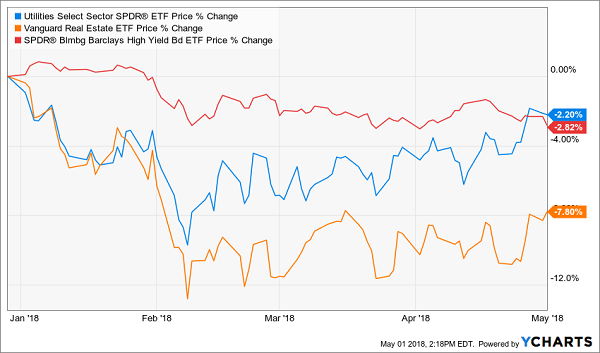

It’s been a rough year thus far for many high paying investments. From utilities to REITs (real estate investment trusts) to high yield bonds, many are getting crushed as rates rise:

Why High Yield Shortcuts are for Losers

But we don’t dumbly buy these indices. We cherry pick the very best of the high yield lot. After all, there is always a bull market somewhere (or in something). And this is where we should invest for big dividends and price upside to boot:

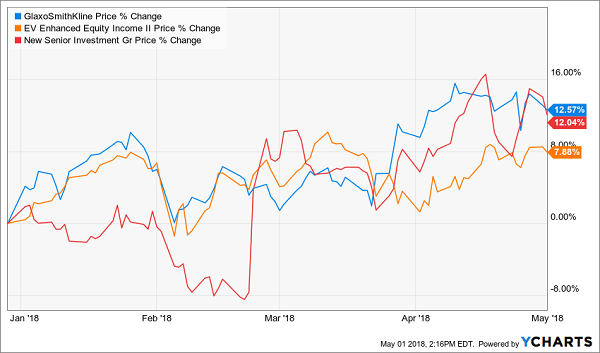

The Strongest Names in High Yield (Year-To-Date)

So let’s discuss these “dividend market leaders” and see why they are acting strong while their cousins make interest rate excuses. All pay 5% to 12% dividends and have additional price upside to boot.

(Remember, when high yield markets turn around, we should first consider the stocks that were acting the strongest when times were tough. Here are three.)

GlaxoSmithKline (GSK)

Dividend Yield: 5.4%

YTD Gains: 13%

GlaxoSmithKline (GSK) is a U.K.-based pharmaceutical stock that has earned a place among healthcare’s blue-chip elite. This is the company behind asthma treatment Advair – one of the top dozen or so best-selling pharmaceutical products of all time – as well as Paxil, Valtrex, Avandia and Zantac.

The company’s success in 2018 has largely come on the back of its fourth-quarter earnings results, released in early February. GSK put up a 72-cent-per-share profit to beat estimates by 3 cents, and revenues grew 4% to $10.3 billion, topping expectations of $9.9 billion. The biggest fireworks came from its New Pharmaceutical and Vaccine products division, which jumped 51% thanks to success in HIV, respiratory and meningitis-prevention drugs.

But GSK also has made a few moves that set it up for continued success for the rest of the year.

GlaxoSmithKline in March took full control over a consumer health joint venture with Novartis (NVS), buying out the latter’s remaining 36.5% stake for $13 billion – a move that was met with optimism by shareholders in both companies. The joint venture includes products such as painkiller Panadol and sensitive-tooth toothpaste Sensodyne.

And just days ago, GlaxoSmithKline hired Kevin Sin away from Roche’s (RHHBY) Genentech unit. Sin has been a part of more than 100 healthcare deals during his career, says Reuters, and is expected to lead Glaxo on its own hunt for new products. That, combined with increased spending on R&D – the company’s $4.5 billion spend was its most dedicated effort in a decade – should do wonders for its pipeline.

One final note: GSK often gets flack for its seemingly untenable payout ratio. As a percentage of earnings, 180% is certainly worrisome – but understand that as a percentage of cash (which actually pays the dividends), it’s just under 85%. That doesn’t leave a ton of room for hikes, but it does put the dividend’s safety in a much kinder light.

Eaton Vance Enhanced Equity Income Fund II (EOS)

Distribution Rate: 6.4%

YTD Gains: 8%

The Eaton Vance Enhanced Income Fund II (EOS) was built for markets like this.

In a nutshell, EOS invests in large- and mid-cap stocks with an eye toward growth and financial stability. While that bent typically would result in a sub-2% yield for a bland index exchange-traded fund, this closed-end fund also writes calls to generate additional income – a strategy that can excel in a flat market.

Right now, it’s putting other growth ETFs to shame.

Eaton Vance’s EOS Is Head-and-Shoulders Above the Competition

The management team of Michael Allison, Lewis Piantedosi and Yana Barton invest in (and trade options against) roughly 60 stocks, including current top holdings Microsoft (MSFT), Apple (AAPL) and Alphabet (GOOG, GOOGL). Trading against individual stocks rather than a full index (again, like several passive options-trading ETFs) allows EOS to be more tactical, grabbing premium when it’s there and avoiding selling covered calls when it might be detrimental to performance.

EOS actually sports long-term outperformance against the S&P 500, gaining about 9.4% annually to the index’s 9.23%. But this CEF has really added some distance over the past year, racing off to 29% gains against the market’s 18%.

In other words, this is far from just a yield play – EOS packs a growth punch, too.

New Senior Investment Group (SNR)

Dividend Yield: 12.1%

YTD Gains: 12%

New Senior Investment Group (SNR) is the quintessential Baby Boomer play. And make no mistake: You want exposure to this American generation, which will send 10,000 of its members into retirement age every day through 2032.

This senior-housing specialist owns 133 properties in 37 states, broken down into 102 independent living facilities, 30 assisted living/memory care property and 1 continuing care retirement community property. This REIT also has a triple-net lease element; 53 of its properties (mostly IL facilities) are in this “Holy Grail” situation in which tenants are on the hook for real estate taxes, insurance and maintenance. This model is simpler and more stable, making for more predictable revenues and income.

Better still, SNR is the only such REIT that is completely private-pay in nature, which means it doesn’t need to worry about changes to government programs.

Why SNR has outperformed this year, however, is complicated.

The company jumped after its Q4 and full-year earnings report in February, but not because of exceptional performance. In fact, adjusted funds from operations (AFFO) declined by 11% to 24 cents per share, and total same-store cash net operating income (NOI) only improved 1%.

What did it was this little excerpt from the same report: “… the Company’s Board of Directors has been exploring strategic alternatives to maximize shareholder value.” Typically, this is corporate speak for “looking for a buyer,” and adds the potential for an additional M&A pop in SNR’s future.

It’s clear that New Senior Investment is running into some operational headwinds despite the rosy narrative. The newfound possibility of a buyout may help prop up shares and even give it a final boost should management strike a deal … but be wary of the potential downside should SNR’s “exploring” lead to nothing.

Learn How to Live Off Dividends Forever – for Free!

Each of these picks features the high yields you need in retirement that ensure you can pay your monthly bills and keep the gravy train rolling long after you’ve stopped collecting a paycheck.

But what none of these picks feature is the consistent dividend growth you need to make sure those large dividends don’t lose their value against the relentless pace of inflation. In fact, as things stand, your purchasing power from the income in all three of the aforementioned stocks is assured to go down every year.

That won’t get you through retirement. You need high yields, dividend growth and capital appreciation – the “triple threat” you can find in the stocks I explore in my 8%-yielding “No Withdrawal” retirement portfolio!

My “No Withdrawal” portfolio ensures that you won’t have to settle during the most important years of your life. I’ve put together an all-star portfolio that allows you to collect an 8% yield, while growing your nest egg – an important aspect of retirement investing that most other strategies leave out.

The high-yield world is a mess right now, with REITs, BDCs and CEFs all filled with “dividend landmines.” That’s why I’ve spent months doing the necessary research to weed out these yield traps and identify the few legitimate opportunities that won’t collapse under the weight of their own payouts in just a year or two. The result is an “ultimate” dividend portfolio that provides you with …

- Rock-solid yields of 6%-8% … and in a couple of cases, double-digit payouts!

- The potential for 7% to 15% in annual capital gains.

- Robust dividend growth that will keep up with (and beat) inflation.

This portfolio will let you live off dividend income alone without ever touching your nest egg. That means never having to worry about how you’ll pay your monthly bills, and never having to worry about wrecking your retirement account if disaster strikes.

Don’t live month to month on 3%-4% portfolio returns and Social Security checks. You’ve worked too hard to settle for less when it matters most. I want to show you how to invest intelligently and collect big, dependable dividend checks that will let you see the world and live in comfort for the rest of your post-career life.

Let me help you reach the retirement you deserve! Click here and I’ll provide you with THREE special reports that show you how to build this “No Withdrawal” portfolio. You’ll get the names, tickers, buy prices and full analysis of their wealth-building potential – and it’s absolutely FREE!