I’m sure you’ve noticed that the media has been fretting about a selloff in the last few weeks. But the S&P 500 is still up a lot on the year.

Even so, there is cause for concern about overvaluation, as the market’s current gain is equal to a whole year’s worth of historical returns, on average. But the softness we’ve seen lately, combined with the deep April selloff, do suggest that while stock valuations are high, we’re not in a bubble—at least not yet.

Which brings me to our beat at my CEF Insider service—closed-end funds (CEFs), many of which yield 8%+. In light of the market’s strong run, there are many more overbought CEFs than usual. It’s critical that we do not let these paupers’ high yields distract us from this.

Below we’ll look at three CEFs with way overinflated premiums to net asset value (NAV, or the value of their underlying portfolios). All three need to be sold now, if you hold them, or avoided if you don’t.

Keep in mind, though, that these aren’t bad funds—in fact, they’re all worth putting on your watch list. It’s just that their prices are way too high right now.

“Overcooked” CEF No. 1: Gabelli Utility Trust (GUT)

You might recognize the Gabelli Utility Trust (GUT), as we discussed this fund’s absurd premium in an August 4, 2025, Contrarian Outlook article. Then, it had a 96.2% premium. So investors were paying 2X GUT’s assets just to get in!

They essentially still are. As I write, the premium has “narrowed” to 89.6%, but that’s still ridiculous. The fund’s market price–based return has also slipped slightly since then, while the S&P 500 gained.

This suggests more investors are realizing that GUT, which holds major US utility stocks, like Duke Energy (DUK), NextEra Energy (NEE) and Wisconsin-based WEC Energy (WEC), would drop if its premium vanishes.

Could that happen?

Well, utilities are getting a lot of attention as a way to play AI’s voracious appetite for electricity. That makes them a crowded trade, so any softness in the AI story (even temporarily) could see them—and GUT’s lofty premium—tumble.

That’s too much risk for us to take, even with GUT’s steady, and monthly paid, 10% dividend. Let’s hold off on this one until after its stratospheric premium returns to earth.

“Overcooked” CEF No. 2: PIMCO Strategic Income Fund (RCS)

Another corner of the market that’s gotten more attention is non-sovereign debt, such as corporate bonds. This explains why the PIMCO Strategic Income Fund (RCS) has seen its market price–based return soar in the last four months, boosting its premium.

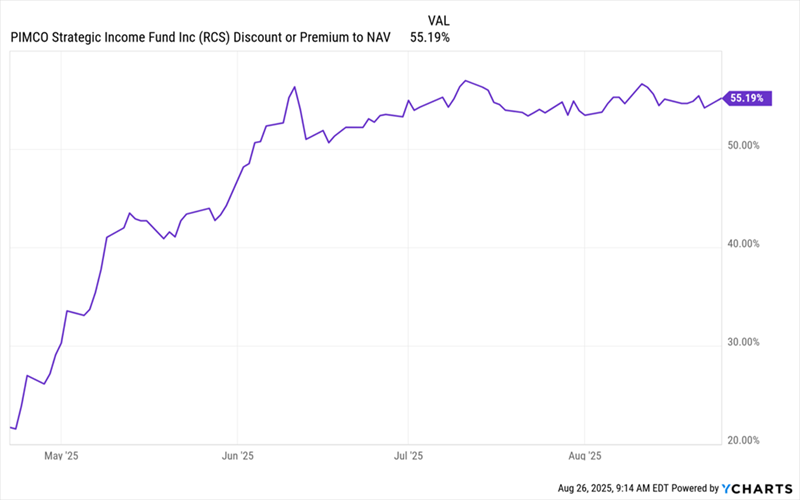

RCS’s Premium Soars—Then Levels Off

During the April selloff, RCS was trading at a bit above a 20% premium. That’s very pricey for a bond fund, but this 7.3% yielder now trades at a premium that’s more than double that! Note also how its premium has not widened since June.

That’s a sign that RCS’s premium might drop, taking unrealized investor profits with it. It wouldn’t be the first time: Look at what happened to the premium at the start of 2025.

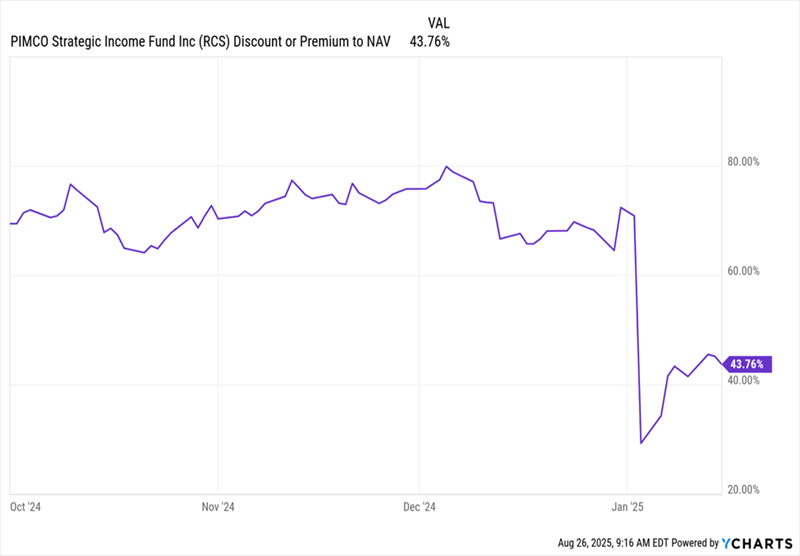

Investors Hit the “Reset” Button on RCS’s Premium …

After months of moving in a narrow range, the fund’s premium tanked, turning what was a tidy profit into a sudden loss:

… Wiping Out Months of Profits

This kind of move is likely to reoccur when investors realize this fund, at a still-absurd 55% premium, remains a “mini-bubble” all its own.

“Overcooked” CEF No. 3: Guggenheim Strategic Opportunities Fund (GOF)

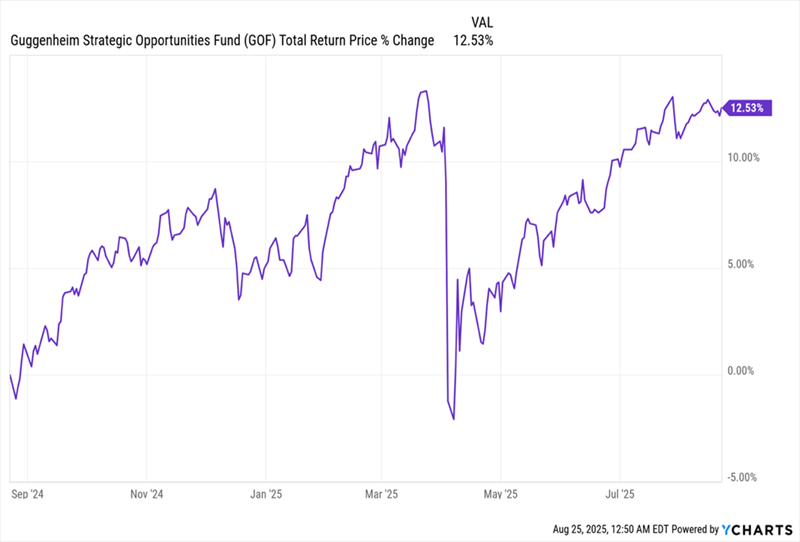

Finally, there’s the Guggenheim Strategic Opportunities Fund (GOF), a corporate-bond fund that’s had an eventful 2025, with big gains, losses, and big gains again.

GOF’s Window of Opportunity Is Gone

Buying this fund during the April selloff made sense, but a lot of funds made sense during the selloff! Now, GOF’s 29.1% premium, while smaller than some extreme mispricings we’ve seen in 2025 (it was above 40% in March) is cause for worry. This chart explains why.

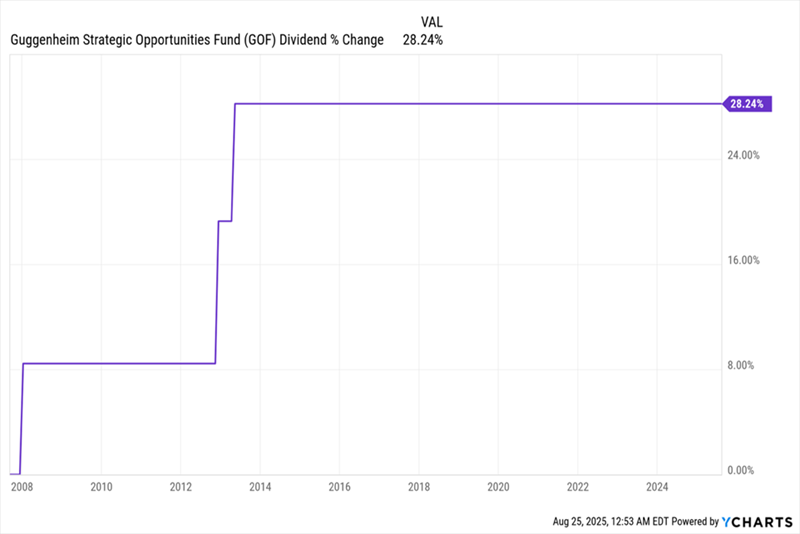

Big Payout Gains Then = Risk Now

GOF has raised payouts three times in its history, impressively doing so during the Great Recession of 2007 to 2009 and twice again in the mid-2010s. The market expects GOF to keep—and indeed grow—that high payout.

After all, that’s what GOF has done for its entire history. Plus, its total NAV return over the last year is 15.5%—surely more than enough to maintain payouts.

Except it isn’t. With a 14.7% yield, it looks like GOF is paying out less than its profits to shareholders. But that 14.7% is based on its market price. What matters is the yield on NAV, since how much management needs from its portfolio to sustain its payout.

And with the fund’s big premium, GOF is paying out a 19% yield on NAV. So even with a 15.5% return over the last year, the fund isn’t earning enough to cover its dividend.

In other words, a cut is likely. And while that wouldn’t be the end of the world (a lot of CEFs make minor payout cuts here and there), there is a risk that GOF shareholders aren’t pricing that in. The result could be a big selloff when it arrives.

5 CHEAP CEFs Dropping 10.2% Dividends (Paid Monthly)

The great thing about CEFs is that the whole sector is off the mainstream crowd’s radar, so we’ve got plenty of bargains to pick from, even in a “pricey” market like today’s.

I’ve got 5 for you that are my top bargain picks now. They pay a 10.2% dividend, on average. They’re ridiculously undervalued (positioning us for gains to go along with our big dividends) and, best of all, they pay dividends monthly.

I’ve prepared a FREE Special Report revealing their names and tickers, and I’m ready to share that with you now. Simply click here and I’ll take you to a private briefing with more details on these stout monthly payers—and our full CEF strategy, too.