ETFs, or exchange-traded funds, are for suckers. There is no reason for any savvy income investor to get wrapped up in this “$3.4-trillion obsession.”

Why do I say $3.4 trillion? Because that’s how much Americans have tied up in them. But there are better ways to buy the same types of stocks, and shortly we’ll highlight three ETF replacements you can buy just as easily for yields up to 7.5%.

Wall Street is (of course) happy to play along with the ETF craze, cranking out fund after fund to give folks their fix—some so “out there” they track wheat futures, casino stocks, even companies that aim to curb obesity.

It’s true! That last one’s called the Obesity ETF, with the catchy ticker SLIM.

If you want a true sign ETFs are overdone, consider this: back in 2007—just 12 years ago—there were 290 ETFs out there.

Today? More than 5,000—17 times more!

Of course, many of these ETFs were slapped together to let the fund companies cash in on the fad of the day.

The result? Way too many endanger your dividends with collapsible payouts, stomach-churning volatility and portfolios so frothy they’re “hardwired” for deep plunges when markets pull back.

Let’s dive into the three high-risk ETFs you must dodge now. After each one, I’ll show you a high-yield closed-end fund (CEF), with dividends ranging from 5% all the way up to 7.5%!

Deadly ETF No. 1: “A Perfect Setup for Massive Losses”

Let’s start with one of today’s hottest trends: the rise of automation and artificial intelligence. It’ll likely come as no surprise that there’s an ETF for that: the iShares Robotics and Artificial Intelligence ETF (IRBO).

Too bad the negatives start piling up right away, especially if you need income. IRBO yields a pathetic 0.7%, so dropping $100,000 into will only get you $700 a year! That’s so sad it isn’t worth spending another second on.

IRBO has beaten the SPDR S&P 500 ETF (SPY) since inception, but that outperformance is marginal (and that’s being generous!). And check out the wild volatility you would’ve had to stomach:

IRBO Crashes, Then Reboots

As you can see above, IRBO is new—it’s only been around 10 months—and it’s already weighed down by stocks with zero profits, like Snap (SNAP), Cloudera (CLDR) and Lattice Semiconductor (LSCC). Throw in a portfolio with a P/E ratio near 21, and you’ve got a perfect setup for massive losses in the next correction.

So let’s sidestep IRBO and go with a tech-focused CEF that crushes it on every point that matters …

High-Yield CEF Pick No. 1: A Monthly 5% Dividend From Tech

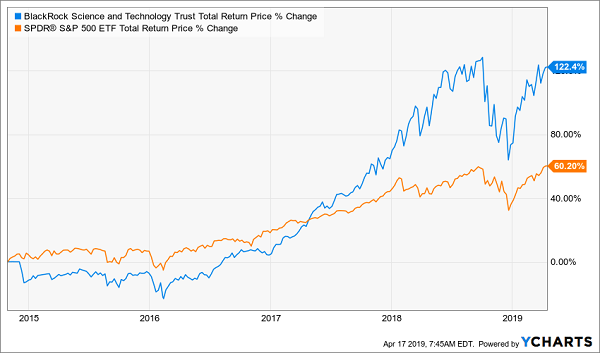

That would be the BlackRock Science and Technology Trust (BST), with a gaudy 5.3% dividend paid monthly.

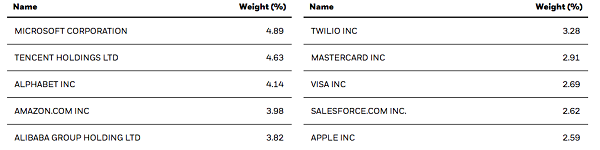

Instead of gambling on which small cap may catch the next wave, BST holds giants that will simply buy out these innovators, or wipe them out with their own tech:

A Who’s Who of Tech Dominators

Source: Blackrock.com

Now let’s talk outperformance—I think you’ll agree that this gap is anything but marginal.

BST 1, S&P 500: 0

BST may look expensive, trading at a 5.5% premium to net asset value (NAV, or the value of its stock holdings). But get this: investors have happily shelled out a 14% premium—$1.14 for every $1 of assets—for this fund in just the past year.

A return to that level (a certainty, in my view) would give us 8% price upside, not including any gains BST’s portfolio throws our way.

Deadly ETF No. 2: “A Grab Bag of Low-Yielding Stocks”

Whenever I see an investment trying to profit from Millennials, I roll my eyes: for one, the oldest Millennials are 37 years old! Not exactly young hotshots anymore.

What’s more, this generation has a wide backstory: some are urban; some are rural; some are desperate to buy a house; others are happy to rent. I could go on.

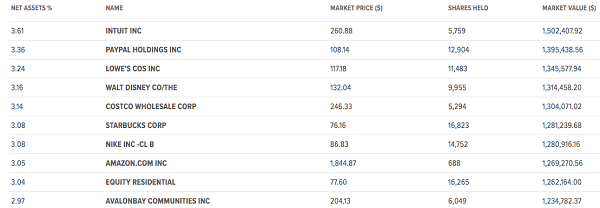

Even so, the Global X Millennials Thematic ETF (MILN) gives it the old, er, college try with this grab bag of low-yielding stocks:

Is This Where the Millennials Are?

Source: globalxfunds.com

As you can see, this is just a list of retail stocks, except for Intuit (INTU), a maker of tax-planning software (if you can see how that ties to Millennials, you’re doing better than me) and two real estate investment trusts (REITs) with apartments in big cities: AvalonBay Communities (AVB) and Equity Residential (EQR).

By far the worst part is the 0.5% dividend. And you don’t even get to keep it! It’s cancelled out when management takes its fee (also 0.5%) out of the fund.

Here’s the bottom line: if you’re going to invest in large-cap stocks, skip the shopworn themes and buy a well-run, diversified equity CEF. You’ll get a higher yield and a pro—who charges a lot less than your dividend—working for you.

Which brings me to …

High-Yield CEF Pick No. 2: A “Superstar” 6% Dividend on the Cheap

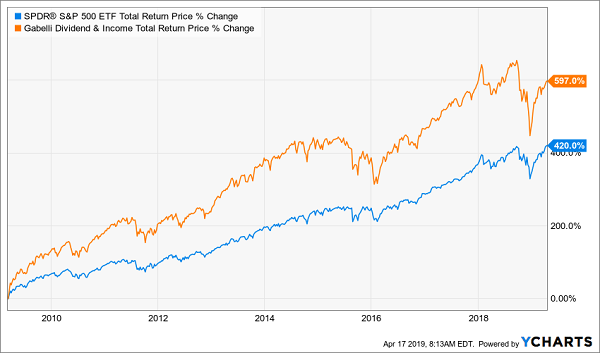

One of your best stock-CEF bets now is the Gabelli Dividend & Income Trust (GDV), run by famed value investor Mario Gabelli, who charges us a 1.35% fee.

That may sound high, but I’ll happily pay it for a rock star like Gabelli, who’s snapped up bargain after bargain since the Great Recession, driving GDV to a massive return net of fees:

Gabelli Earns His Keep

One thing I love about Gabelli is that he doesn’t front-run the latest fad. Instead, he quietly runs plain-vanilla income go-tos like GDV, the Gabelli Equity Trust (GAB) and the Gabelli Utility Trust (GUT).

As I write, GDV trades at an 8.4% discount to NAV, below its 7.2% average in the last year and miles below the 2.4% it topped out at in that time. So you’ve got lots of upside potential and downside protection here.

Finally, the dividend, an outsized 6.1% payout you’ll also pick up every month.

Gabelli’s Armor-Plated Cash Stream

Source: CEFConnect.com

I think the next move here is obvious.

Now let’s move on to our last ETF laggard—and a CEF with a hefty (and safe) 7.5% cash payout!

Deadly ETF No. 3: Real Estate, the Wrong Way

With the Federal Reserve set for zero rate hikes in 2019, look for REITs to gain as the year rolls on.

Why? Because 10-year Treasuries still yield a lame 2.6%. Why settle for that when you can pull in 4% with the ultra-popular Vanguard Real Estate ETF (VNQ)?

Trouble is, not all REITs will benefit equally, which is why buying an ETF is a mistake. When it comes to REITs, there are really only two ways to go:

- Manage your REIT portfolio yourself, or …

- Hire a pro who can steer you toward the fastest-growing REITs (while sidestepping the dogs).

VNQ is the worst of all worlds: it blindly tracks the MSCI US Investable Market Real Estate 25/50 Index, with no active manager around to make a quick change if things sour for one or more REIT sectors.

Consider retail REITs, which sit square in the path of Amazon.com (AMZN). VNQ has 14% of its portfolio mired in this sector. Look at how the fund’s third-biggest holding, mall owner Simon Property Group (SPG), has yanked down its return:

An Anchor VNQ Can’t Cut Loose

I think the downside here is pretty clear. And it gives us a perfect segue to our third CEF.

High-Yield CEF Pick No. 3: 1,500% Gains, 7.5% Dividend

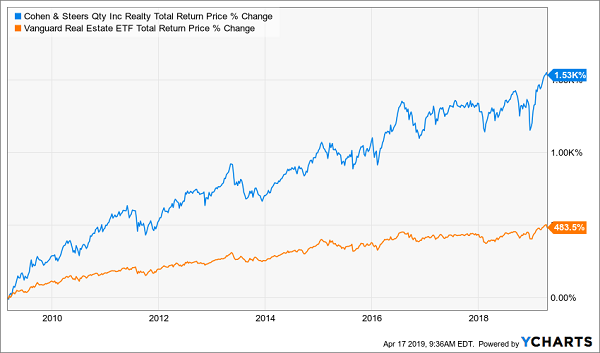

I don’t know why anyone would touch VNQ when they could buy the Cohen & Steers Quality Income Realty Fund (RQI), which has crushed its ETF cousin since the Great Recession:

The Power of Savvy Management

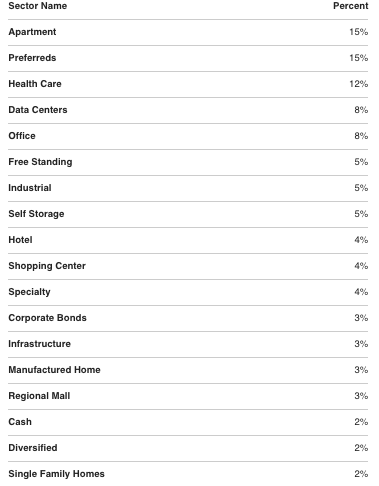

RQI is run by a trio of managers with 72 years of REIT expertise between them, and that shows up in the fund’s portfolio, which is tilted toward fast-growing areas like apartments, health care and data centers (which are my favorite “pick-and-shovel” play on artificial intelligence, by the way).

Shopping malls? They’re way down the list:

RQI’s Flexible Portfolio

Source: cohenandsteers.com

The kicker? You can grab RQI at a 9% discount to NAV—a steal for a fund whose discount has almost completely slammed shut (to as little as 2%) in the past year.

NEW: 5 “Pullback-Proof” Dividends Paying Up to 8.5%

Disasters like the three ETFs I just showed you are exactly why I put together my 5-stock “Pullback-Proof” portfolio, which I’m going to GIVE you today.

The 5 picks inside this breakthrough portfolio deliver two things pretenders like IRBO, MILN and VNQ never could:

- Rock-solid (and growing) 7.5% average CASH dividends and …

- A share price that doesn’t crumble beneath your feet while you’re collecting these massive payouts. In fact, you can bank on 7% to 15% yearly price upside from these 5 “steady Eddie” picks.

And as I said off the top, one of these titans pays a SAFE 8.5%!

Think about that: buy this incredible stock now and every year nearly 9% of your original buy boomerangs straight back to you in CASH.

If that’s not the definition of safety, I don’t know what is.

These 5 stout stocks have sailed through meltdown after meltdown with their share prices intact, doling out huge cash dividends the entire time. I’m ready to share each one of them with you right now.

Editor’s Note: I’ve seen these 5 picks and I think they’re Brett’s best yet. But they have been moving up in the latest upswing (with their dividend yields slowly ticking lower as they do). If you want to grab the biggest payouts (and upside) here, you need to move now.