Here’s one thing most folks get wrong about dividend cuts: They can (and often do) set up terrific buying opportunities!

I know, I know. Before our customer-service inbox lights up here at Contrarian Outlook, let me be clear that we dividend investors hate payout cuts. No one wants to see their income stream and their investment take a hit, as scorned investors toss the stock.

But buying a dividend after a cut (or even before, under the right conditions) can be a winning move. It’s a setup that reminds me of the words of Howard Marks, the most successful investor no one has ever heard of (except Warren Buffett, who is a fan).

Marks wrote (and if you’re a regular reader, you’ll probably find yourself nodding along with the following quote):

The ultimately most profitable investment actions are by definition contrarian: You’re buying when everyone else is selling (and the price is thus low) or you’re selling when everyone else is buying (and the price is high).

But he admits this isn’t easy:

“These actions are lonely and uncomfortable.”

To see what I’m getting at here, consider 3M (MMM), which announced a 44.6% chop to its quarterly dividend on May 14. You’d think that would be the death knell of the stock, right? After all:

- 3M had paid dividends for more than a century before the cut.

- The company had raised its payout for 64 straight years.

- 3M was a charter member of the Dividend Aristocrats, the stocks that have raised their payouts for 25 years or more. Given its history, 3M could’ve joined this group twice!

With all that in mind, you’d expect anyone who bought in the weeks before the cut to get burned.

Not so.

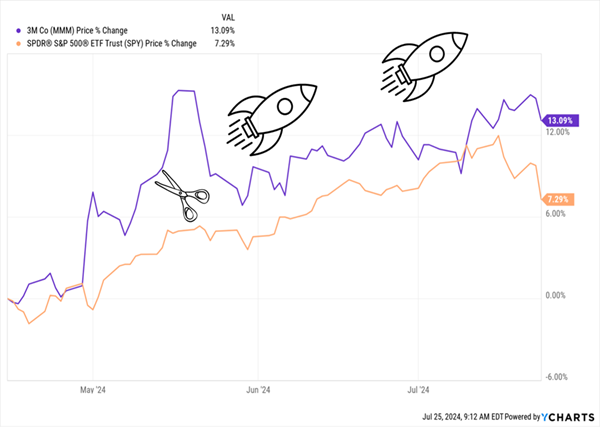

If you’d bought 3M just a month before the cut was announced, you’d have booked a 13.1% gain in the little more than three months from then until July 24—almost doubling the S&P 500.

Investors Who Bought Before the 3M Dividend Cut Beat the Market

And this was before 3M reported blowout earnings on July 26, sending the stock soaring double-digits from here!

So what happened? In this case, the cut was part of a bigger story.

For one, the company was getting set to spin off its medical-devices business, now called Solventum (SOLV), a move it’s completed, save for the 19.9% of Solventum it’s hanging on to for now.

The company was also facing two lawsuits—one over earplugs it sold to the US military and one over its use of so-called “forever chemicals,” which don’t break down easily, found in drinking water.

It settled both in March, at a total cost of around $16 billion. But 3M has long timeframes in which to pay and the company’s cash flow can easily handle these. Management also says it has recorded reserves to pay them.

With all that in mind, when the dividend cut landed, it took away uncertainty around the stock, kickstarting that big gain.

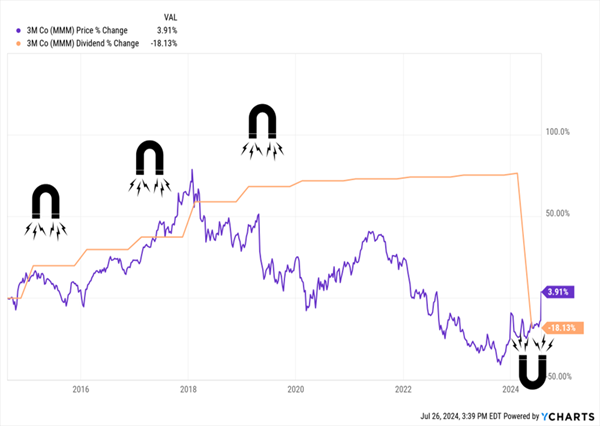

Finally, there’s the “Dividend Magnet” to consider. As you can see below, 3M’s share price tracked its payout higher until around 2019, when it fell off the pace. The dividend cut wiped that out, matching the payout growth with the share price again.

Dividends and Share Prices Always Meet—One Way or Another

Except now, with last week’s earnings-driven price gain, 3M stock is running ahead of the payout once more. With that in mind, I don’t recommend buying the stock today.

But don’t worry! There is another stock I see as a terrific opportunity now. It cut its dividend back in 2020 and has been out of favor ever since. But the selloff looks overdone, and it’s only a matter of time before the stock “catches up” to its dividend (and not in the way 3M’s did!).

Dominion: A “Dividend Magnet” Play That Outshines 3M

I’m talking about Virginia-based utility Dominion Energy (D), which has 4.5 million electricity and gas customers across 13 states, from North Carolina to Utah.

Income investors hold “Big D” in even higher esteem than 3M because the stock’s 5.1% yield, nearly double 3M’s 2.7%.

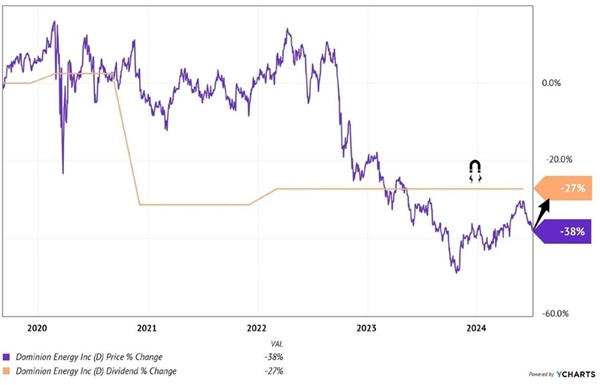

Dominion cut its payout in 2020, and the stock was eventually punished, though it took a while. As you can see in the chart below, it wasn’t until interest rates peaked in mid-2022 that the stock’s dive hit its steepest pitch.

Dominion’s “Lagging” Stock Sets It Up for Extra Upside

That makes sense, as most investors see utilities as bond proxies: When rates rise, bond prices fall. Same goes for utility shares. But this selloff looks overdone. And as you can also see above, the utility has some upside to catch back up to its payout. That’s our opportunity.

Why the 2020 chop? Too much debt, of course. Dominion had embarked on an acquisition binge in the name of growth. Which, ironically, backfired.

The result was a rare payout slash from a utility—an income investor’s worst nightmare. That’s why first-level investors keep Dominion in the doghouse today. Which intrigues us here at Contrarian Outlook. Did we hear doghouse?

“Measure Twice, Cut Once”

With dividend cuts, it’s key to bear in mind that chief financial officers are like carpenters. It’s best if they measure twice and cut only once. As a result, the safest dividend is often the one recently cut.

Unless management is a complete clown show (which Dominion’s is certainly not), the last thing they want is to be forced back into that particular dentist’s chair!

As I mentioned, Dominion yields 5.1% today. It rarely pays this much. The fact that the stock is lagging its payout makes now a good time to buy—and lock in that high yield while we wait for our Dividend Magnet–powered upside to kick in.

5 More “Hated” Stocks With BIG (and Growing!) Dividends to Buy Now

Unloved stocks like Dominion, which boast high yields and stable payouts set to grow, are smart buys anytime. And when a pullback hits (which let’s be honest will likely happen later this year or next), they’re absolute portfolio gems.

Here’s why:

- They keep your high—and growing—payout stream rolling in, no matter what.

- Because they’re already cheap, they have limited downside. And they often lead the charge when markets turn higher again.

I’ve put together a free Investor Report naming 5 more stocks with all of these strengths. They’re urgent buys now and, because of their “recession-resistant” businesses, I’ve got them pegged to deliver 15%+ annualized returns for years to come!

Don’t miss this chance to buy these 5 dividend growers now, before their prices race away from us. Click here to get the full story on all 5 and how to download your free Special Report revealing their names, tickers and my latest research on them.