PIMCO recently cut the dividends of two of its popular closed-end funds (CEFs). Shareholders took a bath and, honestly, none of this was a surprise to us careful contrarians.

The payout cuts themselves were not the reason for the bludgeoning. PIMCO Strategic Income Fund (RCS) reduced by 22% but still yields 7.4%. PCM Fund (PCM) cut by 20% yet it pays 11.5% post-chop.

Yet shareholders down 13% and 12% respectively in the past month are now searching for meaning in their empty dividend lives. Fast double-digit losses are obviously not what these income-hopeful investors signed up for.

Alas, hope is never a good strategy and those that were burned obviously did not research these paper payout tigers in Contrarian Outlook. Yours truly has been warning about RCS for years (see my “do not buy” labels here and here). Since we last trashed RCS it went on to return a piddly 10% over five-and-a-half years. Which is less than 2% per year. Not good from a supposedly safe bond fund.

The fund’s cardinal sin? A premium so high that perfection was priced in. From the wayback machine:

Investors are currently paying $1.37 for a dollar of assets in PIMCO’s Strategic Income Fund (RCS). Maybe it’ll work out for them, but high-priced CEFs are similar to high-flying stocks with big price-to-earnings ratios. What’s to say RCS won’t fetch a “mere” 9% premium someday? That’d be a 25% price haircut from today’s levels.

Turns out it was a 13% price haircut, though the lackadaisical returns leading up to the trim may have “pre-thinned” the target.

Surely vanilla investors have learned their lesson and RCS has been knocked down to par, right? Wrong. RCS trades at a 43% premium to its net asset value (NAV) as I write. Forty-three percent! This means, post-divvie cut, the fund is trading for $1.43 on the dollar. Yikes.

Granted, PIMCO is a first-grade bond shop. Bond King Bill Gross’s successor Dan “The Beast” Ivascyn runs the show and has bestowed royal riches on many PIMCO CEFs during his reign. There really are no bad PIMCO CEFs, but there are bad prices.

RCS fetched a downright offensive markup late last year, averaging a 63% premium over the last six months. The fund was trading for $1.63 on the dollar and now it is trading for “only” $1.43. More trouble could be ahead with a nosebleed valuation like this.

Granted RCS is fine as far as bond CEFs go. The fund has generated 7.7% total returns since inception. It is a big player in the agency mortgage-backed security (MBS) market with more than half its portfolio stacked in MBS’s. I don’t love the overallocation to MBS’s, which tend to underperform when interest rates are rising (and the housing market stalls).

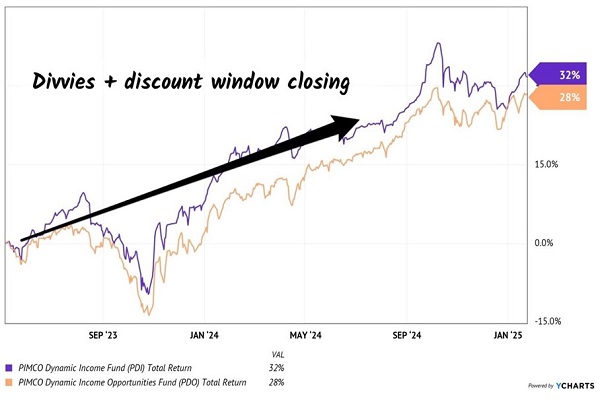

My preferred PIMCO funds are PIMCO Dynamic Income Fund (PDI) and PIMCO Dynamic Income Opportunities Fund (PDO), which have more modest MBS allocations (about 25% each). PDI and PDO are bigger players in high-yield credit, a fixed-income area I do like right now because it does well when the economy is strong.

PDI has also led its PIMCO peers historically, returning 11% per year since inception (outstanding!). PDO has lagged but has (conveniently) picked up momentum since we began talking it up and has actually been the best performer of the bunch over the past year.

I’ll highlight these gains in a moment, but let’s check the premiums first. (Remember, no bad PIMCO funds, only bad prices.)

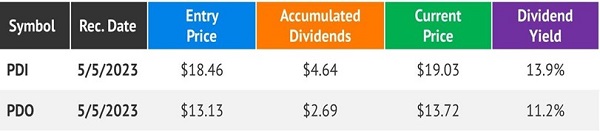

PDI trades 11% above par—not the delicious discount the fund fetched when we added it to our Contrarian Income Report portfolio in May 2023, but not a bad price either. Let’s call it an OK price for a great fund.

I am giving PDI a “premium hall pass” here because I am anticipating the 10-year Treasury yield will grind sideways or lower in the months ahead. This alone will lift PDI’s NAV (net asset value).

PDO likewise has levitated to a 5% premium from a discount when we added it to CIR as well in May ’23. The discount-to-premium flip has helped our total returns by boosting prices:

Rad Returns from Safe Bonds

Of course, as income investors we want most of these returns to come to us as payouts. In less than two years, PDI has returned 25% of our initial purchase price as divvies. PDO, meanwhile, has already given us 20% back. Sweet.

Now, am I worried about dividend cuts? Not really, and here’s why. First, a 20% payout reduction still has these funds dishing 11% and 9% respectively. We can live with those yields.

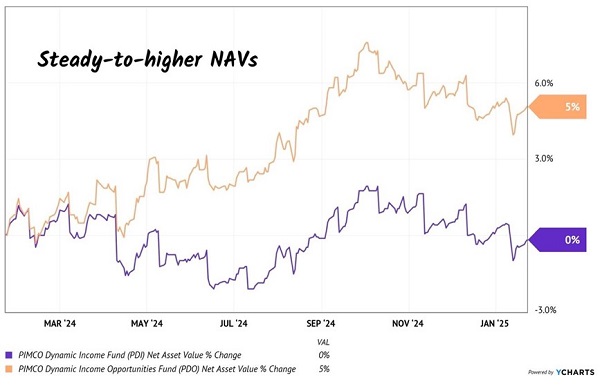

Second, the NAV of these funds is fine. PDI has been steady year-over-year while PDO’s NAV has popped 5%. Often when dividend cuts are brewing, NAVs will “tip off” the news because management taps them like a piggy bank to make its monthly payout.

PDI and PDO NAVs—Last 12 Months

Granted since October, their NAVs are down because the 10-year yield has risen. As I mentioned, a reversal of this key benchmark rate would provide a NAV—and price—catalyst.

But there are 3 other high-yields that I like even better than these PIMCO funds right now.

And these “retirement-changing dividends” dish payouts up to 10% every single month.

We’re talking about great income investments trading at excellent prices. Don’t miss out—details on my “8%+ Monthly Payer Portfolio” are waiting for you here.