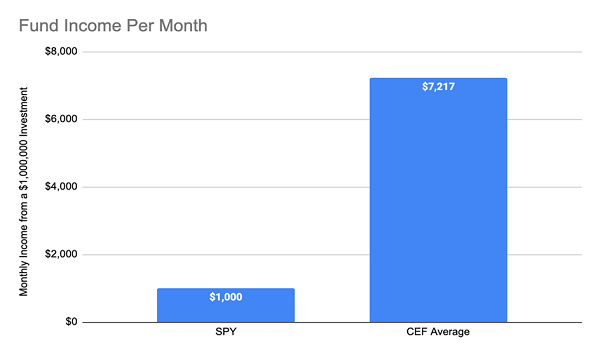

The thing most people love about closed-end funds (CEFs) is, well, pretty straightforward: the dividends! With these income plays kicking out average yields of 8.7%, they really can go a long way to helping us secure a safe retirement.

Beyond that, though, there are many other reasons why CEFs should be in your portfolio. Access to a collection of high-quality assets, for example, since CEFs are well-regulated and hold a wide range of assets, including stocks, bonds and real estate investment trusts (REITs).

Still, with yields that high, it’s fair to wonder if CEFs’ payouts might not be sustainable over the long haul, especially since S&P 500 index funds yield just 1.3%. How can CEFs, while investing in the same kind of assets, yield over six times as much?

There are three quick answers to these questions:

- Truth is, many CEFs do pay too much, which is why picking the right CEFs is critical.

- Since the S&P 500 has earned a total return above 8.7% in the last decade, CEFs can cover their dividends simply by returning market profits to investors.

- Since CEFs trade at an average 5.8% discount to net asset value (NAV, or the value of the assets they hold), that 8.7% yield, which is based on the discounted market price, translates to 8.2% based on NAV. That’s more manageable, and more severely discounted funds have even more sustainable discounts.

Source: CEF Insider

But how can we separate the strong CEFs from the pretenders?

One supposed “signal” that often catches the eye of less-experienced CEF buyers is “return of capital,” or ROC. This, on the surface, sounds like these fund managers are taking your money, charging a fee and then just handing your capital back to you.

This is a common misunderstanding of ROC that misses the fact that it can be (and often is) good for investors. “The negative stigma of ROC is often unwarranted,” noted David Schachter in a December email interview. Schachter is the VP of several Gabelli CEFs and ombudsman for the Gabelli Utility Trust (GUT) and GAMCO Natural Resources, Gold & Income Trust (GNT).

The main reason for this is that, while ROC sometimes is just an investment returning your money minus fees, that’s rarely the case with CEFs, and it’s never the case with high-quality CEFs. In those instances, ROC is a function of accounting rules set up by the IRS that fund managers can use to lower investors’ tax burden.

Schachter notes that this is how GNT passed on profits and passive income to shareholders with a lower tax burden than they would’ve faced without ROC: “Last year, in 2023, GNT saw its NAV return +9.8%. The distribution was 87% tax-free ROC,” Schachter points out. That meant lower tax burdens for GNT shareholders.

Now, you might be wondering: What’s the difference between “good” and “bad” ROC? Bad ROC is easy: That’s when you hand over cash and the fund just hands it back to you, minus fees.

Good ROC is a bit more complicated, so let’s take an example.

Source: CEF Insider

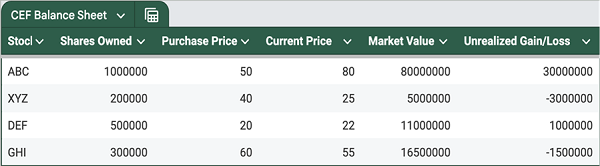

Imagine this hypothetical CEF holding shares in two similar companies (ABC and XYZ) and two other kinds of companies, DEF and GHI. The fund is sitting on big profits from ABC, smaller profits from DEF, and some losses from XYZ and GHI.

Despite the losses, the fund’s management thinks GHI still has short-term profit potential and XYZ has long-term profit potential, while DEF is expected to keep going up, but at a faster pace than ABC, given its recent runup.

Now let’s say the fund needs to distribute $2 million to shareholders as dividends. The prudent thing to do would be to sell ABC to take profits, but that on its own would be a taxable act. So, the fund does this:

![]()

Source: CEF Insider

Here we see the fund selling 100,000 shares of its one-million-share position in ABC to raise $8 million in cash (including $3 million in profits) to pay that $2-million dividend. But the fund also sells 200,000 shares of XYZ to raise $5 million (and realize the $3-million loss) it accrued from that stock and reallocates $2 million of cash to DEF and GHI.

Now the fund has no capital gain at all, so it can distribute $2 million to shareholders and, as far as the IRS is concerned, that $2 million is a return of capital. The fund also has $9 million in cash that, once the wash-sale rule (which states a set time when you can’t buy back shares you’ve recently sold and realize a tax write-off) expires 30 days after this transaction, the fund could invest in XYZ or, if it wanted, into any other stock.

The picture you see here is one of an act of balancing winners, losers and the tax code to maximize shareholder benefit and minimize tax costs. This can be a big deal if you’re investing in an account that isn’t tax advantaged, especially if you’re in a higher tax bracket.

These 5 MONTHLY Dividend Funds (Yielding 10%) Are My Top 2025 Buys

As you can probably tell, for maximum gains (and dividends!) and tax efficiency, we MUST make sure our CEF managers know their stuff.

Here’s one thing I can tell you for certain: The managers of the 5 monthly paying CEFs I’m pounding the table on now are the best of the best: Savvy pros who’ve been in the game for a while—and know how to find the best stocks, bonds and other assets to buy while keeping the fund’s tax situation tight.

The result? More profits (and dividends) for us! These 5 funds also top the CEF average dividend, kicking out an incredible 10% annualized yield as I write this.

Don’t miss your chance to buy these 5 top-flight monthly payers cheap. Click here and I’ll tell you more about them and give you a free Special Report revealing their names and tickers.