Would you believe, my fellow contrarian, that most of our vanilla income friends settle for utility dividends that pay quarterly?

Ha!

Unfortunately (for them) that’s no typo. There are millions of investors just like them who are OK being paid every 90 days.

Yes, ninety!

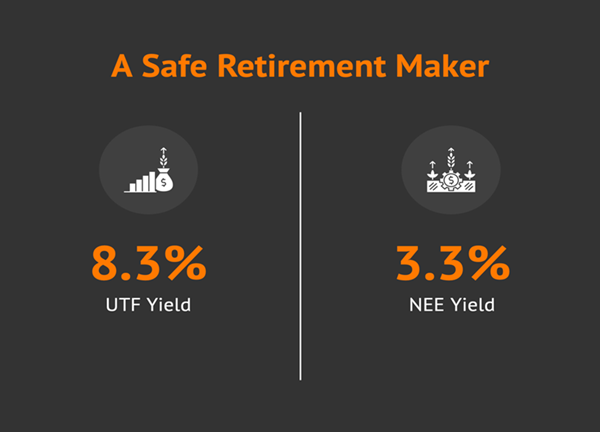

Obviously, they don’t read highbrow publications like Contrarian Outlook, where we highlight monthly dividend payers. Today we’ll discuss two that pay 8.3% and 8.6% respectively.

With yields like these, we can actually retire on dividends. Take a chunk of money that we’ve saved up and convert it into regular cash flow. A million dollars, for example, can become $83,000 or $86,000 annually in dividend income.

The original cash pile stays intact. In reality, it does better than intact. I’ll explain why. Plus, our payouts are delivered every month. Up to $7,166.67 on our million, to be specific.

Most investors aren’t sophisticated enough to take advantage of these “retirement makers.” Even friends we may care enough about to send these articles to! They will buy something safe like NextEra Energy (NEE) and call it a day.

And granted, good for them. NEE is a compelling value here. The stock yields 3.3%. It pays every 90 days, plus likely has some price upside.

But what if we need more income now?

Then we take the elevator to the second floor for a second-level income approach. Here, we consider Cohen & Steers Infrastructure Fund (UTF). UTF is my ‘go to” utility play because, as a closed-end fund (CEF), its mission in life is to dish us a generous dividend.

One of the fund’s top holdings? You guessed it, NEE.

As a CEF, UTF is also allowed to use leverage to boost NEE’s payout. The fund yields 8.3%. Now we’re talking.

UTF’s “cost of money” is about to go down, by the way. It has increased with every Fed rate boost, but the Fed is finished hiking. Each rate cut will likewise reduce the bill for UTF’s 30% leverage.

The fund’s cheap money is about to get even cheaper because…

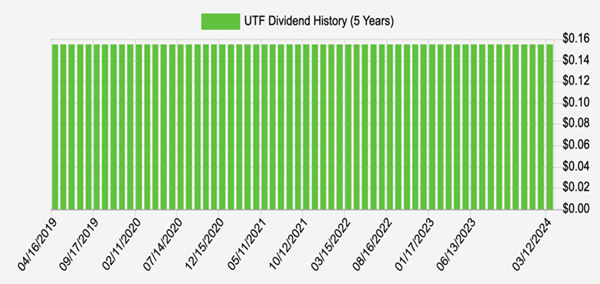

One share will set us back some $22 and change. For that, we’ll receive 15 and a half cents per month, every month.

UTF Pays 15.5 Cents Per Month, Every Month

Source: Income Calendar

If UTF sounds interesting, consider right now a good time to beat the rush. As I write, Wall Street is assuming that the Federal Reserve will stick its “soft landing.” Which is notable because the Fed rarely sticks the landing. It usually breaks something in its rate-setting process.

(The housing market often slows down first. This has already happened. Meanwhile commercial real estate is a bit of a ticking time bomb, with everyone working from home. The “threatdown” is real.)

Let’s say the economy stumbles. The Fed will cut rates. Speculative AI stocks will tank. Money will flow into the safest stocks like utilities.

UTF will pop more than most because its cost of capital will decline rapidly with each rate cut. Plus, it’s a (responsibly) leveraged bet on the utility sector.

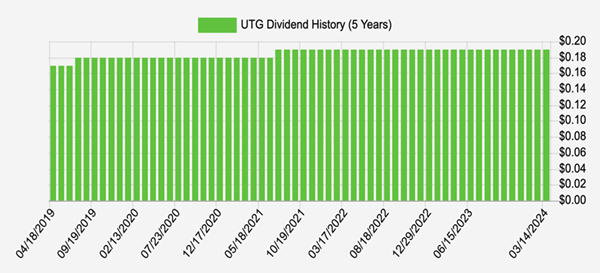

Reaves Utility Income (UTG) will benefit as well. UTG yields even more today—8.6%—and this monthly payer also dishes the occasional raise:

UTG Pays 19 Cents Per Month, Every Month

Source: Income Calendar

UTG focuses more on “old school” utilities like Duke Energy (DUK) and Southern Co (SO). These stocks tend to pay more than UTF’s infrastructure-focused plays, so UTG can use less leverage (20% versus 30% for UTF) to deliver its elite 8.6% dividend.

UTG unfortunately does not trade at a discount, but this is nothing new. The fund frequently trades at premiums to its NAV. In recent years its premium has wandered as high as 13%!

Nope, we’re not interested in paying $1.13 for $1 in assets. But we’ll take the $1 for $1 UTF “fair trade” available today. Especially at this near-term top in long rates, which should be a nice tailwind for the underlying holdings of UTG.

Really, lower rates are going to lift both UTF and UTG. These funds have minimal overlap in their holdings. It’s OK to buy both excellent 8%+ payers today—as long as you don’t mind the monthly payments!

And believe it or not these 8%+ dividends look a bit light in comparison with my favorite monthly payers. We’re talking 9%+ dividends that are dished every single month.