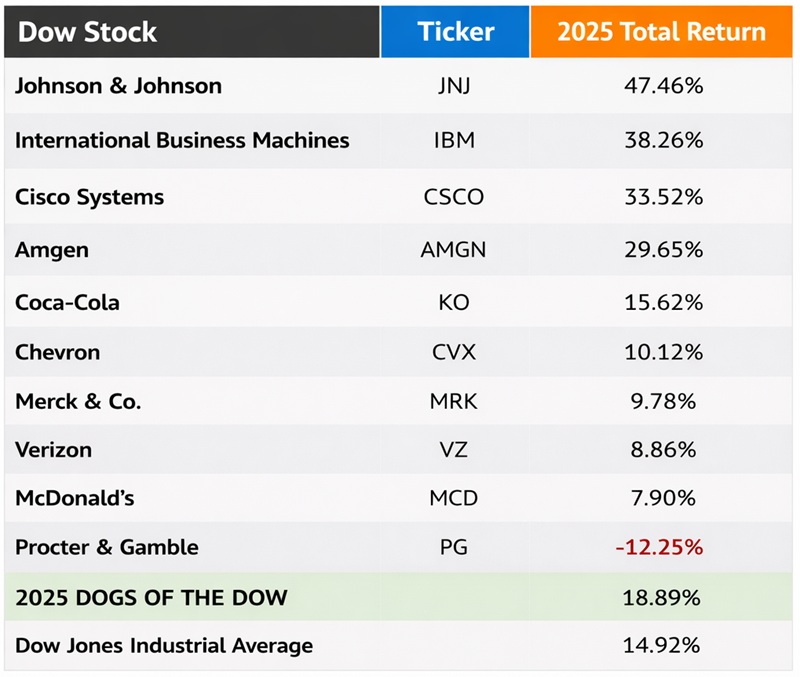

The 2025 Dogs Were Very Good Boys

Obviously, lopsided gains in Johnson & Johnson (JNJ), International Business Machines (IBM) and a couple other stocks helped the Dogs outdo the broader Dow. That’s the case every year—and an argument (for some investors) to cherry-pick the most interesting Dog components rather than blindly buying the group.

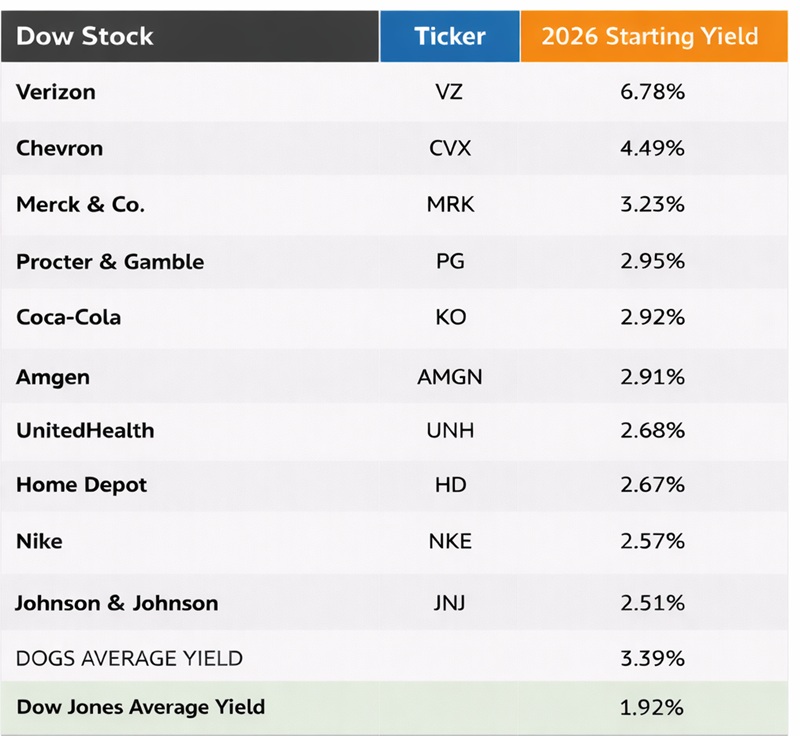

And who do we have to choose from in 2026?

The 2026 Dogs of the Dow

The Dogs’ average yield, which started 2026 north of 3%, is still shy of what we need to retire on dividends alone. So the upside potential of these blue chips is an important consideration, too.

Let’s keep that in mind as we evaluate each of 2026’s 10 Dow Dogs. We’re looking for the total package here: companies that can both deliver the cash and punch above their weight in the year to come.

#10: Johnson & Johnson

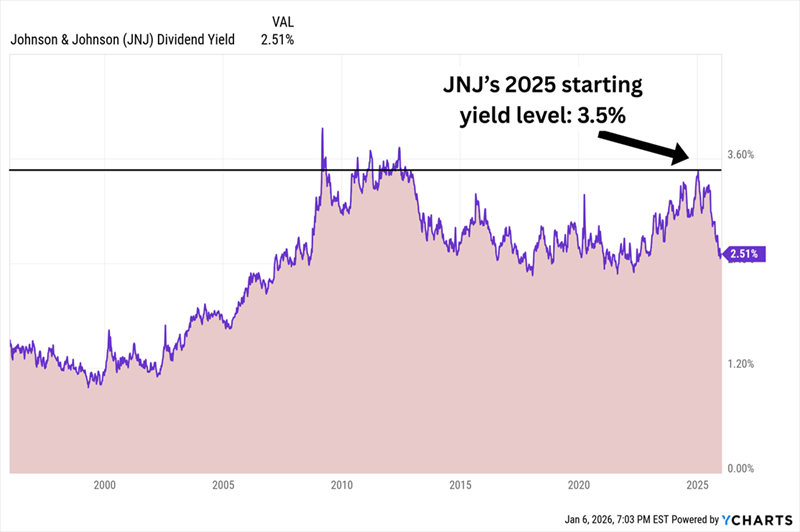

The Skinny: In 2025, Johnson & Johnson (JNJ, 2.5% yield to start 2026) gave us a prime example of what we want out of our Dividend Dogs. Those who jumped on the pharma company’s shares locked in a yield that was well above JNJ’s historical averages, then the stock rocketed to the mean and a 47% total return.

Fundamental drivers? Strength in the company’s immunology, oncology, and medical-tech offerings; launches of new indications for Tremfya and Rybrevant plus Lazcluze; and the announcement that JNJ would spin off the DePuySynthes orthopedics business.

Rarely Had Investors Been Paid More to Own J&J

What Has to Go Right in ‘26: JNJ is still a dog, but it’s starting with a modest 2.5% yield—good but not great for JNJ. It needs continued successes to offset competition to its autoimmune blockbuster Stelara. Legal defense of its talcum powder would help, too. In late 2025, a Baltimore jury ordered J&J to pay $1.5 billion in the largest-ever award to a talc plaintiff—a ruling the company said it would appeal.

#9: Nike

The Skinny: Nike (NKE, 2.6% yield) is the first of three new Dogs in 2026. It has been in freefall since late 2021, losing more than 60% of its value in that time—including a nearly 15% drop across 2025 that pushed its yield into the Dow’s top 10. Nike has been hobbled by numerous problems, including shifting consumer trends, supply chain issues, tariff complications and struggles at its brick-and-mortar locations. And while it closed out 2025 with a Street-beating earnings report, it did so while reporting slumping sales in China. The company also announced its 24th consecutive annual dividend increase, but it was a meager 2% bump that was much smaller than in recent years.

What Has to Go Right: In 2024, the company hired longtime Nike veteran Elliott Hill to replace John Donahoe as CEO, and the company is now roughly a year into its turnaround strategy. The company is trying to “lead with sport” again, realigning thousands of employees around core categories including running, basketball and sportwear. It’s also repairing relationships with wholesalers and pulling back on discounting. Profits are expected to take a big step back this year—current fiscal 2026 estimates would fall just shy of covering the payout—before rebounding significantly in fiscal 2027. And even then, the stock isn’t cheap, trading at 27 times next year’s estimates. If there’s any silver lining, it’s that NKE shares rarely yield this much.

#8: Home Depot

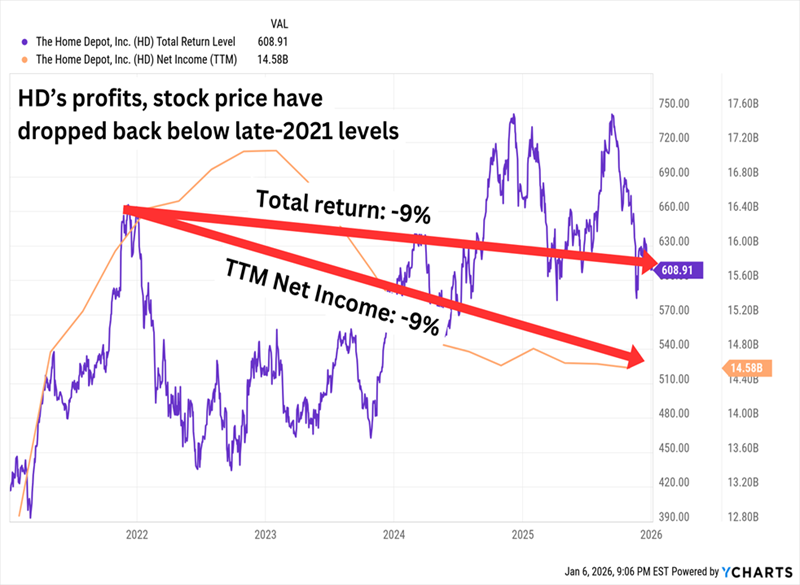

The Skinny: Home Depot (HD, 2.7% yield) is another new Dog for 2026 following an up-and-down 2025 that ultimately resulted in a nearly 10% loss for shareholders. Tariffs are partially to blame here, as are generally more cautious consumers. But we can also point the finger at a stagnant housing market (and an uncertain outlook) that’s keeping a lot of buyers on the sidelines.

What Has to Go Right: The American economy needs a sense of direction. “On the one hand, you look at certain economic indicators, and you say, geez, things are pretty good,” CEO Ted Decker said during the company’s third-quarter earnings call. “You look at GDP, you look at PCE, those are both strong. But on the other hand, what’s impacting us in home improvement is the ongoing pressure in housing and incremental consumer uncertainty.” The U.S. is begging for housing investment; the industry has been underbuilding for years, and nearly three-quarters of the nation’s existing homes are 25 years old or greater. But something must unleash that investment for Home Depot, whose bottom line and stock price have gone stale.

Home Depot Isn’t Building Much of Anything Lately

#7: UnitedHealth Group

The Skinny: The third new Dog, UnitedHealth Group (UNH, 2.7% yield), was already staring at uncertainty heading into 2025 after its CEO, Brian Thompson, was shot and killed in December 2024. But Wall Street didn’t turn on the stock until April, when the company drastically cut back its annual earnings forecast because of high medical costs in its Medicare Advantage plans. It was hardly the only health insurer to suffer, but the pain was most acute at UNH as the nation’s largest provider of the private Medicare plans.

What Has to Go Right: A lot. The same pressures that weighed on UNH are expected to remain persistent in 2026—namely, the high medical utilization that’s tamping down profit margins. The company has also had to shuffle its C-suite, including bringing former CEO Stephen Hemsley back to run the ship. But the administration seems focused on driving down this insurer’s margins to cut costs (and keep inflation low, much like it’s trying to keep energy costs at bay). Like with many of these dogs, UnitedHealth’s yield is near historic highs. But it’s still a sub-3% payday trading at 20 times significantly reduced estimates.

#6: Amgen

The Skinny: Biotech Amgen (AMGN, 2.9% yield) did just about everything it could to get out of the doghouse in 2025, gaining 30% across the year. The stock really took off in November after a beat-and-raise Q3 report, helped in part by a 40% surge in sales of its cholesterol-lowering blockbuster treatment Repatha.

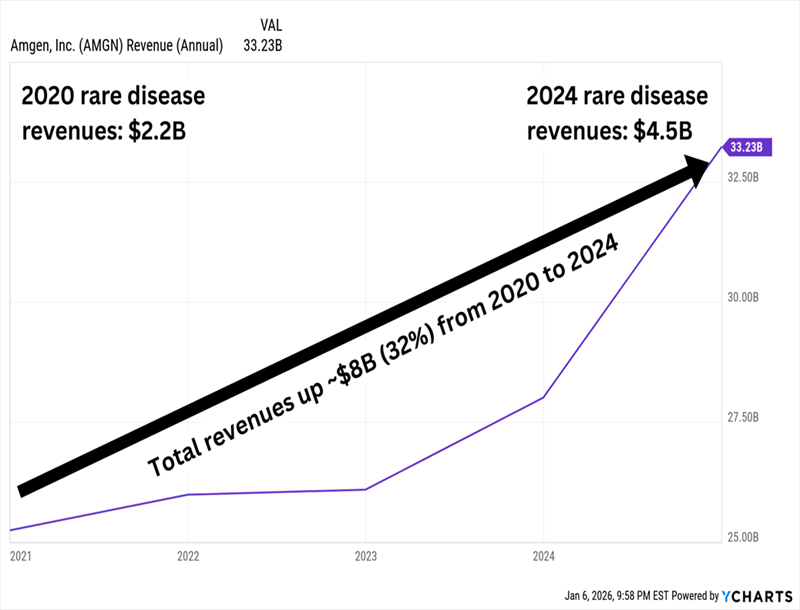

What Has to Go Right: Amgen is, among other things, a play on rare diseases. More than 10,000 exist today, but only 5% have approved medicines. Amgen is one of the most established biotechnology stocks, giving it a blend of R&D and manufacturing know-how to get these drugs to market—and the capital to identify and acquire other potential blockbusters. So for 2026, AMGN just needs to keep doing what it’s doing in growing its rare-disease drug sales. That said, one potential catalyst is an early-stage drug in a pretty crowded space: obesity. Any positive developments from its MariTide monthly injectable for obesity could further propel shares.

Amgen More Than Doubled Rare-Disease Treatment Sales in 4 Years

#5: Coca-Cola

The Skinny: Owners of Coca-Cola (KO, 2.9% yield) had little to complain about in 2025, bringing home a 15% total return from a defensive stock despite a great year for the overall market. Most of those gains came in one big chunk, however—the stock rocketed in February 2025 after a Street-beating Q4 report that showed rising global demand. After that, it didn’t do much of anything despite continuing to post upside surprises throughout the rest of the year. It’s on track to finish the 2025 financial year with low-single-digit top- and bottom-line growth.

What Has to Go Right: Coca-Cola is a master of staying ahead of consumer trends, whether that’s positioning its legacy products or adding to its already enormous stable of brands. I’ve mentioned for a couple of years that a popular worry among KO bears is the rise of GLP-1 drugs—and they could eventually take a more noticeable bite—but for now, even magic diet drugs can’t put a dent in Coke. Obviously, any pickup in global consumer spending could end up being a windfall for Coke. Pullbacks in growthier sectors could also push investors to double up on KO shares, too.

#4: Procter & Gamble

The Skinny: Procter & Gamble (PG, 3.0% yield) entered 2025 as the “last Dog in,” and even a halfway decent 2025 could have kept it off the list this year. Instead, it laid an egg, delivering a slow, steady and substantial 12%-plus loss that, on a total return basis, represented the worst year for P&G shareholders since 2008. We might expect some underperformance from defensive consumer-staples names when the market keeps setting new highs, but deep red ink? The problem for Procter & Gamble is that 2025’s bull market came despite weakening consumer spending. And while that might seem like a recipe for many staples names, P&G is premium-priced in many categories—and when the going gets tough, the tough start stocking up on Walmart (WMT) and Costco (COST) white-label products instead.

What Has to Go Right: For one, the market could recognize that while things aren’t exactly rosy for Procter & Gamble, the arrow is still pointed in the right direction—the company’s full-year 2025 results, due out later this month, are still expected to show improvement on the top and bottom lines, and the pros expect the same for 2026. P&G is showing strength in emerging markets including China and Latin America. Meanwhile, the company is eyeing an eventual national launch of its Tide evo “laundry tiles” among other updates to its product lineup. Another healthy bump to the dividend wouldn’t hurt, either, and PG has the room to do it.

PG’s Dividend Has a History of Picking Up the Stock Price

#3: Merck & Co.

The Skinny: Merck & Co. (MRK, 3.2% yield) started last year in the middle of a slide and kept on slipping, eventually losing 45% of its value between June 2024 and May 2025. That’s largely because Merck’s status as a monster drugmaker has been built on a mighty unsteady frame. Specifically, a single product—Keytruda—accounts for a little less than half the company’s revenues. It’s one heckuva drug, approved for some 40 indications covering about 20 different cancers. While it won’t start to lose exclusivity until late 2028, Wall Street has started to fret over the company’s ability to fill that sales hole. All that said, things looked a lot less bleak in the second half of 2025, with shares rebounding by about 40% off the bottom and finishing the year with a total return of about 10%.

What Has to Go Right: The same thing that started to go right in 2025: Wall Street believing that Merck has solved “the Keytruda problem.” Part of that includes finding new uses for Keytruda, including positive recent trial data on its use, in combination with Pfizer’s and Astellas’ Padcev, to treat muscle-invasive bladder cancer. It’s also launching a faster-acting version of the drug: Keytruda Qlex. But outside of that, MRK now has 16 cancer treatments in late-stage trials, and it has made deals to acquire companies such as Verona Pharma and Cidara Therapeutics to further shore up its pipeline.

#2: Chevron

The Skinny: Chevron (CVX, 4.5% yield) largely survived 2025’s “Liberation Day” drop in oil prices, posting a total return of about 10% across a rocky year for the entire energy sector. The announcement of massive tariffs on most of America’s trading partners sent the commodity plunging by about 15% last spring—even though oil itself wasn’t a target of the levies, fear of the global economy grinding to a halt dragged oil into the dirt. CVX shares spent the rest of the year playing catch-up. Worth noting: Chevron’s last earnings report of the year, in late October, showed booming production in the wake of its Hess acquisition, which closed in July.

What Has to Go Right: Chevron is a victim of its own generosity, doomed to remain a Dow Dog barring an unforeseen catalyst that could double CVX shares overnight. That’s unlikely, of course—even if oil and natural gas prices skyrocketed, the wide-ranging nature of this integrated oil giant wouldn’t benefit as directly as a lot of pure-play energy E&P firms would. Also, the sector has been thrown a serious curveball just a few days into 2026. America’s ouster in Venezuela initially sent the energy sector aloft amid President Donald Trump’s suggestions that he would open the country’s oilfields for business. Chevron is the only American firm that currently operates in the country, and even then under a license that only allows for limited production. But even assuming a much friendlier environment for U.S. firms, experts estimate it would take tens of billions of dollars of investment and many years to meaningfully ramp up production.

#1: Verizon

The Skinny: Verizon (VZ, 6.8%) continued to squeeze blood from a stone for yet another year. It’s on pace to deliver low-single-digit revenue and earnings growth for full-year 2025. Management took its meager profit growth and delivered a 2% bump in the payout. And shares appreciated by just about as much—of course, the total return looked a lot better thanks to the outsized distribution. That doesn’t sound like much to get excited about, but that’s a relatively good year for a company whose stock has lost 13% of its value (on a pure price basis) over the past decade.

What Has to Go Right: At least someone isn’t satisfied with the status quo. “When I look at our performance objectively, Verizon is clearly falling short of our potential,” former PayPal CEO Dan Schulman, who took the reins at Verizon in October 2025, said amid the company’s third-quarter earnings report. “Our primary objective is to build loyalty and drive significant improvements in retention … Verizon will no longer be the hunting ground for competitors looking to gain share. We are reinventing how we operate to make Verizon more agile and efficient.” It’ll take a lot more than fresh, angry blood in the C-suite, of course. Verizon has been trying to secure its subscribers with three-year price locks and better customer service. Meanwhile, VZ remains dirt-cheap at 8 times next year’s earnings, and its 7% yield is in a different area code compared to most blue chips.

5 ‘Don’t-Miss’ Dividends That Could Double Every 5 Years

Stout, unloved dividend payers? That’s my love language.

It’s simple: We buy boring, underappreciated stocks that raise their dividends, then wait for those dividends to inevitably pull shares higher over time. In fact, this simple relationship between dividends and price gains holds the key to 15%+ returns per year from conservative investments.

It’s not flashy. It doesn’t give CNBC’s talking heads anything to chat about. But it works.

In fact, I even rely on one of these boring Dow Dogs to help build my wealth over time. It’s one of five “Hidden Yield” investments that are poised to soar while dishing out solid income.

I see these stocks delivering 15% annualized yearly returns over the long run—that’s enough to double your investment every 5 years.

All 5 stocks are at “low ebb,” making now the perfect time to buy. Click here and I’ll walk you through these 5 robust dividend growers and give you a free Special Report revealing their names and tickers.