Look, this deglobalization trend is hitting high gear—and if you miss your chance to tap it for surging dividend payouts, you will regret it down the road.

After all, it’s megatrends like this one that we contrarian income-seekers live for. Let the “basic” investors sweat headline-driven fears like rising rates and recessions. We’ll happily lock in our “megatrend” dividends and ride along for years, and even decades, as our payouts soar triple-digits!

Really, terms like “deglobalization,” “onshoring” and “friendshoring” are just fancy ways of talking about the flow of manufacturing jobs back to the US, or to US neighbors like Canada and Mexico, from basket cases like Xi’s China.

Just in August, First Solar (FSLR) announced a new $1.1-billion facility in Louisiana, and Northrop Grumman (NOC) said it would open a plant in Maryland to make propulsion systems for hypersonic missiles. And in September, EV-battery maker Gotion said it would open a $2-billion plant in Illinois.

And these are just some of the big announcements we’ve seen, according to research firm IndustrySelect. There have been dozens of smaller plants and expansions rolled out in just the last few months, too.

With each of those factories “baking in” decades of higher demand in their local economies, we’re going to play it through a couple terrific “pick and shovel” plays. That’s a strategy we love at my Hidden Yields dividend-growth service. The term “pick and shovel” goes back to the California gold rush and refers to the fact that it was the folks who sold supplies to the miners, not the miners themselves, who really struck it rich.

So it goes with the two “stealth” deglobalization plays we’ll talk about next:

When a New Factory Opens, Cintas Gets the Call

Cintas (CTAS) churns out work uniforms, mats, cleaning supplies and first aid and safety products. Boring? Certainly. But this is essential stuff in plants across the land—including all those new ones.

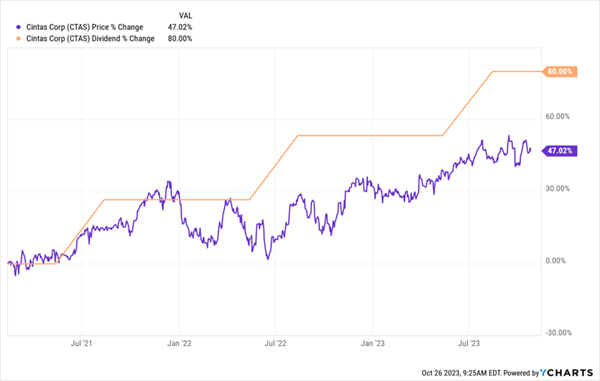

That’s driving the uniform maker’s sales higher—and translating into rapid dividend growth. Even though the stock yields just 1% today, it’s hiked the payout an incredible 80% since early 2021.

As you can see below, the share price (purple) kept pace with the soaring dividend (orange) until it broke away last year. That’s good news for us because share prices tend to catch up to a stock’s dividend growth over time—a phenomenon I call the Dividend Magnet.

“Dividend Gap” Says CTAS Stock Could Nearly Double

We can expect Cintas’s payout to keep powering higher: Its dividend only accounted for 37% of its last 12 months of free cash flow—far below my 50% “safety line”—and its sales are soaring, up 8% in the latest quarter. Earnings per share also popped some 9%.

Debt is no problem for Cintas, either. It’s sitting on about $2.5 billion of long-term borrowings, just 28% of assets and a mere 5% of its market cap. Peanuts!

Finally, Cintas is focused on the US and Canada, making it a pure play on onshoring and friendshoring—and freeing it (and us) from worries that the strong dollar will drain its profits.

Casey’s: Another “Stealth” Deglobalization Play

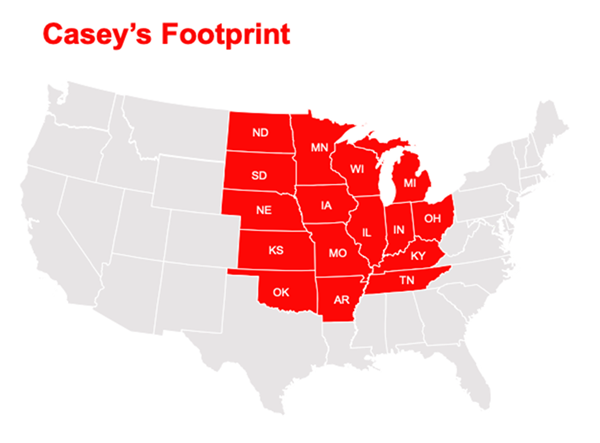

Casey’s General Stores (CASY) might seem like an unlikely play on onshoring, as it sells food and fuel through its 2,500-strong convenience-store chain, the third-largest in the US. But stick with me for just a second here, and I think you’ll see the connection.

We like Casey’s because, like Cintas, it operates right where most of these new plants are going, in states like Ohio, Michigan, Indiana, Kentucky and Tennessee.

Source: Casey’s September 2023 investor presentation

In other words, many of those new employees will be stopping for coffee and gas at a Casey’s on the way to work, then putting on a Cintas uniform when they get there! The company also boasts some other dividend stats that are very appealing indeed:

- Relentless dividend growth, with a payout that’s up 139% in the last decade.

- A low payout ratio, with the dividend accounting for just 15% of the last 12 months of free cash flow. That means Casey’s could boost its payout by 200%+ tomorrow and it would still be safe.

We love stocks with hidden value like Casey’s because it drives the share price higher as more investors come around. And management has tons of options for unlocking that hidden value, like a big dividend hike, a special dividend or an acquisition—and there are plenty of targets for Casey’s in the fragmented convenience-store market.

Meantime, Casey’s continues to take market share by adding new outlets, with plans for 150 in its 2024 fiscal year. Its balance sheet, with just $1.65 billion of long-term debt—a mere 27% of assets and just 16% of its market cap—can backstop that growth and the company’s soaring payout, too.

5 More “Megatrend” Dividends Returning 15% a Year (Bull or Bear)

We love megatrends that last years—and better yet decades—because the stocks driving them, like Casey’s and Cintas, are essentially “baked in” to ride higher over time, no matter what happens with the economy and interest rates.

In fact, any short-term pullback is a buying opportunity—a chance to get on the bus before they snap back to their megatrend-powered growth trends!

We’ve got just such a window in front of us now, thanks to the slow recovery from the 2022 mess. And I want to make sure you have the very best picks at hand to take advantage.

I’ve prepared a Special Investor Bulletin spelling out the details on this opportunity, and I don’t want you to miss it. Click here to learn more about our strategy and get an opportunity to download a free Special Report listing my 5 top “megatrend” dividend payers to buy now.