What could be better than receiving a raise every year? How about getting more cash in your pocket, and increasing your net worth?

Owning high-quality REITs (real estate investment trusts) with track records of consistently growing dividends is a proven strategy that delivers income today and rewards you with attractive gains for retirement, too.

Let’s consider three well-known REIT names to show how dividend growth can drive price appreciation, and generate outsized returns. There is no magic formula. It really boils down to common sense. A dividend cut or stagnant pay-out can spell disaster, while a growing dividend rewards investors two ways.

Well-Covered Dividends Matter

Real estate investment trusts own hundreds or even thousands of properties, with an enormous number of restrooms, parking lots and roofs that must be maintained. Savvy investors check to see that there is a margin of safety to pay the dividend after these expenses.

Each year when a tenant moves out of an apartment building money needs to be spent to refurbish the space. In an office building tenants typically move every three to five years. It can require a lot of cash to remodel the space for the next tenant. Additionally, landlords must pay the brokerage commission up front for the entire lease term.

It is important for REITs to generate extra cash on top of the money they pay out in dividends each quarter. That is why there is an old saying: “The safest dividend is the one that was just raised.”

Owning the Safest Real Estate

Net-lease REITs are popular with income-focused investors because the business model is so simple, it is “bond-like.” While bonds just pay investors a fixed yield, these REITs can also grow earnings from contractual rent increases that help keep up with inflation.

REITs own freestanding single-tenant properties like convenience stores and drugstores, where the leases are signed for ten, fifteen or even twenty years.

But, the news gets even better.

These leases are usually “triple-net.” In addition to monthly rent, creditworthy tenants pay all the taxes, insurance, utilities, and most building maintenance. No fuss, no muss. It is cash flow investors can count on.

2 Dividends to Buy, 1 to Avoid

Have you ever thought about who owns those fancy Walgreens and CVS drugstores located on the best corners?

They’re owned by three of the most popular names in the space:

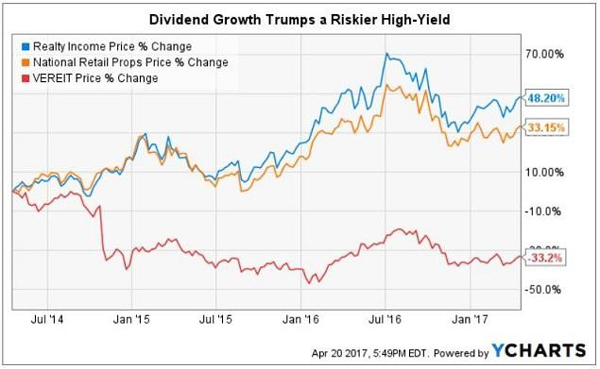

- Realty Income (O) – $16.8 billion market cap, 4.1% dividend yield.

- VEREIT (VER) – $8.65 billion market cap, 6.2% dividend yield.

- National Retail Properties (NNN) – $6.75 billion market cap, 4.0% yield.

Vereit pays the highest yield. It’s 50% higher than the other two large cap net-lease REITs.

However, when we consider price performance, we see that the big dividend isn’t helping:

The chart tells an entirely different story when it comes to safety of principal and price appreciation. We like dividends – but we also want to make sure our capital is secure. Here’s where Vereit fails.

A Closer Look

Vereit shareholders have had to deal with the aftermath of poor decisions made by the former ARCP management team. Over the last two years, CEO Glen Rufrano and his team have improved corporate governance and strengthened the balance sheet by selling non-core assets.

However, during the last two-years there has been zero dividend growth, after a painful cut in 2014. One of the reasons for a stagnant dividend is that 86% of all available cash is already going toward the dividend.

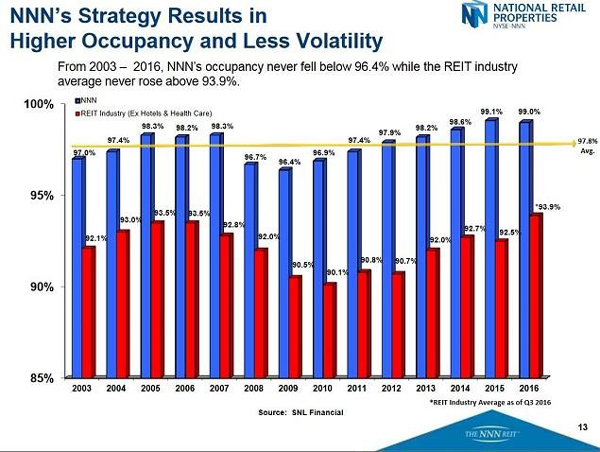

Contrast this “dead dividend” with National Retail, one of the few true “Dividend Aristocrats.” NNN has raised its dividend for 27 consecutive years. There are only 94 out of 10,000 companies that can make that claim. This dividend growth juggernaut pays out just 78% of free cash as dividends.

NNN shareholders continued to get a raise during the global financial crises.

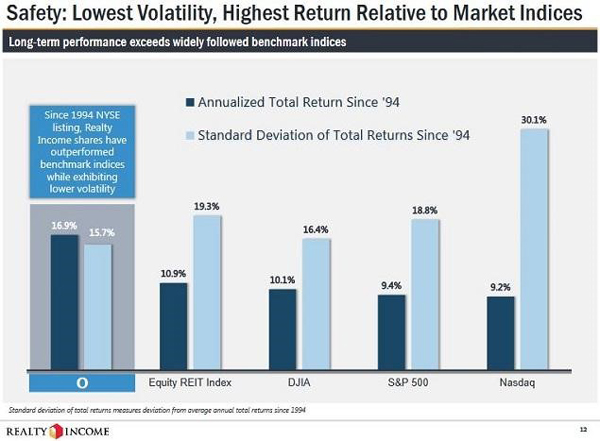

How about Realty Income? This REIT is also called The Monthly Dividend Company for a reason. Last week, Realty Income announced its 562nd consecutive monthly dividend since the IPO in 1994.

Realty Income continued to pay and grow its distribution every year including the Great Recession. This has resulted in considerable outperformance for “O” shares compared with almost any other asset class.

Balance Sheet Strength

Vereit has made great strides in its balance sheet and portfolio transformation. However, this has been accomplished by shrinking the pool of assets, rather than growing them. Moody’s recently raised its rating to Baa3 for Vereit, which will help it to borrow at lower rates going forward. A BBB- balance sheet is a huge step in the right direction for patient VER shareholders.

Meanwhile, Realty Income and NNN both have fortress balance sheets with ratings of BBB+/Baa1 from all the major ratings agencies. You can have confidence that the dividend check will be there like clockwork. Shareholders get a raise at least once a year, which also helps to grow your nest egg.

This “Best of Both Worlds” REIT Pays 7%

While O looks like a better buy than it was a year ago, it still only pays 4.1% today. Here’s a way for you to bank 7% current yields with some upside too.

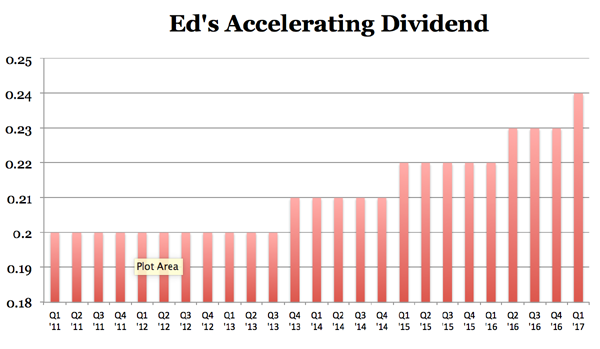

This “best of both worlds” REIT has come a long way since its CEO, Ed, founded the firm fourteen years ago. He admits that back then he had: “zero assets, a dream, and a business plan.”

His dream and plan were plenty – Ed parlayed them into $6.7 billion in assets!

His investors have enjoyed 86% total returns over the last five years (with much of that coming back as cash dividends.) And right now is actually a better time than ever to “bet on Ed” because his growing base of assets is generating higher and higher cash flows, powering an accelerating dividend:

Yet for several shortsighted reasons, Ed’s stock is such a bargain that it pays a gaudy 7% yield today. Much higher than usual.

This stock should be owned by any serious dividend investor already, for three simple reasons:

- It’s recession-proof and rate-proof,

- It yields a fat and secure 7%(!), and

- Its dividend increases are accelerating – and this is typically a cue that big price gains are ahead.

Which is why you need to buy Ed’s stock right now – before its price gets bid up (and its yield gets compressed). We also have two more rate-proof REITs that we love right now, hidden gems actually paying 8% and 9% respectively thanks to similar headline-driven hysteria. In fact, all three are core recommendations in our “No Withdrawal” portfolio. Click here for all the details and learn more about our favorite 7% to 9% REITs.